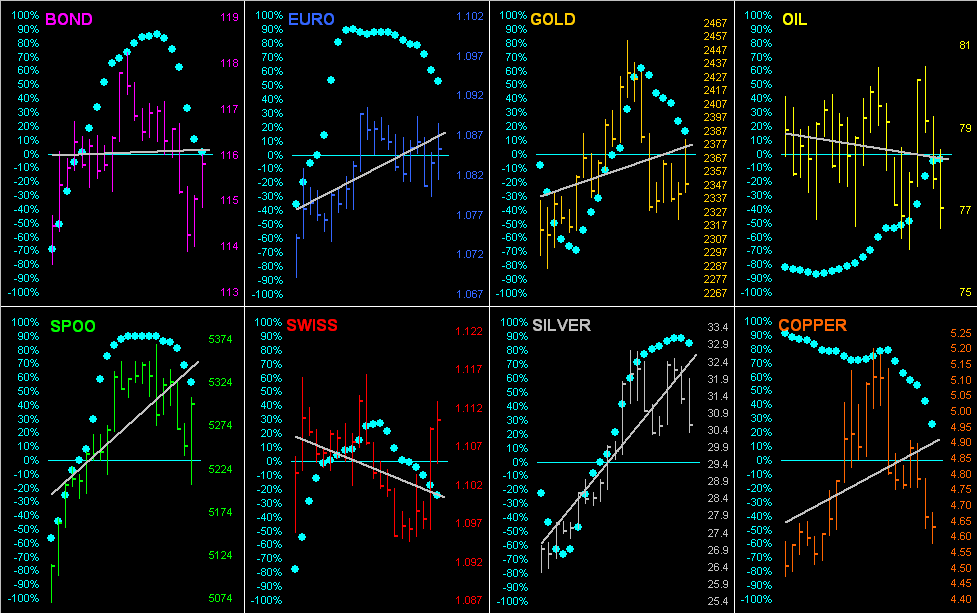

The two-day BEGOS Market’s stint continues. At present we’ve the Euro, Swiss Franc, Gold and Copper above their respective Neutral Zones for the session; none of the other BEGOS components are below same, and volatility (given two days of movement) is moderate-to-robust, both the Swiss Franc and Copper having traced in excess of 100% of their EDTRs (see Market Ranges). Gold has regained firmness this week, albeit not enough to change the more near-term negative nature of the weekly technicals; (more on that in tomorrow’s 764th consecutive edition of The Gold Update). The Spoo is up such that the S&P 500 would (at this moment) open at an all-time high of 5540. And the Econ Baro concludes its down week with June’s Payrolls data.

Mark

Mark

04 July 2024 – 08:16 Central Euro Time

Given the StateSide holiday, the BEGOS Markets are in a two-day session (for Friday Settle) with the Swiss Franc at present above its Neutral Zone whilst Silver is below same; not surprisingly, volatility is light, the Spoo having thus far just traced 13% of its EDTR (see Market Ranges). Looking at Market Rhythms on a purely swing basis, our 10-test group for most consistency is currently the Euro’s 2hr MACD, Oil’s 60mn Parabolics, and Silver’s 15mn Moneyflow; for the 24-test group, we’ve two for the Spoo by its 4hr Moneyflow and daily Parabolics. With the S&P 500 at an all-time closing high (5537), its futs-adj’d “live” P/E is now 43.3x. Tomorrow is a full trading day for US equities, preceded for the “free-fall” Econ Baro by June’s Payrolls data.

03 July 2024 – 08:39 Central Euro Time

The Swiss Franc is at present below its Neutral Zone for today; above same are both Silver and Copper, and BEGOS Markets’ volatility is mostly light ahead of early closures for the Spoo and S&P 500. The latter settled above 5500 for the first time yesterday, albeit two recent days posted intra-day highs above that level: the “live” (futs-adj’d) P/E of the S&P is 43.0x with Q2 Earnings Season commencing next week; the S&P yields 1.324% versus the US 3mo T-bill’s annualized 5.228% Gold is basically staying buoyed above its key Market Profile support of 2338 even as near-term technicals suggest lower prices. The Econ Baro receives a bevy of metrics today: June’s ADP Employment data and ISM(Svc) Index, May’s Trade Deficit and Factory Orders, and because of tomorrow’s StateSide holiday, last week’s Jobless Claims too are squeezed into the mix.

02 July 2024 – 08:39 Central Euro Time

The Swiss Franc is at present the only BEGOS Market outside (below) its Neutral Zone for today; session volatility is quite light. The firmest correlation amongst the five primary BEGOS components is one which is positive between Gold and Oil, although by Market Trends, the former’s linreg is negative whilst the latter’s is positive; (the correlation benefits from both markets being well up from their lows of a week ago, however we remain more attuned to Gold slipping near-term rather than Oil breaking higher). Still, by Market Values, Gold is (in real-time) -43 points below its smooth valuation line whilst Oil is +5.13 points above same. Nothing is due today for the Econ Baro ahead of a bunching of incoming metrics tomorrow for the shortened equities session ahead of Thursday’s holiday.

01 July 2024 – 08:43 Central Euro Time

The year’s second half starts with both the Euro and Oil at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is moderate within the context that by Market Ranges, EDTRs have been narrowing. The Gold Update cites confirmation of the yellow metal’s weekly parabolic trend having flipped from Long-to-Short, the typical move lower from here (strictly by past average adversity) suggesting a meeting with the 2247-2171 structural support zone; Gold by Market Values is (in real-time) -42 points below its smooth valuation line; but by Market Magnets, price appears poised to eclipse up through its Magnet: thus we don’t sense an imminently stark move lower; still, near-term Gold technicals have a negative bent. For the Econ Baro today we’ve June’s ISM(Mfg) Index and May’s Construction Spending.

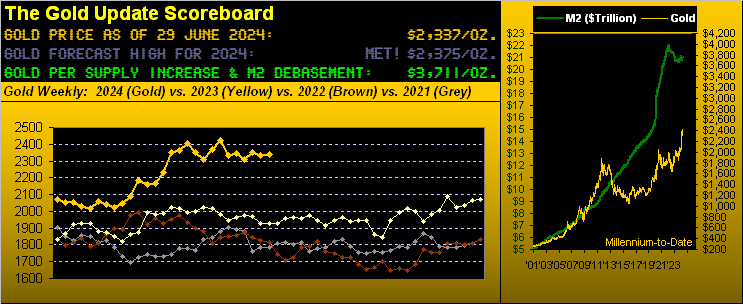

The Gold Update: No. 763 – (29 June 2024) – “Gold Looks to Support as Our Key Trend Goes Short”

“And so we are halfway.” In this case ’tis not Fräulein Irma Bunt to James Bond (in the guise of Sir Hilary Bray) whilst walking upon the snowy flanks of Switzerland’s Schilthorn –[O.H.M.S.S, UA, ’69], but rather for our purposes the mid-point of 2024’s trading year. (Yes, we are aware that the precise mid-point is not until this Tuesday’s settle when with 126 trading days in the books there’ll remain 126 in the balance). Nonetheless, ’tis the end of June and thus time for our monthly view of it all.

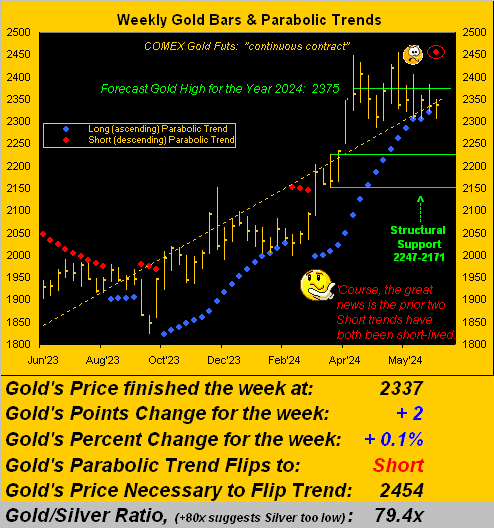

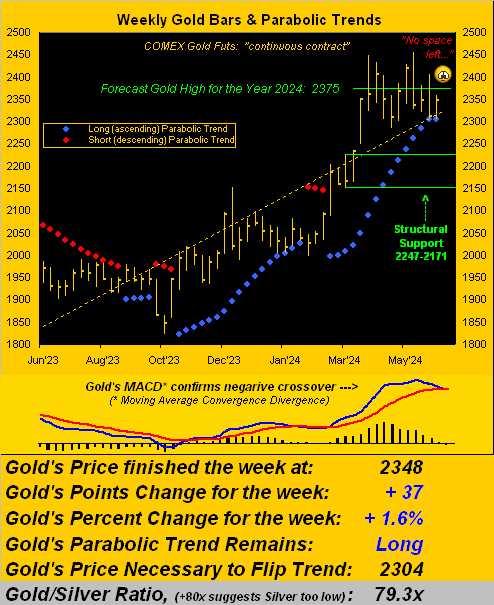

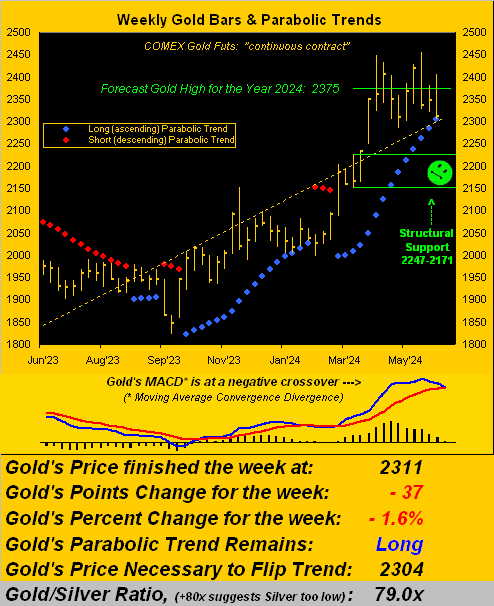

And bang on time in stride with our negative near-term bent for Gold — whilst settling yesterday (Friday) at 2337 for a whopping weekly gain of +2 points — on Wednesday, Gold’s anticipated damage was done as price broke below 2320 such as to flip our key 16-week parabolic Long trend now to Short. (Expected as ’twas, ’twasn’t a beautiful thAng, even as we then “X’d” [@deMeadvillePro] notice of said flip). Regardless, as scored by Chicago back in ’69: ![]() ““Where do we go from here?” ”

““Where do we go from here?” ”![]()

‘Course, you regular readers already know the answer to our musical query. For waiting in the wings as herein depicted via recent missives is Gold’s 2247-2171 structural support zone. Below ’tis with the weekly bars from a year ago-to-date. And encircled therein is the rightmost red dot heralding the start of the new parabolic Short trend:

Specific to the Econ Baro, ’twasn’t all bleak last week. The Chicago Purchasing Managers’ Index for June — whilst still in net contraction for 21 of the past 22 months — nonetheless improved to 47.4, its best reading since that for November of last year; (yet a reading below 50 still signifies manufacturing contraction). Too, Personal Income for May increased +0.5%, tying it for the second-best increase across the past 12 months. But is that inflationary, (nudge-nudge, hint-hint, wink-wink, elbow-elbow…)

Hardly inflationary has been Silver’s rise to the top of our BEGOS Market Standings year-to-date. Best of the bunch as she is, Sister Silver remains cheap! The Gold/Silver ratio is now 79.4x: but the century-to-date average is 68.3x; were Silver thus priced by that yardstick today (just in case you’re scoring at home), rather than being now at 29.44, she’d be +16% higher at 34.22.

Then in second spot lies (appropriate verb there) the S&P 500, its being purely herd driven on Investing Age of Stoopid delusion. Cue that recorded in 1929 by Memphis Minnie and Kansas Joe McCoy: ![]() ““When the Levee Breaks” ”

““When the Levee Breaks” ”![]() Remember what also happened that year? When the “Look Ma! No Money!” crash hits, ’twill be pure herd fear, whilst Silver and Gold are held dear:

Remember what also happened that year? When the “Look Ma! No Money!” crash hits, ’twill be pure herd fear, whilst Silver and Gold are held dear:

Thus with half the year gone, in the proverbial nutshell: Gold broadly looks great to go, but near-term technicals initially say no. Either way, we’ll see what shows. Indeed, how much Gold have you got stowed?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

28 June 2024 – 08:36 Central Euro Time

Early on in the final trading day (by months) of the year’s first half, we’ve the Bond at present below today’s Neutral Zone; above same are Silver, Copper and Oil, and volatility is pushing toward moderate. Going ’round the Market Values horn for our five primary BEGOS Markets: in real-time we’ve the Bond as +1 point “high” above its smooth valuation line, the Euro -0.018 points “low”, Gold -41 points “low”, Oil +3.82 points “high” and the Spoo +211 points “high”. The S&P 500 is now 14 consecutive days “textbook overbought” and its “live” P/E is 42.7x. The Econ Baro looks to June’s Chi PMI and revision to UofM’s Sentiment Survey, plus May’s Personal Income/Spending and the “Fed-favoured” Core PCE.

27 June 2024 – 08:37 Central Euro Time

The Euro is at present above today’s Neutral Zone, whereas the balance of the BEGOS Markets are within same; volatility is notably light, with 10 metrics incoming for the Econ Baro over the next two sessions. As “X’d” (@deMeadvillePro) yesterday, Gold’s weekly parabolic trend has provisionally flipped from Long to Short, setting up a test for the 2247-2171 structural support zone; (more on that in next Saturday’s 763rd edition of The Gold Update). The Bond yesterday crossed beneath its Market Magnet, whilst today its MACD has provisionally crossed to negative: we thus anticipate some degree of further Bond selling overing the ensuing days, (albeit Friday’s PCE data is the wild card). Reports today for the Econ Baro include May’s Durable Orders and Pending Home Sales, plus the final revision to Q1’s GDP.

26 June 2024 – 08:41 Central Euro Time

At present we’ve the Bond, Euro, Swiss Franc, and Gold all below their respective Neutral Zones for today; above same is Oil, and volatility is again light. Preferential Market Rhythms displaying the best swing consistency through yesterday are (on a 10-test basis) the Euro’s 15mn EMA, and (on a 24-test basis) both the Spoo’s daily Parabolics and 4hr Moneyflow. For the S&P 500 itself (now 12 consecutive trading days as “textbook overbought”), the futs-adj’d “live” P/E is 42.8x and yield 1.323%; the StateSide 3mo annualized T-Bill yield is 5.223%. Silver’s cac volume is rolling from July into that for September. And the Econ Baro looks to May’s New Home Sales.

25 June 2024 – 08:49 Central Euro Time

Gold is the sole BEGOS Market at present outside (below) its Neutral Zone for today; session volatility is light. Going ’round the horn for all eight Market Trends: the Bond, Swiss Franc, Oil and Spoo are in positive linreg; negative is that for the Euro, Gold, Silver, and Copper. Whilst the S&P 500 yesterday was -0.3%, its MoneyFlow (regressed into S&P points) fell -1.9%, the biased constituent therein being NVDA: per the S&P Valuations and Rankings page, amongst the 10 largest cap-weighted constituents, that company’s “live” P/E settled yesterday at 68.4x, second-highest only to that of LLY at 133.0x. As to the S&P itself, yesterday concluded its 11th consecutive session as “textbook overbought”. The Econ Baro awaits June’s Consumer Confidence.

24 June 2024 – 08:14 Central Euro Time

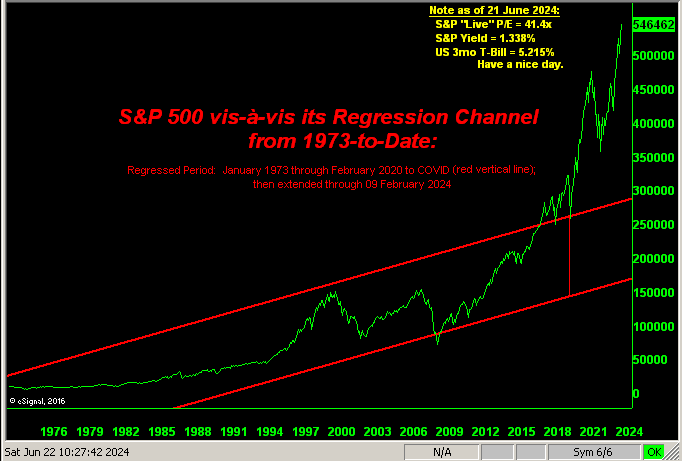

A quiet start to the week as we move toward the mid-point of the trading year: at present, all eight BEGOS Markets are within today’s Neutral Zones, volatility being light. The Gold Update cites the yellow metal’s fundamental grip, albeit the near-term weekly technicals lack strength: penetration of 2320 this week would flip the key weekly parabolic trend from Long to Short. The “live” P/E of the S&P 500 is 41.4x; the Spoo (in real-time) by Market Values is +238 points above its smooth valuation line. Despite much analytical ado about a Bond Market demise, our Bond futs from late April’s lows are nearly +6%, the 21-day linreg firmly positive at Market Trends. Copper’s cac volume is rolling from July into that for September. Nothing is due today for the Econ Baro ahead of 12 incoming metrics for this week, culminating on Friday with the “Fed-favoured” PCE measure of inflaton.

The Gold Update: No. 762 – (22 June 2024) – “Gold Fundamentally Seeking Grip; Technically Still Facing Dip”

Yet how relieved we are that the S&P 500 (red line above) no longer is led by the Econ Baro! Else stocks would have crashed months ago! For as you veteran fans who’ve been with us since the 1990s know, throughout the Baro’s 26 years of existence, it provably had led the S&P 500 through the first 22 of those years, right up to COVID in 2020. Then the Fed flooded the monetary system with $6.7T — an increase to the StateSide liquid “M2” money supply of +43.8% in just two years — and as we’ve previously mathematically demonstrated, the market capitalization of the S&P increased by same: which means (duly acknowledging the benefit of hindsight) that the Fed never really had to print anything! And thus today with the system bloated in equities’ liquidity, the stock market is unable to crash. Reprise: ![]() “We’re in the money, we’re in the money…”

“We’re in the money, we’re in the money…”![]() –[Dance of the Dollars, Dubin/Warren, Gold Diggers of 1933, Warner Bros.] Still graphically, the S&P seems a little bit stretched, what? Hip-hip:

–[Dance of the Dollars, Dubin/Warren, Gold Diggers of 1933, Warner Bros.] Still graphically, the S&P seems a little bit stretched, what? Hip-hip:

Still as regards the stagflating economy, as we herein penned a week ago: “… ’twill be interesting to see just how negative for May the Conference Board’s Leading [i.e. “lagging”] Indicators shall be come next Friday…” followed by yesterday morning’s Prescient Commentary: “The Econ Baro, which has taken a terrific hit this week (indeed across the past two months), looks to May’s … Leading (i.e. “lagging”) Indicators, … [as] potentially quite negative given the dive in the Baro itself.“ That is because throughout the Econ Baro’s history, it regularly leads by weeks the Conference Board’s (with all due respect) misnomered “Leading Indicators” report. Worse, one wonders about the underlying consensii of economic “experts” properly doing their math: when we saw their May expectation for -0.3%, we anticipated a far dire result given the plummeting Baro … and so such came to pass at -0.5%.

Thus cue Captain Obvious: an economy in decline (understatement) upon comforted with a rate cut is a Gold Positive as it enhances the debasement of currency through the “creation of wealth” (i.e. loan-making). So as technically sensitive as the yellow metal may now be, fundamentally we decree: Buy Gold!

“But to buy ‘knowing’ — as you expect anyway — that the price may soon go lower, mmb?“

Squire, recall the late great Richard Russell: “There’s never a bad time to buy Gold.” ‘Tis the perfect place to put excess, unearmarked cash. After all, the Internet’s main sewer line (aka “social media”) goes on ad nauseum about everybody being so rich. Better still, timing the Gold market, (barring your being an in-and-out futures trader), is hardly a critical Gold-owning matter given that price (as historically eventuates) catches up to debasement value, again per the opening Gold Scoreboard.

Or to put it in easier perspective for you WestPalmBeachers down there, let’s quote Jack Lemmon in the role of Hogan from “Under the Yum Yum Tree” –[Columbia Pictures, ’63]:

“Well, it’s an economic necessity. The bank requested that I get rid of excess cash. It’s cluttering up their vaults.”

Yo, you rock, Jack baby: Go for the Gold! (‘Course, ’twasn’t Gold which Jack sought; but we’ll leave that to your viewing curiosity). The point is: as it all goes wrong economically, ’tis good to have a little (or a lotta) Gold.

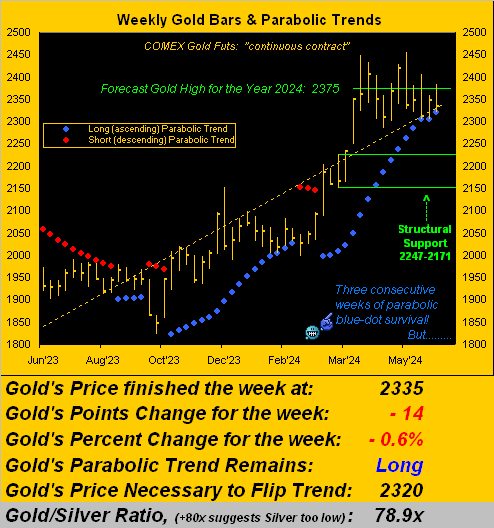

As to Gold’s “now”, we turn to the weekly bars from one year ago-to-date. Note therein the three rightmost blue dots of the parabolic Long trend: price thrice saved by the dots! But now with just a wee 15 points separating price (2335) from its “flip-to-Short” level (2320), to maintain this uptrend that we love, Gold basically needs a straight-up week, else ’tis over. For as sang Martha Davis with The Motels back in ’82: ![]() “Take the ‘L‘ out of ‘Lover’ and it’s ‘over’…”

“Take the ‘L‘ out of ‘Lover’ and it’s ‘over’…”![]() :

:

For the wrap, here is the stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3690

Gold’s All-Time Intra-Day High: 2454 (20 May 2024)

2024’s High: 2454 (20 May 2024)

Gold’s All-Time Closing High: 2430 (20 May 2024)

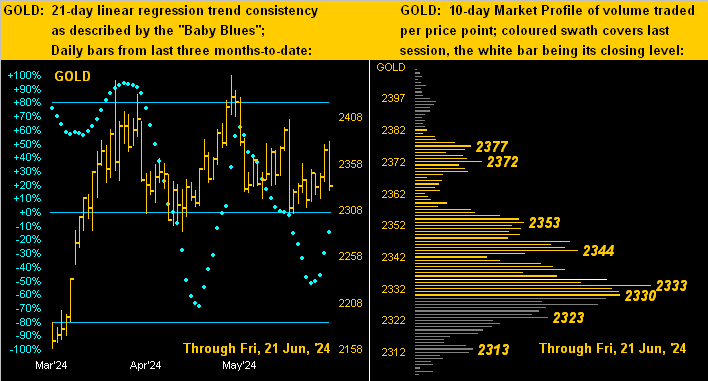

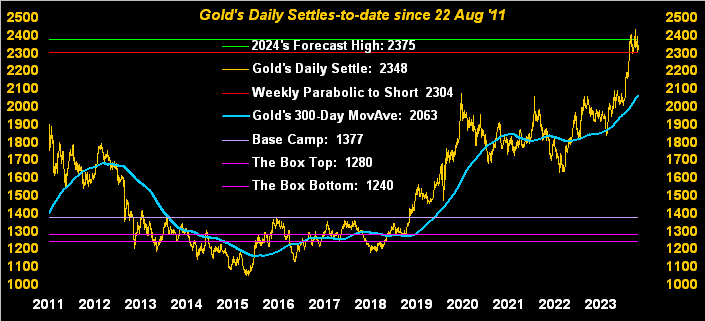

Trading Resistance: per the Profile 2344 / 2353 / 2375 / 2377

10-Session “volume-weighted” average price magnet: 2341: 2341

Gold Currently: 2335, (expected daily trading range [“EDTR”]: 37 points)

Trading Support: per the Profile 2333 / 2330 / 2323 / 2313

The Weekly Parabolic Price to flip Short: 2320

10-Session directional range: down to 2305 (from 2406) = -101 points or -4.2%

Structural Support: 2247-2171

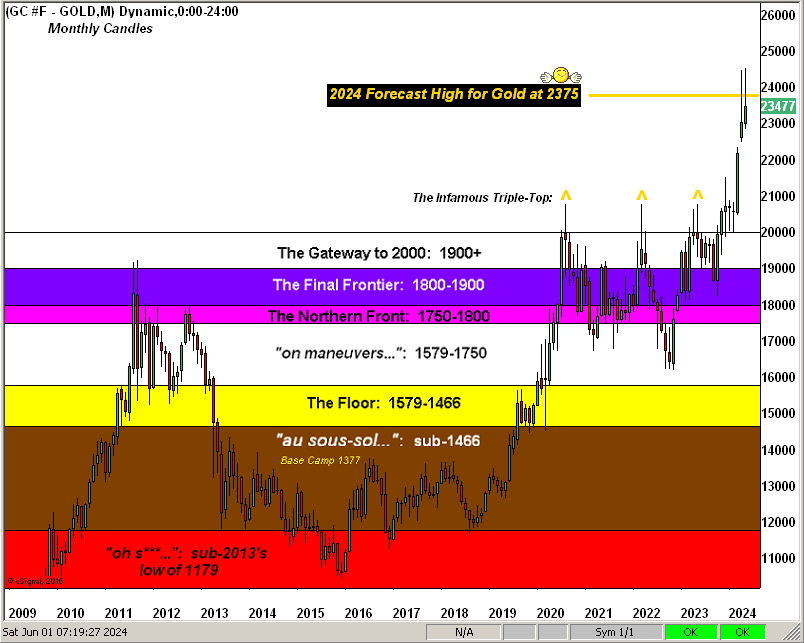

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The 300-Day Moving Average: 2067 and rising

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

So as we glide into next week which culminates with the “Fed-favoured” Personal Consumption Expenditures Price Index, let’s give Jack the final word:

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

21 June 2024 – 08:10 Central Euro Time

Summer’s first full day begins as the week ends wherein we’ve the Euro as the sole BEGOS Market at present outside (above) today’s Neutral Zone; volatility is quite light. Gold has relinquished its positive correlation with the Spoo and is now better teamed with Oil, both exhibiting uptrends these last couple of weeks, albeit Gold’s weekly technicals continue to suggest lower levels near-term: more on that in tomorrow’s Gold Update (No. 762); regardless, both Gold and Silver have broken above their respective weekly highs of the prior week, (even as by Market Trends their linregs remain negative). The Econ Baro, which has taken a terrific hit this week (indeed across the past two months), looks to May’s Existing Home Sales and Leading (i.e. “lagging”) Indicators, the latter potentially quite negative given the dive in the Baro itself.

20 June 2024 – 08:34 Central Euro Time

The two-day session continues for the BEGOS Markets: now we’ve the Bond below today’s Neutral Zone, whilst above same are Gold, Silver and the Spoo; session volatility expectedly has upshifted to moderate. Given the rise in the Spoo from Tuesday, the S&P 500 is poised to open (at this writing) above 5500 for the first time; its futs-adj’d “live” P/E is 42.1x and the yield 1.337%; (three-month U.S. dough pays 5.235%). By Market Trends, four components are in positive linregs (the Bond, Swiss Franc, Oil and Spoo), the other four being negative (Euro, Gold, Silver and Copper). Included today for incoming Econ Baro metrics are June’s Philly Fed Index, May’s Housing Starts/Permits, and Q1’s Current Account Deficit.

19 June 2024 – 08:43 Central Euro Time

Given the StateSide holiday, we’ve a two-day GLOBEX session in progress: at present, all eight BEGOS Markets are within their respective Neutral Zones for the session, and volatility is very light. Looking at Market Rhythms for pure swing consistency, on a 10-test basis the leader is the Euro’s 1hr MACD, whilst on a 24-test basis ’tis the Bond’s 1hr Moneyflow. The primary BEGOS components with the best recent correlation is one that is positive between Gold and the Spoo; however, by Market Trends, Gold is in a 21-day linreg downtrend whereas the Spoo’s is up; regardless, both markets are directionally higher from their lows of eight sessions ago The one metric due today for the Econ Baro is June’s NAHB Housing Index..

18 June 2024 – 08:44 Central Euro Time

Following another record-high day for the S&P 500 (the “live” fut’s adj’d P/E now 42.1x; and by our MoneyFlow page, dough continues to pour into this vastly overvalued Index), we’ve Oil at present the sole BEGOS Market outside (below) its Neutral zone for today; session volatility is mostly light. At Market Values, the insatiable Spoo is (in real-time) +285 points above its smooth valuation line; the other four primary BEGOS components are not trading excessively far from their respective valuation lines; of note therein, Oil yesterday moved above its valuation line, which by rule is a Long signal, whilst at Market Trends, Oil’s linreg looks poised to rotate from negative to positive. For the Econ Baro we await May’s Retail Sales and IndProd/CapUtil, plus April’s Business Inventories.

17 June 2024 – 08:20 Central Euro Time

As the week commences we’ve all eight BEGOS Markets in the red; six of the eight (save for the Swiss Franc and Spoo) are at present below their respective Neutral Zones for today, and session volatility is mostly light, expect for Copper having thus far traced 64% of its EDTR (see Market Ranges). The Gold Update remains remindful of the yellow metal’s near-term negative stance, the weekly MACD having confirmed a downside crossover at the conclusion of last week, price potentially en route to a test of the 2247-2171 structural support zone, (notably should the 2311 low of two weeks ago go). Cac volume for the Spoo is now on September; by its 10-day Market Profile, the Spoo’s most dominantly-traded handles (basis Sep cac) have been 5502, 5492, 5430, 5365 and 5350. 14 metrics come due this week for the Econ Baro, beginning today with June’s NY State Empire Index.

The Gold Update: No. 761 – (15 June 2024) – “Gold Firms; Fed Squirms”

‘Course the above analysis is purely a nearer-term technical read which has historically led to lower price levels. From a broader-term fundamental perspective –certainly so given inflation having just abruptly stopped — the Federal Reserve absolutely must cut its Funds Rate come 31 July, right? A Gold positive, to be sure. And in turn that puts to bed our year-to-date musings for a Fed hike, right? “Curiouser and curiouser!” cried Alice.

Toward economic mold (including more on the sudden absence of inflation), initially we’ve these two sentences from The Federal Open Market Committee’s Policy Statement of 12 June 2024:

- First paragraph, opening sentence –> “Recent indicators suggest that economic activity has continued to expand at a solid pace.

- Second paragraph, closing sentence –> “The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.”

So is the Fed sensing an economic inflection point?

But wait, there’s more: hat-tip Dow Jones Newswires from the ever-ebullient Ayahn Kose (who is the World Bank’s Deputy Chief Economist as everyone knows) came his 13 June prose –> “U.S. growth is exceptional”.

Your having thus absorbed all that parroted wisdom from on high, here’s the Economic Barometer, borne of the math beneath it all. Indeed, ![]() “Go ask Alice…”

“Go ask Alice…”![]() –[Slick/Jefferson Airplane, ’67]:

–[Slick/Jefferson Airplane, ’67]:

And yes, also go ahead and quote one John Patrick McEnroe: “You canNOT be SERious!!” For 29 April-to-date is the worst plunge for such time frame in the Econ Baro’s 26-year history!

To see the Econ Baro so plunge, one ought think the Fed — as it did under Chairman Greenspan pre-“911” both on 03 January 2001 and 18 April 2001 — make an emergency rate cut straightaway. For after all, along with this economic erosion, inflation within the one mere month of May just comprehensively went away! “Don’t delay, cut today!” Yet for some unforeseen reason, the Fed doesn’t see the Econ Baro; neither do CNBS, Bloomy nor Foxy. But in staying the “no inflation” proclamation:

- At the retail level, the Consumer Price Index showed no inflation (0.0%) for May, the 12-month CPI summation now +3.1% (and “core” +3.5%) … courtesy of The Bureau of Labor Statistics;

- At the wholesale level, the Producer Price Index showed deflation (-0.2%) for May, the 12-month PPI summation now +1.9% (and “core” +1.8%) … courtesy of The Bureau of Labor Statistics.

However, recall a week ago also courtesy of The Bureau of Labor Statistics: May’s unexpected upside explosion in Payrolls’ creation was accompanied by an inflationary doubling of the increased pace of Hourly earnings from +0.2% to +0.4%. So fortunately, there’s no inflation, (let alone stagflation), right?

“Well, it is an election year, mmb, and this is the Labor Dept…“

Avoiding any book-cooking notions there, Squire, (this being a financial treatise rather than one political), you know and we know and everyone from Bangor, Maine to Honolulu and right ’round the world knows that hardly has inflation slowed: “Been to the store lately?” Moreover, were Gold to react to inflation having suddenly vanished, price would be rate-cut-influenced moon-bound rather than (at least technically) indicative of moving down.

To be sure, ’tis said the Fed is typically “behind the curve”, indeed today in a state of squirm. For the Fed to opine (at best ‘twould seem) that “economic activity has continued to expand at a solid pace”, we’d say their analysis has (in Formula One lingo) “gone beyond the edge of adhesion and into the Armco!”

And as for the tumbling Econ Baro: ’twill be interesting to see just how negative for May the Conference Board’s Leading [i.e. “lagging”] Indicators shall be come next Friday (21 June). Economic mold, indeed.

Too, there’s earnings mold, our live price/earnings ratio for the S&P 500 settling the week at a historically unsupportable 41.4x. But until real fear hits, everything’s great, right? As is our wont to quip: marked-to-market, everybody’s a millionaire; marked-to-reality, nobody’s worth squat.

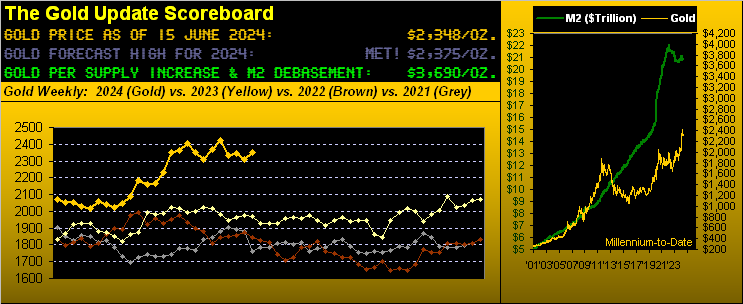

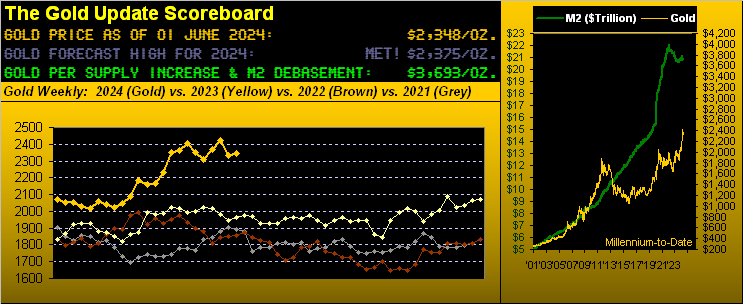

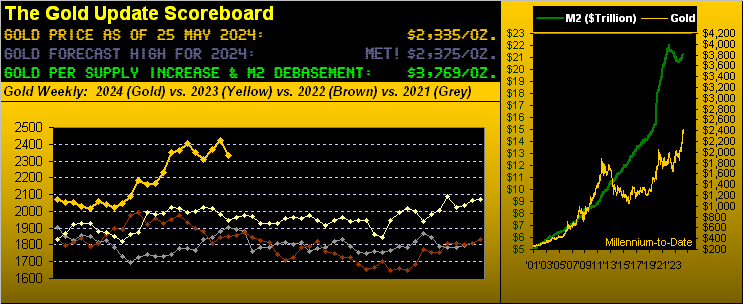

From such mold, back to firm Gold. Whilst price near-term may be a bit challenged, the broader picture remains most positive — perhaps technically too positive — but fundamentally there’s so much currency debasement ground to gain, (our opening Scoreboard valuation of 3690 versus Gold currently just 2348).

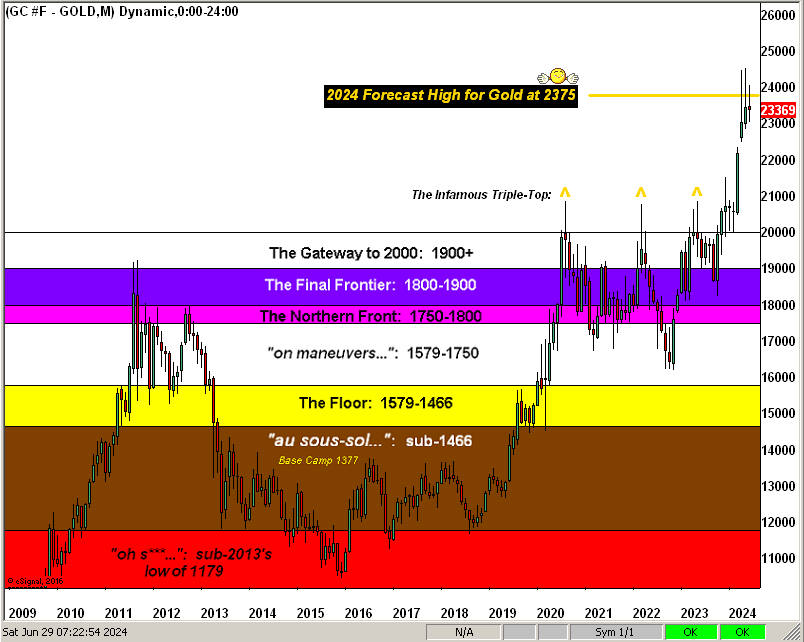

That noted, we go to Gold’s daily closes and 300-day moving average across the past 13 years, (the graphic still remindful of those tiresome 1200s-1400s during the prior decade). Therein, our green-line forecast high for this year (2375) has thus far held reasonably well, notwithstanding the brief, recent spike to 2454. And by this big picture, Gold’s sub-2000 days really do now appear permanently histoire, with an inevitable run to 3000+ in the balance ![]() “As time goes by…”

“As time goes by…”![]() –[Hupfeld ’31 … Wilson, Casablanca, ’42]:

–[Hupfeld ’31 … Wilson, Casablanca, ’42]:

To close, yes the Econ Baro looks terrible, again in its worst plummeting streak we’ve ever recorded. However, perhaps there’s happier news on the horizon: of the 14 metrics scheduled to hit the Baro in the new week, 10 by consensus are expected to have improved period-over-period. ‘Course, to be factored in as well shall be prior period revisions with which to weigh one’s decisions.

But when it comes to increasing one’s Gold buying program, as Bogey said, “Play it again, Sam!”

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

14 June 2024 – 08:37 Central Euro Time

Gold is at present the only BEGOS Market outside (above) its Neutral Zone for today; still, barring a significant up day, Gold shall compete its week with the weekly MACD having confirmed going negative: more in tomorrow’s 761st consecutive Saturday edition of The Gold Update. Session volatility is light; of note however is the Yen (not yet a BEGOS component) having traced 128% of its EDTR (see Market Ranges for those of the other components). Cac volume for the Spoo is beginning to move from June into September with a whopping +65 points of additional price premium: that in turn finds the Sepember cac (in real-time) +259 points above its smooth valuation line (see Market Values). The Econ Baro looks to more inflation information via May’s Ex/Im Prices; too arrives UofM’s Sentiment Survey for June.

13 June 2024 – 08:35 Central Euro Time

Following the somewhat “stubborn-to-cut-Fed” (let alone our year-to-date musings instead about a hike), the Dollar’s furthering a bit of a bid today: at present below their respective Neutral Zones for this session are the Swiss Franc, Gold and Silver; indeed across the board, all eight BEGOS Markets are underwater, and volatility is mostly light, save for Silver having already traced 5% of its EDTR (see Market Ranges). Yesterday’s S&P surge to a record high (5447) without supportive earnings puts the “live” futs-adj’d P/E at 41.2x. Currencies’ cac volumes are beginning their roll from June into September. And at the wholesale inflation level, today’s incoming metrics for the Econ Baro include May’s PPI.

12 June 2024 – 08:34 Central Euro Time

Oil is at present the sole BEGOS Market outside (above) its Neutral Zone for today; session volatility “ahead of the Fed” is very light. At Market Values, Oil is just a point or so below its smooth valuation line, the upside penetration of which by rule is a Long signal; and at Market Trends, whilst Oil’s linreg is negative, the “Baby Blues” of trend consistency are now into their third day of ascent; on a 10-test pure swing basis, Oil’s best Market Rhythm is the 1hr Price Oscillator; and for within swing profit-taking ’tis the 6hr MACD (as graphically detail on our Oil page). Late in the session we’ve both the FOMC’s Policy Statement, Powell presser and Treasury Budget for May, prior to which comes that month’s CPI.

11 June 2024 – 08:39 Central Euro Time

Gold, Silver and Oil are all at present below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility again is light. Leading our Market Rhythms for pure swing consistency on a 10-test basis are Silver’s 1hr Price Oscillator, the Spoo’s 8hr MACD, and Copper’s 30mn Price Oscillator; on a 24-test basis the leaders are the Spoo’s daily Parabolics, the Yen’s (not yet an official BEGOS Market) 30mn Moneyflow, and Silver’s 1hr MACD. The best correlation amongst the five primary BEGOS components continues to be positive between the Euro and Gold. The Econ Baro is again quiet today ahead of nine metrics due — including inflation measures at the retail, wholesale and ex/im levels — from Wednesday through Friday. The FOMC’s two-day meeting begins today with their Policy Statement and Powell presser due tomorrow.

10 June 2024 – 08:32 Central Euro Time

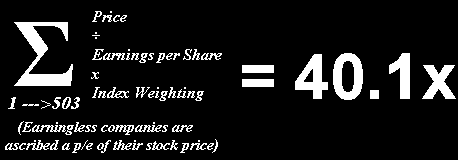

The back-loaded EconData week (plus the FOMC’s Policy Statement come Wednesday) at present finds the Bond, Euro and Swiss Franc below today’s Neutral Zones, whilst above same are both Silver and Copper; BEGOS Markets’ volatility is light. The Gold Update maintains its near-term negative price stance: of technical import thereto, Gold’s weekly MACD has now provisionally crossed to negative; (confirmation would arrive at week’s end); downside price follow-throughs of this study average some -90 points, which in this case would place Gold well-within its 2247-2171 structural support zone. The S&P 500 settled its week with the “live” P/E at 40.1x. And by Market Values (in real-time), the Spoo is +136 points above its smooth valuation line.

The Gold Update: No. 760 – (08 June 2024) – “Inflation’s Strain Remains Gold’s Bane”

With the Federal Open Market Committee’s Policy Statement and Powell Presser due Wednesday, we’ll wrap with this from the “Retraction/Correction/Blew It Dept.” given reference to the aforementioned brilliance of AI.

In last week’s missive we performed quite the song and dance over how $34T might be “visualized”. And via proper math we concluded that $34T in One Dollar bills laid end-to-end essentially equated to 5.5x the distance from Earth to Neptune. However, we fell afoul of the cardinal rule not to depend on stoopid source material. Indeed, rather than scrounge round through a wallet-full of Euros in search of a stray One Dollar bill for our measuring tape, we instead queried: “How many One Dollar Bills laid end-to-end make one mile?” And now after further review following email spew, Assembled Inaccuracy didn’t have a correct clue. (So what else is new…)

Start with the wrong number … End with the wrong number! For the correct answer and proper use of brain function, we leave it to you StateSiders to get out a buck, your ruler, and do the math from there. And you’ll still find the number unfathomably impossible.

‘Course, near-term negativity notwithstanding, the one number to grab is Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

07 June 2024 – 08:40 Central Euro Time

At present we’ve Copper as the only BEGOS Market outside (below) its Neutral Zone for today; session volatility is light with StateSide jobs data in the day’s balance. Curious to note yesterday’s ECB rate reduction despite the Governing Council’s outlook for increasing inflation. Going ’round the Market Trends page (21-day linreg basis and “Baby Blues” consistency): that for the Bond is up and reinforcing; the Euro up but weakening; the Swiss Franc up and reinforcing; Gold barely up and neutral; Silver up but weakening; both Copper and Oil down and worsening; and the Spoo up but weakening. The tumbling Econ Baro completes its busy week with May’s Payrolls data as noted, plus April’s Wholesale Inventories and (late in the session) Consumer Credit.

06 June 2024 – 08:35 Central Euro Time

The Swiss Franc, Gold and Silver all are at present above today’s Neutral Zones; none of the other BEGOS Markets are below same, and volatility is pushing toward moderate. Following yesterday’s record high, the “live” P/E of the S&P 500 is a futs-adj’d 40.5x and the yield 1.352%; three-month annualized U.S. T-Bill dough yields 5.240% without the risk of capital loss. An interesting Market Rhythm to mind is Gold’s 2h MACD: its last nine swings (both Long and Short) from 16 May-to-date have produced at least 12 points of signal follow-through ($1,200/cac); whilst the yellow metal both yesterday and today is having a recovery run, the weekly MACD is nearing a negative cross, in line with our recent writings being wary of near-term price retrenchment. Incoming metrics today for the Econ Baro include April’s Trade Deficit and the revision to Q1’s Productivity and Unit Labor Costs.

05 June 2024 – 08:01 Central Euro Time

The Bond and Swiss Franc are at present below their respective Neutral Zones for today; above same is Gold, and BEGOS Markets’ volatility is light. Gold’s weekly MACD is poised for a negative crossing, the last five of which over three years have led to lower prices of at least -30 points; The Gold Update cites specific lower levels of which to be aware following the “double-top” which formed across the past seven weeks; and price has been flirting with either side of its smooth valuation line (see Market Values). But that same metric, Oil (in real-time) shows as -7.83 points “low” and the Spoo as +123 points “high”, The Econ Baro looks to May’s ADP Employment data and the ISM(Svc) Index.

04 June 2024 – 08:26 Central Euro Time

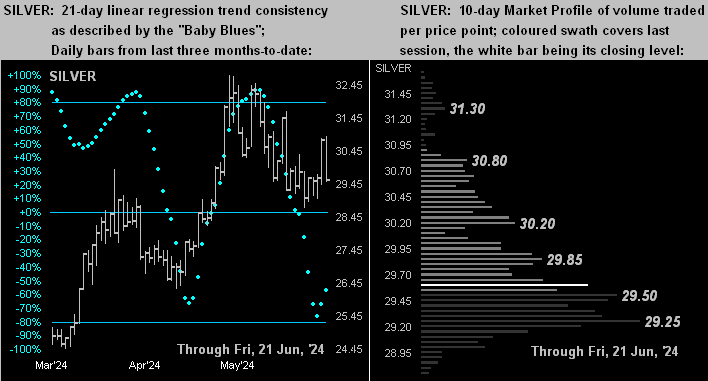

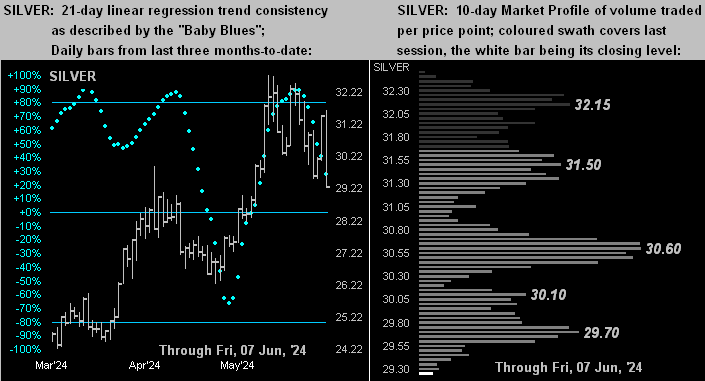

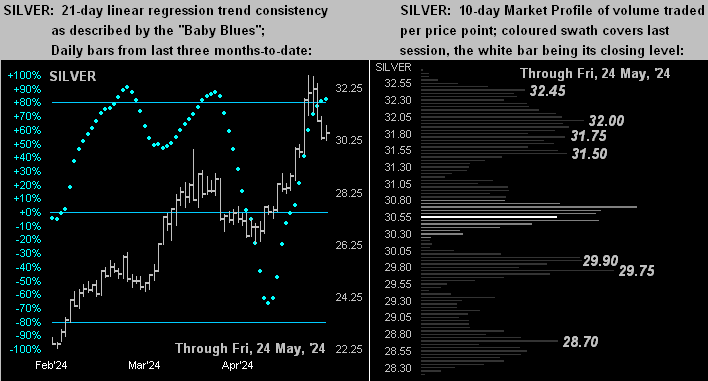

BEGOS Markets’ volatility is lighter than ’round this time yesterday, all eight components having thus far traced less than 50% of their EDTRs (see Market Ranges). The Swiss Franc is at present above today’s Neutral Range, whilst below same is Oil. Yesterday was a sizable up day for the currencies, both the Euro and Swiss Franc moving to nearly two-month highs. At Market Trend’s, Silver’s “Baby Blues” of trend consistency confirmed dropping below their key +80% axis, suggestive of lower prices near-term: should yesterday’s low of 29.940 go, a test of 29.000 (10 May’s high) appears structurally reasonable; Silver’s Market Profile support is 30.650 to 30.500; note as well at on our page for Silver that its EDTR presently exceeds 1.000 (the actual reading being 1.155 points per day). April’s Factory Orders come due for the Econ Baro.

03 June 2024 – 08:36 Central Euro Time

The week begins with the Bond at present above its Neutral Zone for today; below same are Oil, Silver and Gold; volatility is moderate. The Gold Update still is slanted toward lower prices near-term following the yellow metal’s have created a notable “double-top” within the past seven weeks, such pattern generally leading to further downside. The best correlation amongst the five primary BEGOS Markets is positive between the Euro and Gold. Leading our Market Rhythms for pure swing consistency on a 10-test basis is again the Yen’s (not yet a formal BEGOS component) daily Parabolics, and on a 24-test basis ’tis Gold’s 1hr MACD; (as highlighted in The Gold Update, the yellow metal’s 12hr MACD is best for profit taking within swings). The Econ Baro starts a busy week with May’s ISM(Mfg) Index and April’s Construction Spending.

The Gold Update: No. 759 – (01 June 2024) – “Gold’s Double-Top Primes Price Plop”

The above chart tracks Gold by its 12-hour bars from nearly the beginning of this year-to-date. (The inset at lower right is by Gold’s daily candles specific to the August contract for the past two months). And stark thereon is the double-top (both being chronological All-Time Highs) achieved at 2449 on 12 April and again at 2454 on 20 May. The rationale for displaying the double-top per 12-hour bars is — that by price’s 12-hour MACD (moving average convergence divergence) — such study presently ranks as Gold’s best Market Rhythm for taking signals followed by profit. Green bars indicate price when the MACD is Long and red bars when Short, the latter as you know being a bad idea; (profitability results of this study are included on the website’s current Market Rhythms list).

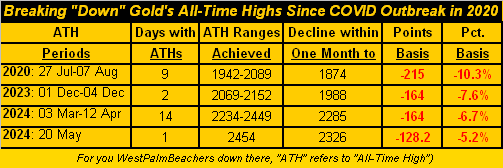

The key point of course is that double-tops in major markets are prime for selling (be it by humans or algorithms), which — in spite of our being broad-based bullish on Gold — has been our near-term bearish analytical slant given the abrupt downtrend from that 20 May All-Time High at 2454. Indeed since then, Gold has dropped (basis the June contract) from 2454 to as low as 2321 (-133 points or -5.4% in just eight trading days). Now by the August contract having settled yesterday (Friday) at 2348, should 2309 go, the 21 March high of 2263 ought come into play … just in case you’re scoring at home.

More importantly, what’s coming into play in the words of Bloomy last Wednesday is “Revived Hike Chatter”. For some irrational reason, the FinWorld just seems to be figuring that out now. However, we’ve regularly herein been musing since the start of this year about the Federal Reserve ~~perhaps~~ having to raise rather than cut interest rates. The difference between ![]() “Us and Them”

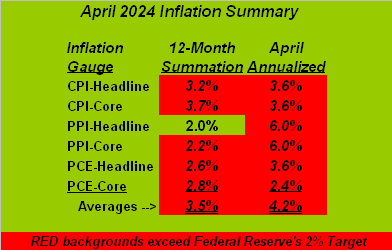

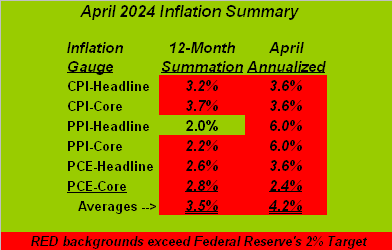

“Us and Them”![]() –[Pink Floyd, ’73] is simple: we do the math; the FinWorld parrot one another. And by the math, inflation remains on the move as below summarized in our April table:

–[Pink Floyd, ’73] is simple: we do the math; the FinWorld parrot one another. And by the math, inflation remains on the move as below summarized in our April table:

Therein are the three major measures of StateSide inflation: the Consumer Price Index (CPI), Producer Price Index (PPI) and “Fed-favoured” Personal Consumption Expenditures Price Index (PCE), all listed with both their headline and attendant core readings. The left column is each category’s 12-month summation and the right column is April’s data annualized. Now look at the two averages, bearing in mind the Fed’s inflation target is 2%: for the 12-month summation ’tis 3.5%; but for April’s annualized paces ’tis 4.2%. Which for you WestPalmBeachers down there means: “We’re going the wrong way…”

So is the StateSide economy. Recall our penning a week ago: “…the Baro looks to be lower still in a week’s time as stagflation creeps ‘cross the nation…” Cue Tag Team from back in ’93: ![]() “Whoomp! (There It Is)””

“Whoomp! (There It Is)””![]()

To wrap: with each passing week, more and more internet information (or “bilge” if you will) builds toward financial end-times, part and parcel of which would include our “Look Ma, no money!” S&P crash. ‘Course this being big election years coinciding both on this side of the Pond (five-year Parliamentary) and StateSide (four-year Presidential), the hype of “Well, it’s the election, you know…” already is quite rife. But even were it not, the following macro-prudential fact remains: the S&P 500 is priced at nearly double its earnings support, whilst Gold is priced at nearly half its Dollar debasement valuation. And as we’ve demonstrated ad nauseum throughout 16 years of these weekly missives, price inevitably reverts to valuation. Therefore, near-term price plop or not: hopefully your Gold is well-guarded when sought!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

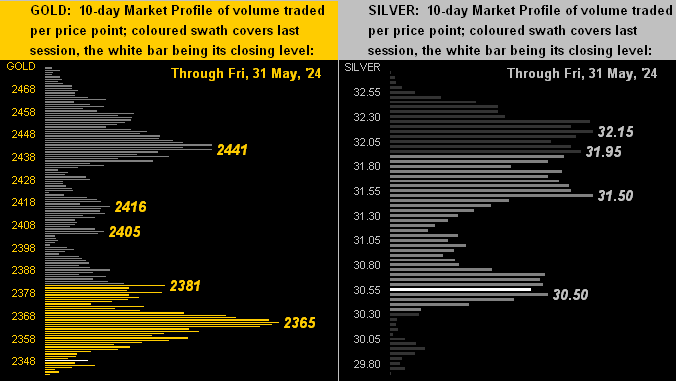

31 May 2024 – 08:16 Central Euro Time

The BEGOS Markets are fairly quiet ahead of “Fed-favoured” inflation data due for April: both the Euro and Swiss Franc are at present a bit below their Neutral Zones for today; otherwise the balance of the components are within same, and volatility is light. The Spoo’s “Baby Blues” (see Market Trends) confirmed closing yesterday below their key +80% axis: year-over-year there’ve been six prior such negative crossovers, price then averaging -96 points of downside within the ensuing 21 trading days (one month); and by Market Values (in real-time), the Spoo still is +81 points above its smooth valuation line; too, this past Wednesday, the Spoo crossed below its Market Magnet, also indicative of further near-term price fallout; there is some structural support for the Spoo in the 5154-5036 zone, (i.e. beginning some -90 points below present price). The Econ Baro looks to May’s Chi PMI, plus April’s Personal Income/Spending and Core PCE Prices.

30 May 2024 – 10:26 Central Euro Time

On the heels of yesterday’s declines across all eight BEGOS Markets, we’ve at present both the Bond and Swiss Franc above their respective Neutral Zones for today, whilst below same are Gold, Silver, Copper, Oil and the Spoo; session volatility is moderate. At Market Trends, save for Silver and Oil, the “Baby Blues” of trend consistency are falling for the balance of the bunch. Looking at Market Rhythms on a profit-taking (rather than pure swing) basis, the best study is the Spoo’s daily Price Oscillator: there have been 10 signals extending as far back as 20 December 2022 for which all 10 produced price follow-through of at least 44 points (i.e. $2,200/cac); the current signal has been Long since 08 May. Metrics for the Econ Baro today include April’s Pending Home Sales and the first revision to Q1 GDP.

29 May 2024 – 08:24 Central Euro Time

Gold picks up +23 points of fresh premium as cac volume moves from June into that for August; however, the yellow metal is lower today, at present below its Neutral Zone as is the Spoo; none of the other BEGOS Markets are above same, and volatility is light. Looking at Market Rhythms for pure swing consistency: on a 10-test basis our best three are the Yen’s (not yet an official BEGOS Market) daily Parabolics, Copper’s 5mn Moneyflow, and the Spoo’s daily Parabolics; on a 24-test basis, the top three are the Yen’s 4hr Moneyflow, Gold’s 2hr Parabolics, and Copper’s 1hr MACD. Our best correlation amongst the five primary BEGOS components is positive between Gold and Oil. No metrics are due today for the Econ Baro.

28 May 2024 – 08:37 Central Euro Time

The BEGOS Markets’ two-day session continues, all three elements of the Metals Triumvirate at present above today’s Neutral Zones, as are Oil, the Euro and Swiss Franc; within same are both the Bond and Spoo; volatility has expectedly widened, now mostly moderate-to-robust, Silver with the largest EDTR (see Market Ranges) tracing at 150%. The Spoo is (in real-time) +192 points above its smooth valuation line (see Market Values); by Market Profiles, the Spoo’s most commonly traded price of the past 10 sessions is 5333. The S&P’s MoneyFlow has been significantly skewed to the upside on further piling into NVDA; otherwise by the page’s quarterly measure, the trend had been in mild decline. The Econ Baro awaits May’s Consumer Confidence.

27 May 2024 – 08:35 Central Euro Time

The two-day session for the BEGOS Markets is underway, (for Tuesday settlement given the StateSide holiday). The precious metals are getting the bid, both Gold and Silver at present above today’s Neutral Zones; the other six BEGOS components are within same, and volatility expectedly is quite light: only Silver has thus far traced in excess of 50% (55%) of its EDTR (see Market Ranges). The Gold Update acknowledges the most recent All-Time High (2454) as being at best “marginal” and cites what have become “habitual” moves lower typically following such post-COVID highs. The S&P 500 settled Friday as 13 days “textbook overbought”: the futs-adj’d “live” P/E is 39.7x. The Econ Baro anticipates just nine incoming metrics as the week unfolds, including on Friday the “Fed-favoured” PCE for April.

The Gold Update: No. 758 – (25 May 2024) – “Gold’s Marginal High and Habitual Cry”

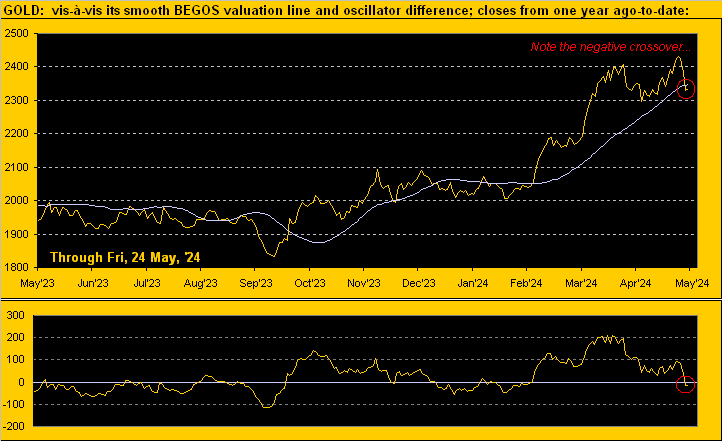

Our takeaway is: ‘twould be folly not to anticipate lower Gold prices near-term. In addition to price having just crossed beneath the aforeshown smooth valuation line, we’ve the following technical negatives: Gold’s daily Parabolics flipped from Long to Short effective yesterday’s open as did the MACD (moving average convergence divergence); the daily Price Oscillator is dwindling and the Moneyflow is nearing a cross from inflow to outflow.

Still, with prudent cash management always paramount — and acknowledging that “shorting Gold is a bad idea” — let’s wrap with the stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3769

Gold’s All-Time Intra-Day High: 2454 (20 May 2024)

2024’s High: 2454 (20 May 2024)

Gold’s All-Time Closing High: 2430 (20 May 2024)

10-Session “volume-weighted” average price magnet: 2385

Trading Resistance: various per the Profile from here at 2335 up to 2440

Gold Currently: 2335, (expected daily trading range [“EDTR”]: 38 points)

10-Session directional range: down to 2326 (from 2454) = -128 points or -5.2%

Trading Support: none per the Profile

The Weekly Parabolic Price to flip Short: 2263

Structural Support: 2247-2171

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The 300-Day Moving Average: 2046 and rising

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

‘Course the bottom line is, regardless of its marginal high but then habitual cry, don’t miss out when Gold goes to the sky!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

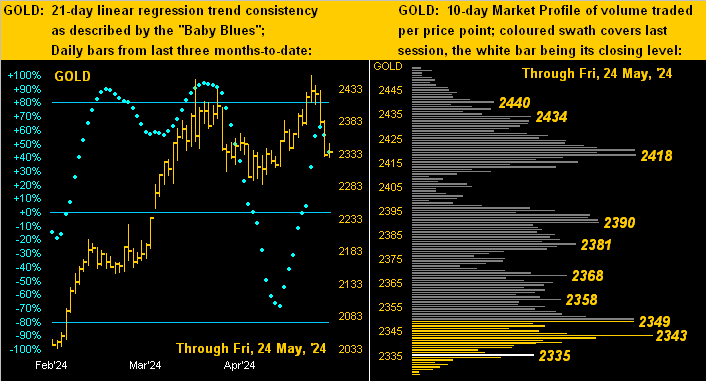

24 May 2024 – 08:28 Central Euro Time

The precious metals are getting a grip, both Gold and Silver at present above their respective Neutral Zones for today; the other six BEGOS Markets are within same, and session volatility is quite light ahead of the StateSide long weekend. In recent years, Gold after recording All-Time Highs has habitually, indeed materially, pulled back somewhat swiftly: more on that in tomorrow’s 758th consecutive Saturday edition of The Gold Update; too, the yellow metal finally has returned to its smooth valuation line (see Market Values) for the first time since 28 February. At Market Trends, the Spoo’s “Baby Blues” of trend consistency have (in real-time) kinked lower (but not so much as to yet penetrate their key +80% axis); still the S&P itself technically remains “textbook overbought” and is overwhelming expensive given its cap-weighted lack of earnings support. The Econ Baro concludes its quiet week with metrics including April’s Durable Orders.

23 May 2024 – 08:34 Central Euro Time

Following what we’d now classify as Gold’s “marginal” All-Time High on Monday (at 2454), the yellow metal has since been in sell mode (at present 2364), and along with Silver (30.545) is below today’s Neutral Zone; the Spoo is above same, and BEGOS Markets’ volatility is light-to-moderate. Such selling has dutifully brought down the Market Value excess we’ve had for Gold for nearly three full months: price (in real-time) is now +20 points above its smooth valuation line; a month ago the deviation was +200 points. “Over-valued” too by such metric is the Spoo (+230 points) whilst “under-valued” we’ve Oil -5.78 points. Specific to our S&P MoneyFlow page, the three-month differential of Flow relative to the Index (per that page’s lower-right panel) has developed a detectably negative bent to it. The Econ Baro’s incoming metrics today include April’s New Home Sales.

22 May 2024 – 08:24 Central Euro Time

At present we’ve both the Bond and Copper below today’s Neutral Zones; the other BEGOS Markets are within same, and volatility is mostly light. Silver has quieted a bit relative to its ranginess into this week: indeed by Market Ranges, the white metal’s EDTR is now 0.99 points, (whereas last September ’twas as low as 0.46 points). The S&P 500 is now 10 consecutive days “textbook overbought”: the “live” (fut’s-adj’d) P/E is 40.4x and the yield 1.369% versus an annualized 5.240% on risk-free U.S. 3-month dough. One wonders for how much longer the investing herd shall continue seeking unrealistic capital gains rather than equities reasonably priced by earnings support: mind our S&P 500 Valuation and Rankings page. The Econ Baro awaits April’s Existing Home Sales; and the Fed releases the 30 Apr-01May FOMC meeting minutes.

21 May 2024 – 08:39 Central Euro Time

All three elements of the Metals Triumvirate as well as Oil are at present below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility is light-to-moderate, again save for Silver which today already has traced 153% of its EDTR; quietest is the Spoo with just a 10% tracing and nothing due for the Econ Baro. Following Gold’s new All-Time High yesterday (2454), price has backed off: still per Market Values, the yellow metal is (in real-time at 2419) +79 points above its smooth valuation line. Gold’s best Market Rhythm for pure swing consistency is (on a 10-test basis) its 12hr Parabolics and (on a 24-test basis) its 30mn Moneyflow; on a profit-taking basis, Gold’s daily Parabolics have reached follow-through of $2,700/cac in nine of the past 10 swings as listed on the Market Rhythms page; that, too, is the Rhythm featured on the Gold page.

20 May 2024 – 08:40 Central Euro Time

Gold has recorded another All-Time High this morning: The Gold Update mused it could happen as soon as today, and so it has, the intra-day high at present 2454, with price above its Neutral Zone as ’tis too for both Silver and the Euro; the other BEGOS Markets are within same. Session volatility is moderate, albeit specifically robust for Silver which already has traced 139% of its EDTR (see Market Ranges). Q1 Earnings Season has completed: for the S&P 500, 64% of reported constituents bettered the bottom lines over Q1 of a year ago, a somewhat sub-par performance given improvement (ex-COVID quarters) averages 69%; whilst the “live” P/E of the S&P was reduced from 46.1x, the current (futs-adj’d) 40.0x remains a dangerously high level. ‘Tis a very quiet week for the otherwise plunging Econ Baro: just five metrics are due, none until Wednesday.

The Gold Update: No. 757 – (18 May 2024) – “Another Gold All-Time High is Nigh”

Let’s wrap with our assessment of Q1 Earnings Season. As just ended “by the calendar”, for the S&P 500 — which also set a record high on Thursday at 5325 — we count 439 constituents having reported. Of those, 64% improved their bottom lines over Q1 of a year ago, (meaning that 36% did not so do). Excluding the four COVID quarters of 2020, the average year-over-year improvement runs ’round 69%: thus this past Earnings Season might be couched as rather sub-par. Yet upon its start back on 08 April, the S&P was 5204 and its “live” price/earnings ratio 46.1x. Today they are respectively 5303 and 39.9x: so some relative progress was made there in getting the p/e down a bit. Yet by any historical yardstick — especially in this positive interest rate environment — the p/e of 39.9x remains treacherously (understatement) high.

‘Course, ’tis made all the more complicated by this, (hat-tip Hedgeye’s hilarious Bob Rich):

So goodness gracious, with a new high nigh, stay gripped to Gold … and Silver bold!

Cheers!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

17 May 2024 – 08:16 Central Euro Time

‘Tis a fairly quiet start to Friday on the heels of a heavy week of incoming metrics for the Econ Baro, itself in a rather severe plunge. At present, just Copper is outside (above) today’s Neutral Zone, and BEGOS Markets’ volatility is mostly light, the red metal being the only component having thus far traced in excess of 50% (55%) of its EDTR (see Market Ranges). Going ’round the Market Values horn for the five primary BEGOS components (real-time readings): the Bond is nearly +3 points “high” above its smooth valuation line, the Euro +0.02 points “high”, Gold +56 points “high”, Oil -3.6 points “low”, and the Spoo +205 points “high”, the S&P itself having extended its “textbook overbought” stance through a seventh consecutive trading day. The Econ Baro completes it significantly down week with April’s Leading (i.e. “lagging”) Indicators. And today is the final day of Q1 Earnings Season, which for the S&P 500 has been somewhat sub-par by year-over-year growth.

16 May 2024 – 08:29 Central Euro Time

Following all-time highs yesterday for both Copper and Spoo (including the S&P 500 itself), we’ve at present all eight BEGOS Markets inside their respective Neutral Zones for today, ahead of another heavy round of incoming EconData; volatility is moderate. For the S&P, the combination of a new high and below-par Q1 Earnings Season growth has pushed the “live” P/E back above 40x, the futs-adj’d level now 40.5x; the Index is now at an extreme “textbook overbought” reading. As to the Euro, recall from earlier in the prior week our having noted per the Market Values page the currency’s having crossed above its smooth valuation line such that price by that leading indicative method could make a run toward the 1.10s: then ’twas in the 1.07s, having since traded up into the 1.09s. As for the Econ Baro, amongst today’s metrics are May’s Philly Fed Index, April’s Housing Starts/Permits, Ex/Im Prices, and IndProd/CapUtil.

15 May 2024 – 08:36 Central Euro Time

Copper is the sole BEGOS Market at present outside (above) today’s Neutral Zone; the red metal continues to be in play, having already traced 146% of its EDTR (see Market ranges); otherwise, session volatility for the other components is light with a bevy of EconData in the day’s balance. Looking at Market Trends we’ve only two with negative linregs: Gold and Oil; until the former clears at least 2385 (the Golden Ratio retracement cited in the current edition of The Gold Update), the recent near-term correction would technically remain in place; Gold at present is 2362 and its EDTR is 35 points. The Econ Baro’s busy day looks to May’s NY State Empire Index, Business Inventories and NAHB Housing Index, plus April’s reads on retail inflation (CPI) and Retail Sales.

14 May 2024 – 08:25 Central Euro Time

Both Silver and Copper are at present above their respective Neutral Zones for today; the other BEGOS Markets are within same, and volatility pre-StateSide inflation data is very light. Of the 405 Market Rhythms we test nightly, Copper (on a 10-test swing basis) is leading for consistency by its 30mn MACD; second-best is Gold’s 12hr Parabolics; too (on a 24-test swing basis) Copper’s 1hr MACD leads for consistency, followed again by its 30mn MACD. As well, Copper is the only BEGOS Market for which its EDTR (see Market Ranges) widened yesterday both day-over-day and week-over-week: thus vis-à-vis the whole bunch, Copper is most in play. And as noted, today the Econ Baro awaits April’s inflation at the wholesale level (PPI).

13 May 2024 – 08:37 Central Euro Time

The week begins with Gold at present below its Neutral Zone for today; the balance of the BEGOS Markets are within same, and volatility is light. The Gold Update inconclusively questions as to whether or not the yellow metal’s recent correction off its All-Time High (2449 on 12 April) has run its course: Gold’s rally this past week went precisely up to the perfect Golden Ratio fib retracement at 2385 (from the correction’s low [thus far?] of 2285), but has since pulled back (now 2358); too, by Market Values, Gold (in real-time) is +54 points above its smooth valuation line, and by Market Trends, the linreg remains negative. Whilst the Econ Baro is quiet today, a very busy week awaits with 18 metrics due, including those for April’s wholesale (PPI) and retail (CPI) inflation. As well, this is the final week of Q1 Earnings Season, which by year-over-year comparison has been rather mediocre (and thus is why the P/E of the S&P remains treacherously high, the “live” reading 39.2x).

The Gold Update: No. 756 – (11 May 2024) – “Gold Garners a Groovy Golden Ratio Retracement”

‘Course, the question then remains: has the near-term downside Gold correction run its course? Or is the perfect Fibonacci Golden Ratio retracement and subsequent same-day pullback signaling the resumption of such downside? To be sure, Gold’s daily “textbook technicals” (MACD, Price Oscillator, Moneyflow) — which a week ago were leaning lower — are just now bending up a bit. And yet per both the website’s Market Values and Gold pages, price is still +69 points above its smooth valuation line, (it has not been below same since 28 February). Also fundamentally, in a week almost completely bereft of incoming metrics for the Economic Barometer, save for some arguably “hawkish” FedSpeak to end said week, there’s really not that much upon which to critique. Yet as we all know, “the trend is your friend”, and as we next go to Gold’s weekly bars from a year ago-to-date, both the rising dashed linear regression trendline and blue-dotted parabolic Long trend look great. Warily however, prior to Gold next scoring a fresh All-Time High at 2450+, it may be a bit premature to start dancing to The Chipmunks ![]() “Funky Monkey“

“Funky Monkey“![]() :

:

Toward the wrap, let’s go to the stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3765

Gold’s All-Time Intra-Day High: 2449 (12 April 2024)

2024’s High: 2449 (12 April 2024)

Gold’s All-Time Closing High: 2391 (11 April 2024)

10-Session directional range: up to 2386 (from 2285) = +101 points or +4.4%

Trading Resistance: 2374

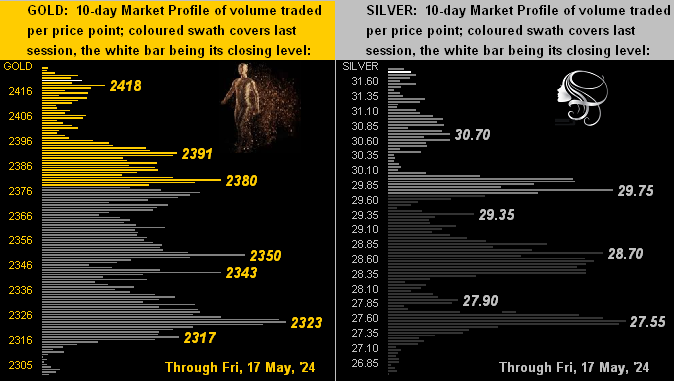

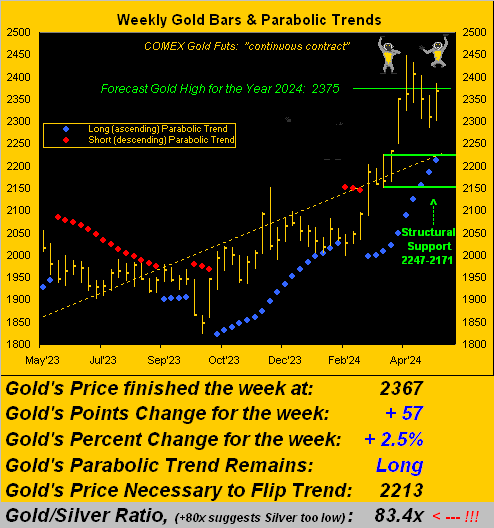

Gold Currently: 2367, (expected daily trading range [“EDTR”]: 37 points)

Trading Support: various from 2333 to 2298, most notably therein 2324

10-Session “volume-weighted” average price magnet: 2328

Structural Support: 2247-2171

The Weekly Parabolic Price to flip Short: 2213

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The 300-Day Moving Average: 2028 and rising

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

“So, mmb, we got your closer ready to go!“

And thank you, Squire, ’tis as rich as they come. We’ll spare (to benevolently save embarrassment) such pundit’s identity, but here we go. Ready? Hat-tip Dow Jones Newswires from last Monday:

- “Gold is overvalued now and won’t help you beat inflation in coming years.”

(Even the “doggy” can’t believe that one!)

Write it down and diarize to review, given ever-groovy Gold 3700+ is already overdue!

Cheers!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

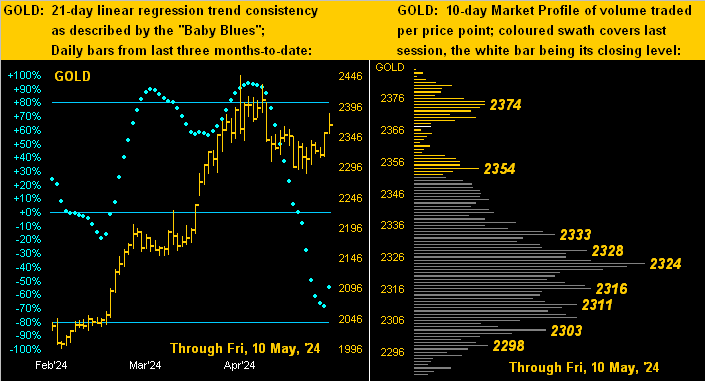

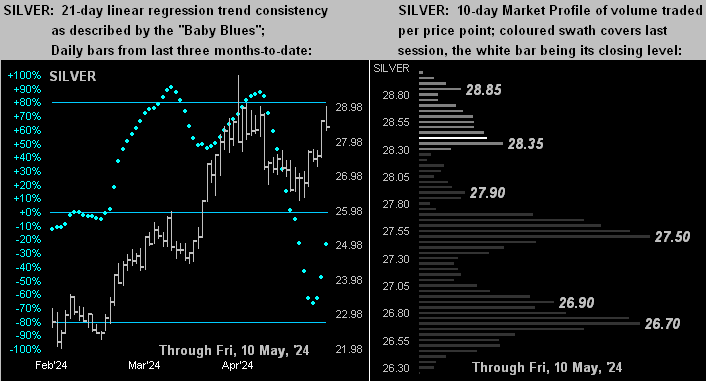

10 May 2024 – 08:37 Central Euro Time

The Metals Triumvirate is on the move this morning as Gold, Silver and Copper are getting the bid, all at present above today’s neutral Zones; the other BEGOS Markets are within same and volatility is mostly light, the exception being Copper having already traced 73% of its EDTR (see Market Ranges). Gold appears on track for a positive weekly close for the first time since that ending 20 April; in real-time, the yellow metal still is +70 points above its smooth valuation line (see Market Values); and at Market Trends, Gold’s linreg remains negative, however the “Baby Blues” therein have today lurched to the upside, and the “textbook technicals” have begun turning positive; more on it all of course in tomorrow’s 756th consecutive Saturday edition of the Gold Update. In a day replete with FedSpeak, the Econ Baro concludes its week with May’s UoM Sentiment Survey and April’s Treasury Budget.

09 May 2024 – 08:31 Central Euro Time

At present we’ve the Bond below its Neutral Zone for today, whilst Silver is above same; BEGOS Markets’ volatility by this hour remains quite light, again in a week with little incoming EconData. Looking at Market Rhythms for pure swing consistency, on a 10-test basis our leader is Copper’s 1hr MACD; on a 24-test basis ’tis the Swiss Franc’s 30mn Moneyflow. By Market Trends, when just recently Copper was sporting the only positive linreg, positive too now are those for the Bond, Euro, Swiss Franc and Spoo; ’tis indicative for Fed rate cut expectations. Our best correlation amongst the five primary BEGOS components is positive between the Bond and the Euro. Simply today for the Econ Baro arrives last week’s Initial Jobless Claims.