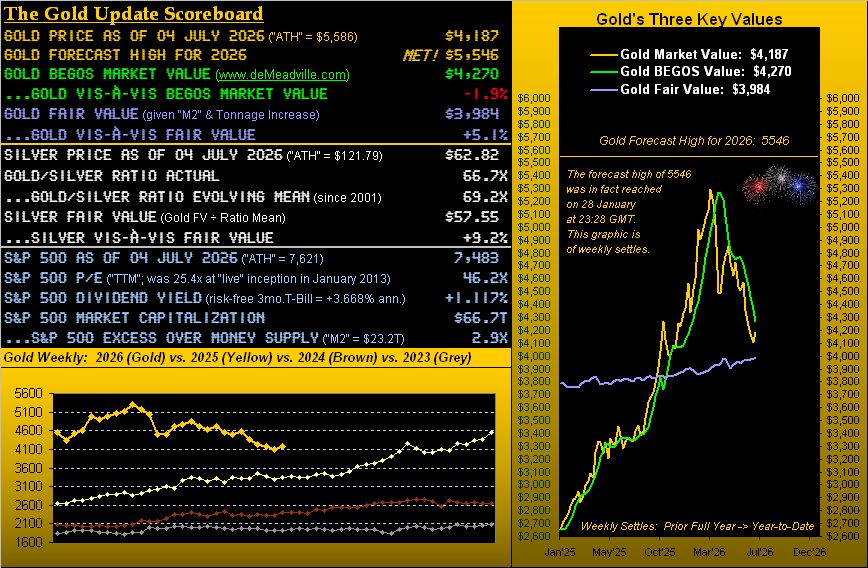

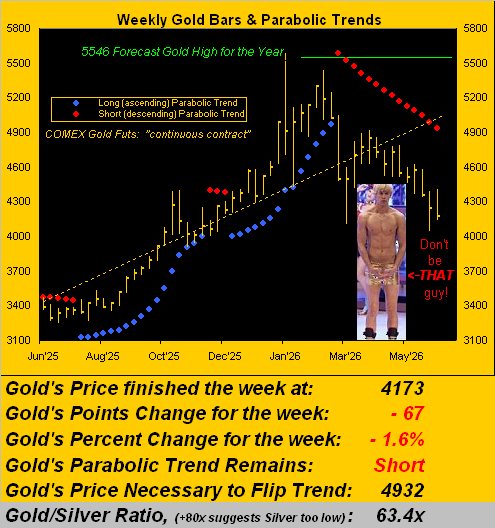

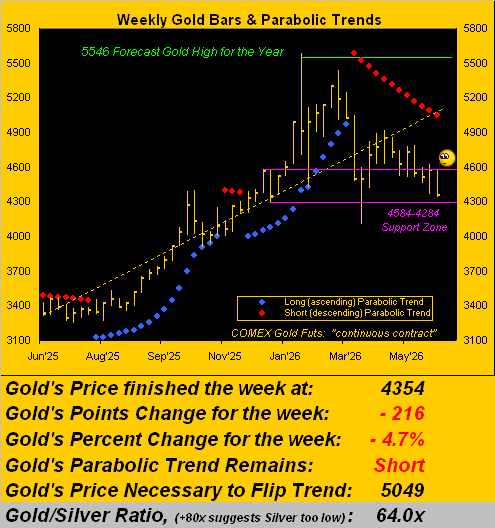

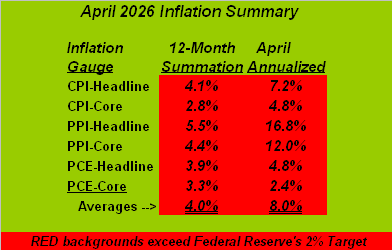

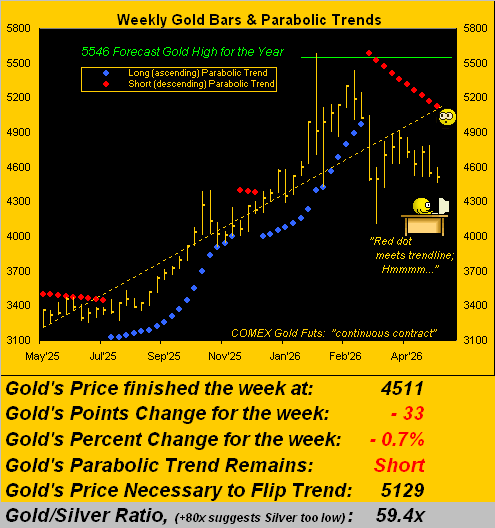

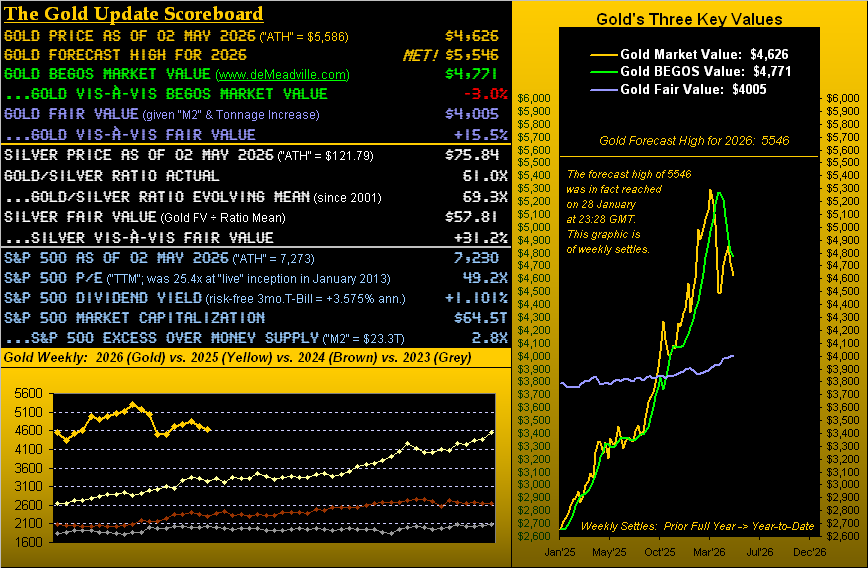

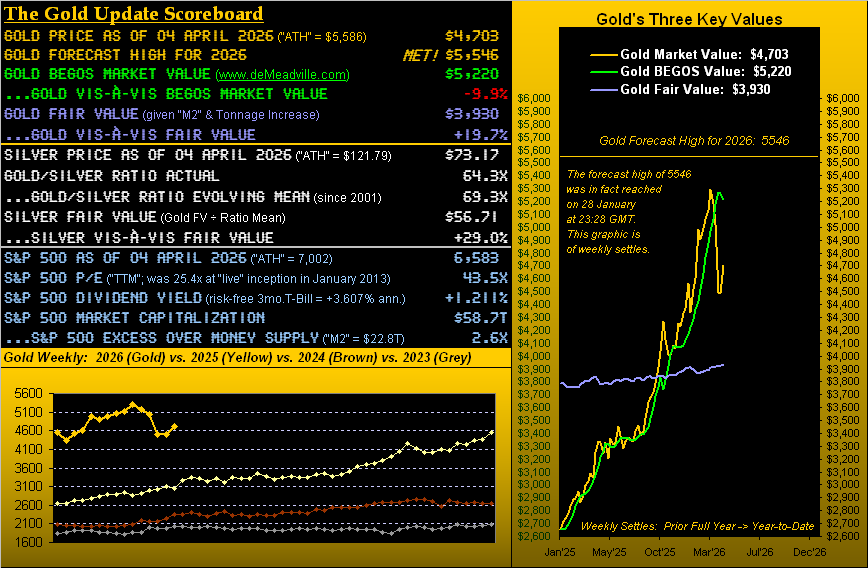

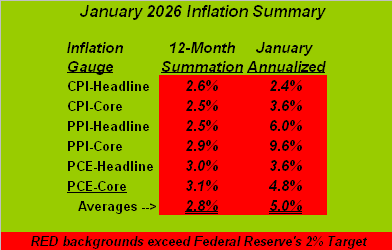

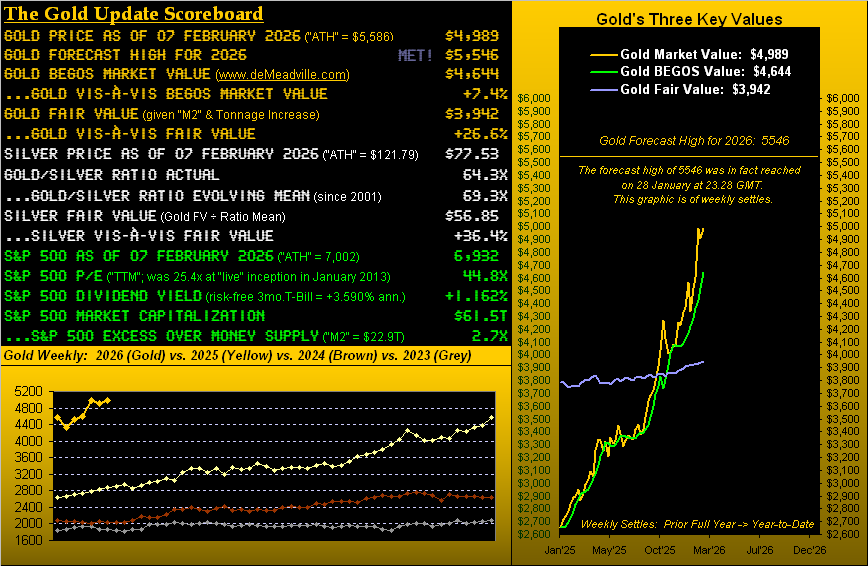

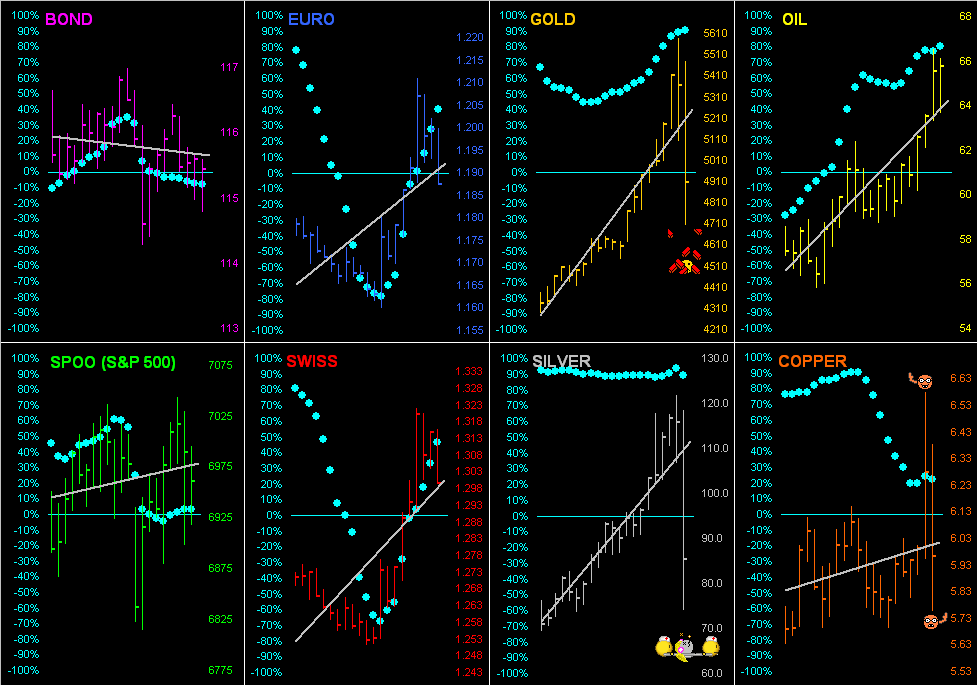

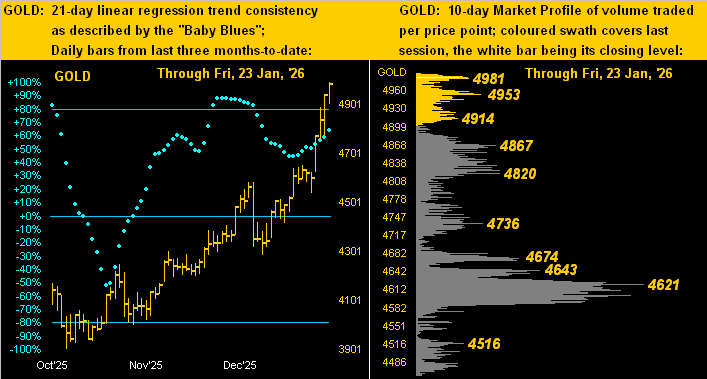

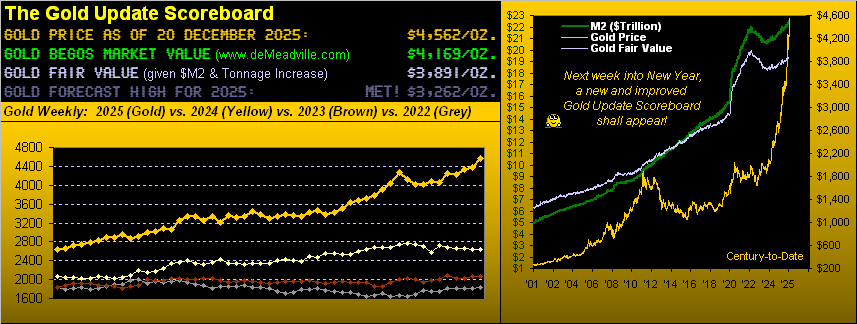

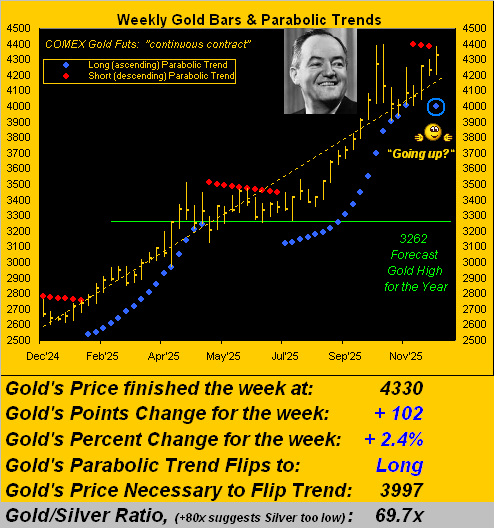

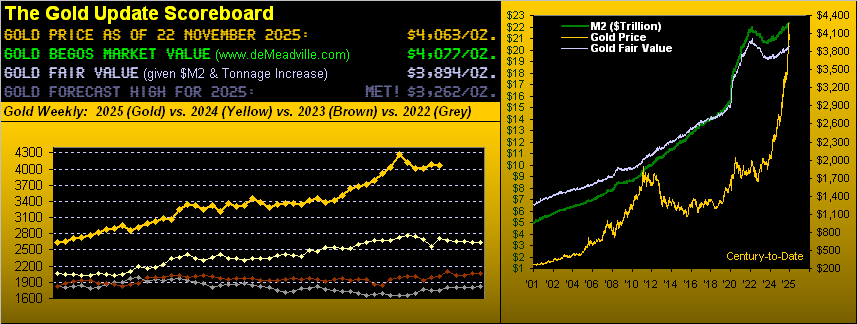

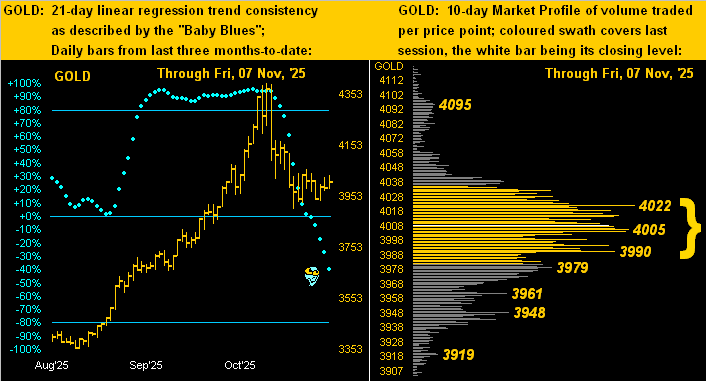

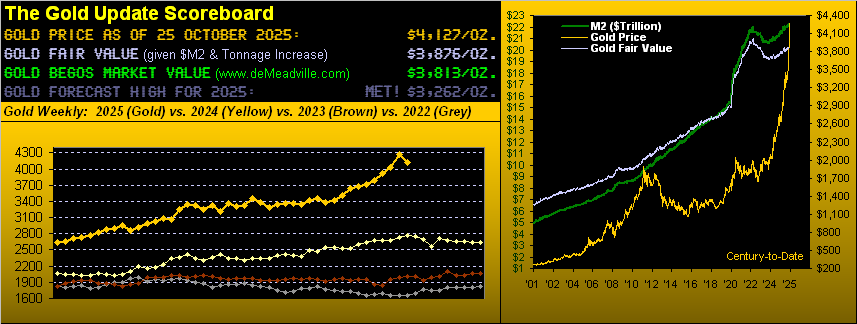

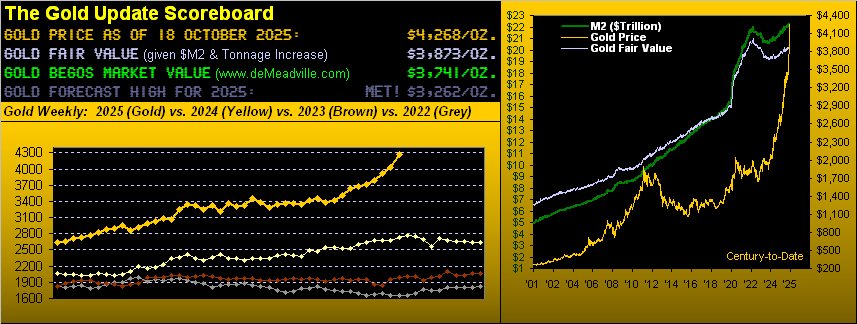

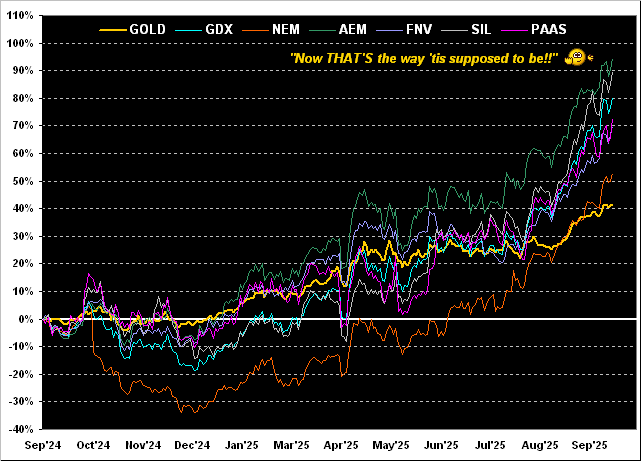

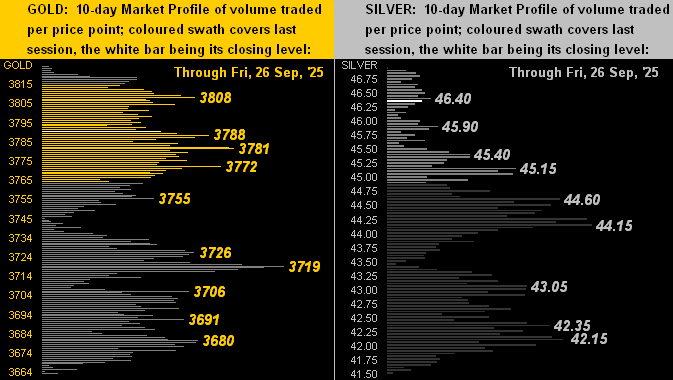

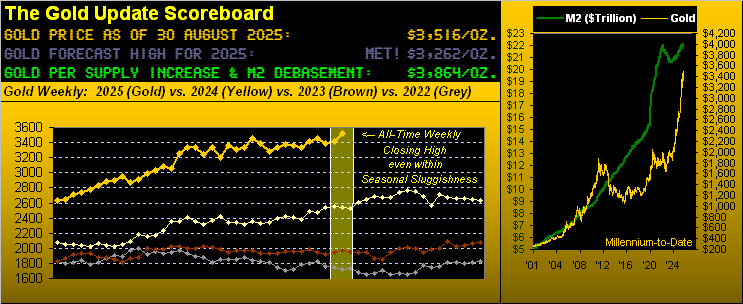

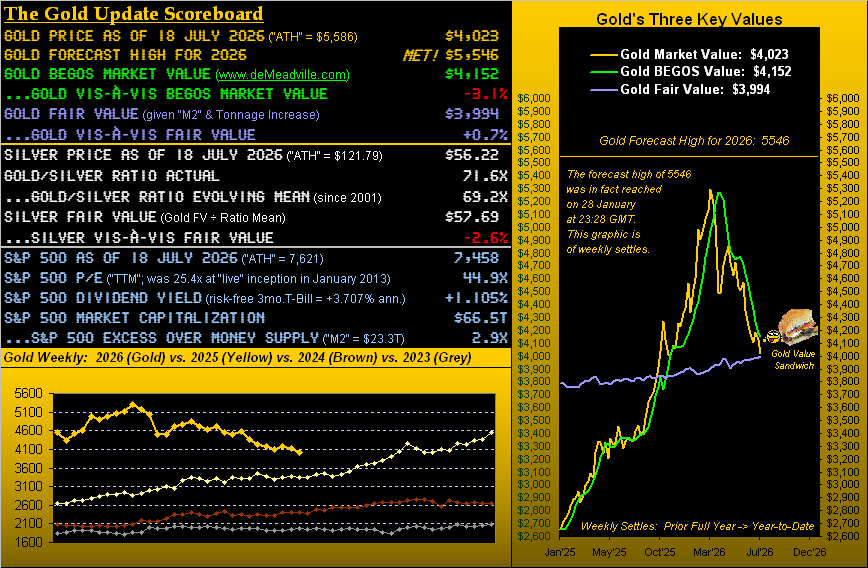

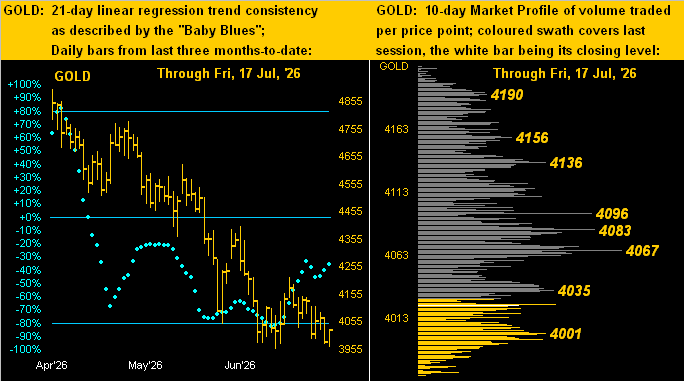

Our having taken on more of a bullish bent these last few weeks, we ~finally~ can open with some pleasing news: Gold just recorded an up week.

“Well, it really wasn’t much of a big deal, mmb… ”

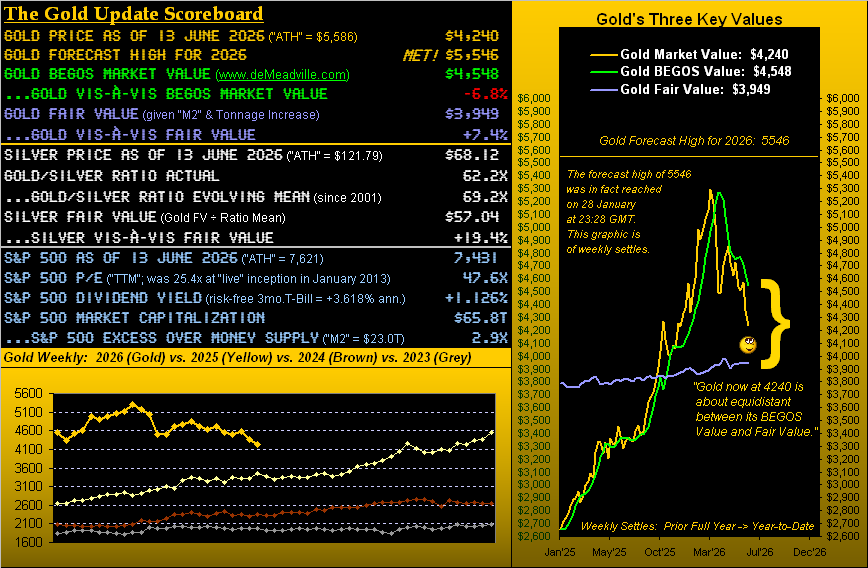

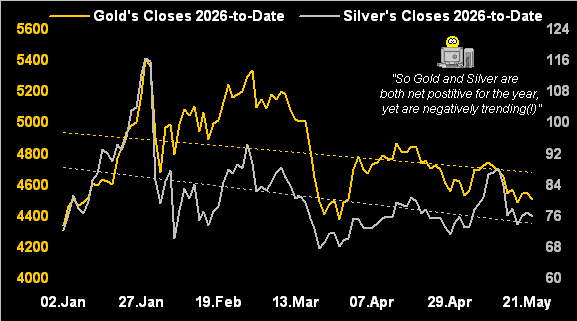

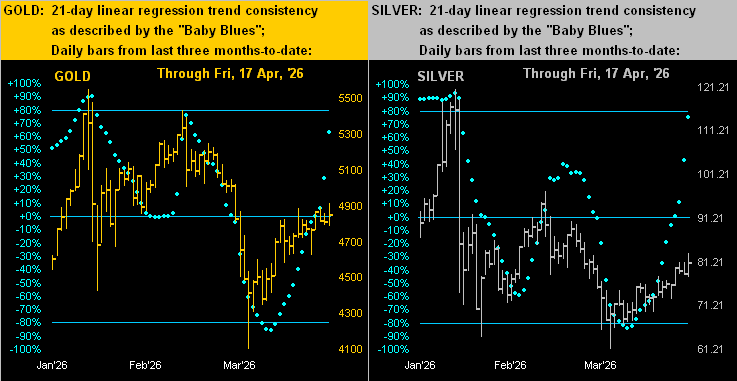

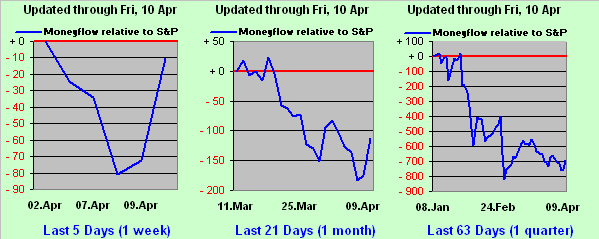

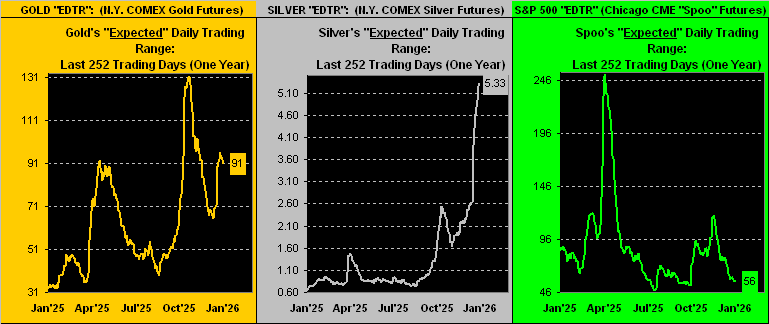

True enough, Squire. Yet thus far through the year’s 29 trading weeks, Gold just recorded only its fourth positive one in the last 14: ![]() “Happy days are here again…”

“Happy days are here again…”![]() –-[Milton Ager & Jack (not Janet) Yellen, ’29].

–-[Milton Ager & Jack (not Janet) Yellen, ’29].

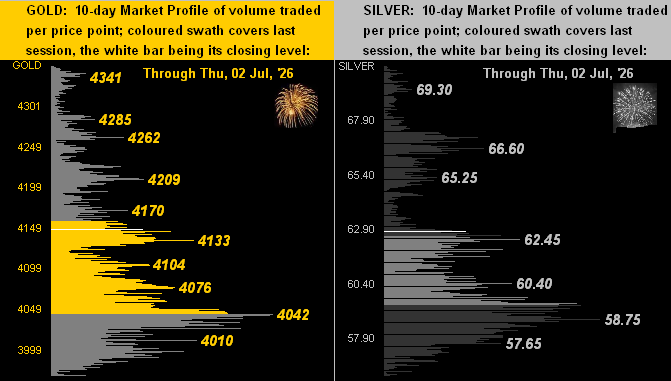

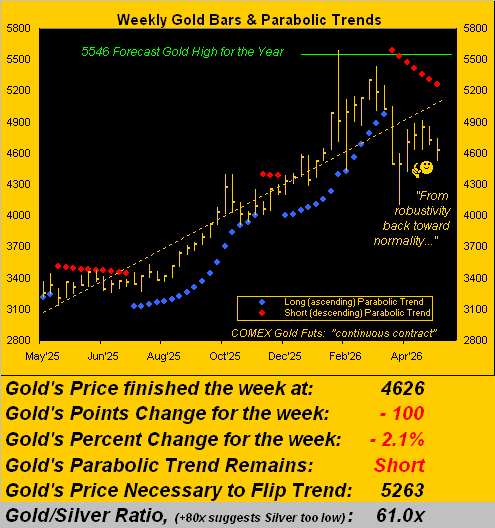

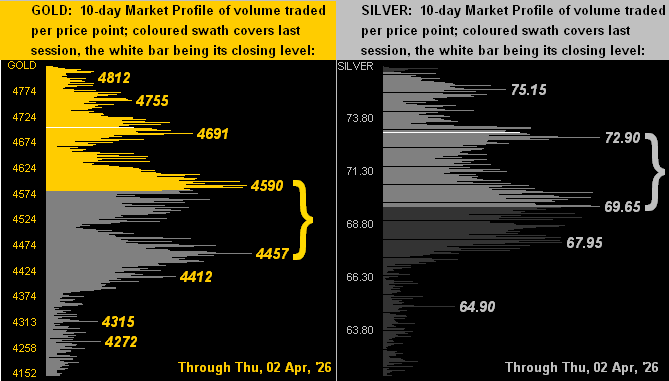

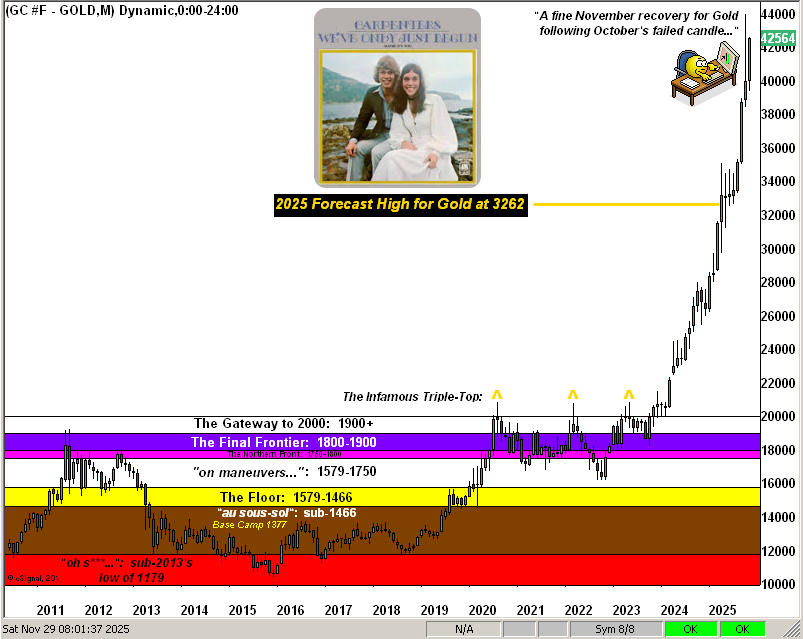

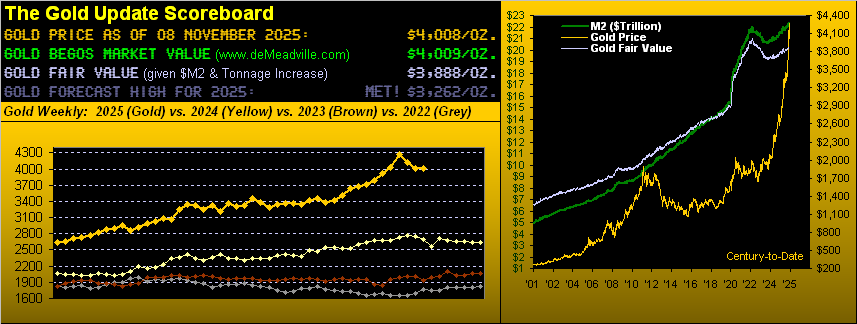

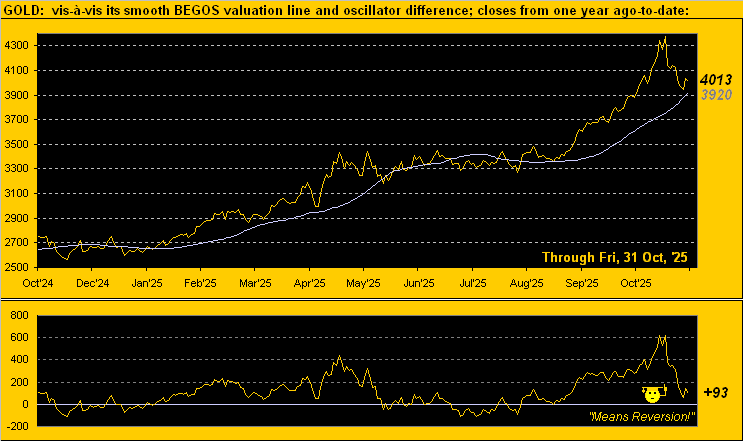

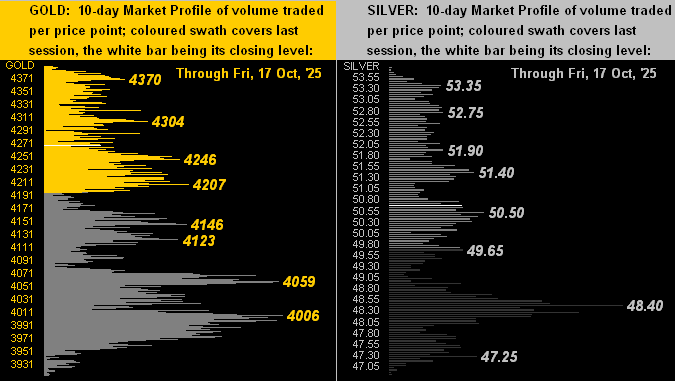

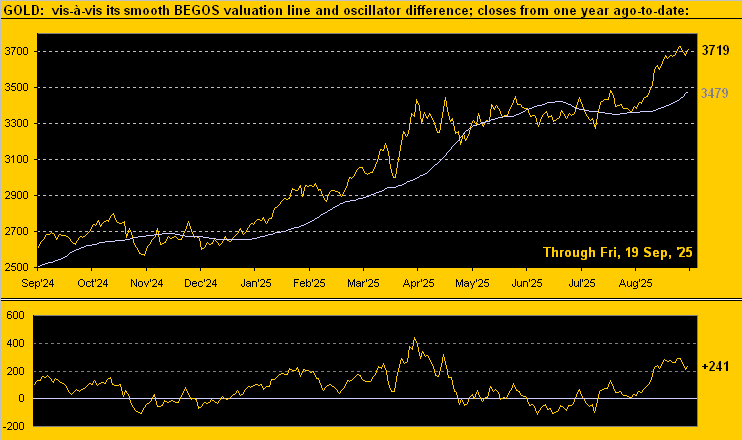

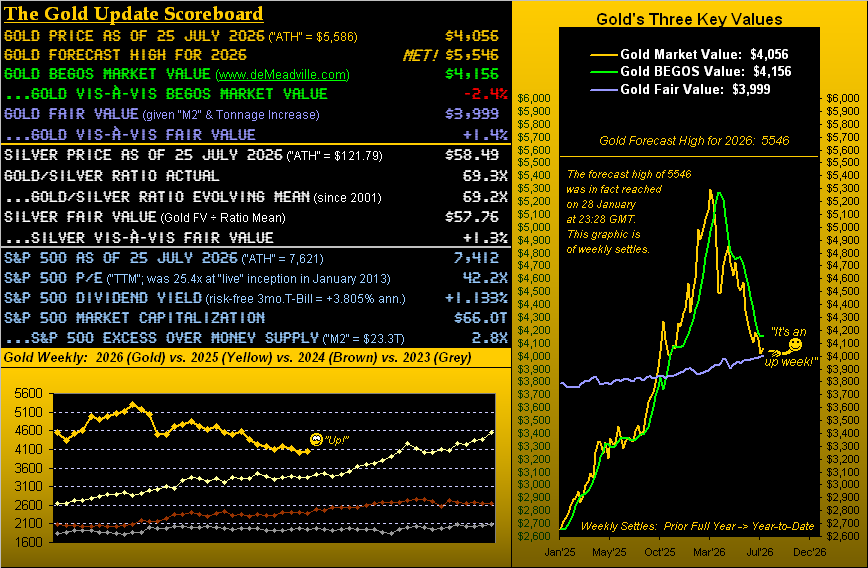

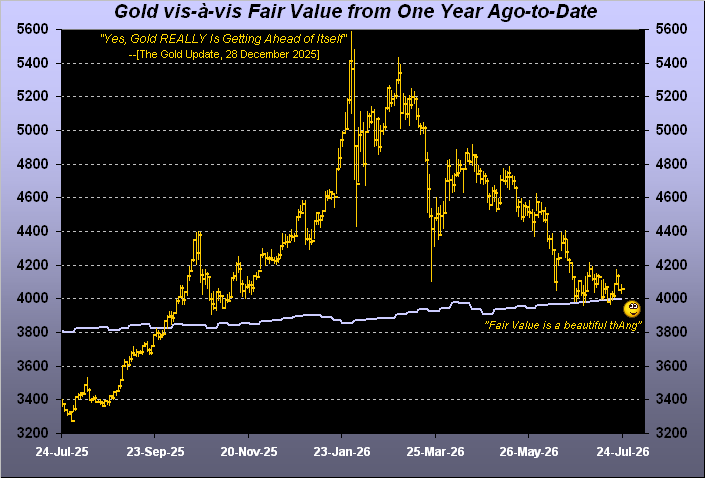

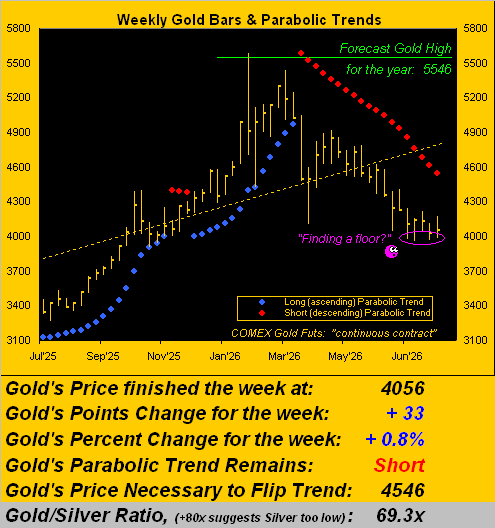

Indeed en route to settling this past week yesterday (Friday) at 4056, price rocketed higher from Monday into Wednesday, at one point up +3.7% to 4171. But we’ll gladly accept the week’s net gain — wee as ’twas (+0.8%) — after all the recent fits and starts — dare we say “derring-do” — that Gold’s been through.

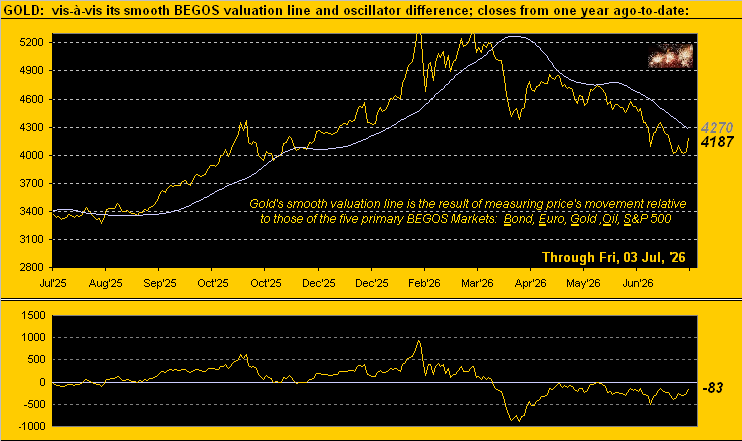

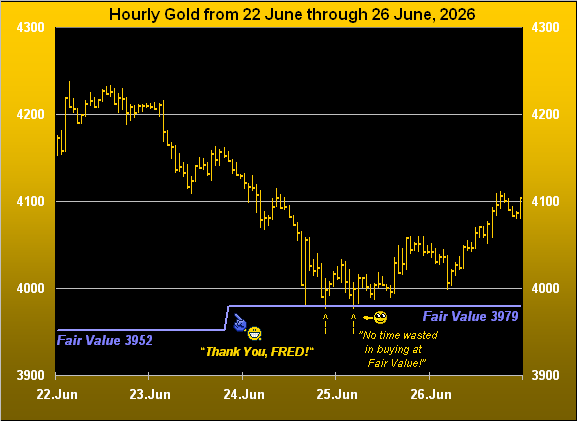

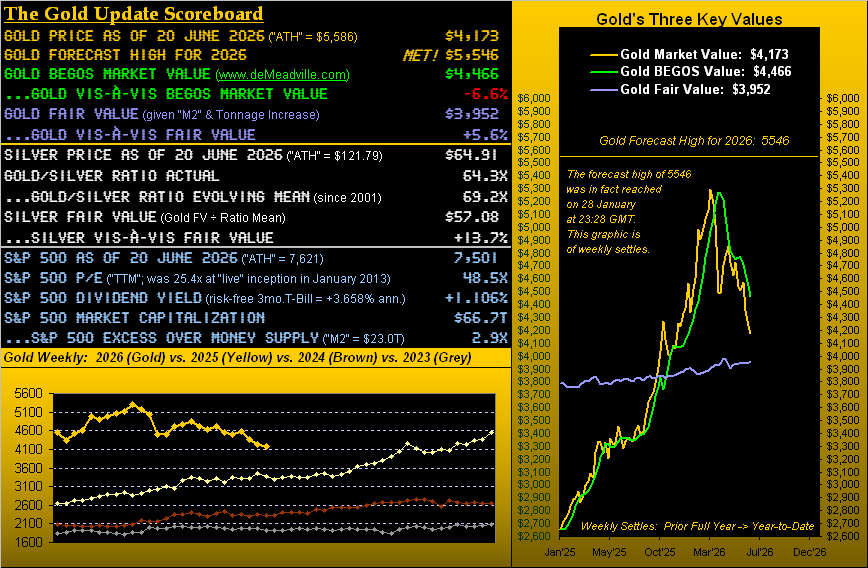

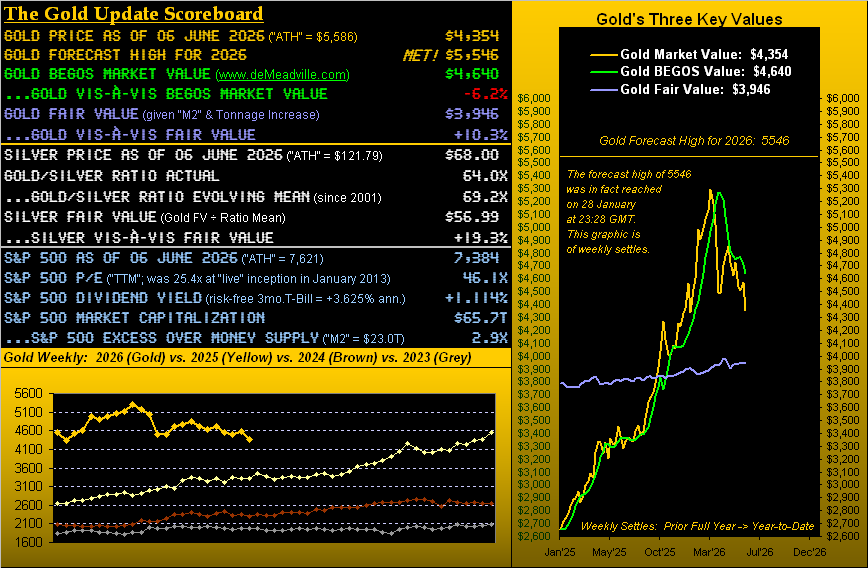

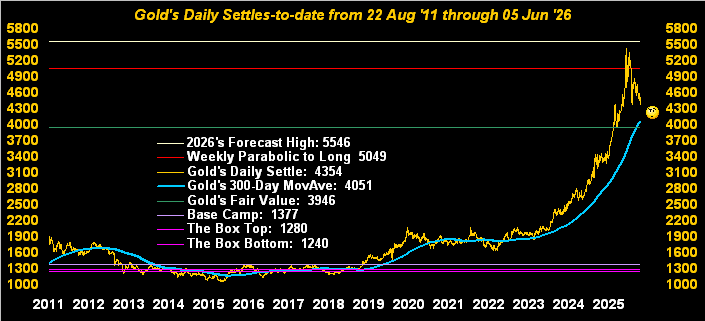

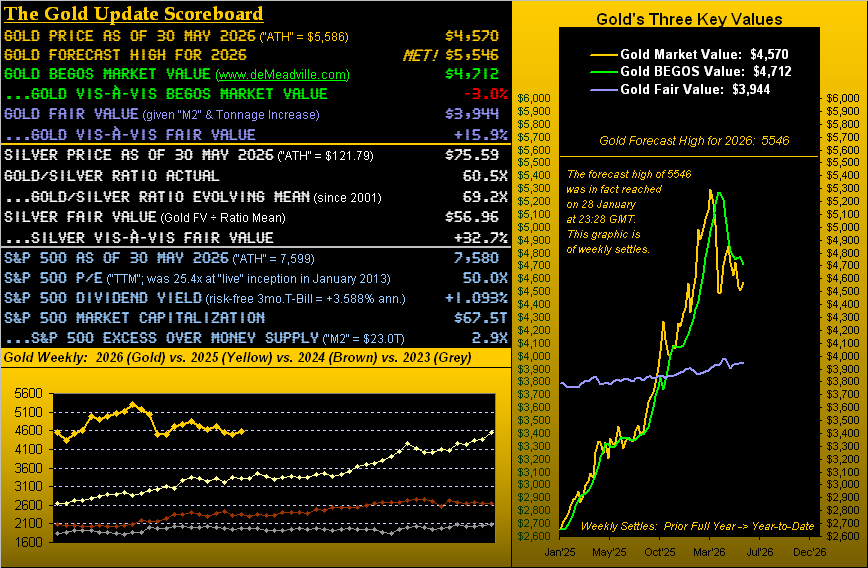

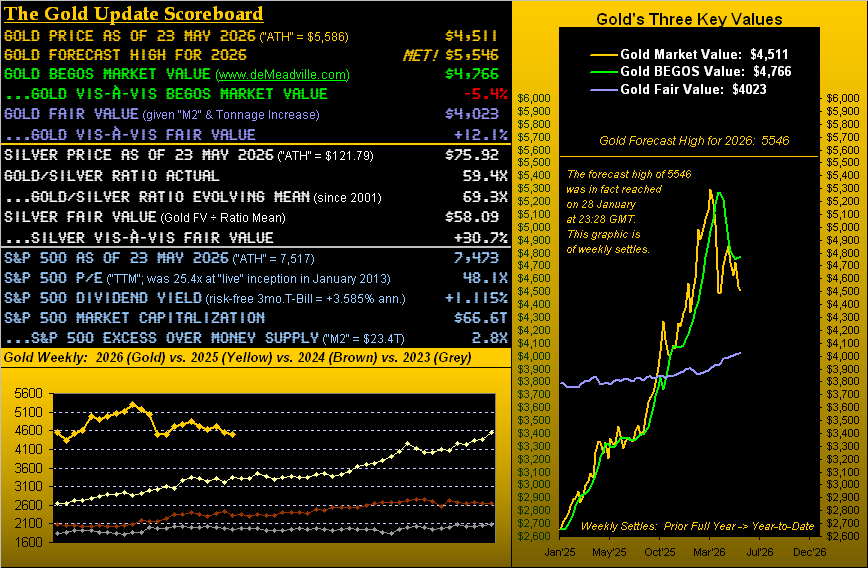

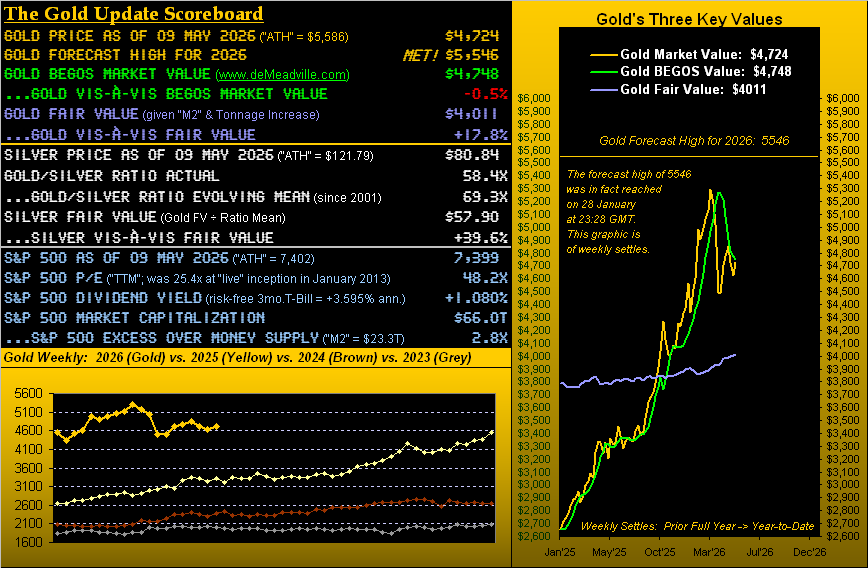

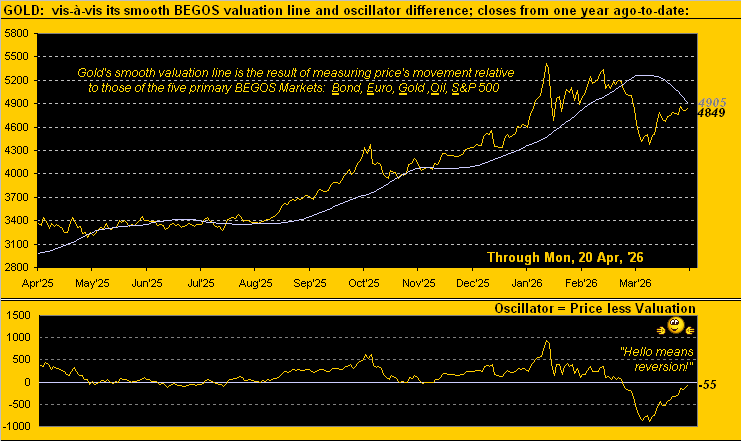

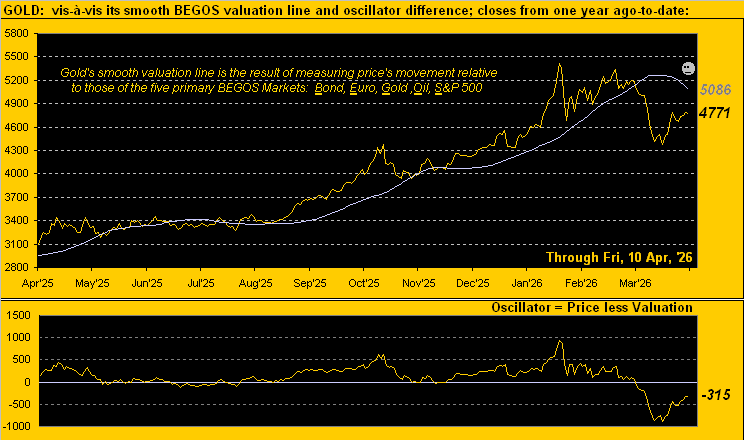

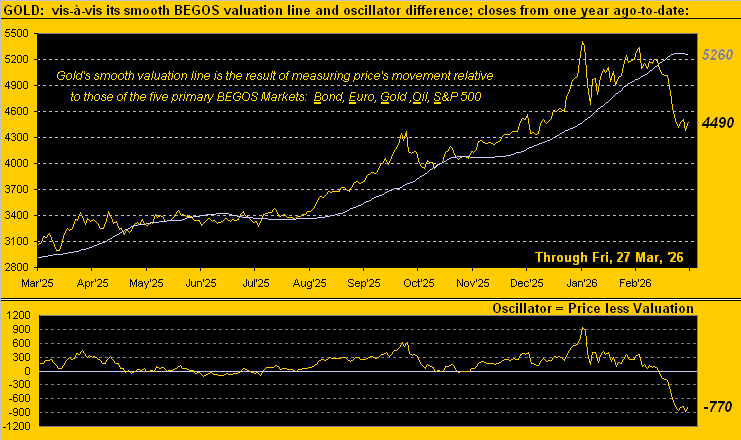

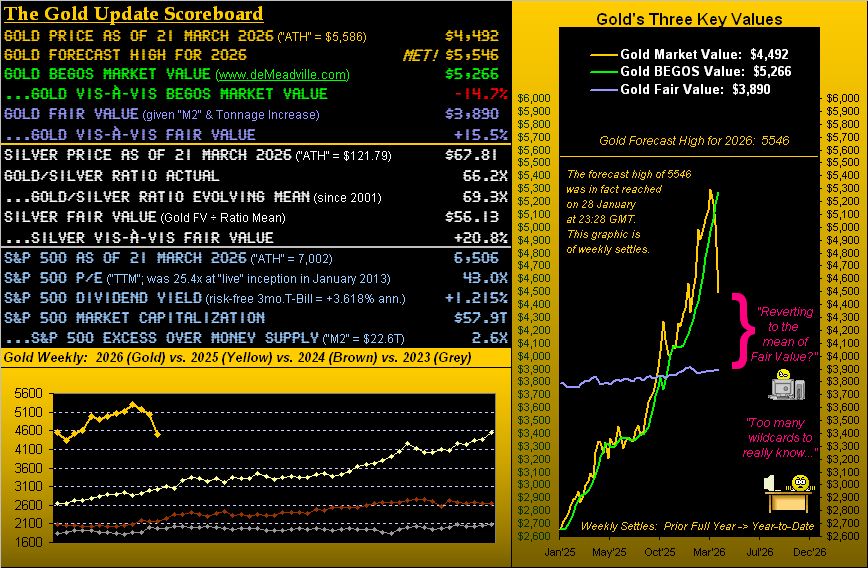

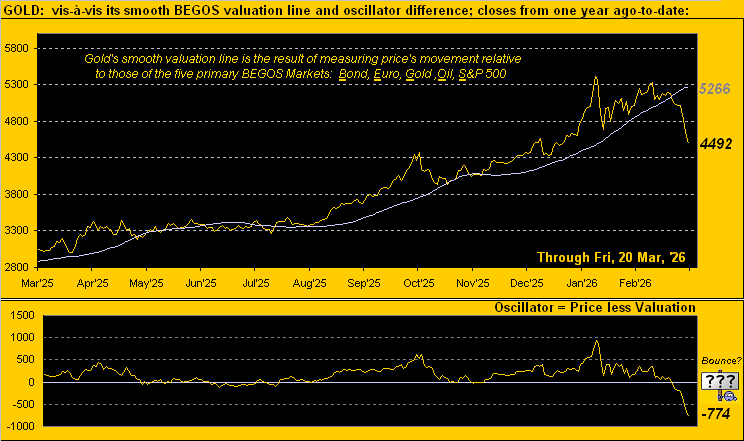

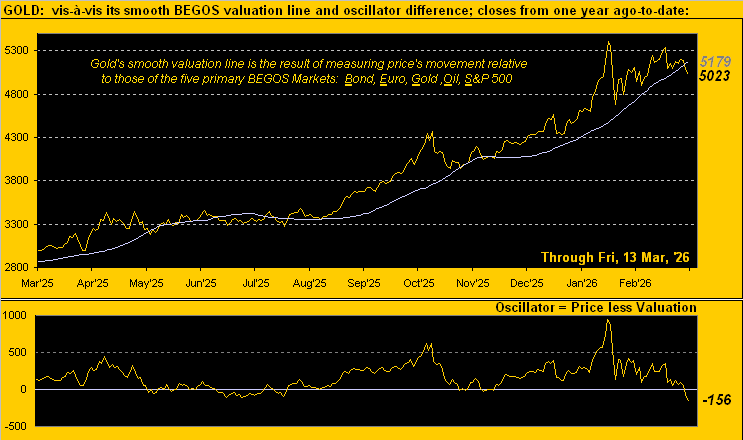

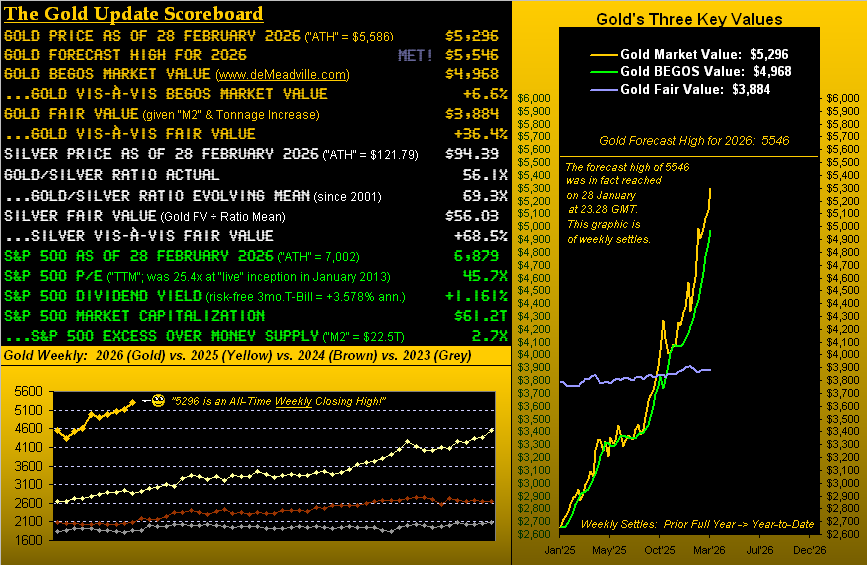

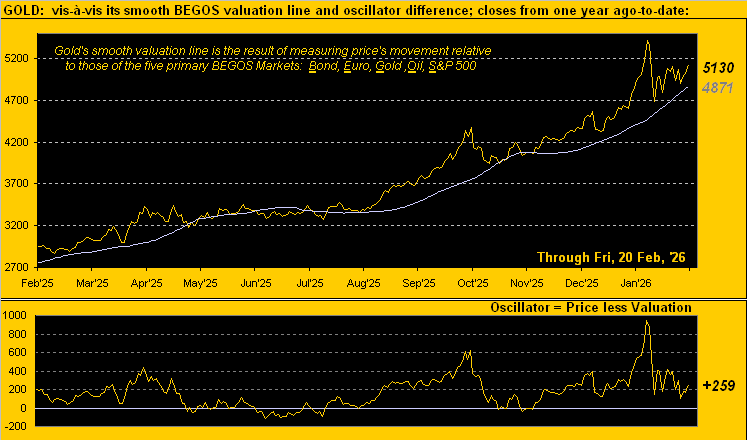

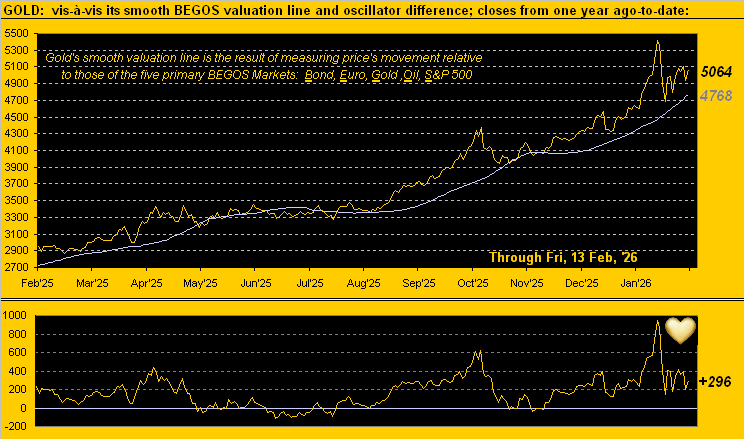

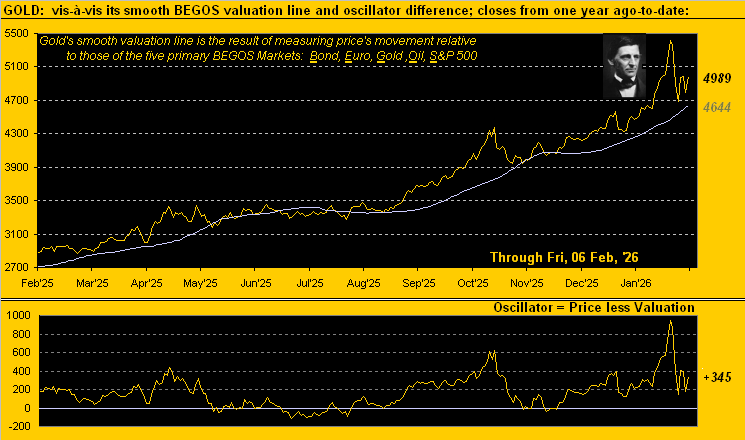

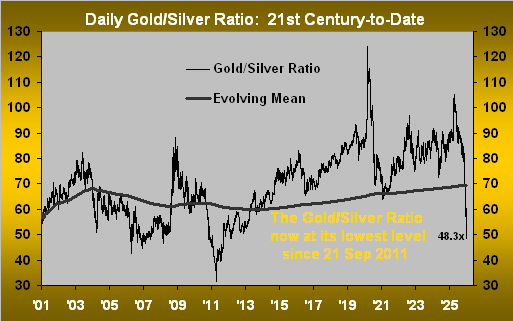

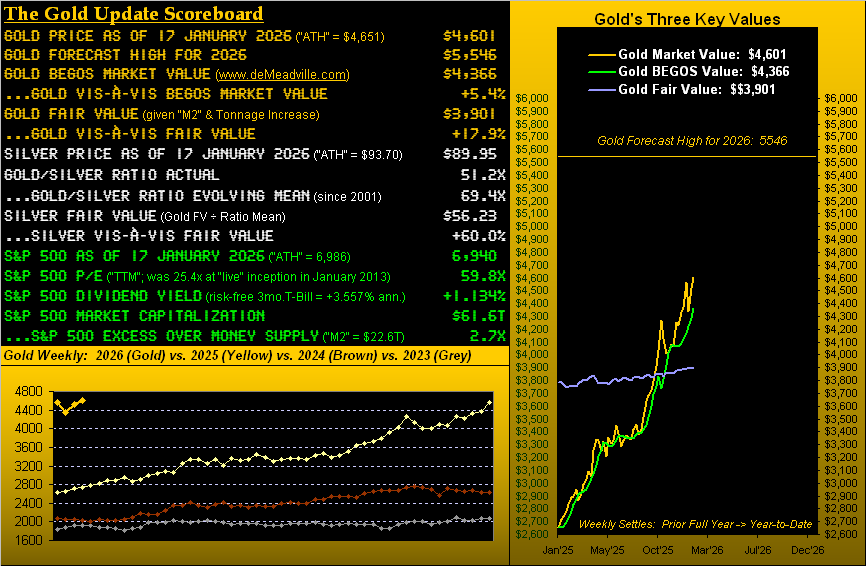

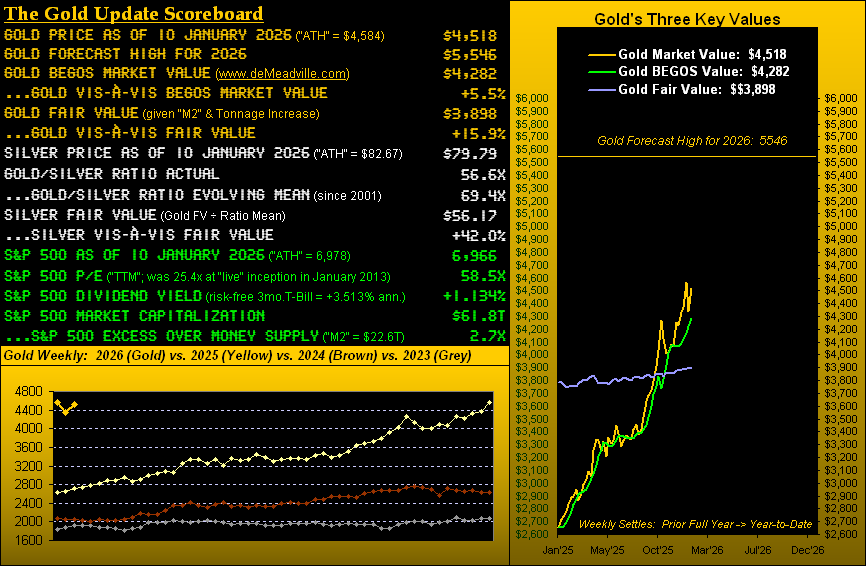

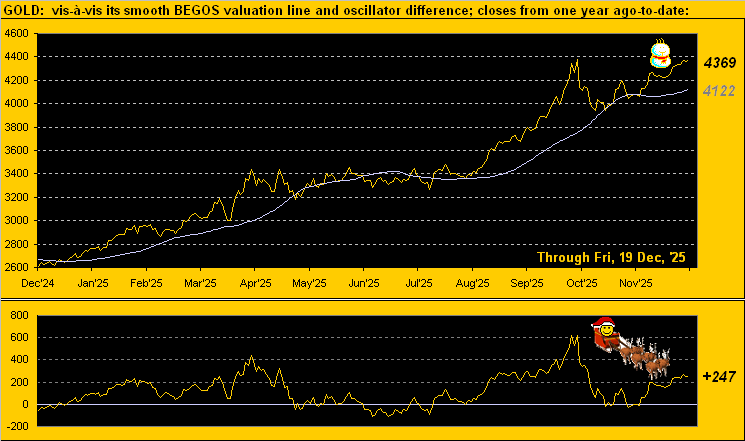

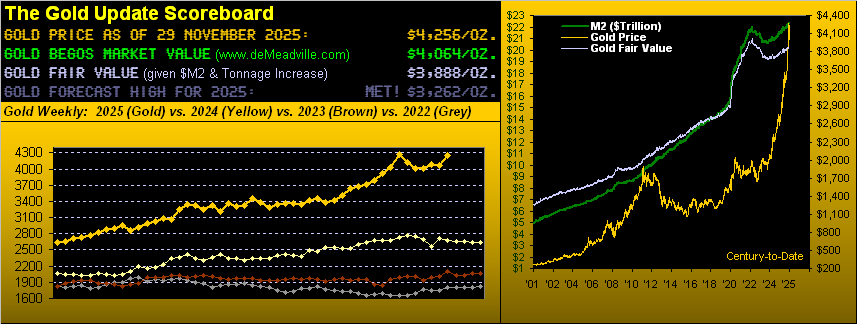

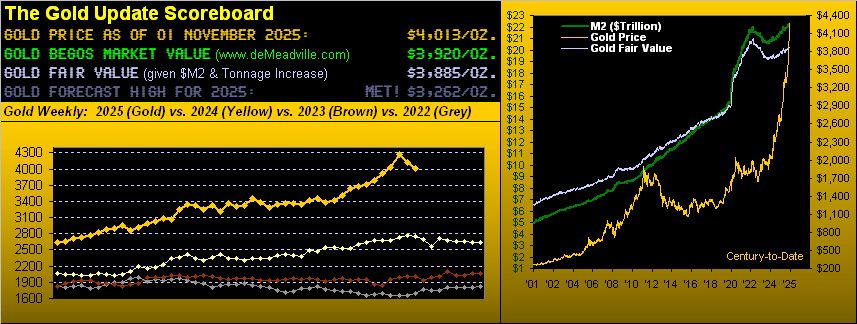

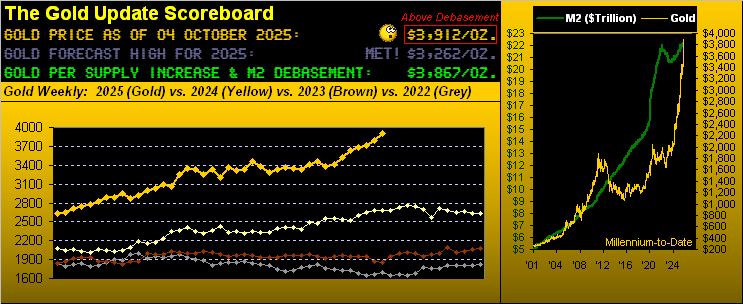

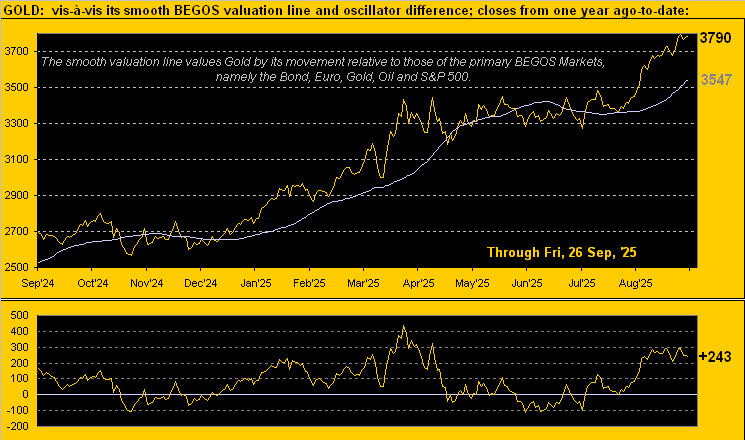

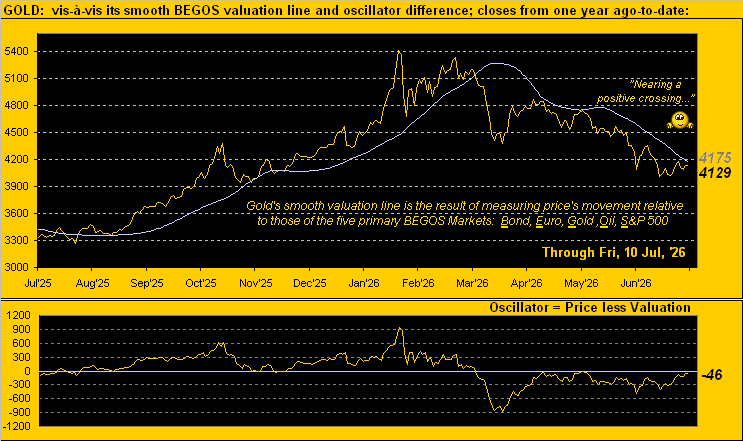

Further, Gold (serendipitously or otherwise) has been fostering friendship with Fair Value.

“That’s ’cause you’ve been pointing it out a lot, mmb… ”

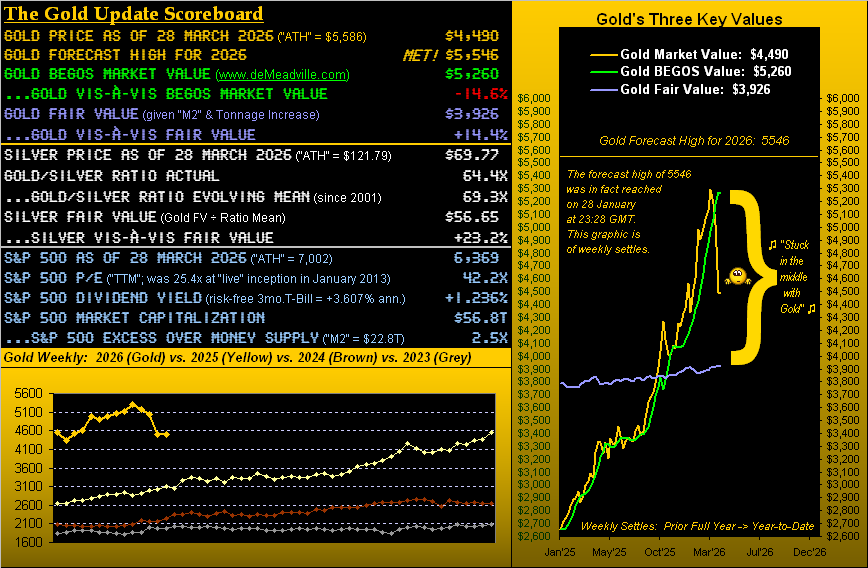

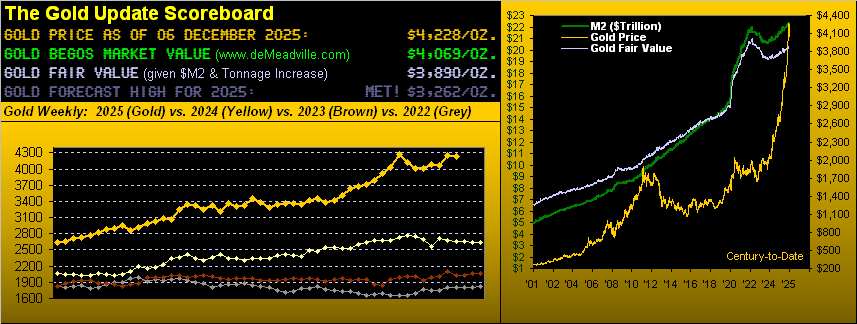

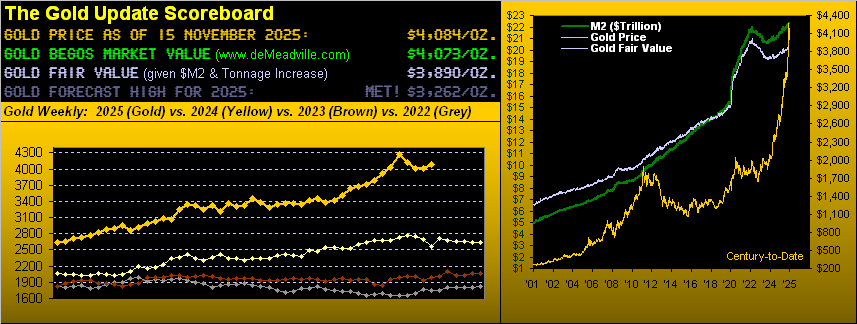

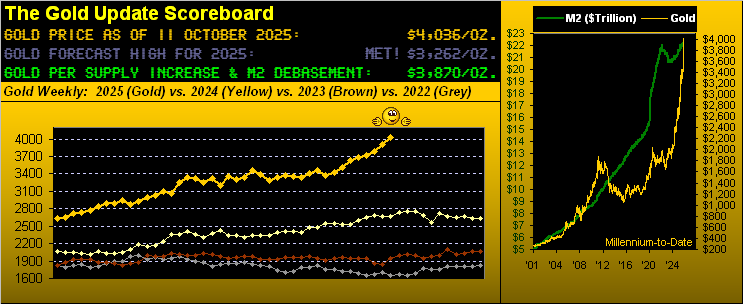

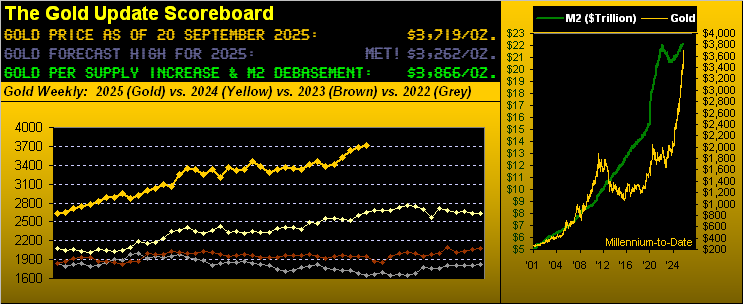

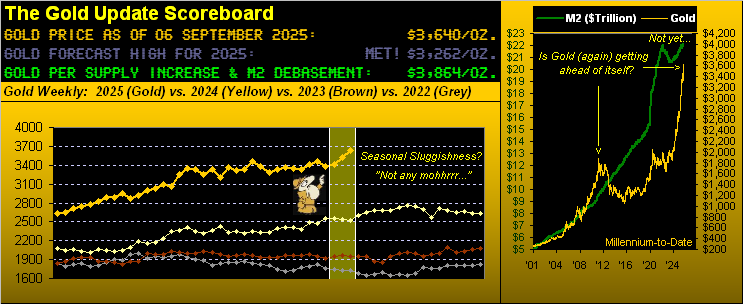

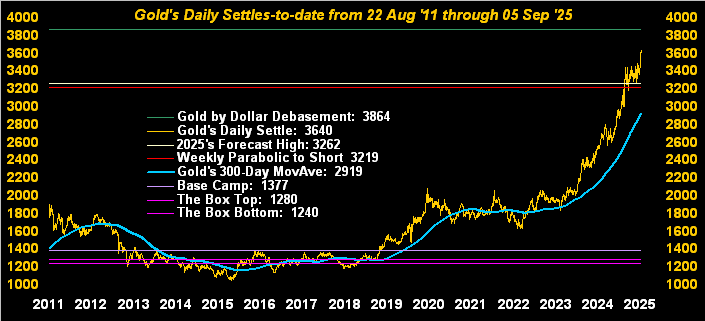

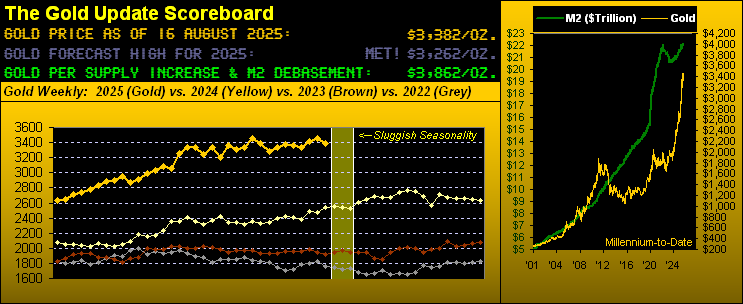

Squire, we appreciate the supportive comment. Either way, Fair Value remains our favoured — albeit the most particularly ponderous measure — for reasonable Gold valuation. To be sure, Fair Value shall be a bit of a laggard to the actual price of Gold upon the Federal Reserve having to bail out both the U.S. Treasury’s debt and to fund investment banking coffers (thus avoiding your receiving an I.O.U. instead of cash upon selling your stock) given the ratio of the S&P 500’s market capitalization/liquid money supply is now 2.8x (per the opening Scoreboard). In the offing then comes five-figure Gold, as previously we’ve herein foretold.

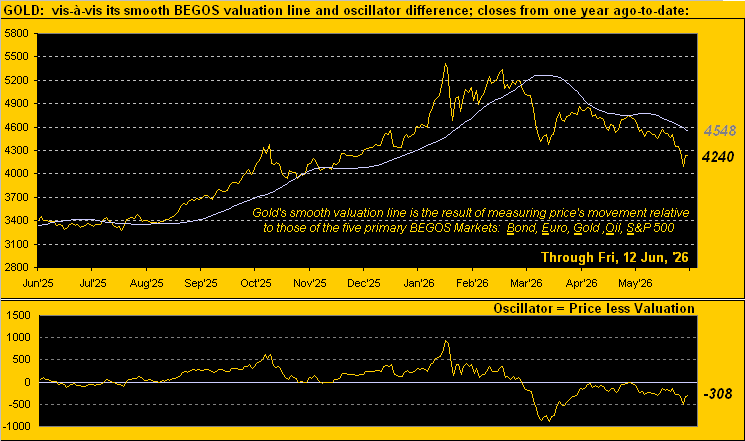

But again, the beauty of Fair Value (barring a deflationary depression and a sapping/reinvention of the money supply) is that it rises over the long haul. Yes, since President Nixon nixed the Gold Standard back on 15 August 1971, the price of Gold has typically trailed Fair Value, only to have dramatically caught up — and then some (understatement) — upon Gold last year having “morphed into a meme stock” as the trading herd changed the yellow metal’s status from “Relic” to “Must have it!”

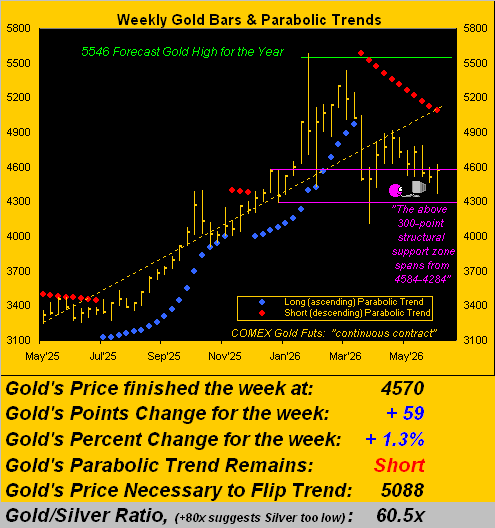

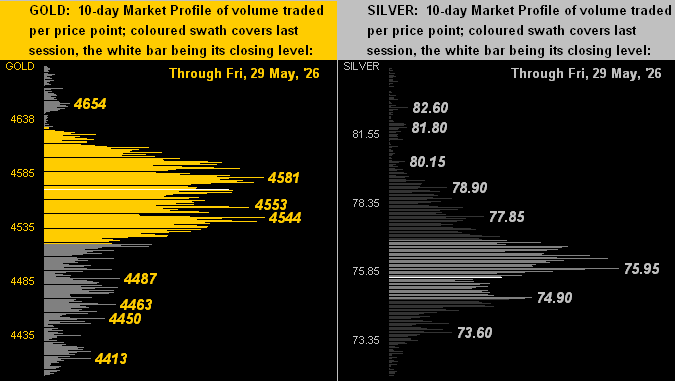

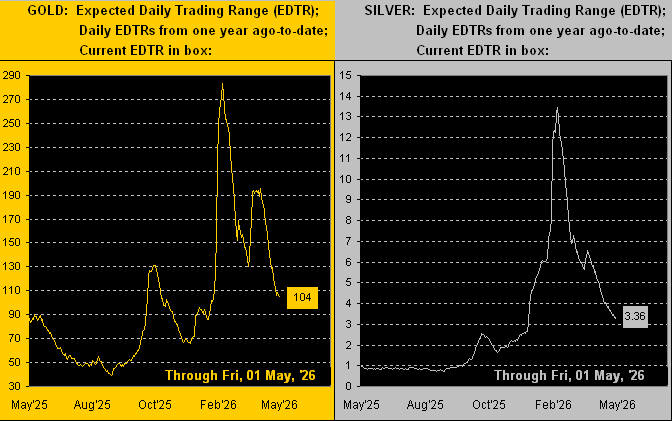

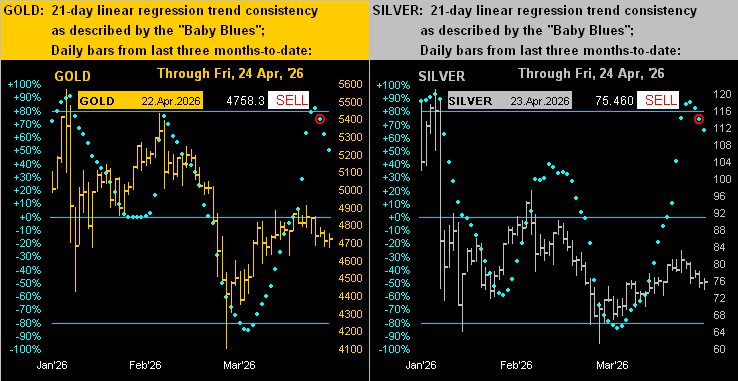

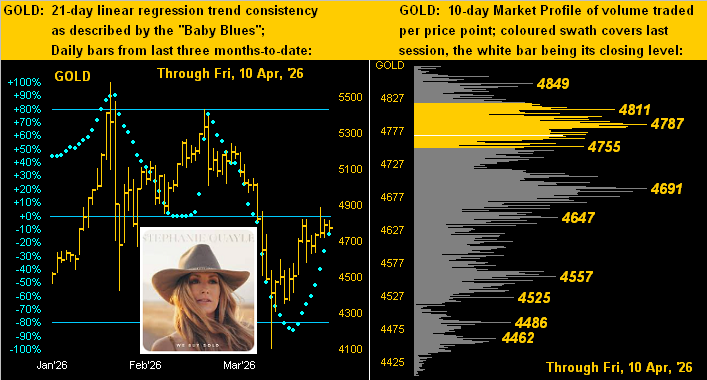

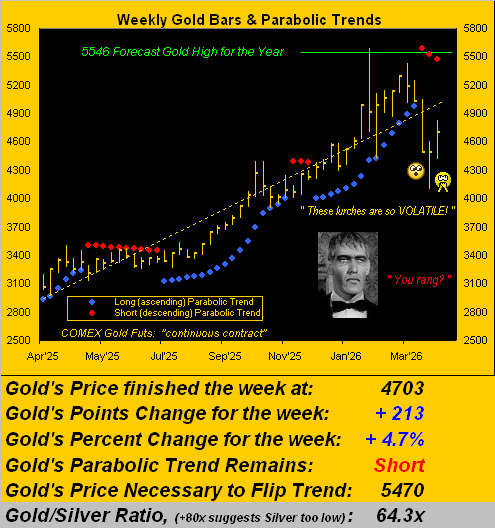

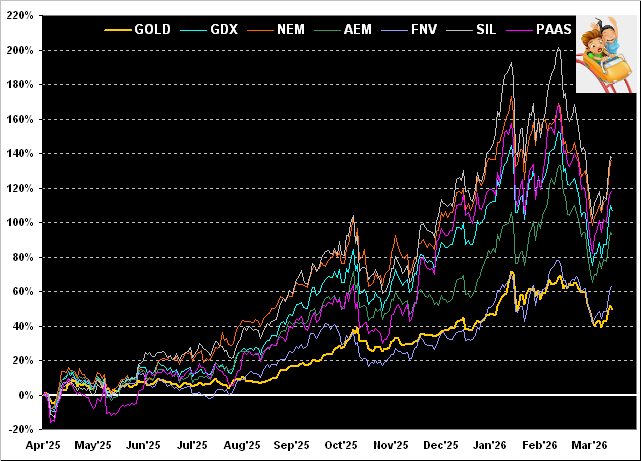

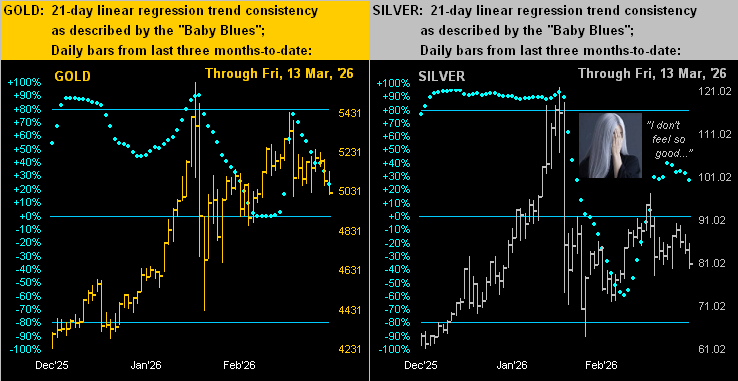

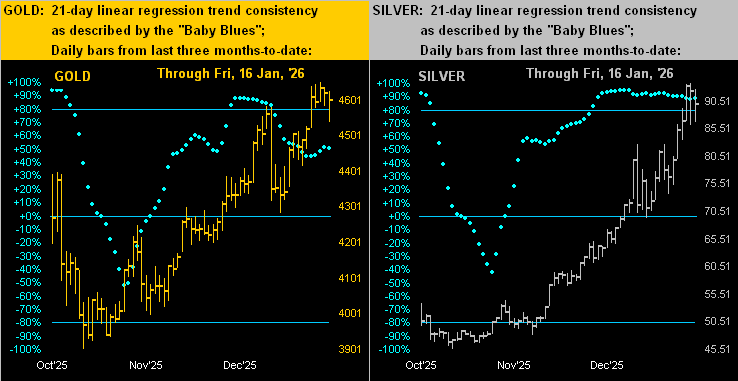

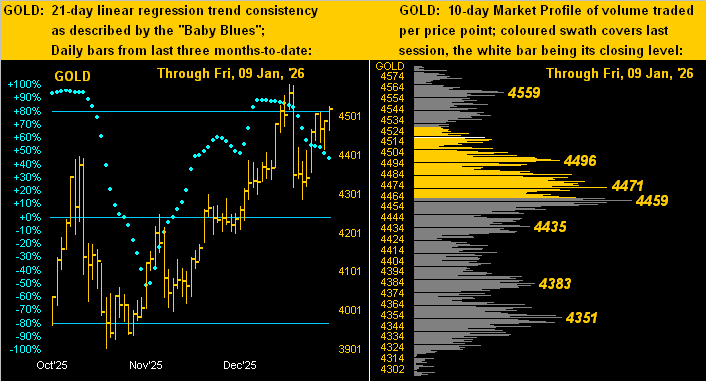

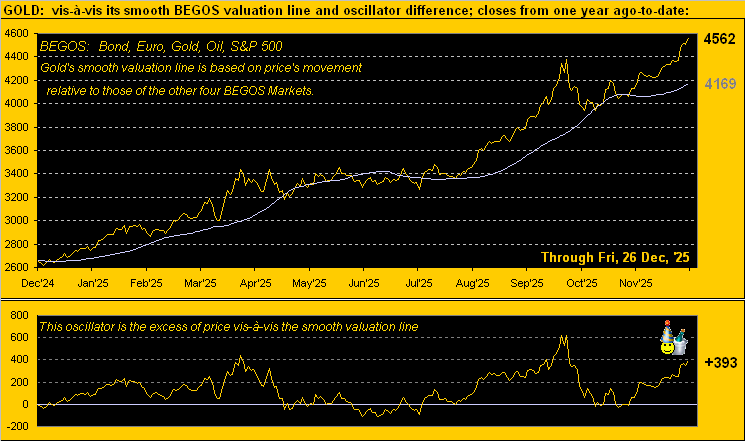

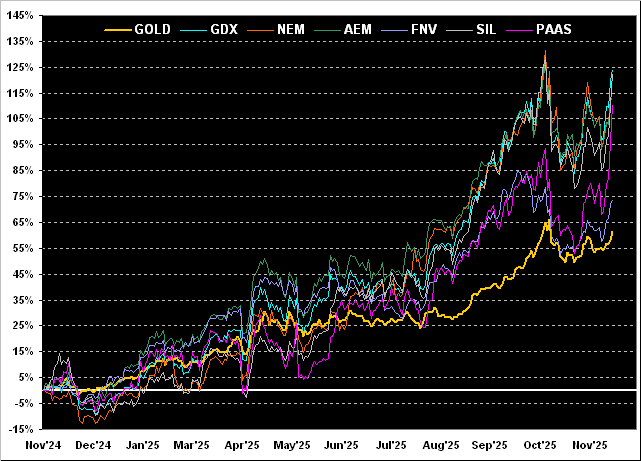

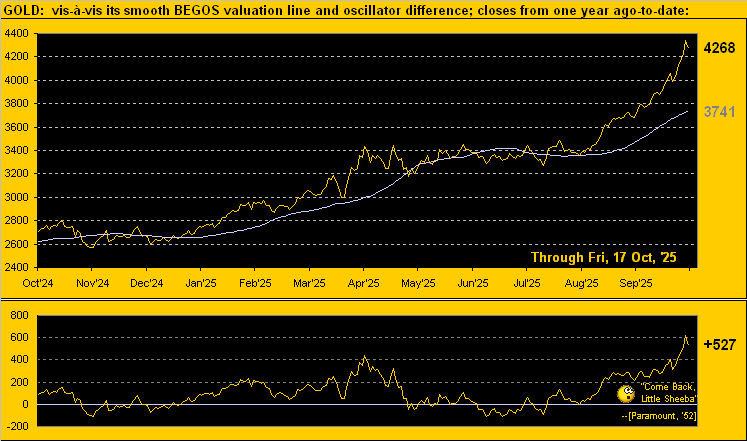

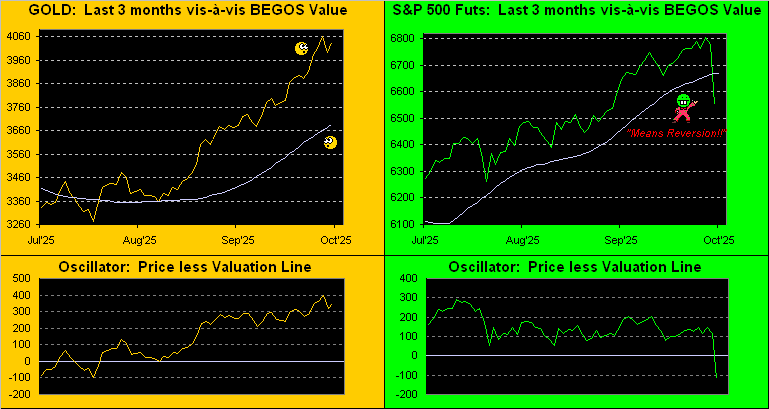

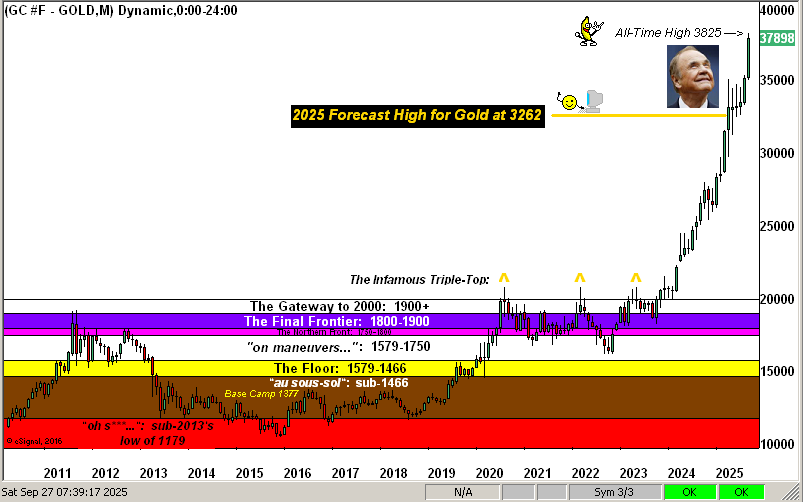

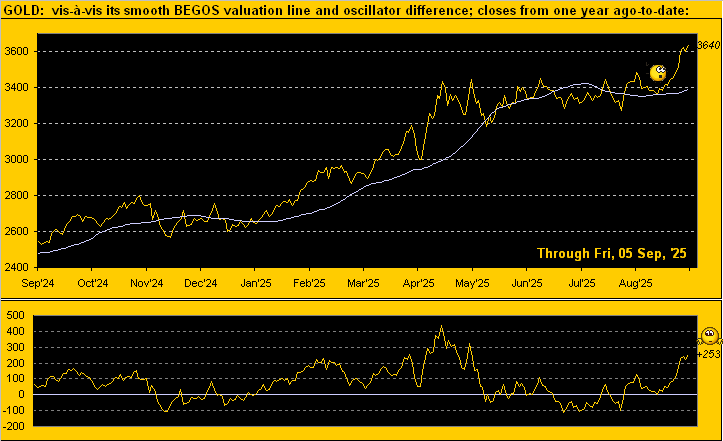

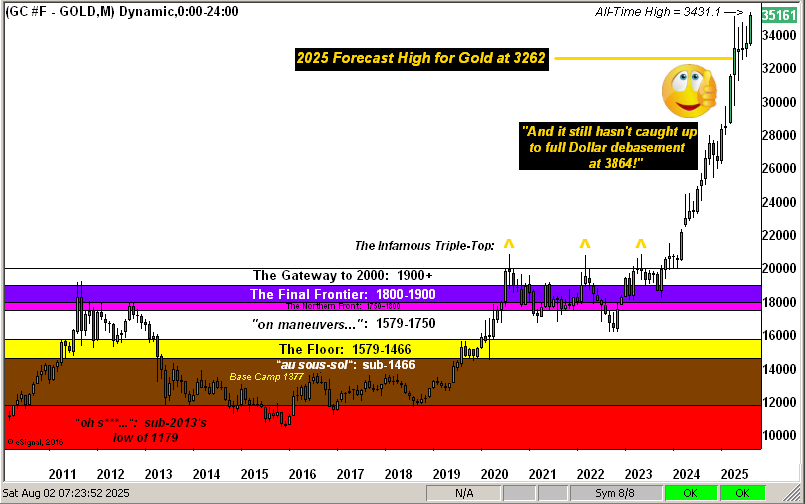

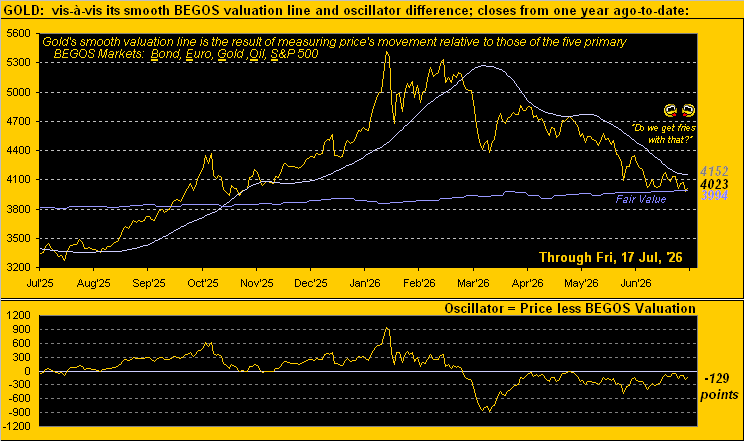

All that said, we oft think of Gold as an attractive, very long-term buy when trading at or below Fair Value. Here from one year ago-to date are Gold’s daily bars and gradually rising Fair Value line. Note therein Fair Value’s rightmost “supportive” nature of late:

Be that as it may, the wildcard remains the war which from one day to the next waxes and wanes on that being said from behind the White House’s window panes. Cue The Temptations’ hit from back in 1970: ![]() “Ball of Confusion (That’s What the World Is Today)”

“Ball of Confusion (That’s What the World Is Today)”![]()

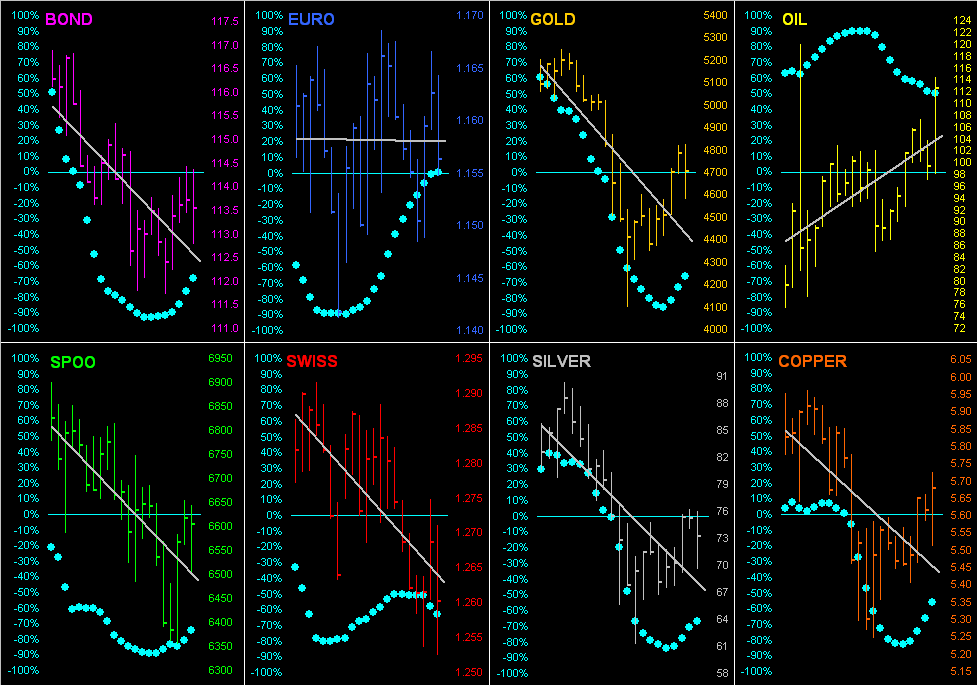

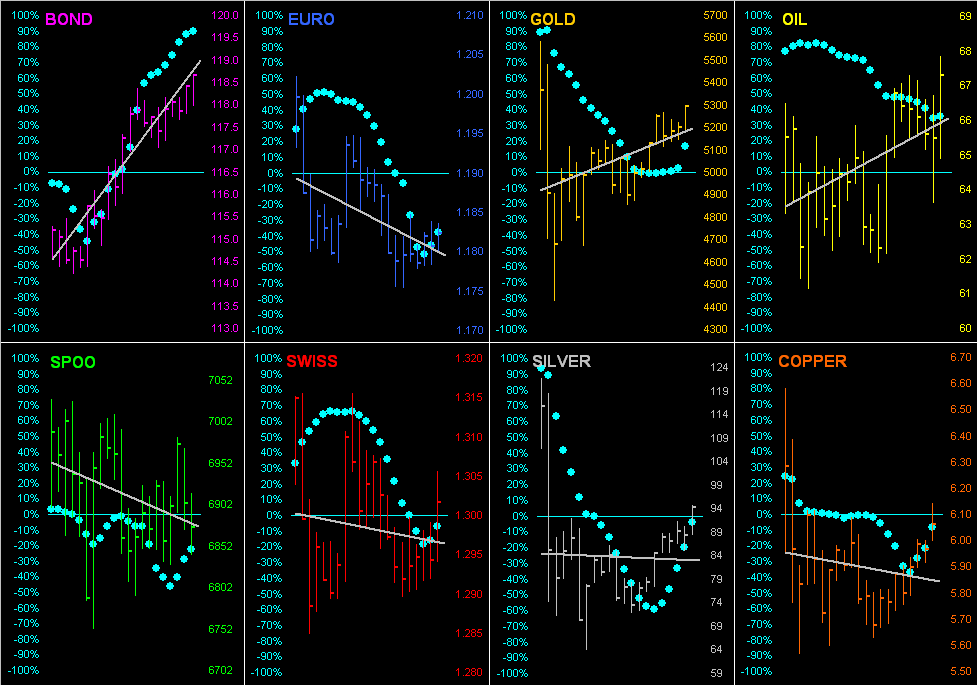

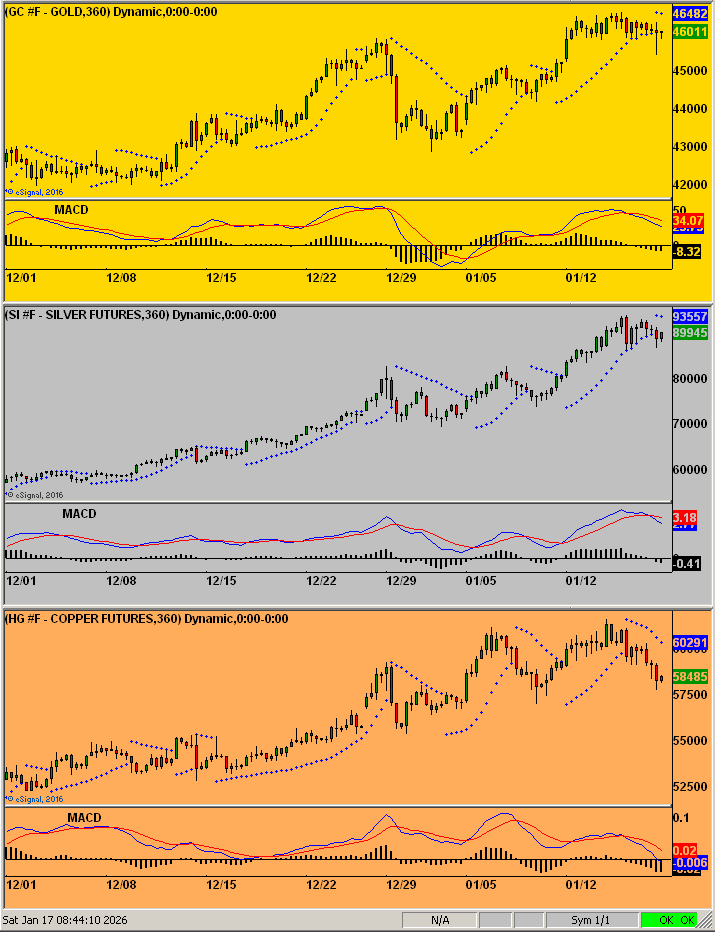

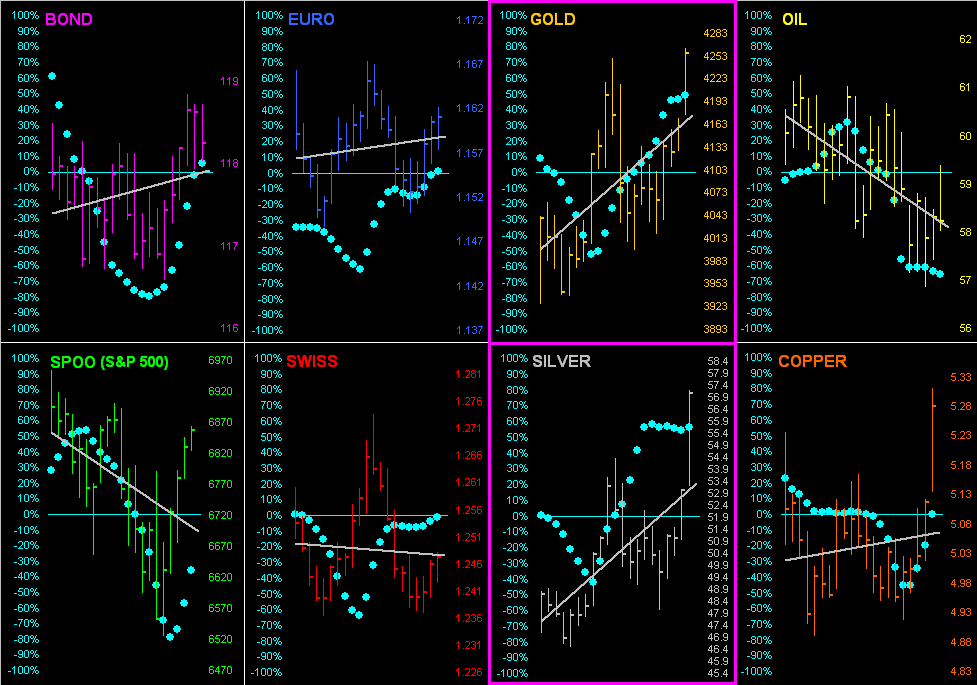

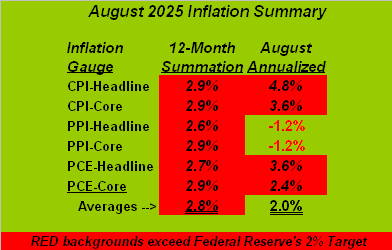

Which is a neat segue into the Economic Barometer. The Baro has been in a confused state for some three months, yet fortunately had a deserved rest this past week as just three incoming metrics arrived, the downer being the Conference Board’s Leading (i.e. “lagging”) Indicators for June. But the month’s New Home Sales beat both consensus and those for May, which also were revised higher. Moreover came the math-challenged FinMedia excitedly reporting that Initial Jobless Claims for the week ending 18 July at 187k were the lowest since 1969. Wrong: since the Baro’s inception in 1998, there’ve been not one but seven other weeks of less Claims, the least being 167K for the week ending 02 April 2022. (Still watching that FinTV, Bunky? Bummer). Here’s the Baro:

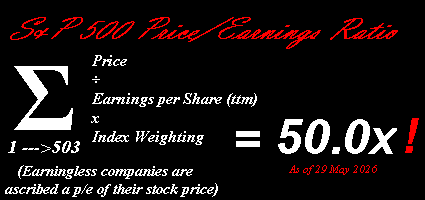

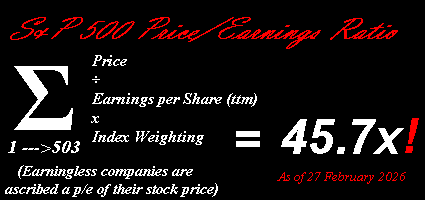

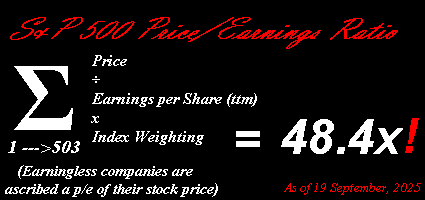

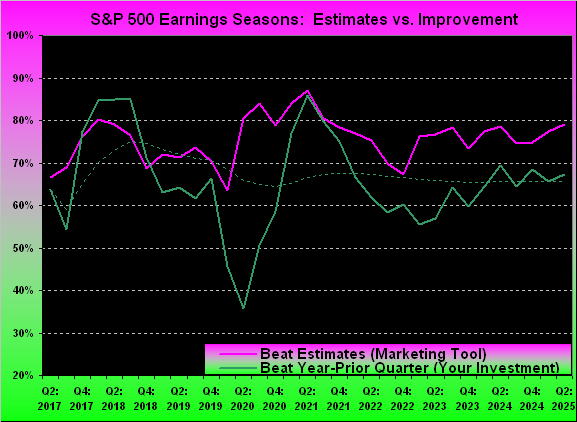

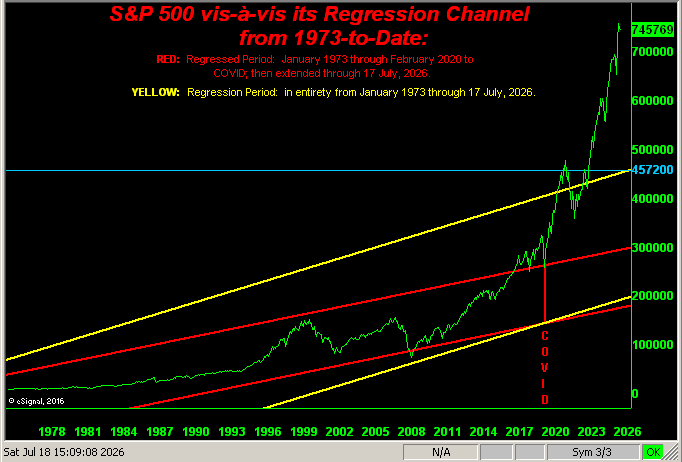

With respect to stocks, yesterday we received a solicitory email with the subject “Are you ready for the crash?” We’ve been ready for four years. “Oh, but earnings season is so great!”, they say. Year-over-year, yes, thus far ’tis “great”. Of the 118 S&P 500 constituents having reported, 85% (100) have recorded bottom-line improvement. However, from “The Record Needle is Stuck Dept.”, we again point out that to sustain such excessive levels of prices, earnings ought be doubling, if not tripling.

“But they’re not, right mmb?”

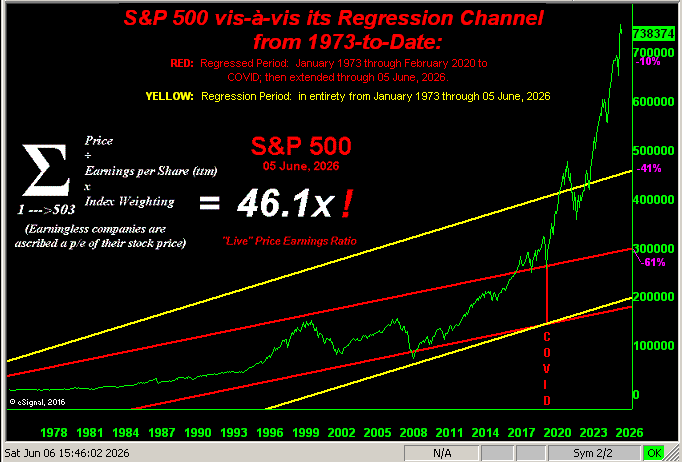

No they’re not, Squire, although the S&P’s “live” price/earnings ratio has come down a bit through these first three weeks of Q2 Earnings Season from 46.5x to now 42.2x (again per our opening Scoreboard). For you WestPalmBeachers down there, that means if you buy the S&P today, you’re paying $42.20 for something that earns $1.00. Sure, one can add in the teeny 1.133% dividend yield, but prices (believe it or not) can actually go south. ‘Course, they always come back, right? Recall it took the S&P 500 a mere 13 years to record a 2% peak-to-peak gain from 2000 into 2013 … just in case you’re scoring at home.

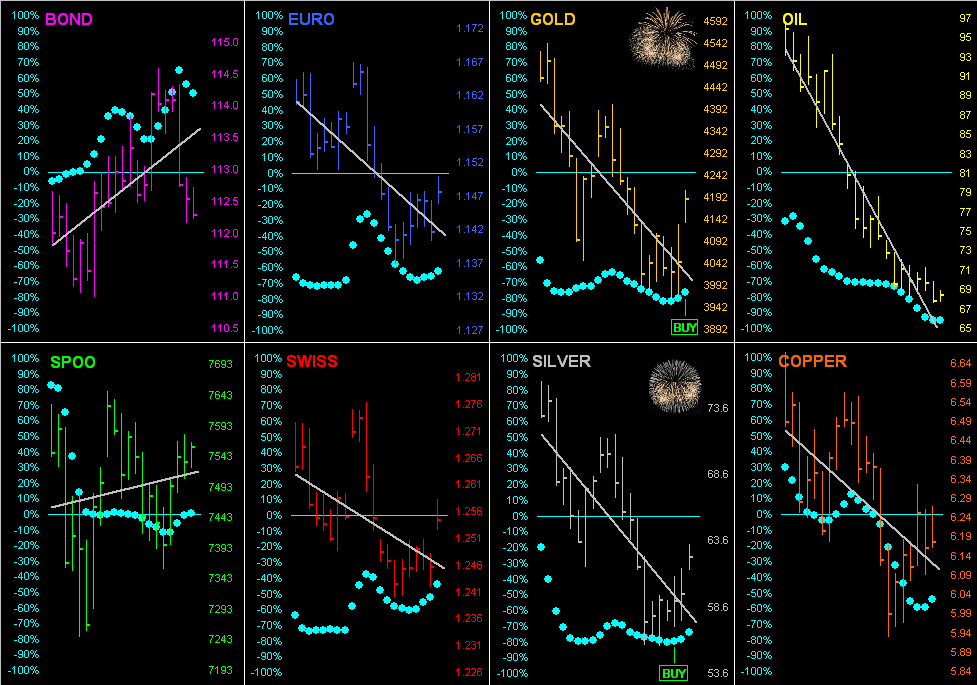

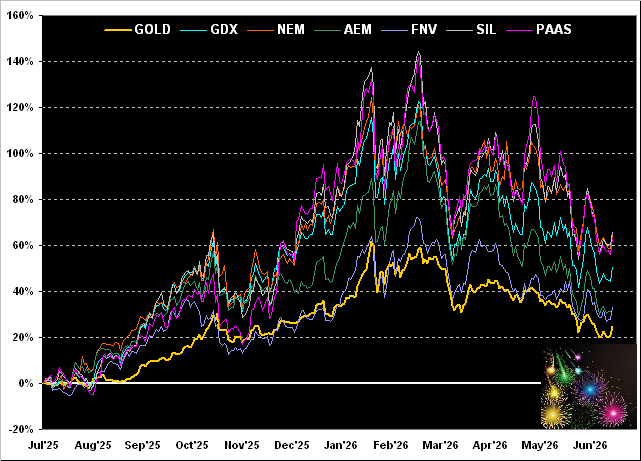

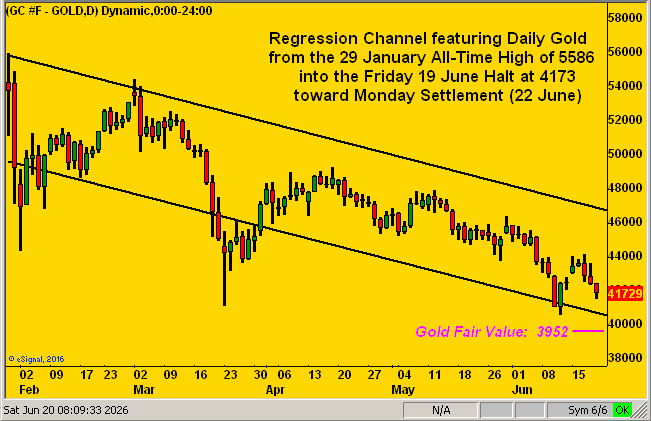

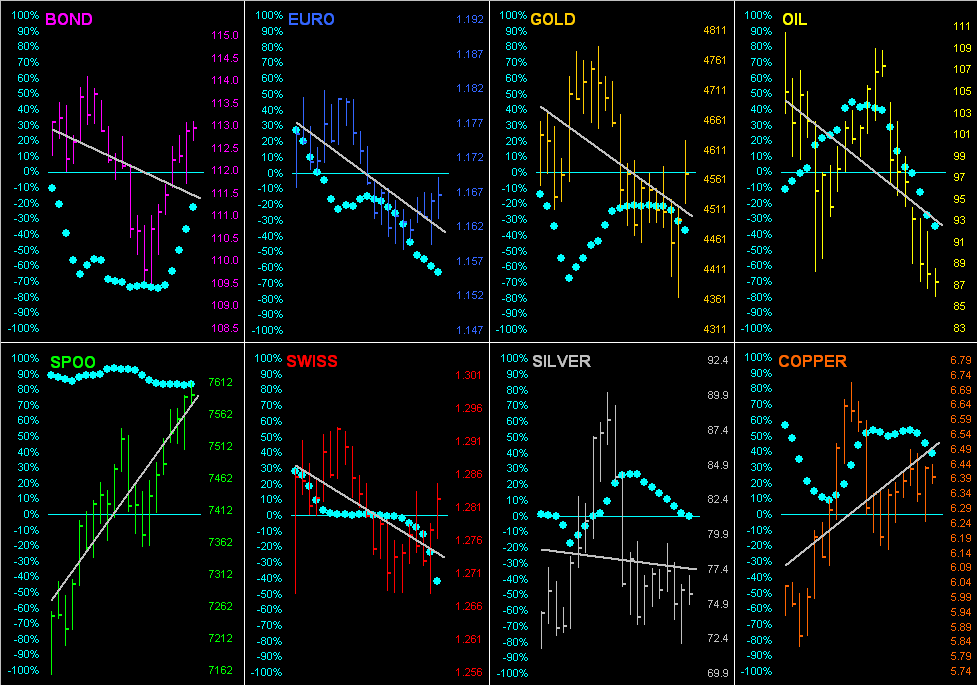

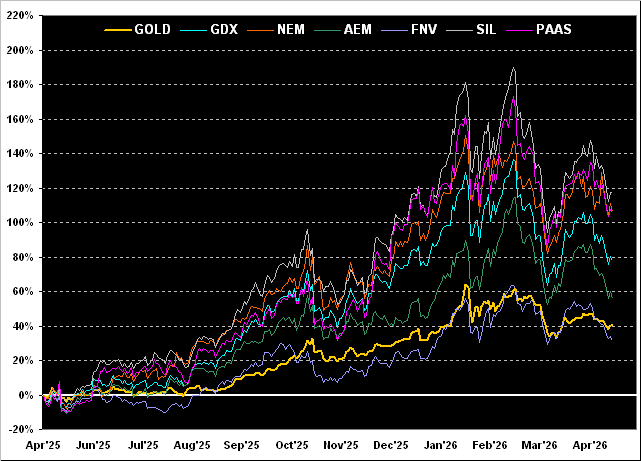

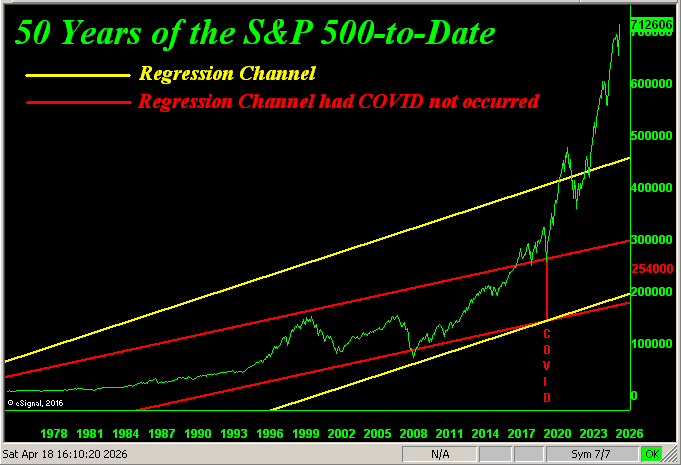

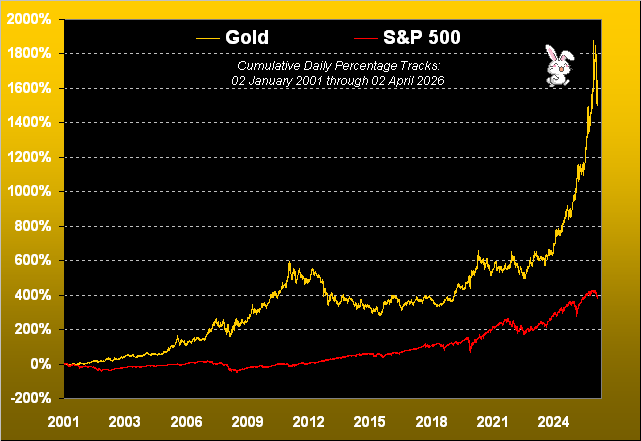

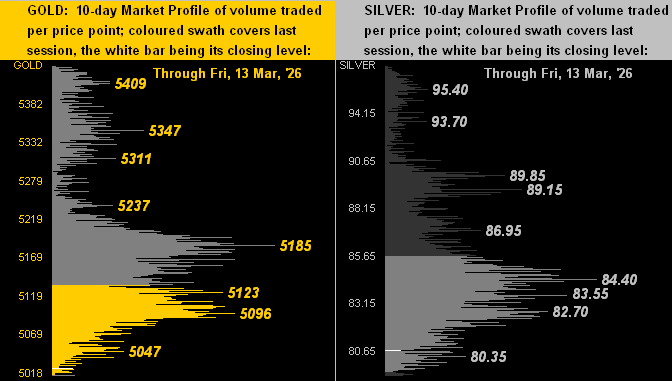

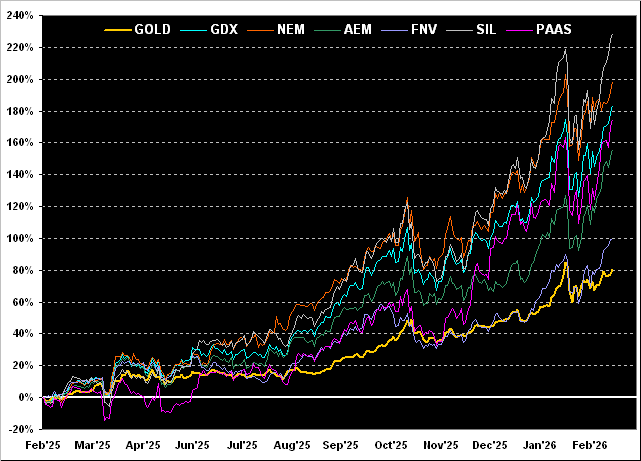

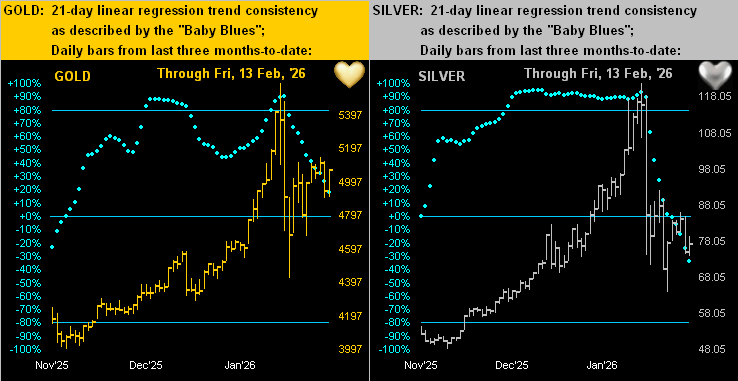

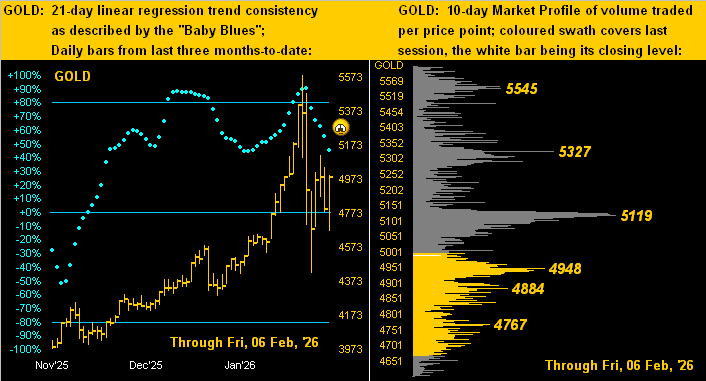

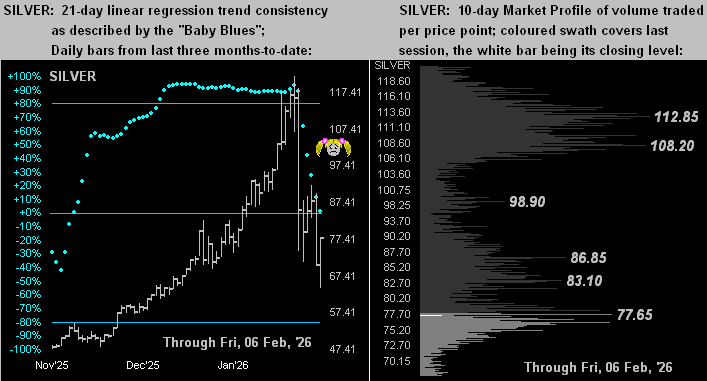

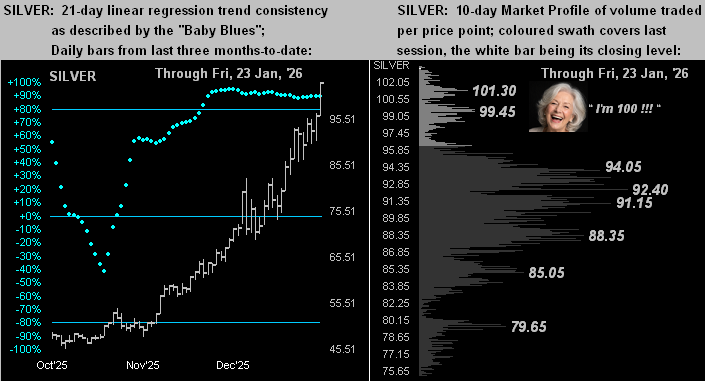

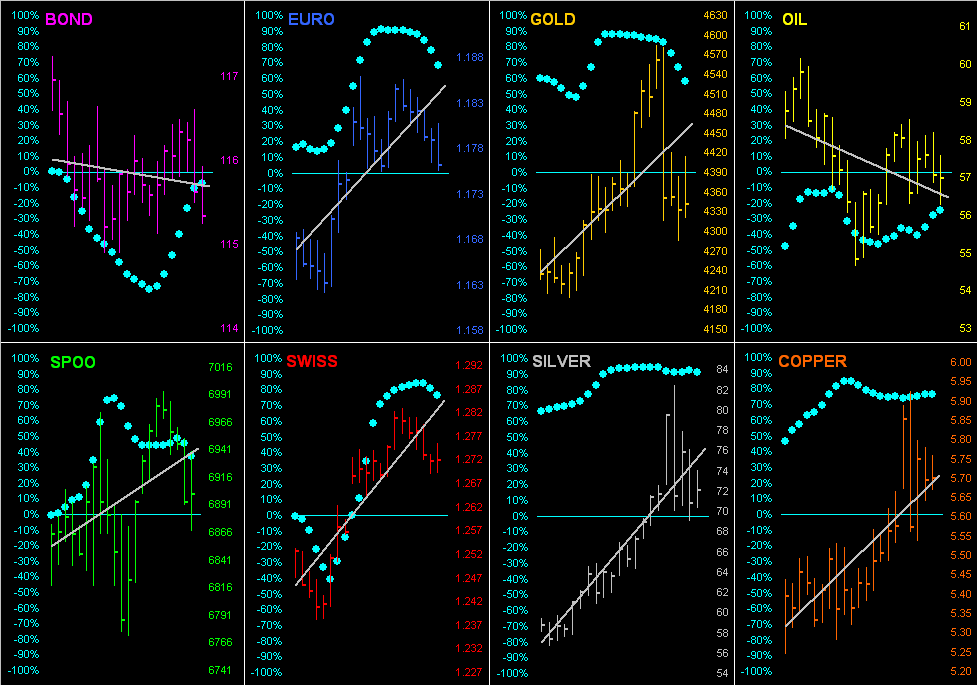

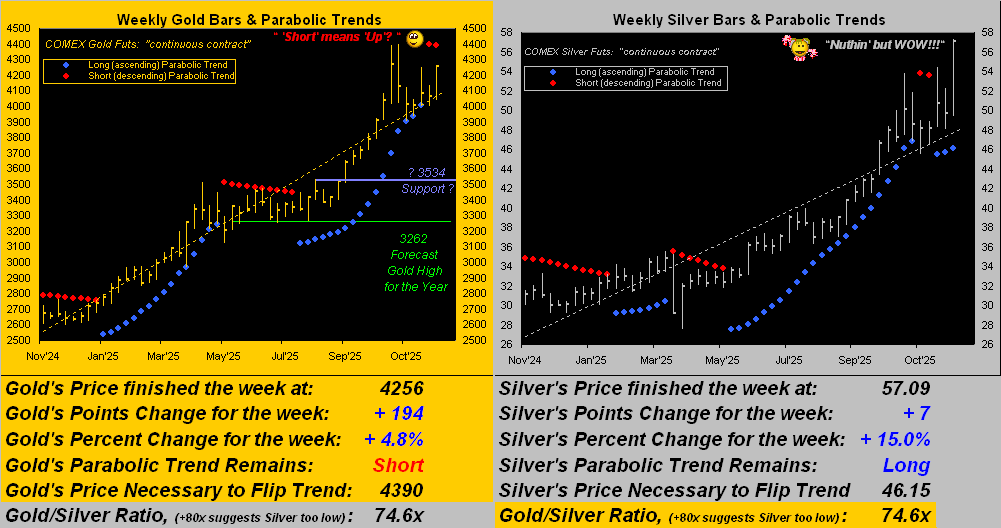

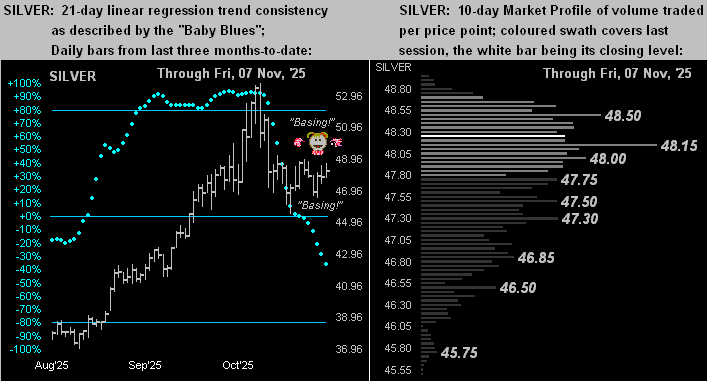

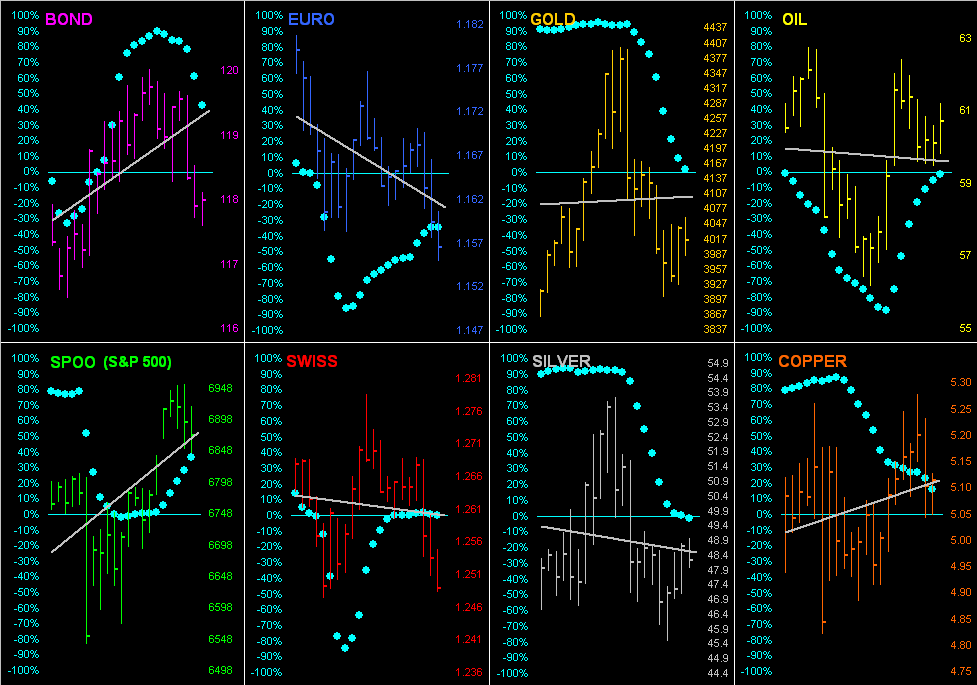

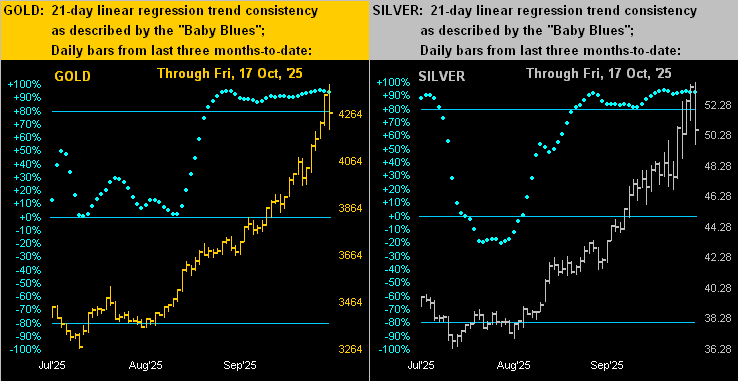

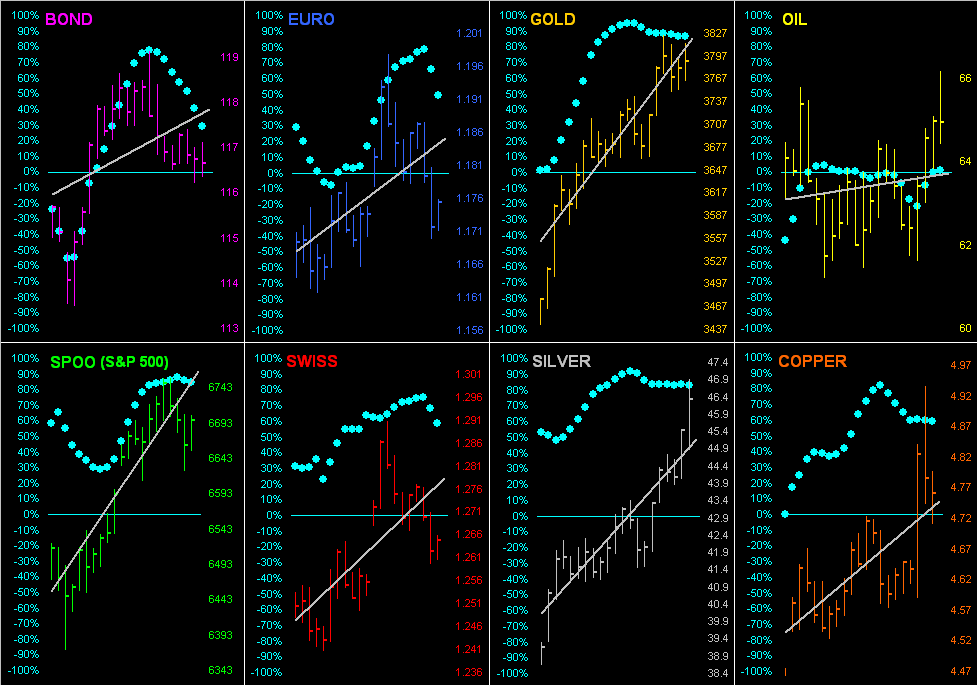

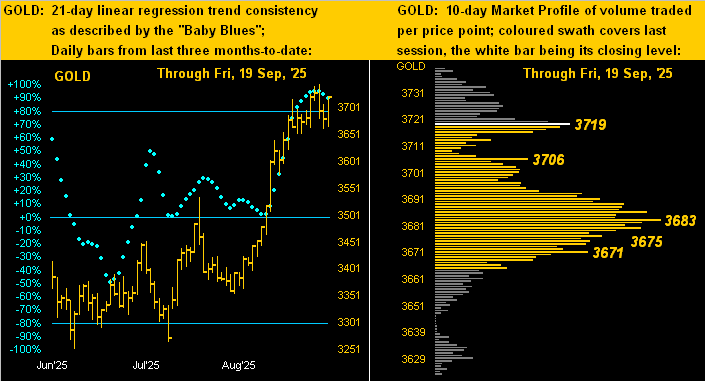

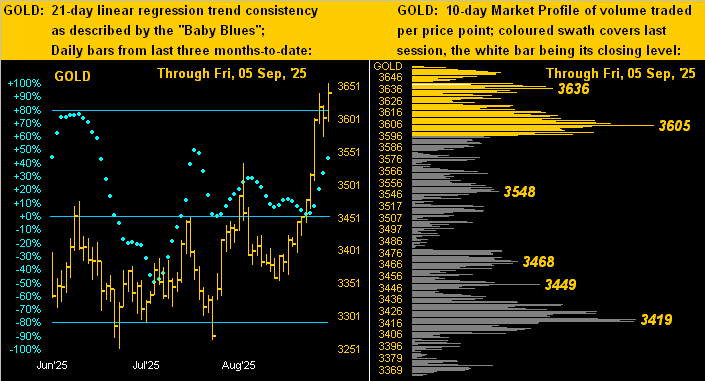

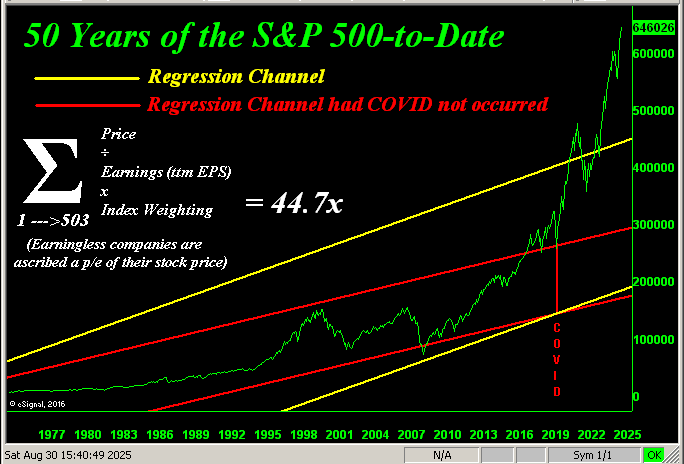

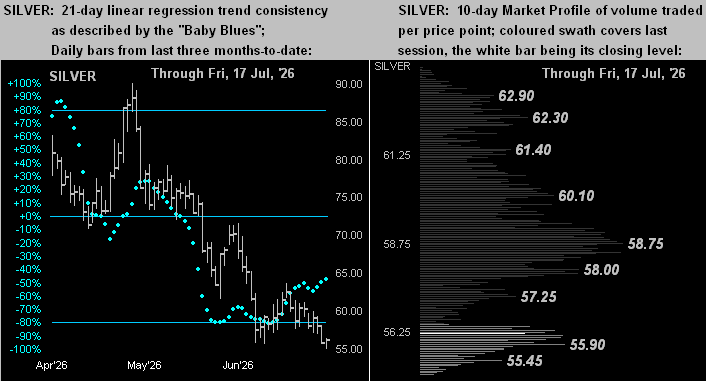

Obviously we find this more preferential:

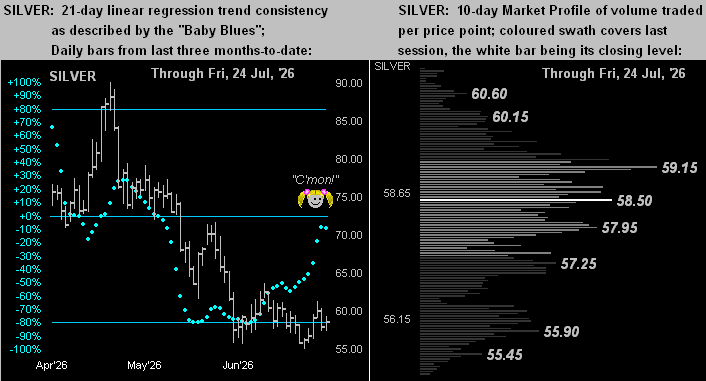

Quick note: Next week’s 872nd consecutive Saturday edition of The Gold Update shall likely be composed on somewhat of a short time fuse. Still, it being a month-end missive, ’twill contain all the graphics you expect to see with just a bit less verbosity, but to the point. On verra … and for Gold and Silver, hopefully a “Hurrah!” for finding a floor!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

.png)