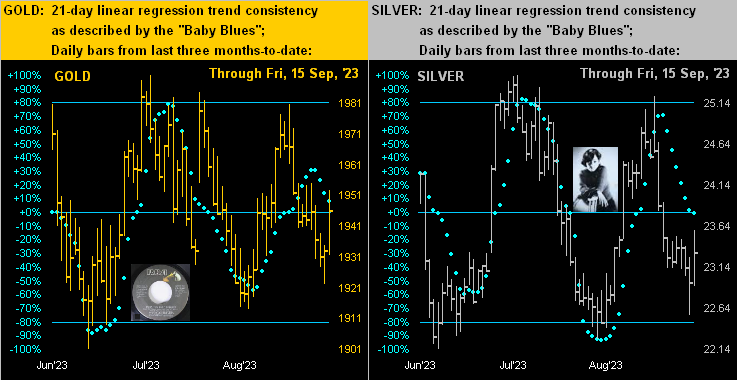

As for the precious metals from three months ago-to-date, here next we’ve their daily bars along with those “Baby Blues” that depict the consistency of the evolving 21-day linear regression trend. For both Gold on the left and Silver on the right, the baby blue dots are falling, which does not lend well to price’s firming and turning higher. Still, the rightmost bar in each case is indicative of buying interest, which beneath the umbrella of the weekly parabolic Long trend — plus the aforeshown pending MACD positive cross — can combine to ![]() “Turn the beat around…”

“Turn the beat around…” ![]() –[Vicki Sue Robinson, ’76]:

–[Vicki Sue Robinson, ’76]:

Time to wrap with the stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3706

Gold’s All-Time Intra-Day High: 2089 (07 August 2020)

2023’s High: 2085 (04 May)

Gold’s All-Time Closing High: 2075 (06 August 2020)

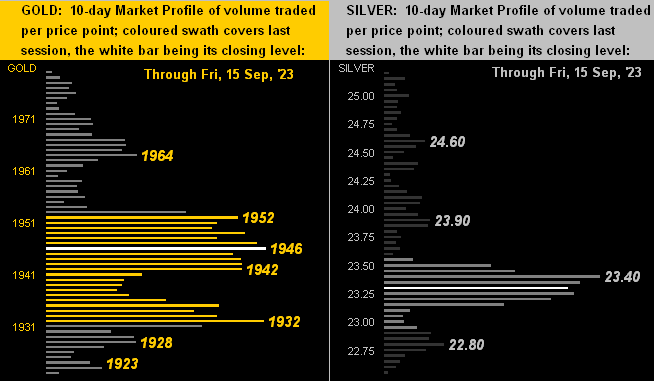

Trading Resistance: 1952 / 1964

Gold Currently: 1946, (expected daily trading range [“EDTR”]: 16 points)

10-Session “volume-weighted” average price magnet: here at 1946

Trading Support: here at 1946, then 1942 / 1932

10-Session directional range: down to 1922 (from 1980) = -58 points or -2.9%

The Weekly Parabolic Price to flip Short: 1904

The Gateway to 2000: 1900+

The 300-Day Moving Average: 1859 and rising

2023’s Low: 1811 (28 February)

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro