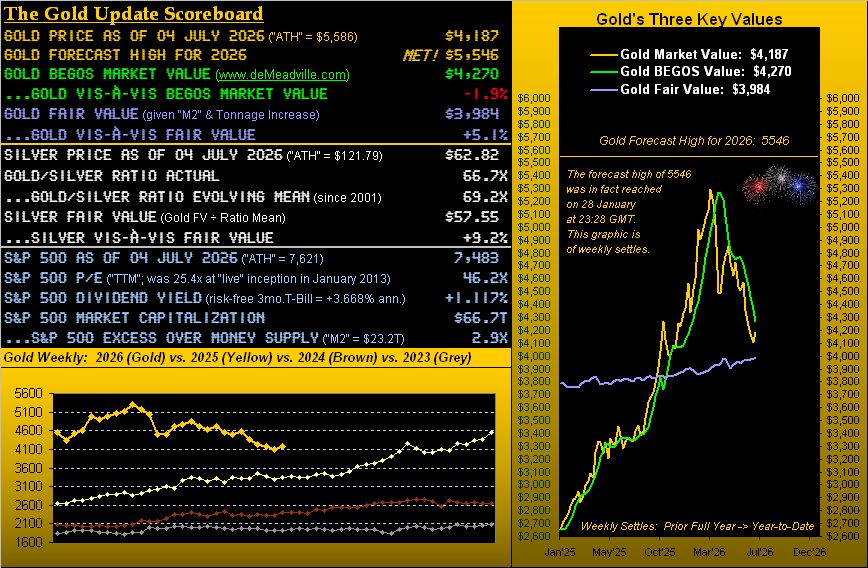

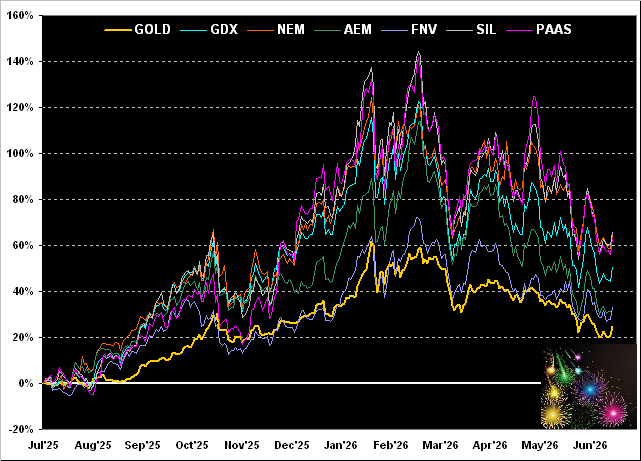

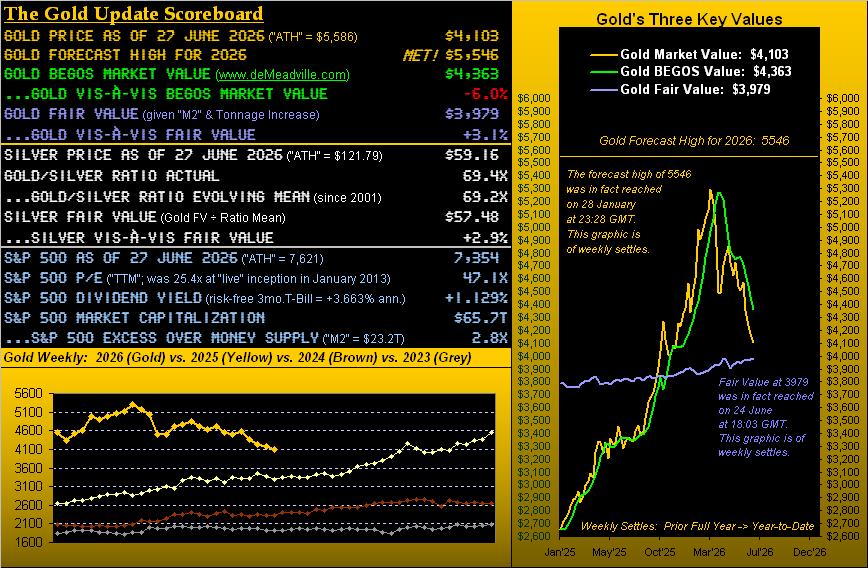

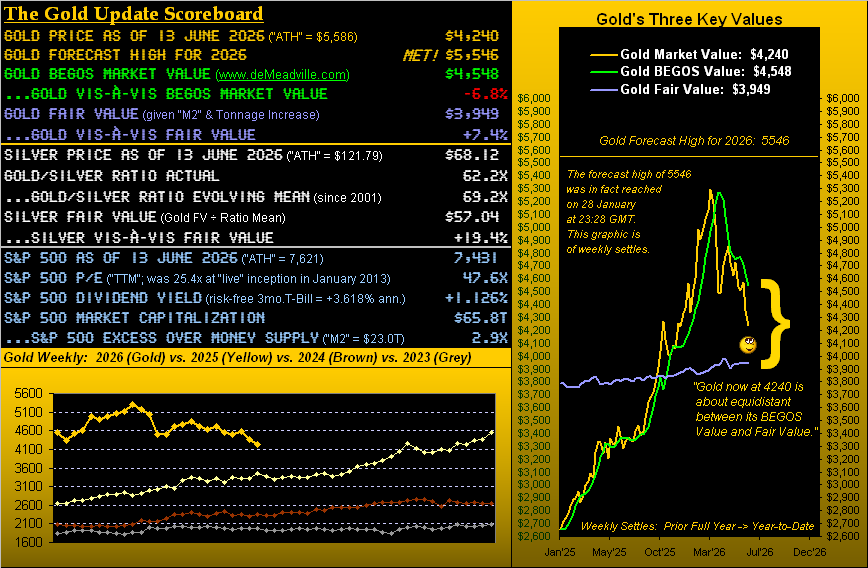

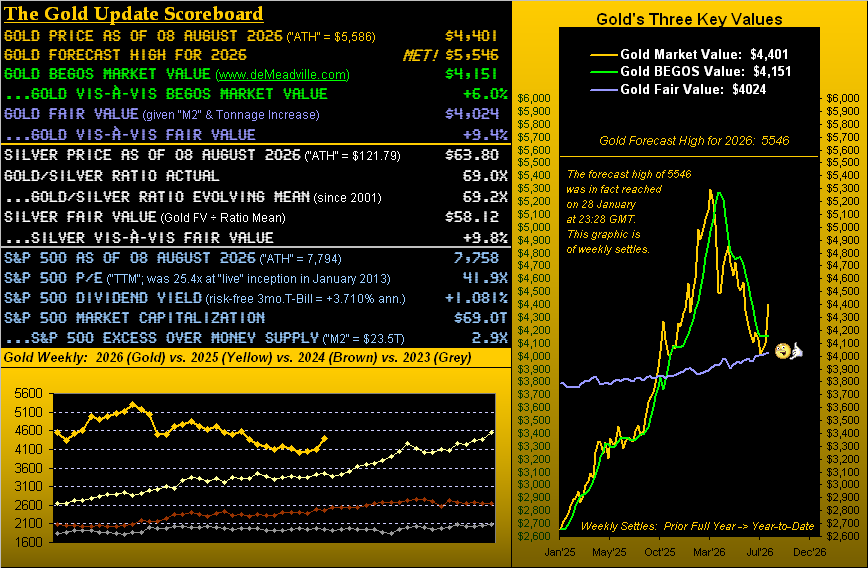

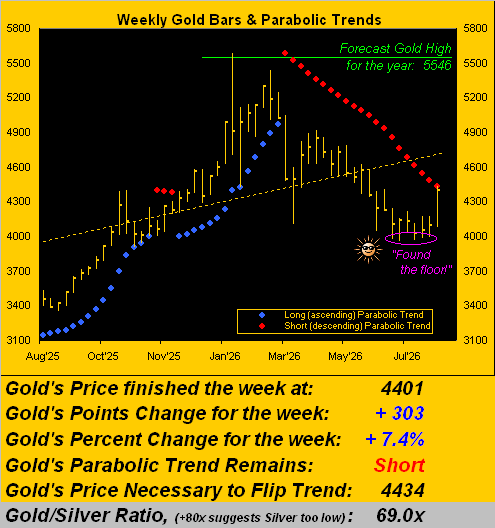

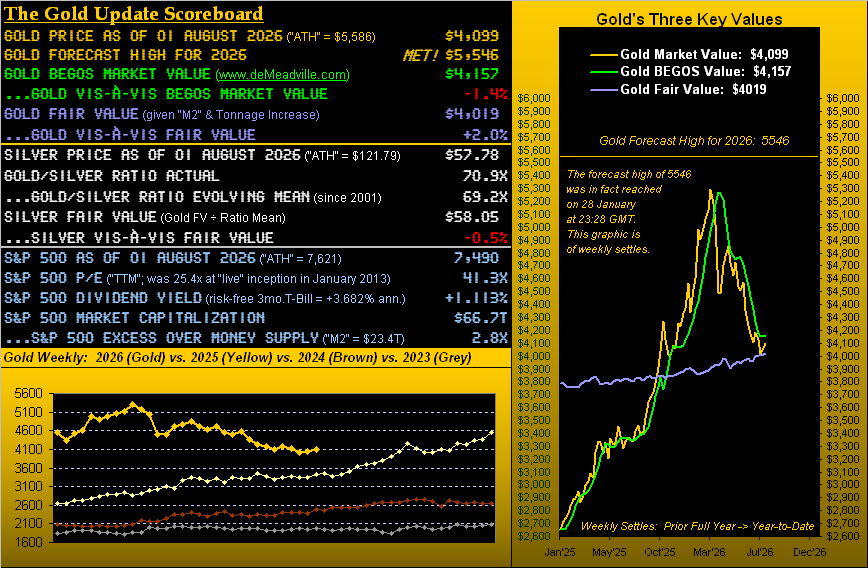

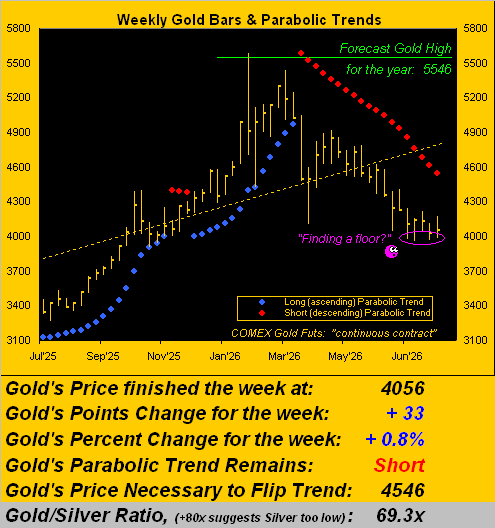

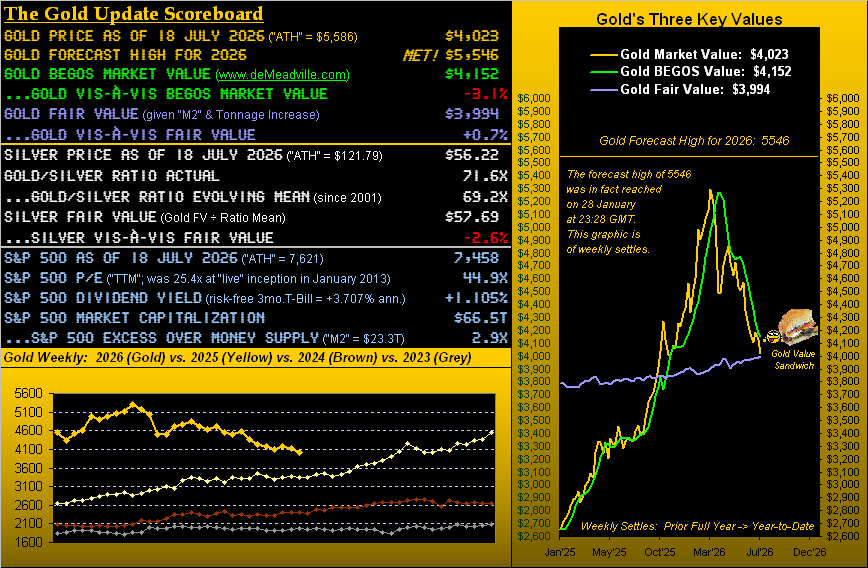

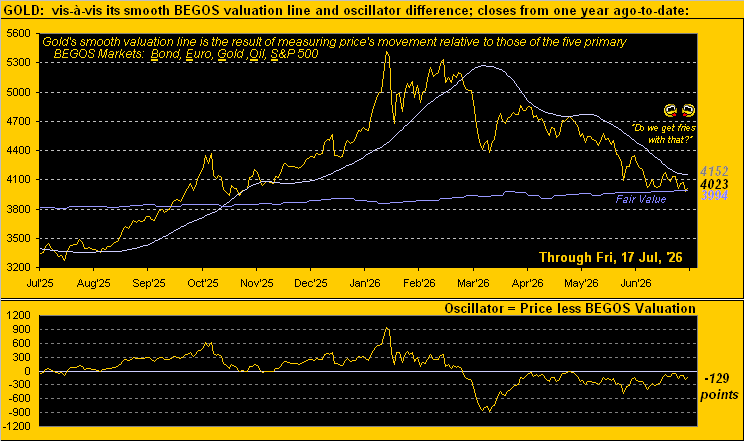

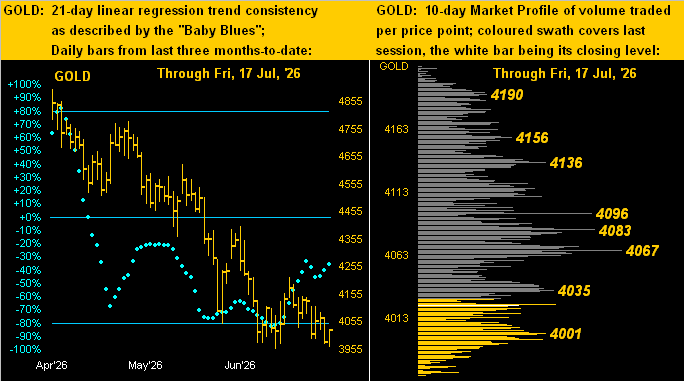

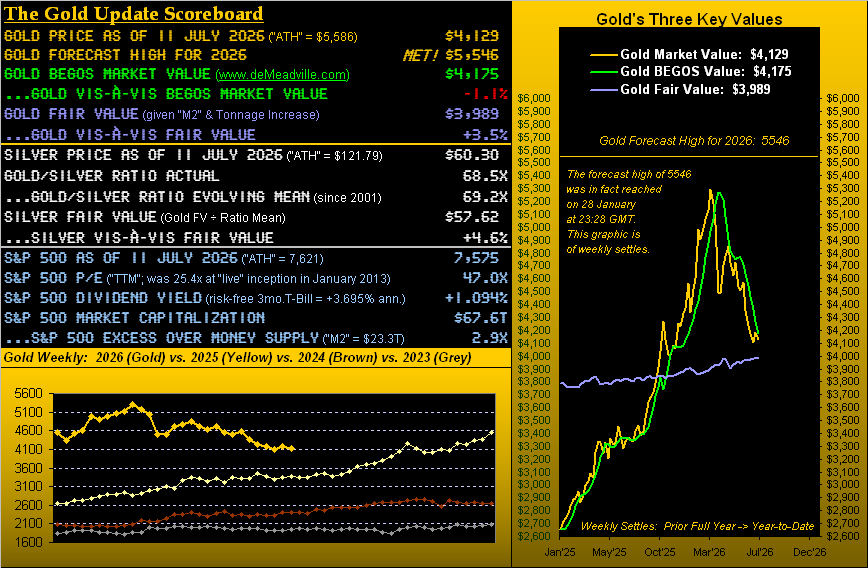

In settling yesterday (Friday) at 4401, Gold just posted its second best of the 31 full trading weeks year-to-date: a +7.4% increase, second only to the +8.3% gain for that ending back on 23 January. Cue ![]() “This Magic Moment”

“This Magic Moment”![]() –[The Drifters, ’60] … or more specifically the “magic minute” of the past week that arrived Friday at precisely 12:30 GMT upon the StateSide release of July’s “Non-Farm Payrolls”.

–[The Drifters, ’60] … or more specifically the “magic minute” of the past week that arrived Friday at precisely 12:30 GMT upon the StateSide release of July’s “Non-Farm Payrolls”.

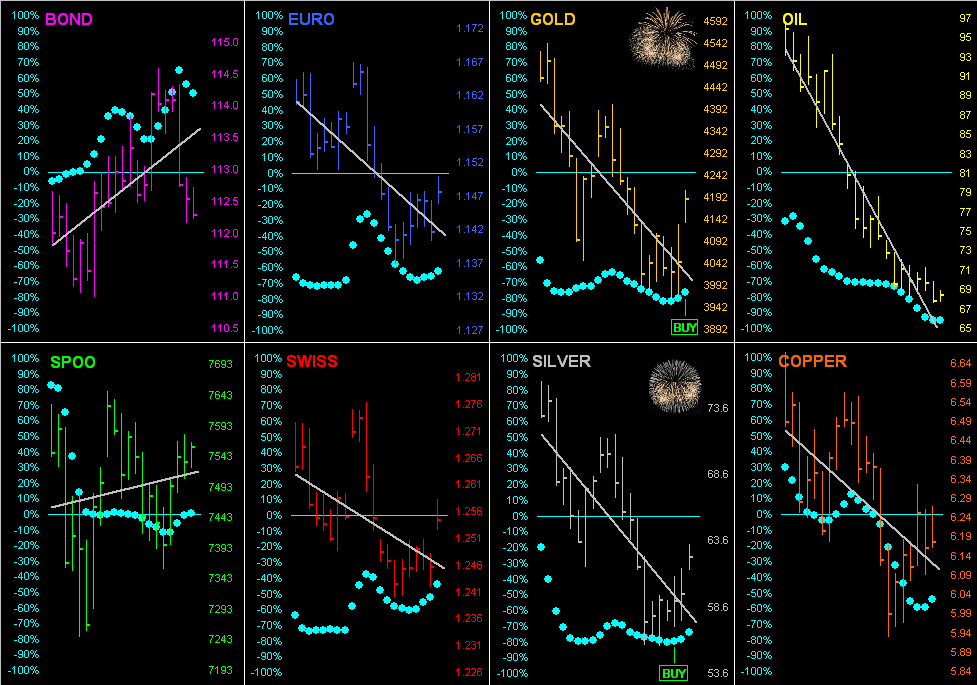

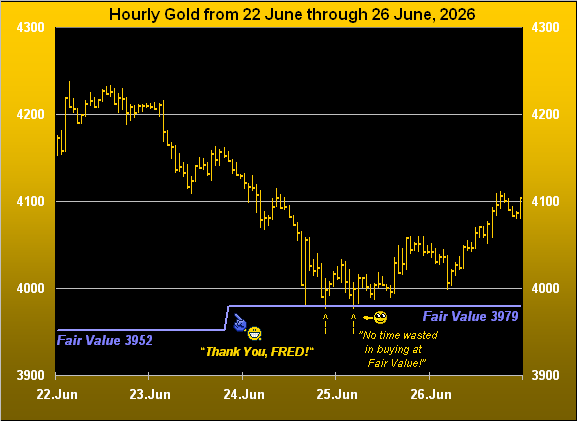

As is our wont come the release, rather than look at what — back in the day — was referred to as “The Mother of All Numbers”, we simply watched the markets. And within the 60 seconds from 12:30-12:31, the price of Gold low-to-high went from 4371 to 4418, some +47 points or +1.1%. Instantly our notion (without yet being knowledgeable of the data) was that Payrolls — rather than having increased per consensus — must actually have shrunk: so then we looked … and indeed they had! More on that later when we assess the eroding state of the Economic Barometer.

“Don’t forget the ¥en support also, mmb… ”

Noted, dear Squire, (and welcome back from your appreciated fire zone duties). As to the ¥en, whilst not eliciting as instantaneous a move for Gold, price nonetheless benefitted into the new week following the previous Friday’s direct dumping of €26B by the NY Fed for ¥en, with the Finance Ministry in Japan further loading up on its own currency in dispensing some $90B. Thus by conventional wisdom, (even as we’ve demonstrated over these many years that Gold plays no currency favourites), ’twas down with the Dollar and up with Gold.

“And so 4000 is now lookin’ like a floor, huh mmb?”

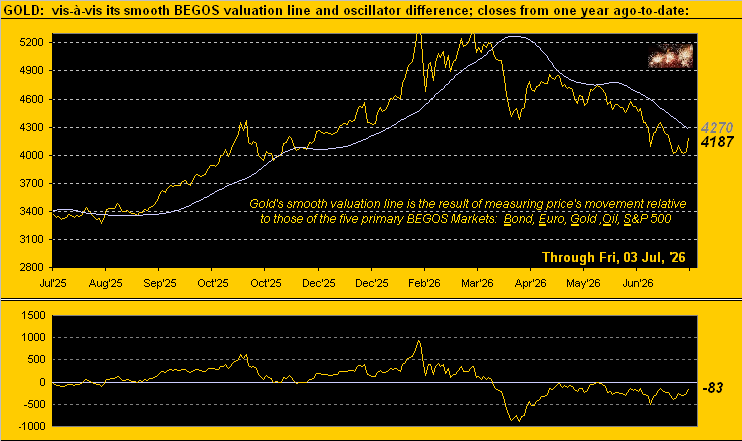

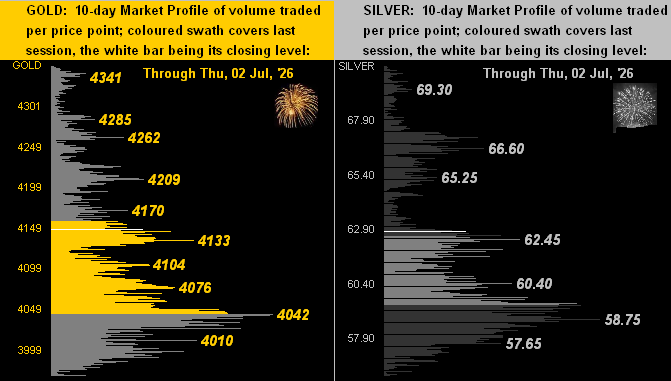

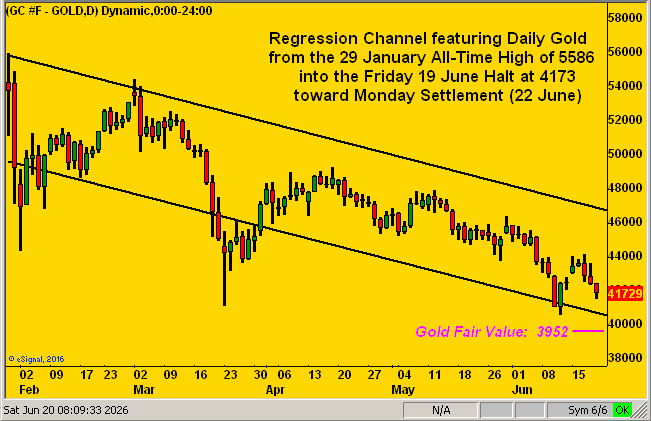

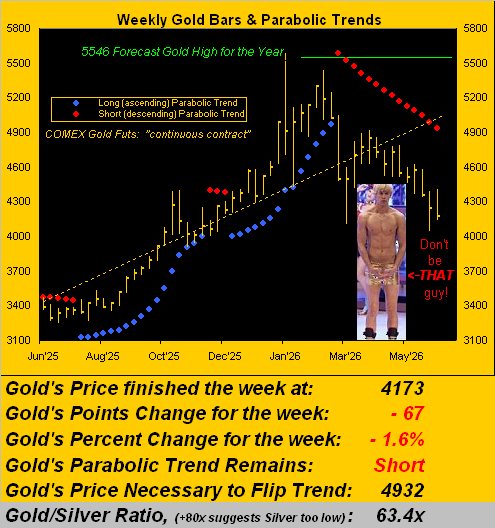

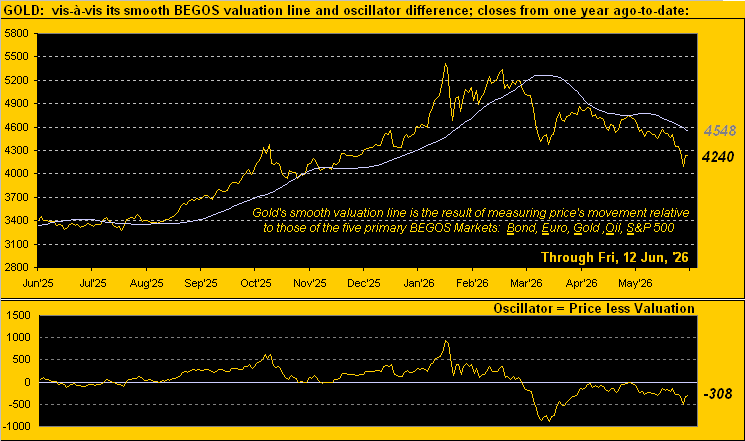

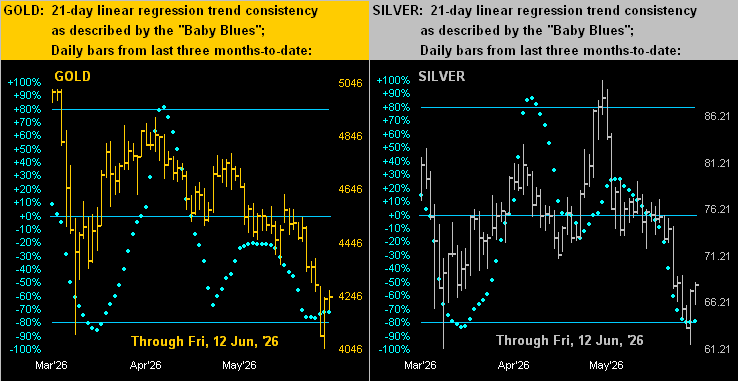

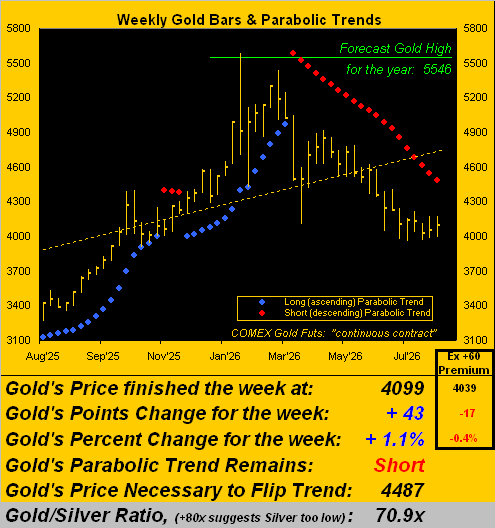

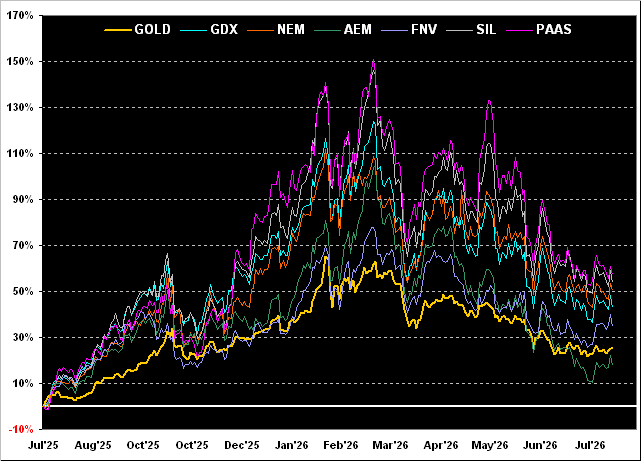

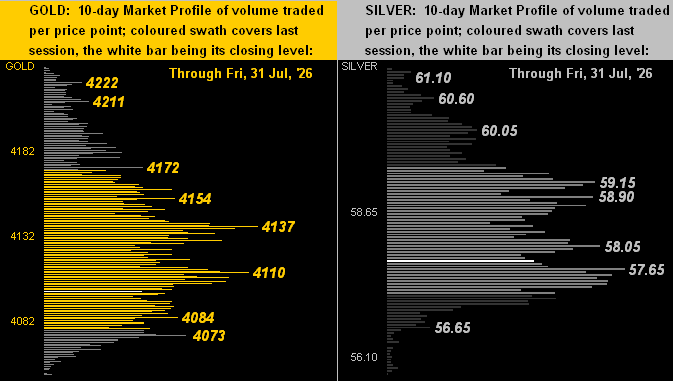

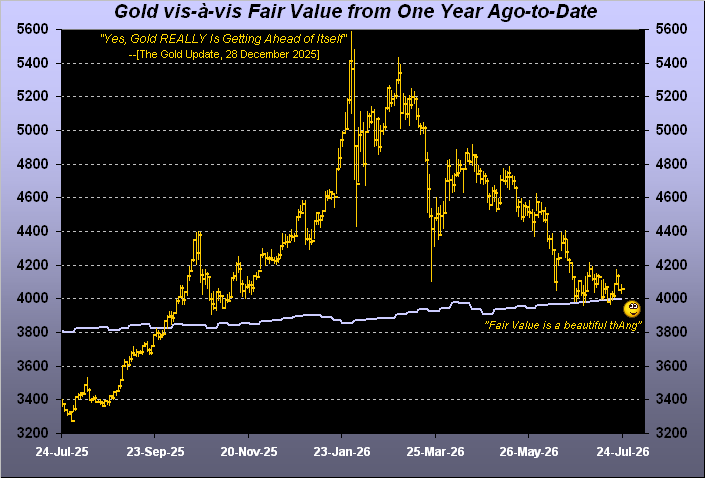

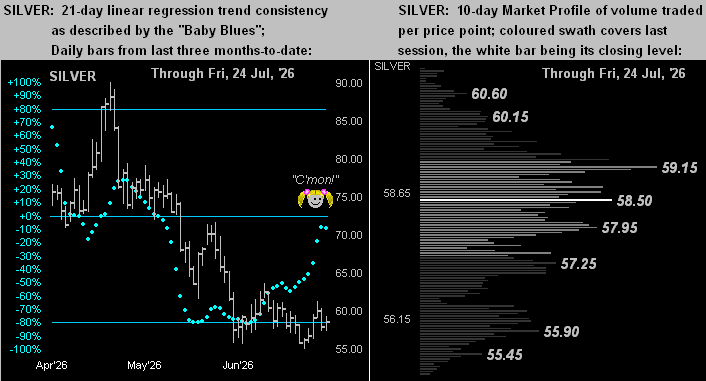

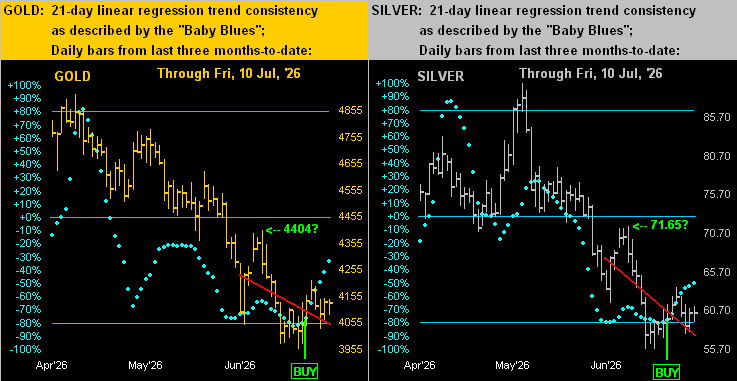

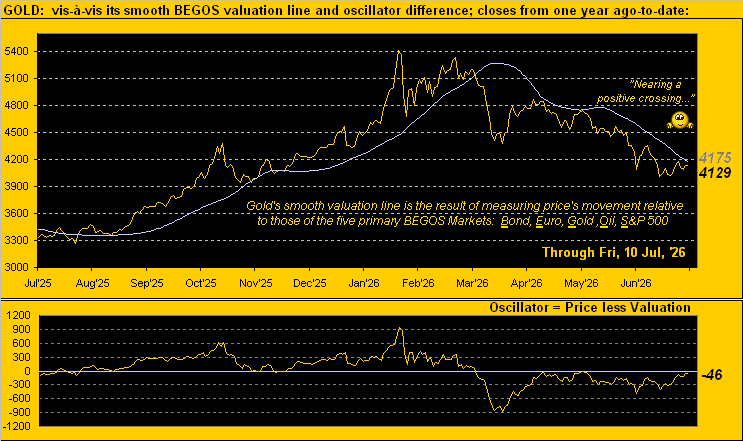

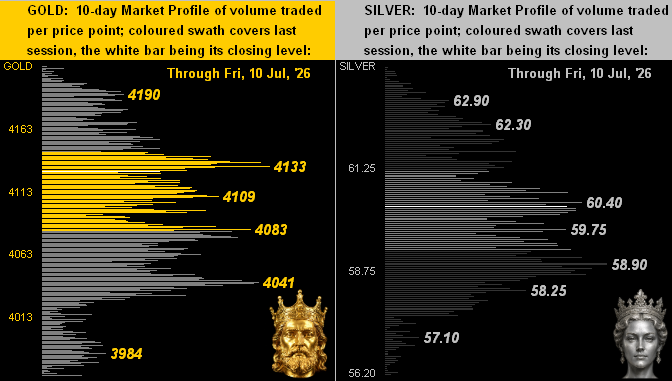

‘Twould appear at least the near-term case, Squire. Two missives ago we encircled the 4000 area within “Gold’s Fits and Starts in Finding a Floor”, only to just last week acknowledge “Gold Resumes Skidding…”. But then came the USA/JPN yen to buy the ¥en (which actually settled this past week slightly below Monday’s open, although still well up from the prior Friday), and thus — along with Payrolls’ shrinkage for July — here is the rightmost effect of it all by Gold’s weekly bars from a year ago-to-date:

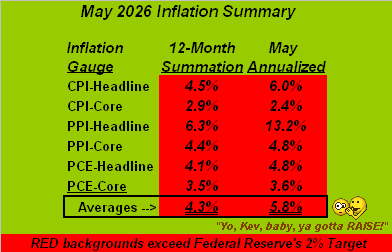

As to our aforementioned Econ Baro, the blue line continues a downward drift in this year ago-to-date view. The best incoming metric of the past week was Q2’s preliminary Productivity having nearly doubled from +0.8% in Q1 to now +1.4%. Problematic thereto? Productivity tends to rise as the human workforce subsides: “Oh blame it on AI!” For indeed, the week’s weak links were the stated July Payrolls’ shrinkage, ADP’s own July employment data reported as less than half that gained in June, and Construction Spending (for which workers are on-site requisite) also shrinking in July, missing estimates, with June revised lower as well. Reprise Fleetwood Mac from ’69: ![]() “Oh well…”

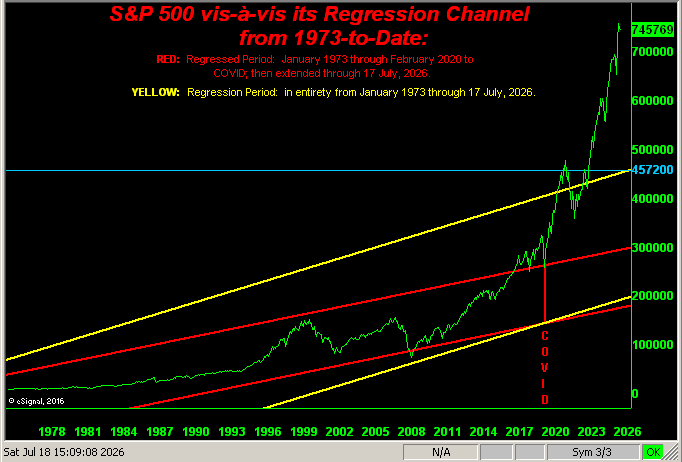

“Oh well…”![]() . Besides, with the S&P 500 at an all-time high, all must be well, (do tell?):

. Besides, with the S&P 500 at an all-time high, all must be well, (do tell?):

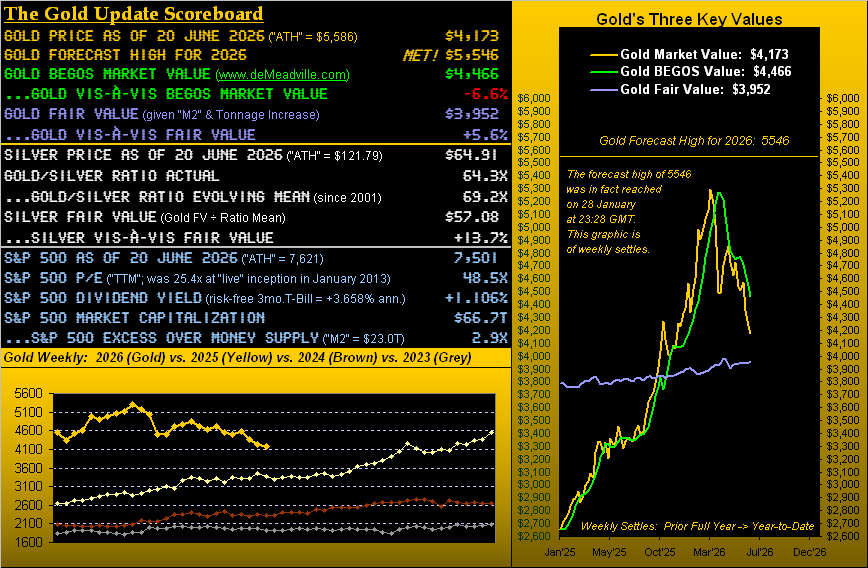

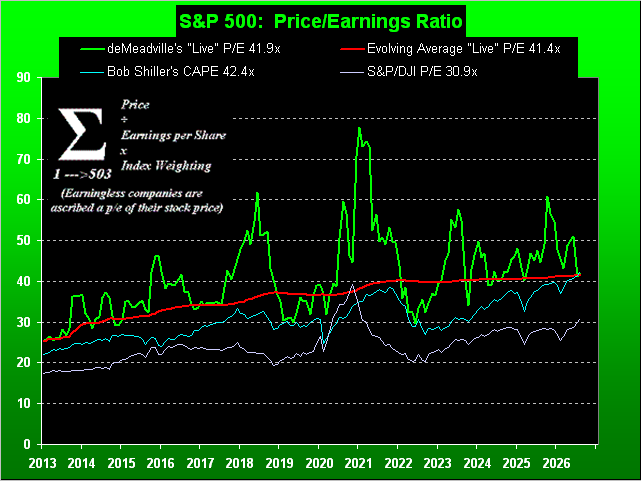

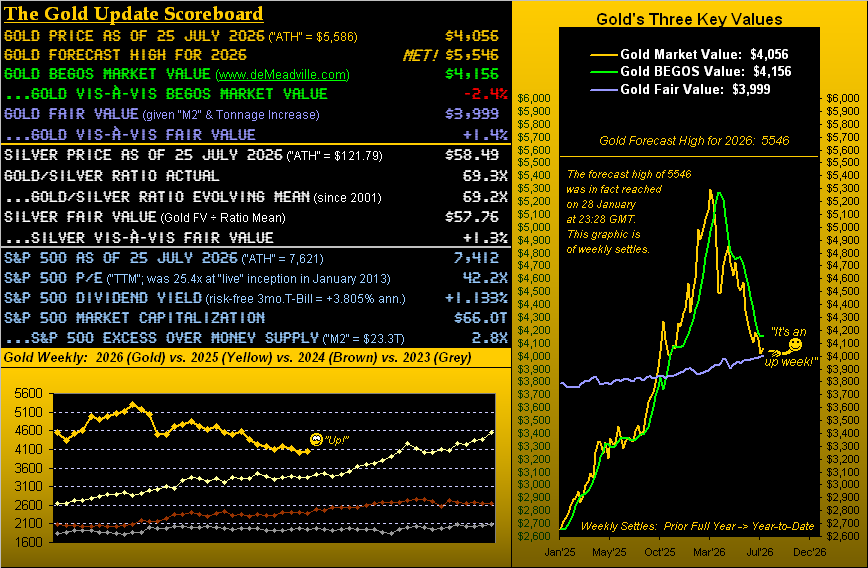

Speaking of the S&P, we close with its price/earnings ratio … and guess what just happened? Bob Shiller’s long-revered CAPE (Cyclically Adjusted Price/Earnings) just surpassed ours. Since the debut of the ever-honestly calculated deMeadville “live” P/E back in 2013, here by the month we’ve ours, along with Shiller’s and that compiled by S&P/DJI itself, the latter being comparably lower, yet still double the “acceptable maximum” as taught in portfolio theory, (an ancient science with which has been discarded in this modern Investing Age of Stoopid):

Thus as we on occasion quip, (until they again do), “Earnings don’t matter anymore.”

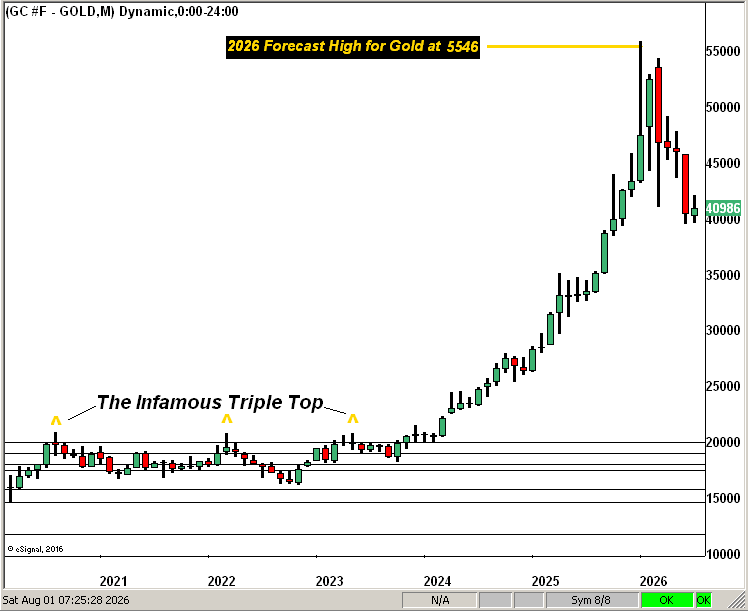

But Gold always matters, regardless of a 4000 floor, or more!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

.png)