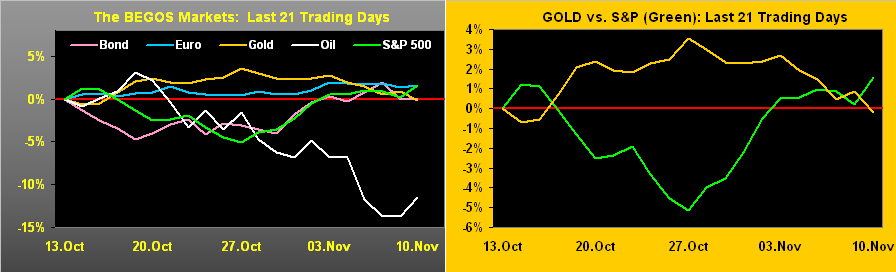

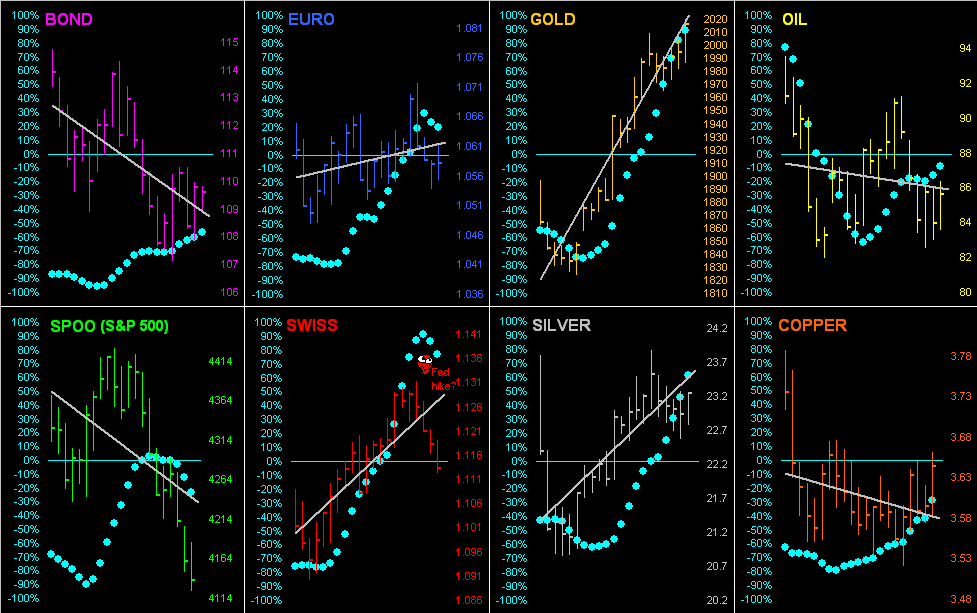

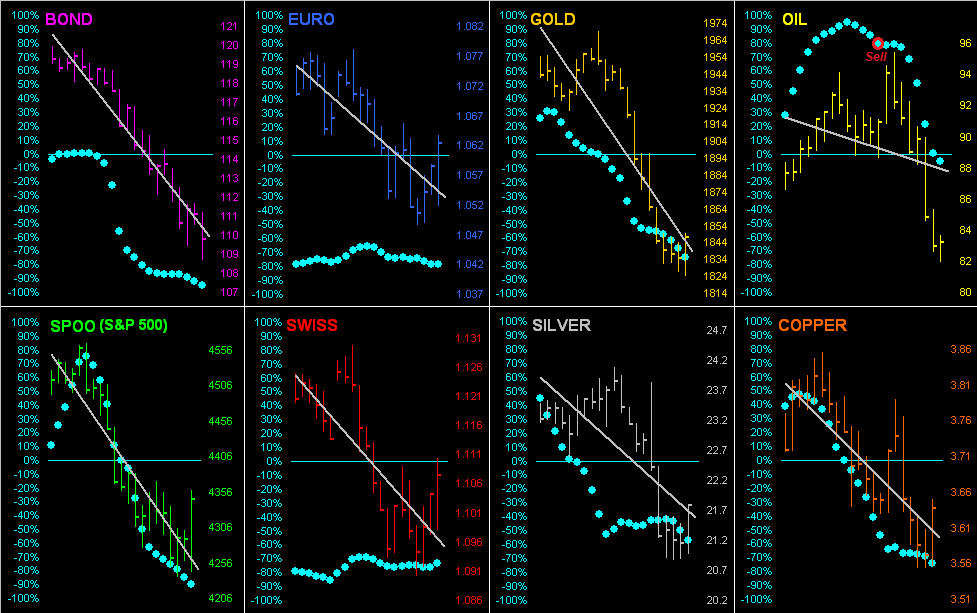

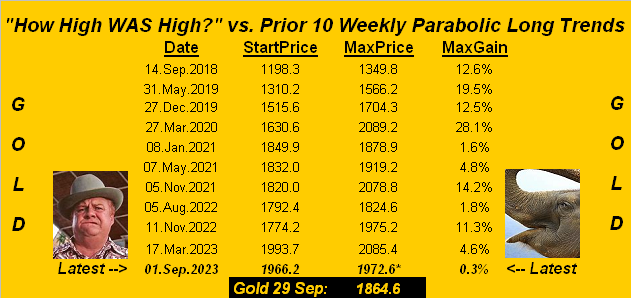

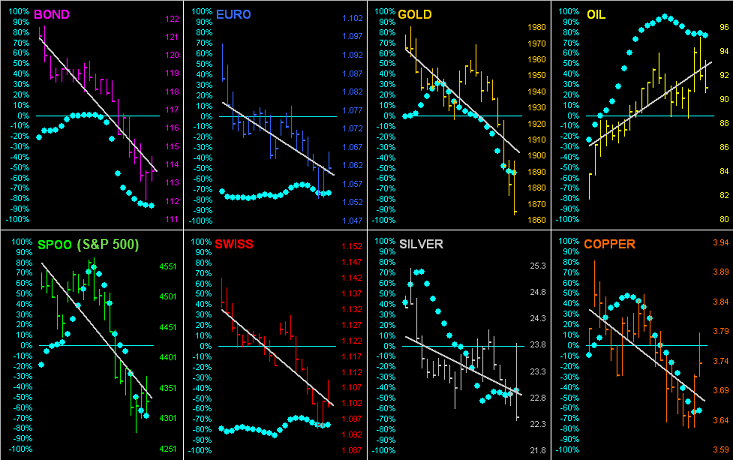

The Bond, Swiss Franc, Gold and Silver are all at present above their respective Neutral Zones for today; the other BEGOS Markets are within same, and volatility is leaning toward moderate, (the non-BEGOS Yen having again exceeded 100% of its Expected Daily Trading Range). The S&P 500 is now “textbook overbought” through the past 10 sessions, the last five of which are at an extreme overbought reading: the “live” P/E (futs-adj’d) is 44.7x, essentially double the 66-year historical mean. The Econ Baro awaits October’s Existing Home Sales; and late in the session comes the FOMC’s 31 Oct/01 Nov meeting minutes.

Mark

Mark

20 November 2023 – 09:17 Central Euro Time

The abbreviated trading week gets going with the Swiss Franc and Oil at present above today’s Neutral Zone; below same is the Bond: recall our noting to mind the Bond’s “Baby Blues” (at either the Bond or Market Trends page); the Blues in real-time are beginning to roll over (albeit still are above their key +80% level). BEGOS Markets volatility is moderate; indeed for the Yen (not yet officially a BEGOS component), it has already traced 120% of its EDTR (see Market Ranges). The Gold Update cites price having moved back above successfully tested support, in concert with inflation having purportedly come to a halt and the Econ Baro recording its 10th worse 12-day stint since the Baro’s inception back in 1998. The Baro today looks to October’s leading (i.e. “lagging”) indicators, one of just five metrics due for this week.

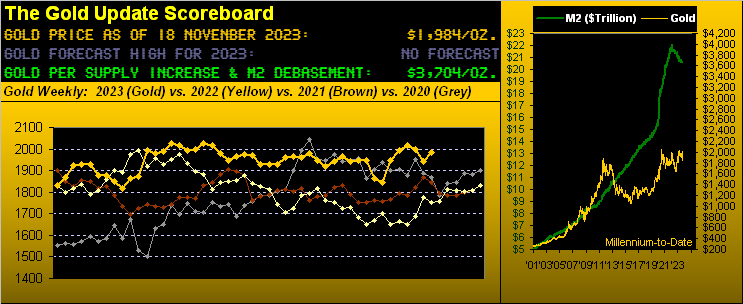

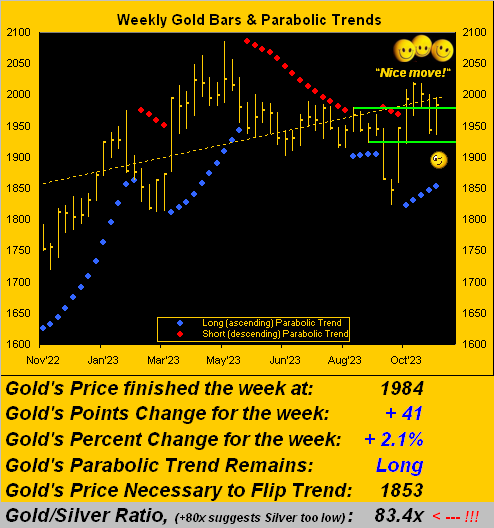

The Gold Update: No. 731 – (18 November 2023) – “Gold Pops as Inflation Stops and the Economy Flops”

In sum, Gold again has a chance to go for an All-Time High. The S&P by any and all rights is due for a dive (understatement). And certainly both “ought be” similarly priced right ’round “3000” … at least if you do the math. (What a rare concept, eh?)

We’ll close it here with this logistical note:

Next week’s 732nd consecutive Saturday edition of The Gold Update is planned to be quite brief as we shall be “in motion”: just straight to the point with a salient graphic or two along with our view. In any event, don’t be a turkey, given what can ensue…

…rather, keep your eyes (and wealth) on the Golden prize clearly due!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

17 November 2023 – 08:57 Central Euro Time

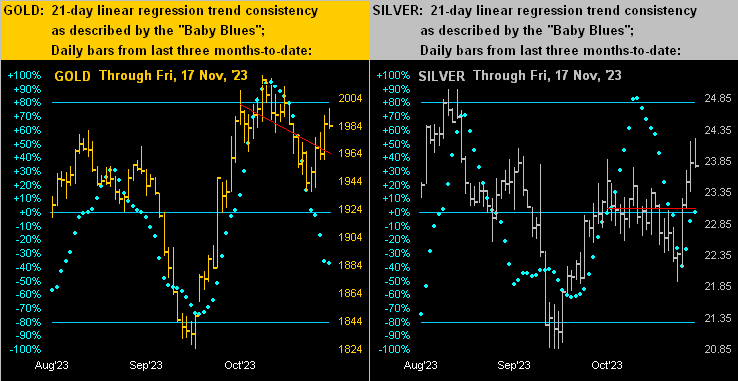

‘Twould appear to be a quiet Friday in the making: all eight BEGOS Markets are at present within their respective Neutral Zones, and volatility is very light. October’s Housing Starts/Permits come due for the Econ Baro, which itself has had quite the torrid week (https://demeadville.com/economic-barometer/); more on that in tomorrow’s 731st edition of The Gold Update. In real-time at Market Trends, the 21-day linreg trends are now perfectly flat for both the Swiss Franc and Silver, (the latter nonetheless getting a boost from the aforementioned daily Parabolics having flipped to Long). ‘Tis the final day of Q3 Earnings Season, for which the S&P 500 constituents finds 64% having improved their bottom lines of a year ago.

16 November 2023 – 08:58 Central Euro Time

Both the Bond and Gold are at present above today’s Neutral Zones; the rest of the BEGOS Markets are within same, and volatility is mostly light ahead of a busy day for incoming EconData. Silver’s daily Parabolics flipped to Long effective today’s open (23.510): the average maximum follow-though of the past 10 such studies (either Long or Short) is 1.695 points. At Market Trends, the Bond’s “Baby Blues” are above the key +80% axis; upon their eventual decline below that level, we’d then anticipate lower price levels. Included amongst today’s seven incoming metrics for the Econ Baro are November’s Philly Fed and NAHB Housing Indices, along with October’s Ex/Im Prices and IndProd/Cap/Util.

15 November 2023 – 08:59 Central Euro Time

October’s CPI indeed was “center stage” (per yesterday’s comment), the headline retail level coming in “unch”. In turn the Dollar dove and the BEGOS Markets unimpededly rose. Today ahead of wholesale inflation we’ve both Gold and Silver at present above their respective Neutral Zones for today; the other BEGOS components are within same, and volatility is light. Yesterday’s S&P 500 +1.9% rise now finds the Spoo (in real-time) +216 points above its smooth valuation line (see Market Values): historically such extreme deviation leads on average to price descending by well over -100 points within the ensuing weeks such that we may soon see the S&P below where ’twas prior to the inflation data (4411 vs. now 4491); too there’s the “live” P/E of the S&P now 44.9x. Overall today for the Econ Baro we’ve November’s NY State Empire Index, October’s PPI and Retail Sales, plus September’s Business Inventories.

14 November 2023 – 09:08 Central Euro Time

The Bond is the sole BEGOS Market at present outside (above) its Neutral Zone for today; session volatility is very light, the Econ Baro awaiting October’s CPI to take center stage. Heading our Market Rhythms for trading consistency are (on a 10-test basis) the Euro’s daily Moneyflow, Oil’s 30mn Parabolics and Silver’s daily Parabolics, (too, whilst not a BEGOS component, the Yen’s 1hr Moneyflow also qualifies). The “live” (futs-adj’d) p/e of the S&P 500 is now 42.9x and the yield 1.569% whereas that for the “riskless” U.S. three-month T-Bill is an annualized 5.260%. And in real-time, the Spoo is +127 points above its smooth valuation line, the S&P itself now “textbook overbought” through the past five sessions.

13 November 2023 – 09:04 Central Euro Time

Both Silver and Oil are at present below today’s Neutral Zones; above same is Copper, and BEGOS Markets volatility is pushing toward moderate. The Gold Update confirms our anticipated typical post-geopolitical price pullback: visually therein on the Weekly Bars graphic we’ve placed the 1980-1922 support structure, (expandable to 2001-1901 if need be); and in real-time, Gold is now just +35 points above its smooth valuation line (see Market Values) after having been some +120 points above it. ‘Tis a very busy week for the Econ Baro with 18 metrics due, beginning (again purportedly) today with October’s Treasury Budget. Too, ’tis the final week of a “so-so at best” Q3 Earnings Season.

The Gold Update: No. 730 – (11 November 2023) – “Gold’s Bang-On-Time Dive”

“But mmb, those PPI annualized percents are in line with the Fed’s target…”

Duly noted, Squire. If that Producer Price Index is truly leading, then we ought see the other inflation percents stall, if not fall, although the Fed does have a lean toward those Core Personal Consumption Expenditures. As well, Minneapolis FedPrez Neel “Cash n’ Carry” Kashkari per Dow Jones Newswires “…is not convinced rate hikes are over…” Or to reprise the great Bonnie Raitt from back in ’88: ![]() “It’s just too soon to tell…”

“It’s just too soon to tell…”![]()

In the midst of all this, we read the Fed’s interest-rate increases of the past two years being deemed as “historic”. Again, the Fed’s Effective Funds Rate is presently 5.33% (i.e. the targeted 5.25% + 5.50% ÷ 2). Hardly is that “historic”. Anyone remember the Prime Rate at 22% back in 1980? We do. (What would be today’s FinMedia adjective for that? “Steroidic”?)

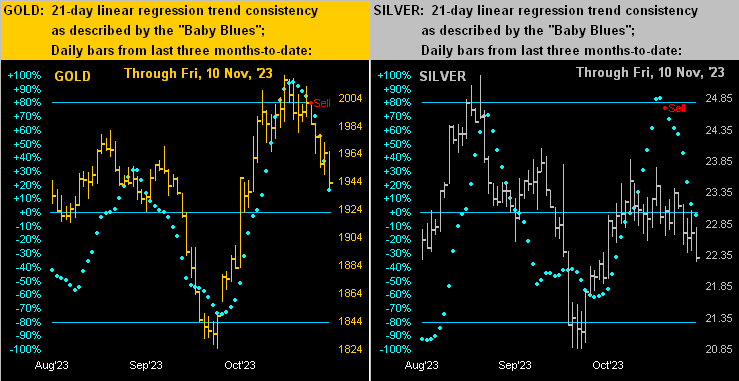

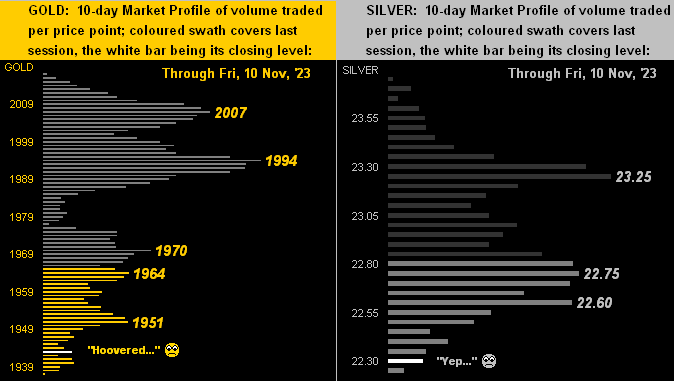

Specific to the precious metals this past week, a more apt adjective would be “atrophic” as next we’ve the two-panel display of Gold’s daily bars for the past three months-to-date at left and same for Silver at right. As aforementioned for Oil, here we’ve the “Baby Blues” signaling “Sell” in both metals’ current cases upon the dots having slipped below their respective +80% axes. Again we commend “The trend is your friend” even if it must descend:

Indeed with respect to Gold, we tweeted (@deMeadvillePro) this graphic last Monday, reflective of the “Baby Blues” heading south:

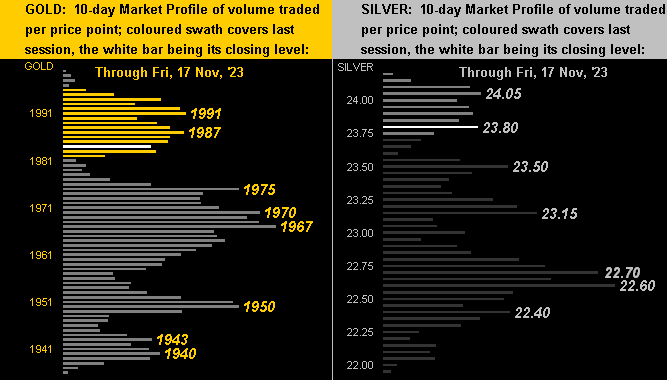

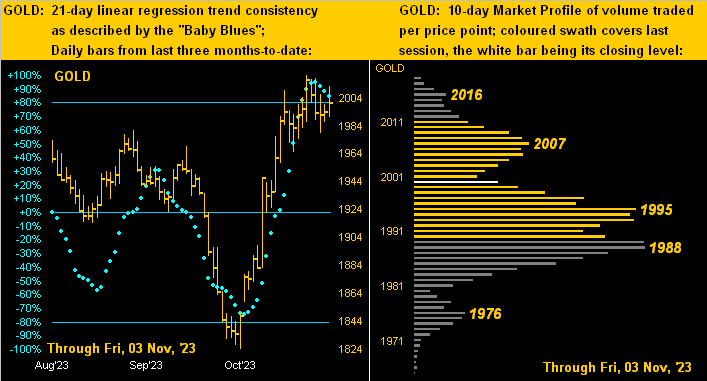

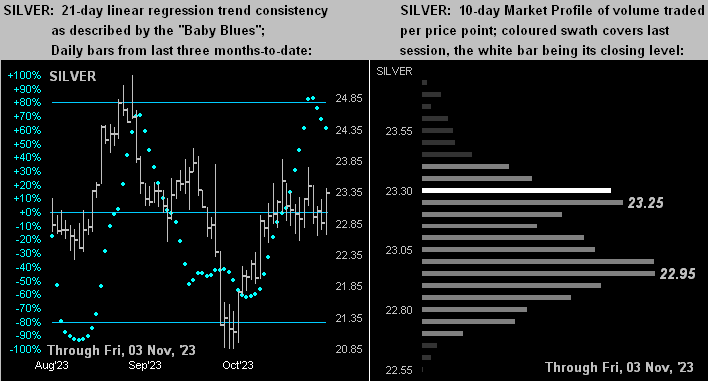

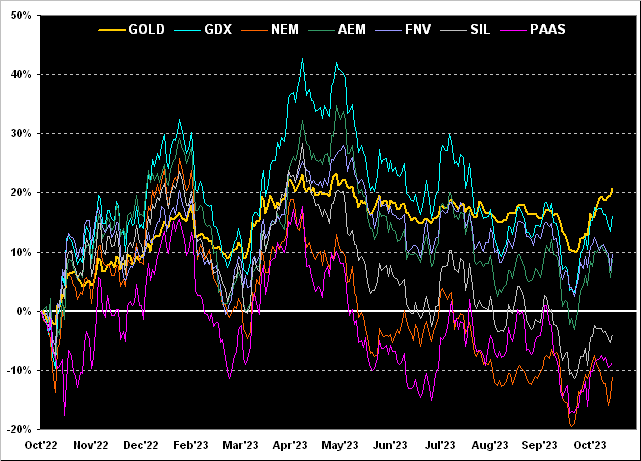

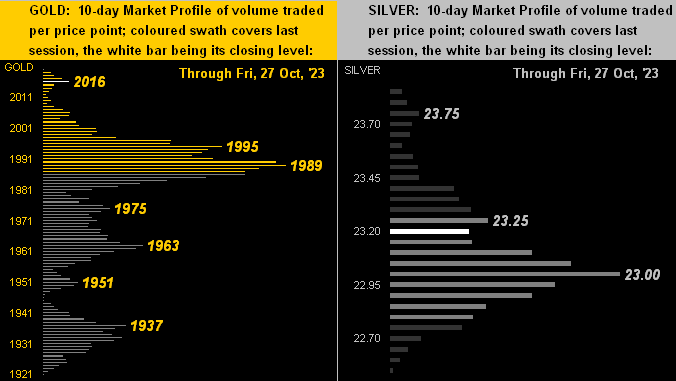

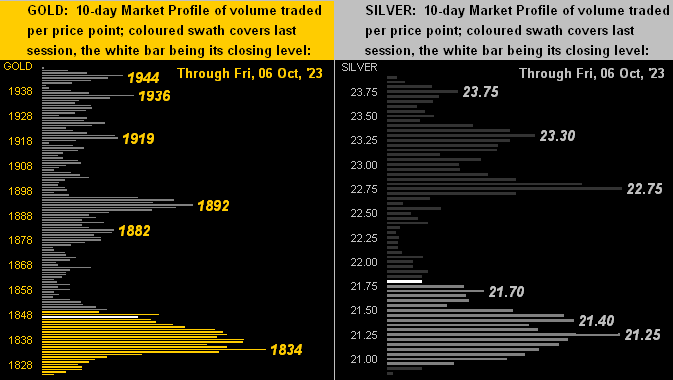

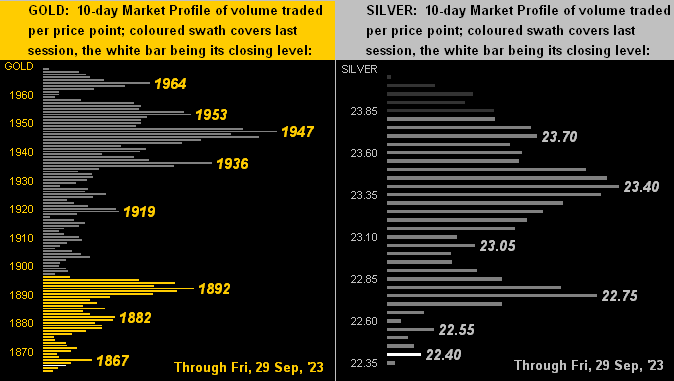

And so in turn we go to the 10-day Market Profiles for Gold (below left) and Silver (below right). Simply stated from high-to-low, the word “hoovered” is apropos, with all labeled lines now overhead trading resistance. As for their two-week percentage changes, Gold’s from top-to-bottom is -4.0% whilst that for Silver is -6.3%. Is it any wonder the Gold/Silver ratio — now 87.1% — is at its second-highest level since last March? No ’tisn’t. Reprise: Do not forget Sister Silver!

Toward the wrap, here’s the stack.

The Gold Stack

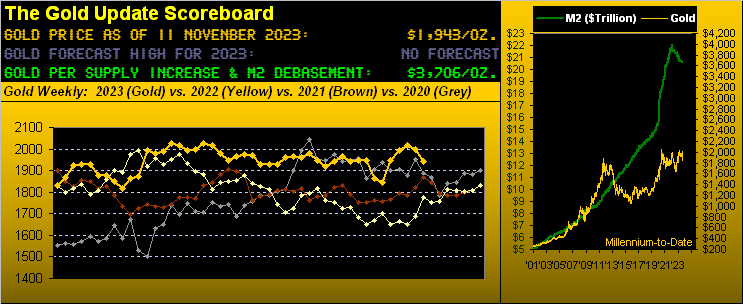

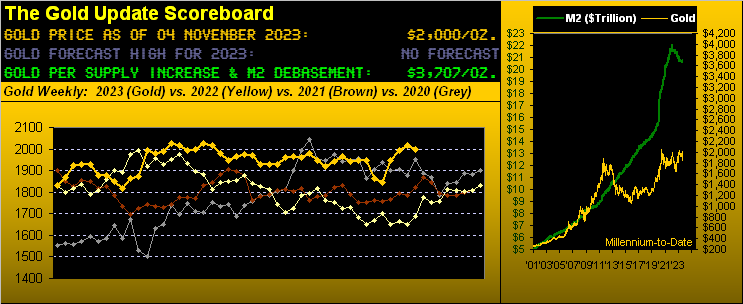

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3706

Gold’s All-Time Intra-Day High: 2089 (07 August 2020)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar ’22); 2085 (04 May ’23)

2023’s High: 2085 (04 May)

Gold’s All-Time Closing High: 2075 (06 August 2020)

10-Session “volume-weighted” average price magnet: 1985

Trading Resistance: 1951 / 1964 / 1970 / 1994 / 2007

Gold Currently: 1943, (expected daily trading range [“EDTR”]: 24 points)

Trading Support: none by the Profile

10-Session directional range: down to 1922 (from 1980) = -81 points or -4.0%

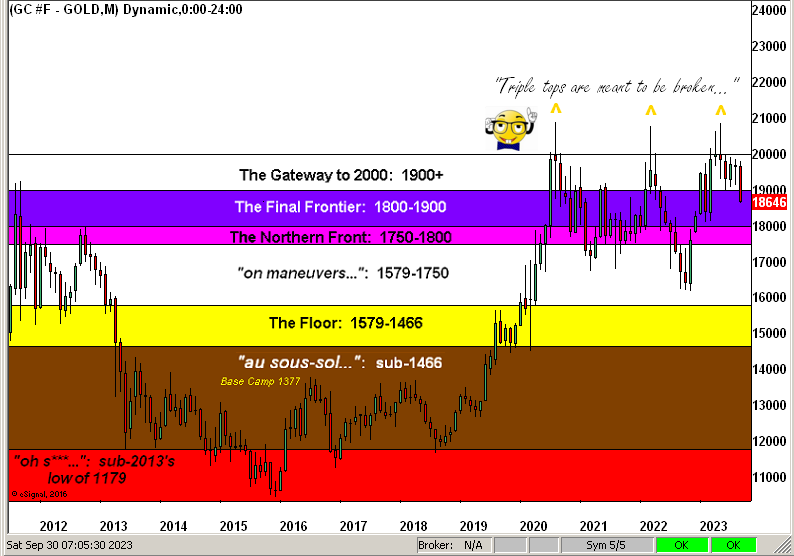

The Gateway to 2000: 1900+

The 300-Day Moving Average: 1883 and rising

The Weekly Parabolic Price to flip Short: 1846

2023’s Low: 1811 (28 February)

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

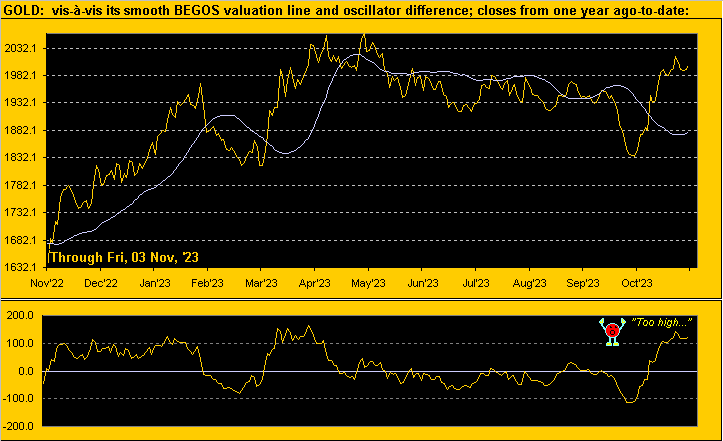

In sum, Gold is definitely getting the anticipated post-geopolitical pullback. Does it continue? Per the website’s Gold and/or Market Values page, recall that price a mere week ago was +120 points above its smooth valuation line; that deviation has since been reduced to now +39 points. Yet even as Gold’s “Baby Blues” are accelerating lower, again note the cited structural support bases: 1922, 1914 and 1901, the notion thus being that Gold is “safe” above the 1800s.

‘Course, given Gold’s valuation by Dollar debasement is now 3706, ’tis clearly requisite toward maintaining one’s bridge to wealth security.

Thus: don’t be that guy…

…rather consider that Gold today is THE bang-on attractive Buy!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

10 November 2023 – 09:04 Central Euro Time

The Bond is at present above its Neutral Zone for today; the Swiss Franc is below same, and BEGOS Markets volatility is mostly light. Looking at Market Profile resistors for the Spoo (presently 4372) we’ve the 4381-4384 area followed more dominantly by 4396; whilst by Market Trends the Spoo’s linreg in real-time has just rotated to positive, there is broader structural resistance running from 4341 up to 4431; and by Market Values, the Spoo is now +59 points above its smooth valuation line; for the S&P itself, ’tis now “textbook overbought” through these past three trading days. The Econ Baro concludes its quiet week with November’s UofM Sentiment Survey and (purportedly) October’s Treasury Budget.

09 November 2023 – 08:54 Central Euro Time

Copper is the sole BEGOS Market at present outside (below) its Neutral Zone for today; session volatility is light, save for Copper which has traced 57% of its EDTR (see Market Ranges). As Gold’s “Baby Blues” continue to descend, price has thus far traded to as low as 1953: recall from the current edition of the Gold Update the mention of 1951 as a mid-structural support level; currently priced at 1955, Gold is now +58 points above its smooth valuation line (see Market Values) after having been better than +100 above it through recent days. Indeed for Gold, Silver and the Swiss Franc, their “Baby Blues” all having fallen below the key +80% level have in turn seen lower price levels. As the Econ Baro’s subdued week continues, only due today are the usual weekly Jobless Claims.

08 November 2023 – 09:01 Central Euro Time

The Bond and EuroCurrencies are at present below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light. At Market Ranges, the recent EDTR widenings for the Bond, Gold, Silver, Oil and the Spoo appear for now to have peaked. Following Gold’s “Baby Blues” falling below their key +80% level, price (now 1974) has since weakened to as low as 1963 yesterday; the Blues in real-time continue to drop as do those for the Swiss Franc, Silver and Oil. The “live” (fut’s adj’d) P/E of the S&P is now 42.5x and the Gold/Silver ratio a very “Silver-attractive” 87.4x despite the present Blues negativity. The Econ Baro awaits September’s Wholesale Inventories.

07 November 2023 – 09:03 Central Euro Time

All eight BEGOS Markets are in the red and all at present (save for the Bond) are below their respective Neutral Zones for today; volatility is mostly moderate. Gold confirmed its “Baby Blues” (see Market Trends) dropping below their key +80% level; priced now at 1976, we can see 1946 trading near-term, well within the context of the support zone described in the current edition of The Gold Update. By Market Rhythms, the most consistent on a 10-test basis is the Euro’s daily Moneyflow which has been near or at the top of all 405 studies now for some time; on a 24-test basis, both the Bond’s 15mn Parabolics and Moneyflow studies top the list, along with the Spoo’s 15min Parabolics. The Econ Baro’s rather “un-busy” week looks to September’s Trade Deficit and Consumer Credit.

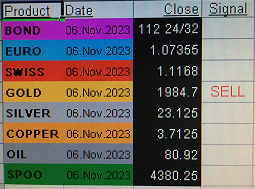

06 November 2023 – 08:33 Central Euro Time

The BEGOS Markets’ volatility is light-to-moderate as the new week unfolds. At present, Copper is above its Neutral Zone for today, whilst Gold is below same. The Gold Update anticipates a typical post-geopolitical price pullback is nigh; indeed at Market Trends, Gold’s “Baby Blues” are in real-time slipping below their key +80% axis, (as have Silver’s already so done); confirmation of the “Baby Blues” settling below that level generally leads to lower prices near-term; too, Gold by Market Values is (in real-time) +106 points above its smooth valuation line. Despite all the excitement over the S&P’s recent rally, price has merely returned to where ’twas three weeks ago, the P/E ratio accelerating last week now to 40.9x as Q3 Earnings Season remains rather average at best; (’twas 39.0x those three weeks ago). Nothing is due today for the Econ Baro as it faces a fairly light load this week with just six metrics due through Friday.

The Gold Update: No. 729 – (04 November 2023) – “Gold’s Post-Geopolitical Pullback”

Now beyond the world of reality, the S&P 500 is going giddy! Or at least those following it are. On Monday: “The S&P gained +1.2%!” Then Tuesday: “The S&P added another +0.6%!” Wednesday: “The S&P is soaring, +1.1%!” Thursday “The S&P is straight up +1.9%!” Friday: “The S&P is all bullish, up yet again +0.9%!”

And thus for the week the S&P garnered growth of +5.9%. Cue the late, great Howard Cosell: “Looook at it GO!”

Here’s to where we saw it go: merely back to now 4358 as ’twas three weeks ago. Thus predictably, you know the next sentence. “Change is an illusion whereas price is the truth.” In other words, (’tis our turn to say): “Nothing to see here.”

In the midst of it all, ‘natch, is Q3 Earnings Season. And for the S&P 500, of the 381 constituents having so far reported, 65% have made more dough than in Q3 a year ago.

But shouldn’t they all be making more? After all, this is the S&P 500, the top-tier, best-of-the-best. And when it does not all go right, valuation is the plight. Thus our honestly-calculated “live” price/earnings ratio for the S&P went from 34.0x on Monday to 40.5x come Friday’s settle. For you WestPalmBeachers down there, that means if you buy the S&P right now, you’re willing to pay $40.50 for something than earns $1. Further, the cap-weighted dividend yield for the S&P is but 1.625%. Do not reprise ![]() “Bargain”

“Bargain”![]() –[The Who, ’71]. Worth reprising: the U.S. three-month T-Bill annualized yield is now 5.253%.

–[The Who, ’71]. Worth reprising: the U.S. three-month T-Bill annualized yield is now 5.253%.

Then there’s Gold, which as aforementioned can rise +85% just to reach its current Dollar debasement value. (Remember: given historically such eventually happens, this is not a difficult decision). And although price may languish near-term in post-geopolitical recoil, we don’t expect it to come well off the boil, (on which is has been for nearly a month).

So to Gold’s two-panel graphic we go with the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. Especially note the baby blue dots of trend consistency. Barring price imminently/rapidly rising, those “Baby Blues” shall cross beneath the key +80% axis: such has occurred twice within the past year resulting in subsequent point drops (within 21 days) of -67 and -20 respectively; and that reasonably aligns with the underlying 1980-1922 support structure noted earlier. Specific to trading support, by the Profile the 1995-1988 zone may be the first to go toward further below:

So with our expectations for Gold getting a post-geopolitical pullback — but still more broadly maintain an uptrend — we’ll wrap it up here with this from the “Is the FinMedia Really Running the Fed? Dept.” To wit:

As you all know, the FOMC per this past Wednesday’s Policy Statement unanimously voted to maintain the Bank’s FedFunds target range as 5.25%-5.50%. But did they really need to have their traditional two-day meeting? After all, we were informed the previous Friday (27 October) by Dow Jones Newswires that:

“Inflation Trends Keep Fed Rate Hikes on Pause–Underlying inflation picked up in September, government data showed, keeping the Federal Reserve on track to hold short-term interest rates steady at its next meeting.”

Therefore: why meet at all? Even as the recent inflation data we herein recounted a week ago clearly justified the Fed raising rates, the FinMedia already had decided “No no, Jerome” and that was that. (One wonders if they have to sign non-disclosure agreements. Just a passing thought…)

Regardless of who’s running the Fed show, pullback or not, don’t pass on Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

03 November 2023 – 09:02 Central Euro Time

Silver is the only BEGOS Market at present outside (below) today’s Neutral Zone; session volatility is light with October’s Payrolls data in the balance. Yesterday’s +1.9% S&P 500 rise was sufficient to fully unwind the “textbook oversold” stance that had been in place since 23 October; too on Thursday, the S&P’s P/E rose from 34.7x to now 38.8x: with still some 100 Q3 earnings reports due for the S&P, fully one-third thus far have not improved their year-over-year bottom lines; (as penned in last Saturday’s edition of The Gold Update, for the S&P we’re seeing that “…bounce before the next trounce…”); and by Market Values, this bounce has lifted the Spoo up to its smooth valuation line, price back to where ’twas two weeks ago. In addition to the Econ Baro’s incoming jobs data, we’ve also October’s ISM(Svc) Index.

02 November 2023 – 09:01 Central Euro Time

Post-Fed the EuroCurrencies are getting a bid, both the Euro and Swiss Franc at present above their respective Neutral Zones for today, as is Copper; the other BEGOS Markets are within same, and volatility is light-to-moderate. Silver confirmed its “Baby Blues” (see Market Trends) moving below the key +80% level, indicative of lower prices near-term: we are eying 22.18 (current is 23.10) barring geo-political price-rise resumption. As the S&P 500 works through Q3 Earnings Season, with 318 constituents having thus far reported, 65% have bettered their bottom lines from a year ago; however more broadly, only 52% have improved. For the Econ Baro, today’s incoming metrics include the initial read of Q3 Productivity and Unit Labor Costs, plus September’s Factory Orders.

01 November 2023 – 09:00 Central Euro Time

As Mid-East headlines fall a bit from above the fold, so too falling are the precious metals’ prices: both Gold and Silver are at present below their Neutral Zones for today; the other BEGOS Markets are within same, and volatility is light with the FOMC’s Policy Statement in the balance. By Market Profiles, Gold is testing its 1989 trading support, the next such level being 1963; for Silver, its key 23.00 level is being tested. Also by Market Trends, Gold’s “Baby Blues” have started to roll over to the downside, and moreover, those for Silver (in real-time) have provisionally dropped below their +80% level suggestive of lower prices near-term. The Econ Baro looks to October’s ADP employment data and ISM Index, plus September’s Construction spending.

31 October 2023 – 08:59 Central Euro Time

The Bond is at present above its Neutral Zone for today; the balance of the BEGOS Markets are within same, and volatility is again light-to-moderate; thereto of note, whilst not (yet) a BEGOS component, the Yen has traced 235% of its EDTR (see Market Ranges for those of the BEGOS Markets) as the BOJ maintains its long-term debt rate of 0% (as opposed to going negative). StateSide, the S&P 500 yesterday gained +1.2%: however the MoneyFlow was only +0.5%, indicative of the relief rally (from the Index’s still “textbook oversold” condition) lacking substance. Going ’round the Market Values page (in real-time) for the primary BEGOS Markets, we’ve the Bond nearly +3 points “high” above its smooth valuation line, the Euro +0.016 points “high”, Gold +131 points “high”, Oil -4.89 points “low” and the Spoo -143 points “low”. The Econ Baro awaits October’s Chicago PMI and Consumer Confidence, plus Q3’s Employment Cost Index.

30 October 2023 – 09:05 Central Euro Time

The “textbook oversold” S&P 500 looks to get a boost at the open, the Spoo at present above today’s Neutral Zone; below same are both Gold and Oil, and volatility is light-to-moderate. The Gold Update reiterates the yellow metal still as “range-bound” rather than “moon-bound”: 1989 is dominant trading support by the 10-day Market Profile; we’re wary as well that by Market Values, Gold (in real-time at 2005) is +131 points above its smooth valuation line. Leading the Market Rhythms for consistency (10-test basis) is Silver with a variety of studies: its daily Parabolics, 12hr MACD, 8hr Price Oscillator, and both the 6hr Price Oscillator and Moneyflow; too, is the Euro’s daily Moneyflow. ‘Tis a busy week for the Econ Baro with 15 metrics on the table, (none due today).

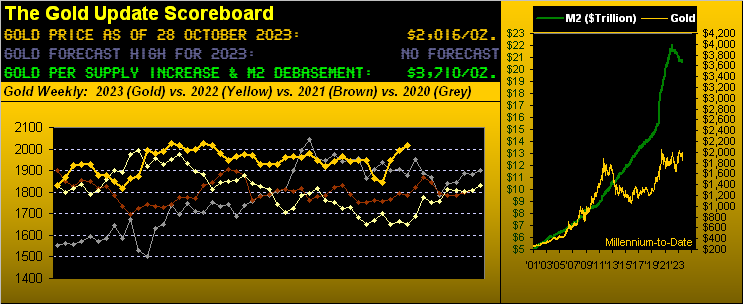

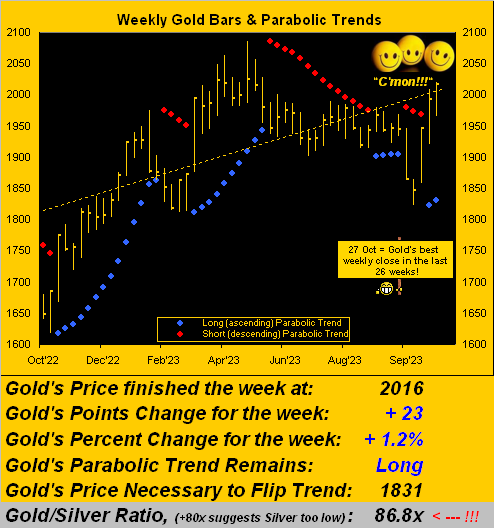

The Gold Update: No. 728 – (28 October 2023) – “S&P Squirms; Gold Firms”

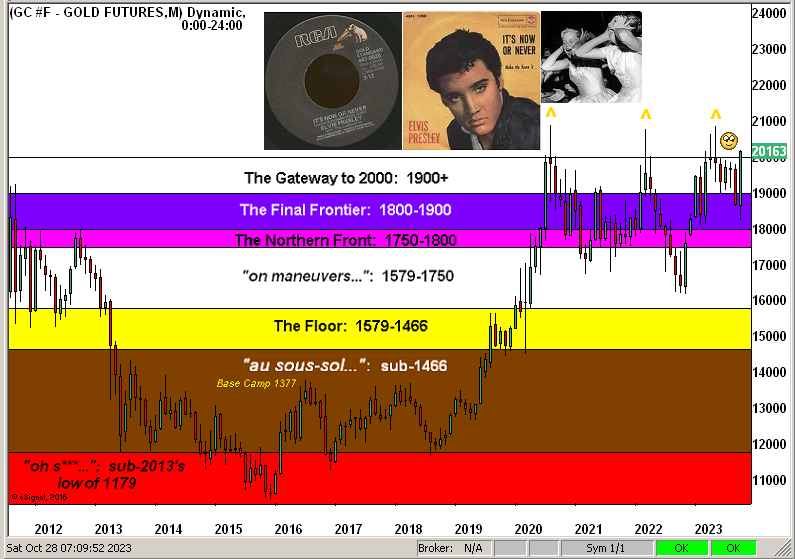

So with but two trading days remaining in October, here now is our stratified Gold Structure by the month across these past dozen years. As oft previously shown, now courtesy of the “Here We Go Again Dept.” we’ve Gold’s triple top which “is meant to be broken” as highlighted by the three Golden arrows. Moreover, we’ve anticipated on occasion throughout this year’s missives that Gold shall record a fresh All-Time High in 2023: obviously the momentum is there, barring a post-geo-political price retrenchment (as is the rule rather than the exception). Nonetheless, let’s cue Elvis from back in ’60 with ![]() “It’s now or never…”

“It’s now or never…”![]() :

:

Through these 10 months we’ve emphasized the importance of doing the math to get to the truth of such critical metrics as economic inputs, p/e calculations, and so forth. And whilst nothing light can be made of the horrific Mid-East mayhem, as this past week unfolded a mathematical “challenge” shall we say “came to light” over at the United States Department of State. Hat-tip ExecutiveGov which reported: “The Department of State has issued an advisory cautioning United States citizens against travel to more than 200 countries amid rising geopolitical tensions and conflict.” ‘Course, you can see where this is going, given (hat-tip Quora) stating: “Today, there are 197 countries in the world…“ The bottom line here being: if you’re in the States, you’re sorta stuck from going anywhere, nor beyond! Best therefore not to squirm; rather stay firm and stuck in Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

27 October 2023 – 09:01 Central Euro Time

The Bond is at present below its Neutral Zone for today, whilst above same are Copper, Oil and the Spoo; BEGOS Market’s volatility is mostly light. As tweeted (@deMeadvillePro) last evening, we’re finally seeing some “fear” in the Flow, the S&P 500 falling -1.2% yesterday, but its MoneyFlow regressed into S&P points was -2.4%; still, the Index for the present is “textbook oversold”, so perhaps some bounce to unwind that condition, followed then by lower levels sub-4000 (S&P at present is 4137). At Market Trends, the Swiss Franc’s “Baby Blues” have (in real-time) provisionally slipped below their +80% level, suggestive of lower prices near-term, which coincident with a Fed rate hike would further foster Dollar strength. Indeed ahead of next Wednesday’s FOMC Policy Statement, the Econ Baro’s incoming metrics for today include the “Fed-favoured” Core PCE Price Index along with the month’s Personal Income/Spending.

26 October 2023 – 09:03 Central Euro Time

At present we’ve the Metals Triumvirate higher and the EuroCurrencies lower. Notably for the second straight session (to this point), both Gold and the Dollar are gaining, (“Gold plays no currency favourites”). The Spoo continues to work lower: as we’ve (yet) to see “fear” in the S&P’s MoneyFlow, (when otherwise Flow falls at a faster rate than the Index itself), this feels mildly reminiscent of the old so-called “Gentlemen’s Crash”, although hardly has price fallen nearly to any crash proportion. These next two days have key incoming metrics for the Econ Baro ahead of next Wednesday’s FOMC Policy Statement: today we await the first peek at Q3’s GDP, along with other reports including September’s Durable Orders and Pending Home Sales.

25 October 2023 – 09:07 Central Euro Time

At present, all eight BEGOS Markets are within their respective Neutral Zones for today, and volatility is at best light. In looking at Market Rhythms on a 10-test basis, the most profitably consistent through yesterday are Silver’s 8hr Price Oscillator, 12hr MACD, 6hr Moneyflow and daily Parabolics, plus Oil’s 4hr Moneyflow, the Euro’s daily Moneyflow, and the Swiss Franc’s daily MACD. On a 24-test basis, the best is Gold’s 1hr Price Oscillator. By our S&P MoneyFlow page, we’ve still yet to detect any real fear, even as our “live” P/E (futs-adj’d) is now 36.9x. The Econ Baro gets its back-loaded week underway with September’s New Home Sales.

24 October 2023 – 09:02 Central Euro Time

The Bond, Gold and Copper are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light, save for Copper having already traced 67% of its EDTR (see Market Ranges). By Market Values we’ve Gold in (real-time) +107 points above its smooth valuation line. In tandem with the Dollar having weakened across the past two weeks, by Market Trends the linregs for Gold, Silver, the Euro and Swiss Franc all have rotated to positive; those for the other four BEGOS components remain negative. Yet Silver is still a laggard to Gold, the G/S ratio at 86x vs. the century-to-date average of 68x: as we from time-to-time quip in The Gold Update: “Don’t forget the Silver!”

23 October 2023 – 09:24 Central Euro Time

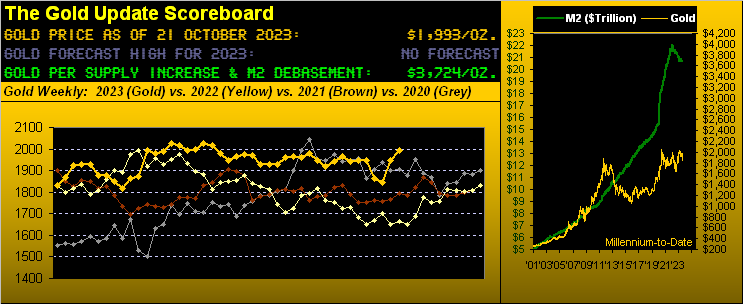

Save for the Spoo, the other seven BEGOS Markets are in the red, all at present below their respective Neutral Zones for today; session volatility is pushing toward moderate. The Gold Update sees the yellow metal as remaining “range-bound” until the All-Time High (2089 vs. the current 1986) is eclipsed, (from which Gold then becomes “moon-bound”, ideally to its present Dollar debasement value of 3724). The Econ Baro is back-loaded this week from Wednesday on, key reports including Q3 GDP and the “Fed-favoured” Core PCE Index. And thus far, Q3 earnings by year-over-year comparison is relatively weak: mind our Earnings Season page.

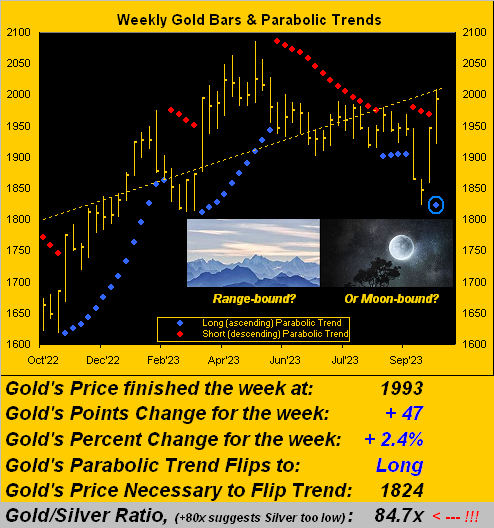

The Gold Update: No. 727 – (21 October 2023) – “Gold: Range-Bound? Or Moon-Bound?”

So: is Gold remaining range-bound? Or is it finally moon-bound? Let’s start with the former.

For the bazillionth time we postulate that “change is an illusion whereas price is the truth”. Whilst the low-information, short-attention span, instant gratification crowd have recently been yanked to and fro through Gold’s plunge before its ![]() “Going to a Go-Go”

“Going to a Go-Go”![]() –[Miracles, ’65], let’s focus on price, the truth to know. To wit:

–[Miracles, ’65], let’s focus on price, the truth to know. To wit:

Today’s 1993 price also traded during 34 of the prior 168 weeks going all the way back to that ending 31 July 2020. And as anyone who is paying attention knows, Gold’s infamous triple top (2089/2079/2085) has yet to be broken, (which they are meant to so do). Thus until the next All-Time High is achieved, price remains range-bound, for 1993 today ain’t anything over which to bray “Olé!” Here is price (i.e. “truth”) via the monthly candles from 2020-to-date, denoting the triple-top:

Neither is it easy for the S&P, given both the geo-political climate and the Index’s ongoing overvaluation, our “live” price/earnings ratio settling the week at 36.2x. And speaking of earnings, (or lack thereof), have you been following their Q3 season? Specific to the S&P 500, 68 constituents have thus far reported: just 34 (50%) of those bettered their bottom lines from a year ago. More broadly? ‘Tis worse: with 134 companies’ (of some 1800 to eventually report) results in hand, just 44% have bettered. Too as tweeted (@deMeadvillePro) this past Thursday, “Flow leads dough…” per our S&P MoneyFlow page depicting a more negative stance.

And again from the “They’re Just Figuring This Out Now? Dept.”, iconic ol’ Morgan Stanley finds U.S. Treasuries attractive at 5%. (‘Course you readers of The Gold Update have known for months that the T-Bill’s been yielding at least 5% since 18 April.) Oooh and this quick update: the market capitalization of the S&P 500 per Friday’s settle is now down to $36.9T; but the liquid money supply (“M2”) of the U.S. is only $20.8T. It doesn’t add up very well, does it? No it doesn’t.

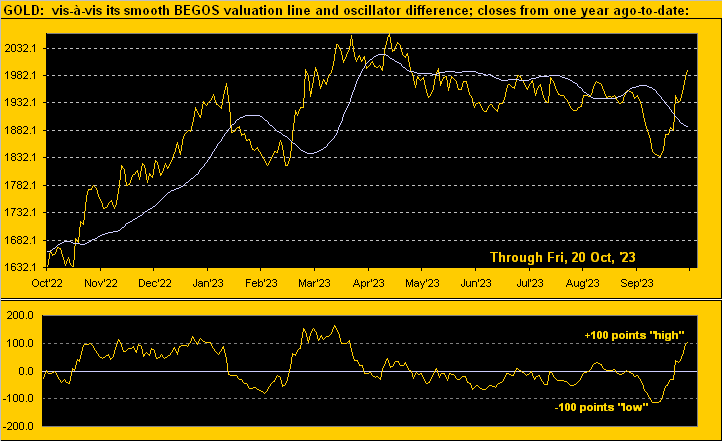

But ’tis adding up quite nicely for Gold as we next go to its two-panel display of daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. The baby blue dots of trend consistency have only just crossed above their 0% axis, suggesting the uptrend has more ![]() “Room to Move”

“Room to Move”![]() –[Mayall, ’69] in spite of near-term technicals being somewhat stretched. Thus given some natural price retraction, we can see the key underlying support levels as labeled in the Profile:

–[Mayall, ’69] in spite of near-term technicals being somewhat stretched. Thus given some natural price retraction, we can see the key underlying support levels as labeled in the Profile:

To sum up, ’twas a great week for Gold and a poor one both for equities and the StateSide Economic Barometer, the latter in the new week looking to the first peek of Q3 Gross Domestic Product and that “Fed-favoured” Core Personal Consumption Expenditures metric for September.

And with geo-politics continuing to dominate the airwaves whilst the lousy Q3 Earnings Season unfolds, one ought expect more of the same at least near-term, albeit liquid markets don’t move in a straight line. But the “Baby Blues” at the website’s Market Trends page tend to keep one on the correct side of it all.

Indeed all-in-all — at least until Gold posts a new All-Time High above 2089 — we still see price as more range-bound than moon-bound. But again, as Jackie points out to Alice:

Or as we time-to-time say: “Tick tick tick goes the clock clock clock…” Got your precious metals?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

20 October 2023 – 08:53 Central Euro Time

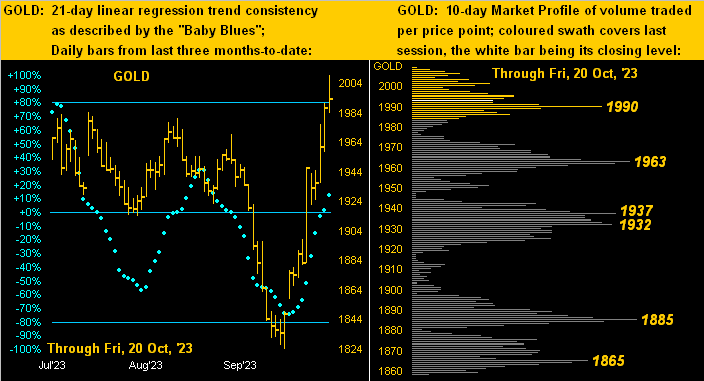

Per our tweet (@deMeadvillePro) last evening, “Flow leads dough…” as is now being depicted on the MoneyFlow page for the S&P 500; too, our notion of the Spoo attaining the 4500 level at least near-term (based on the upside reversal at Market Trends of the “Baby Blues” two weeks ago) is now nixed, even as the Spoo’s 21-day linreg trend has just turned positive; again, 4431 nears to clear for a run to 4500. Today at present, the Bond is above its Neutral Zone; both the Euro and Copper are below same, and BEGOS Markets volatility is mostly light, within the context of Market Ranges (EDTRs) having expanded. Gold’s EDTR is now 26 points, meaning that 2000+ is within range today; presently 1987, Gold’s nearest dominant Market Profile supporter is 1963. The Econ Baro is scheduled to close its week with September’s Treasury Budget.

19 October 2023 – 09:04 Central Euro Time

Narrow ranges thus far characterize the BEGOS Markets: only the Bond is at present outside (below) its Neutral Zone for today, and volatility is notably light, the Bond with the widest EDTR tracing to this point (see Market Ranges) at just 37%. Gold’s weekly parabolic trend has provisionally flipped from Short to Long, (confirmation to come upon Friday’s settle); price, which just two weeks ago was better than -100 points below its smooth valuation line (see Market Ranges) is now (in real-time) 71 points above same. As for the Spoo, should the recent 4431 high not be eclipsed, our 4500 notion likely gets nixed. Incoming metrics for the Econ Baro include October’s Philly Fed Index plus September’s Existing Home Sales and Leading (i.e. “lagging”) Indicators.

18 October 2023 – 10:53 Central Euro Time

The Metals Triumvirate and Oil are the BEGOS Markets’ leaders thus far, those four all at present above today’s Neutral Zones; below same is the Bond, and volatility is moderate. On a $/cac basis, Silver is the broadest mover, at present +$1725. At Market Trends, the Spoo’s “Baby Blues” appear poised to break above their 0% axis by week’s end: again from the week prior we’ve ruminated about the Spoo making a go for 4500, (the S&P’s vastly high “live” P/E of 38.3x notwithstanding). And per the Euro’s page, its best Market Rhythm — the daily MoneyFlow study — triggered a Long signal per yesterday’s open (1.05885). For the Econ Baro we’ve September’s Housing Starts/Permits; then late in the session comes the Fed’s Tan Tome for October.

17 October 2023 – 09:03 Central Euro Time

‘Tis red across the board for the BEGOS Markets, notably with the Bond, Euro, Gold, Copper and Oil all at present below their respective Neutral Zones for today; volatility however is mostly light. On a $/cac change basis, Copper’s is the most at the moment, -$1,012. At Market Trends, whilst all eight components are still in negative linreg trends, all their “Baby Blues” are in ascent, meaning the trends’ downside consistencies are waning. By the Spoo’s Market Profile the most dominant resistor above present price (4394) is 4401. And Oil’s cac volume is rolling from November into December. For the Econ Baro we await October’s NAHB Housing Index, September’s Retail Sales and IndProd/CapUtil, and August’s Business Inventories.

16 October 2023 – 09:12 Central Euro Time

We begin the week with both the Euro and Copper at present above today’s Neutral Zones; below same are the Bond, Gold and Silver. With respect to the yellow metal, note in the current edition of The Gold Update the “tease” as regards Friday’s “Hobson Close”; should Gold further dip, we see structural support in the 1898-1881 zone; as well, 1885 is a key Market Profile support apex for Gold. BEGOS Markets volatility is light-to-moderate. The Econ Baro’s busy week of 14 incoming metrics starts today with October’s NY State Empire Index. And mind our Earnings Season page with reports for Q3 picking up the pace as the week unfolds.

The Gold Update: No. 726 – (14 October 2023) – “Awakening to Gold”

We now close on a memorializing note for James E. Sinclair.

We were honoured to meet “Mr. Gold” in San Francisco some nine years ago on 15 November 2014. Long-time readers of The Gold Update know ’tis infrequent that we read the fine writings of other Gold analysts (so as not to bias our own thinking and interpretation of data). Jim was an exception with whom we occasionally corresponded, and he’d always reply. And his thorough understanding of The Gold Story was rarely paralleled. Thanks for the awakening, Jim.

In his memory, let’s indeed add a word to this moving ’73 Pink Floyd piece, his now resting at ![]() “The Great GOLD Gig in the Sky”

“The Great GOLD Gig in the Sky”![]() :

:

Cheers to Jim!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

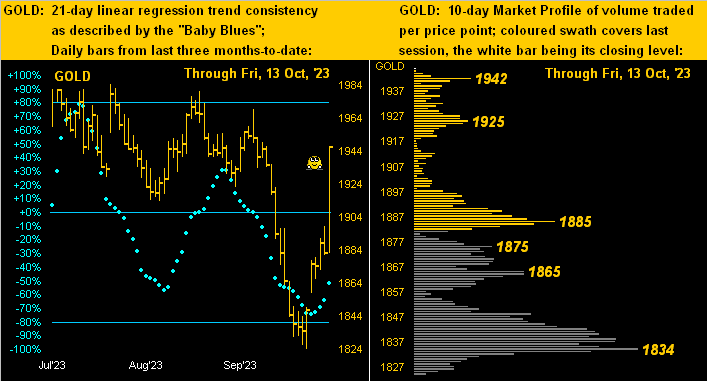

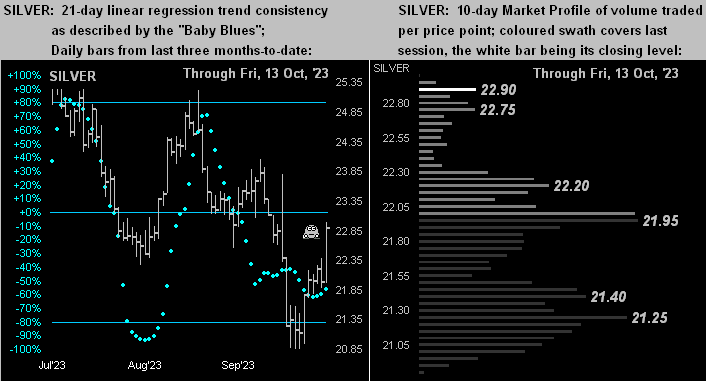

13 October 2023 – 08:58 Central Euro Time

The Bond, Gold and Silver are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is quite light. Even as equities struggled yesterday, there remains no “fear” for the S&P 500 per our cap-weighted MoneyFlow page. Further per our Market Trends page, the Spoo’s “Baby Blues” in real-time continue their ascent; our best Market Rhythm at present for the Spoo on a 10-test basis is its 6hr Moneyflow study; on a 24-test basis ’tis the daily Price Oscillator study. To wrap the week for the Econ Baro, September’s Treasury Budget has been moved to next week; however today we’ve the month’s Ex/Im Prices, plus October’s UofM Sentiment Survey.

12 October 2023 – 08:59 Central Euro Time

Money is moving into the BEGOS Markets this morning: at present, the Bond, Euro, Swiss Franc, Gold, Silver and Copper all are above today’s Neutral Zones; otherwise, Oil and the Spoo are within same, and volatility is again light. At Market Trends, even as all eight components remain in linreg downtrends, respective “Baby Blues” are rising, (save those for Oil). Gold has significantly firmed on the geo-political bid, prior to which price was better than -100 points below its smooth valuation line (see Market Values): that reading in now real-time is just -19 points; whilst as noted the yellow metal tends to decline following geo-political price spikes, price already was overly low pre-event. More in this coming Saturday edition of The Gold Update. The Econ Baro awaits metrics including September’s CPI and the Treasury Budget (originally listed for yesterday).

11 October 2023 – 09:12 Central Euro Time

Copper is the sole BEGOS Market at present outside (above) its Neutral Zone; session volatility is light. As tweeted (@deMeadvillePro) last night, the Spoo did confirm its “Baby Blues” (see Market Trends) moving above the key -80% axis, inferring high price levels: structurally there appears room to move near-term to 4500 (present price is 4393); ‘course as we regularly cite, fundamentally the S&P remains significantly overvalued, its “live” P/E at 38.8x. Gold has (yet) not returned to its pre-Middle East event level of the 1830s: typically such price retrenchments occur following geo-political price-spikes; current price is 1877. The Econ Baro looks to September’s PPI and the month’s Treasury Budget; late in the session we’ve the minutes from the FOMC’s 19-20 September meeting.

10 October 2023 – 09:08 Central Euro Time

A whirl ’round day yesterday for the S&P, arguably getting a safe-haven bid given events in the Middle East; as well the S&P is now “textbook oversold” through 13 days and the MoneyFlow differential is still positive, indicative of “fear” remaining at bay; moreover at Market Trends, the Spoo’s “Baby Blues” are in real-time moving above their -80% level, indicative of further price rise near-term. For today at present, Gold, Copper and Oil are below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility is light-to-moderate. And for the Econ Baro we await August’s Wholesale Inventories.

09 October 2023 – 08:58 Central Euro Time

Expectedly, given the incursion in the Middle East, Gold gapped notably higher at last night’s open and the Spoo notably lower. The latter along along with the Euro are at present below today’s Neutral Zones, whilst above same are the Bond, Metals Triumvirate and Oil; BEGOS Markets’ volatility is moderate. The Gold Update looks to 1800 as support: whilst the geo-political event has given Gold the typical boost, history reminds us that such spikes tend to reverse themselves as the ensuing days unfold; still (in real-time) Gold now at 1865 is -66 points below its smooth valuation line (see Market Values). And of course broadly, Gold remains vastly undervalued by currency debasement and the S&P 500 vastly overvalued by unsupportive earnings.

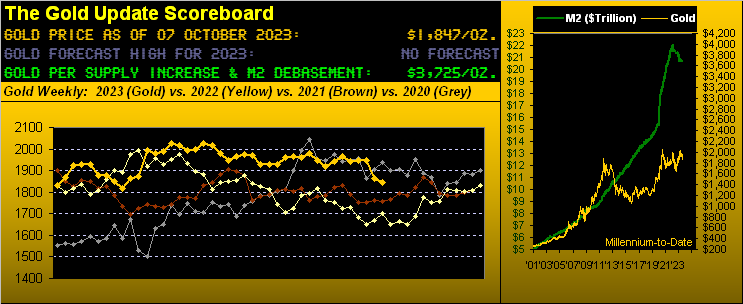

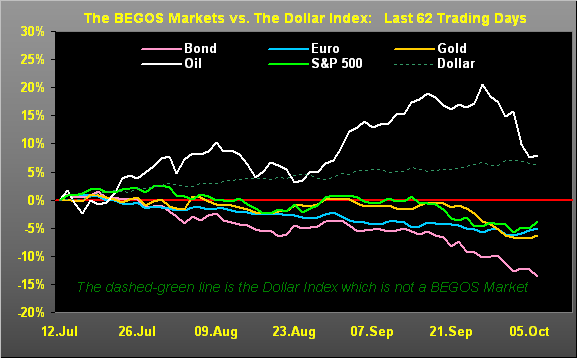

The Gold Update: No. 725 – (07 October 2023) – “Gold Further Tanks; to the Dollar No Thanks”

“Well ya know, Gold is down because of Dollar strength…”

Oh good grief are we sick of hearing that. Honest to Pete, knee-jerk “conventional wisdom” is hardly our investing indicator of choice, especially when it comes to owning Gold, which at this writing — in having settled out the week yesterday (Friday) at 1847 — is as cheap as can be. More on that as we move forward.

But let’s begin by (again) debunking the notion of “Dollar strength”. ‘Tis axiomatic that which is worth zero (“0”) — regardless of it being acceptably transacted in exchange for other currencies, goods and services — is at any price still worth “0”. Further to our point — given we oft quip Gold plays no currency favourites — let’s point (►) to past periods (sampled from three-to-four months in duration) of positive correlative strength for both the Dollar and … oh say it ain’t so … Gold! To wit:

► Just after the turn of the century (which for those of you who can do math began with 2001), the Dollar Index (“Dixie”) from 19 Feb ’01 to 21 May ’01 recorded a net gain of +6%: Gold’s net gain for the identical stint was also +6%.

► How about in 2005: from 29 Aug through 28 Nov, Dixie’s net was +7% and Gold’s was +12%.

► Then there were the FinCrisis throes of 2008: from 08 Sep through 08 Dec both Dixie and Gold netted gains of +7%. Are we having fun yet?

► Check out 2010: from 01 Feb through 14 June whilst Dixie gained +7%, Gold nearly tripled same with +20%. They say: “No Way!” … Way.

► Ah, then came infamous 2011: from 27 Jun through 26 Sep Dixie’s net change was +6% … Gold’s was +9%.

► Three years hence from 27 Oct ’14 through 02 Feb ’15 Dixie netted +9% and Gold a still respectable +5%.

► And similarly just last year in 2022 from 10 Jan through 25 Apr, Dixie gain a net +8% and Gold again a net +5%.

Thus to paraphrase the Johnny Paycheck tune from back in ’77, you can ![]() “Take this Dollar strength and shove it.”

“Take this Dollar strength and shove it.”![]()

Regardless, as we’ve emphasized, of late ’tis hardly just Gold being pinned down by the Dollar. The primary BEGOS Markets (Bond / Euro / Gold / Oil / Spoo) have all — save somewhat for Oil until just these last few days — been on the skids. The following picture depicts their percentage tracks from some three-months ago-to-date along with the green-dashed Dixie:

With Q3 Earnings Season underway and 10 metrics due for the Econ Baro in the new week, let’s wrap here with two notes from deMeadville’s vast array of departments.

First from the “Core No More? Dept.” we perused an interesting essay (hat-tip FI’s Todd Bliman) emphasing that the Federal Reserve evaluates inflation and the economy well beyond the oft-mentioned Core Personal Consumption Expenditures Price Index. We (indeed one would assume all of us) agree, albeit the Core PCE month-in and month-out seems very closely aligned with the Fed’s 2% inflation goal. Nevertheless, as hard-wired ad nauseum throughout the FOMC’s Policy Statements, they “…will continue to monitor the implications of incoming information for the economic outlook…” and oh baby as payrolls grow but consumers lie low, which way shall the Fed go? The next Core PCE reading is three trading days prior to the next FOMC vote.

Second from the “They’re Just Figuring This Out Now? Dept.” (the popularity of which is growing by leaps and bounds), Dow Jones Newswires discovered this past week that “Rising Interest Rates Mean Deficits Finally Matter“. Otherwise, who knew, right? Moreover, does this (finally) threaten the ongoing Investing Age of Stoopid? Stay tuned…

As to ongoing so-called “Dollar strength” ultimately getting shoved, we reprise Daryl Cagle’s oldie-but-goodie graphic given that ultimately 0 = 0: So do stay with Gold and Silver!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

06 October 2023 – 08:58 Central Euro Time

The Eurocurrencies are the weak link thus far with both the Euro and Swiss Franc below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light with September’s Payrolls data due (12:30 GMT). Oil having come off, all eight BEGOS components are now in negative 21-day linear regression downtrends. Specific to the S&P 500, there remains no sight of “fear” given the positive differentials of Index change vs. flow per our MoneyFlow page; too, by “textbook technicals”, the S&P stands as “oversold” through 11 trading days; ‘course, the big fundamental bug-a-boo remains the “live” P/E now 37.6 (futs adj’d real-time). In addition to Labor’s jobs data, the Econ Baro also awaits August’s Consumer Credit late in the sessdion.

05 October 2023 – 09:01 Central Euro Time

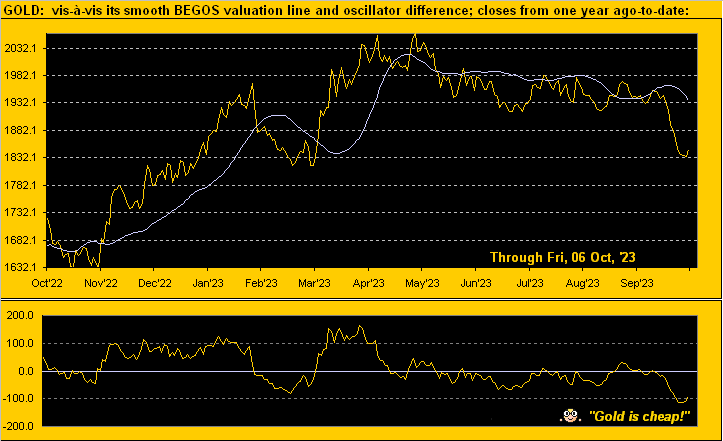

With EDTRS (see Market Ranges) having ramped up of late, the BEGOS Markets are notably subdued this morning, all eight components at present within their respective Neutral Zones for today; volatility is light-to-moderate. As tweeted (@deMeadvillePro) last evening, Oil (the Market Trends sell signal via the “Baby Blues” having come 7 trading sessions ago on 26 September, albeit price initially zooming higher still into the 95s) has finally come off down into the 84s; price has thus finally returned to its smooth valuation line (see Market Values). As for Gold, currently 1836, ’tis (in real-time) -107 points below its smooth valuation line. Today’s incoming metrics for the Econ Baro include August’s Trade Deficit.

04 October 2023 – 09:05 Central Euro Time

Red returns to the BEGOS Markets this morning for all eight components, only three of which are not at present below their Neutral Zones (Euro, Silver, Oil). Session volatility is again moderate to this time of day, and indeed by Market Ranges, EDTRs are (finally) turning upward toward more relatively “normal” levels across the last 12 months. By Market Rhythms: on a 10-test basis the Euro’s daily Moneyflow study is our most consistent, followed by Silver’s 12hr MACD and then again the Euro’s 4hr Parabolics; on a 24-test basis, the best of the bunch is Copper’s 1hr Parabolics. Mind our Earnings Season page as that for Q3 is underway. And for the Econ Baro today we’ve September’s ADP Employment along with the ISM(Svc) Index, plus August’s Factory Orders.

03 October 2023 – 09:02 Central Euro Time

The gutting of Gold (1839) continues, the Dollar Index approaching its 107 handle, a level not seen since November 2021. However, Gold by Market Values is (in real-time) -115 points below its smooth valuation line, a fairly historical extreme: such prior deviation (per 01 July 2021) then found Gold move up by better than +200 points into the start of the 2022 RUS/UKR conflict, even as the Dollar strengthened across the same stint; (more on that in next Saturday’s edition of The Gold Update). At present, Gold is below today’s Neutral Zone, as are the Swiss Franc and Copper; none of the other BEGOS Markets are above same, and volatility is again moderate. At Market Trends, Oil’s “Baby Blues” are (in real-time) accelerating their drop: with the two recent daily lows in the 88s having been breached, the next structural low is 85.49. The Econ Baro is quiet today ahead of 10 metrics due tomorrow through Friday. And Q3 Earnings Season begins this morning.

02 October 2023 – 09:07 Central Euro Time

The BEGOS Markets begin October on a mixed note. At present, we’ve the Bond, Gold and Silver below today’s Neutral Zones, whilst above same are the Swiss Franc, Copper and the Spoo; volatility is moderate. The Gold Update confirms the yellow metal’s weekly parabolic trend as having flipped to Short; and as anticiapted, such trend for Silver today has provisionally flipped as well to Short. Oil continues to flirt with its 90 handle: at Market Trends, Oil’s “Baby Blues” are slowly slipping lower; and at Market Values in real-time, Oil is +7.36 points above its smooth valuation line; price has not been below such line since 03 July, (price then 69.53 vs. today’s 91.24). The Econ Baro awaits September’s ISM(Mfg) Index and August’s Construction Spending.

The Gold Update: No. 724 – (30 September 2023) – “Gold Guillotiné !”

To close, per our aforementioned tease, here we go courtesy of the “Where Have You Been These Last Four Years? Dept.”

Regular readers know — and notably so since 2019 — we’ve been constantly concerned as to the overvalued state of equites, especially the S&P 500 Index as a whole. Oft we’ve quipped that we’re in “The Investing Age of Stoopid” purely by doing the honest math to compute the S&P’s price/earnings ratio, presently 37.7x as opposed to the parroted, dumbed-down 24.5x believed by your broker, (who frankly today appears incapable of doing the math). But that’s where we are now. And as we herein have written ad nauseum through these recent years: “…earnings are not supportive of price…”

Well here it comes… READY?

This past Wednesday the lightbulb finally illuminated in the children’s writing pool over at Barron’s, headlining their webpage “above the fold in bold” with:

“The Stock Market Has a Big Problem. It’s Called Earnings.”

They’re just figuring this out now???

And yet when we view our MoneyFlow page for the S&P 500 — even during its current decline — true “fear” has yet to appear.

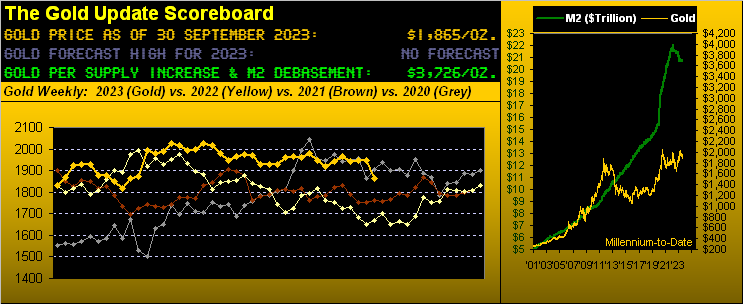

But what appears most appealing to us is Gold being priced today (1865) at just half its Dollar debasement value (3726) per our opening Gold Scoreboard.

Thus — precious metal guillotines and Dollar Revolution aside — in strolling along life’s path, what ought you have glowing in your vault? Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

29 September 2023 – 09:09 Central Euro Time

Following its fourth-consecutive down day, Gold is at present above its Neutral Zone as are Silver, Copper, the Euro and Swiss Franc; none of the other BEGOS Markets are below same, and volatility is moderate-to-robust, the white metal already having traded 108% of its EDTR (see Market Ranges). Oil, which yesterday traded its widest high-to-low range (-3.64 points) since 22 June, still finds its “Baby Blues” (see Market Trends) not having recovered their +80% level, (thus Tuesday night’s Sell signal remains intact if not over-ridden by prudent cash management): price yesterday reached to as high as 95.03 vs. the present 91.71; 90.50 continues as Market Profile support, followed somewhat structurally by the low 88s. Among today’s income metrics for the Econ Baro we’ve September’s Chi PMI, plus August’s Personal Income/Spending along with the Fed-favoured inflation gauge: the Core PCE Index.

28 September 2023 – 09:09 Central Euro Time

Gold’s weekly parabolic trend has provisionally flipped from Long to Short, (as tweeted [@deMeadvillePro] last evening); more on this outlying exception in next Saturday’s edition of The Gold Update. Tweeted too was Oil’s breaking above its recent high (93.74) such that from a cash management perspective ’tis better to stand aside for the moment. At present, Silver is the sole BEGOS Market outside (below) today’s Neutral Zone: currently 22.70, should 22.32 trade, its weekly parabolic trend would also, like Gold, flip to Short. As for the S&P 500, its down-stint during these past two weeks has lacked “fear” as revealed our MoneyFlow page. Today’s metrics for the Econ Baro include August’s Pending Home Sales and the final read of Q2 GDP.

27 September 2023 – 09:06 Central Euro Time

The BEGOS Markets are at present mixed: both the Swiss Franc and Gold are below their Neutral Zones, whilst above same are both the Bond and Oil; volatility is pushing toward moderate. Gold is a disappointment: trading to as low as 1913, should 1905.1 (precisely) trade, the weekly parabolic Long trend shall provisionally flip to Short. As for Oil, despite it being up today, its “Baby Blues” did confirm settling yesterday below their key +80% axis: the price area of 87 to 85 shows some degree of structural support, whilst nearer Market Profile support shows at 90.50; and by Market Values, Oil’s smooth valuation line (in real-time) is 83.19. The Econ Baro looks to August’s Durable Orders.

26 September 2023 – 09:10 Central Euro Time

Red is the watchword for the BEGOS Markets, all of which at present are below their respective Neutral Zones for today. Session volatility is moderate across the board, which is refreshing given the otherwise narrower-than-average EDTRS (see Market Ranges). Oil (currently 88.69) has its real-time “Baby Blue” dot at +78%: if this provisional sub +80% level is confirmed by close, we look to lower price levels, just as was the case some five weeks ago, albeit the downside follow-through from that signal was muted; the average price follow-through of the four “Baby Blues” signals that have occurred from one year ago-to-date is 5.7 points, (which in that vacuum alone from here “suggests” the 83s, without regards for other measurings). The Econ Baro gets its week going with September’s Consumer Confidence and August’s New Home Sales.

25 September 2023 – 09:00 Central Euro Time

The Bond begins its week on a down note, at present trading below today’s Neutral Zone; the balance of the BEGOS Markets are within same, and volatility is mostly light. The Gold Update points to price’s still not being able to get off the mat even as the weekly parabolic trend enters its fifth week of being Long. As for Oil (currently 90.58), its “Baby Blues” (in real-time) have further slipped to the +86% level as we continue to watch for the +80% level to be breached, toward then anticipating lower price levels; at Market Values, Oil is +7.85 points above its smooth valuation line. The Econ Baro looks to 12 incoming metrics for the week, (with none due today), notably featuring the Fed’s favoured inflation gauge of the Core PCE Index for August come Friday.