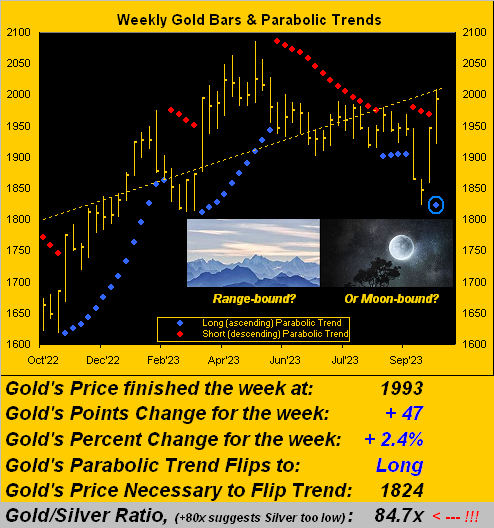

So: is Gold remaining range-bound? Or is it finally moon-bound? Let’s start with the former.

For the bazillionth time we postulate that “change is an illusion whereas price is the truth”. Whilst the low-information, short-attention span, instant gratification crowd have recently been yanked to and fro through Gold’s plunge before its ![]() “Going to a Go-Go”

“Going to a Go-Go”![]() –[Miracles, ’65], let’s focus on price, the truth to know. To wit:

–[Miracles, ’65], let’s focus on price, the truth to know. To wit:

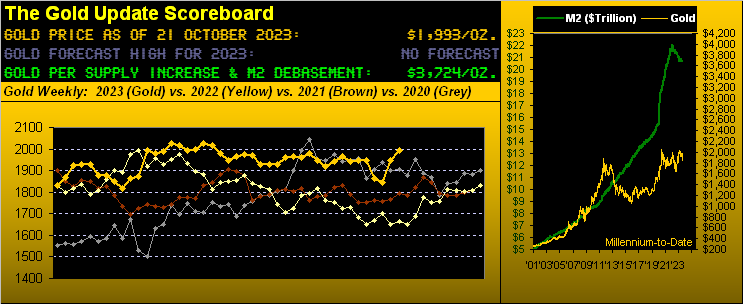

Today’s 1993 price also traded during 34 of the prior 168 weeks going all the way back to that ending 31 July 2020. And as anyone who is paying attention knows, Gold’s infamous triple top (2089/2079/2085) has yet to be broken, (which they are meant to so do). Thus until the next All-Time High is achieved, price remains range-bound, for 1993 today ain’t anything over which to bray “Olé!” Here is price (i.e. “truth”) via the monthly candles from 2020-to-date, denoting the triple-top:

Neither is it easy for the S&P, given both the geo-political climate and the Index’s ongoing overvaluation, our “live” price/earnings ratio settling the week at 36.2x. And speaking of earnings, (or lack thereof), have you been following their Q3 season? Specific to the S&P 500, 68 constituents have thus far reported: just 34 (50%) of those bettered their bottom lines from a year ago. More broadly? ‘Tis worse: with 134 companies’ (of some 1800 to eventually report) results in hand, just 44% have bettered. Too as tweeted (@deMeadvillePro) this past Thursday, “Flow leads dough…” per our S&P MoneyFlow page depicting a more negative stance.

And again from the “They’re Just Figuring This Out Now? Dept.”, iconic ol’ Morgan Stanley finds U.S. Treasuries attractive at 5%. (‘Course you readers of The Gold Update have known for months that the T-Bill’s been yielding at least 5% since 18 April.) Oooh and this quick update: the market capitalization of the S&P 500 per Friday’s settle is now down to $36.9T; but the liquid money supply (“M2”) of the U.S. is only $20.8T. It doesn’t add up very well, does it? No it doesn’t.

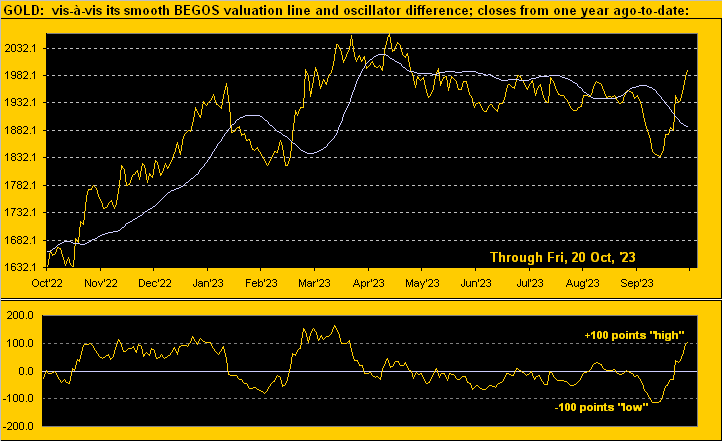

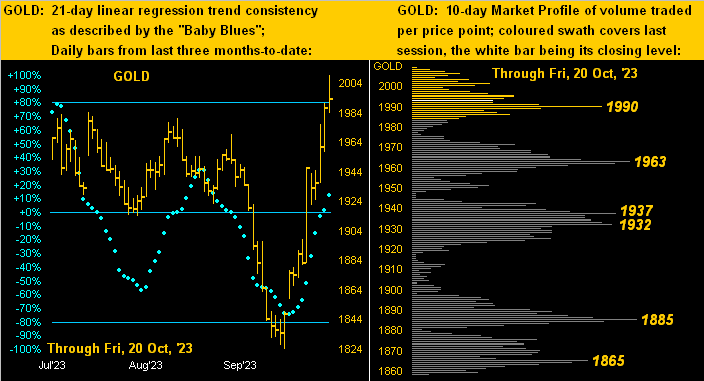

But ’tis adding up quite nicely for Gold as we next go to its two-panel display of daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. The baby blue dots of trend consistency have only just crossed above their 0% axis, suggesting the uptrend has more ![]() “Room to Move”

“Room to Move”![]() –[Mayall, ’69] in spite of near-term technicals being somewhat stretched. Thus given some natural price retraction, we can see the key underlying support levels as labeled in the Profile:

–[Mayall, ’69] in spite of near-term technicals being somewhat stretched. Thus given some natural price retraction, we can see the key underlying support levels as labeled in the Profile:

To sum up, ’twas a great week for Gold and a poor one both for equities and the StateSide Economic Barometer, the latter in the new week looking to the first peek of Q3 Gross Domestic Product and that “Fed-favoured” Core Personal Consumption Expenditures metric for September.

And with geo-politics continuing to dominate the airwaves whilst the lousy Q3 Earnings Season unfolds, one ought expect more of the same at least near-term, albeit liquid markets don’t move in a straight line. But the “Baby Blues” at the website’s Market Trends page tend to keep one on the correct side of it all.

Indeed all-in-all — at least until Gold posts a new All-Time High above 2089 — we still see price as more range-bound than moon-bound. But again, as Jackie points out to Alice:

Or as we time-to-time say: “Tick tick tick goes the clock clock clock…” Got your precious metals?

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro