Just like that. “Who knew?”

Perhaps our neighbour knew in walking past us mid-week with just a single word uttered our way: “3000”.

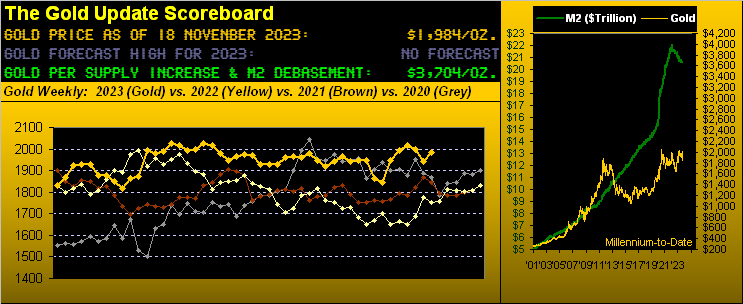

Great to hear some Gold awareness there, even as price settled the week yesterday (Friday) at 1984. Yet per the above Gold Scoreboard, the yellow metal’s Dollar debasement value is 3704. At least somebody’s paying attention.

Or (oui, c’est ‘Gold’ en français): was the utterance of “3000” instead a reference to valuing the S&P 500, itself now 4514? The inevitable reversion of the Index’s honestly calculated price/earnings ratio (43.8x “live”) to our historical 66-year mean (22.7x incorporating Bob Shiller’s CAPE pre-2013) brings the S&P well sub-3000. Further, we’ve on occasion herein graphically depicted that were it not for the massive monetary infusion to counter COVID, the S&P by our 50-year regression channel would today be in the high 2000s, a level otherwise gratefully accepted by the investing community had there been no pandemic monetary response. Just a few things to make one go “hmmm…”

Regardless, let’s break down Gold’s pop, inflation’s stop, and the economy’s flop.

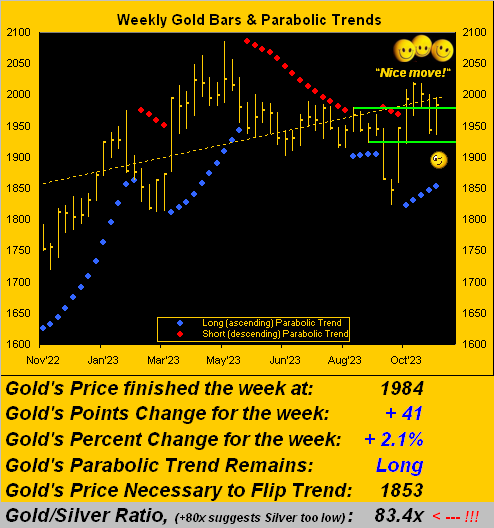

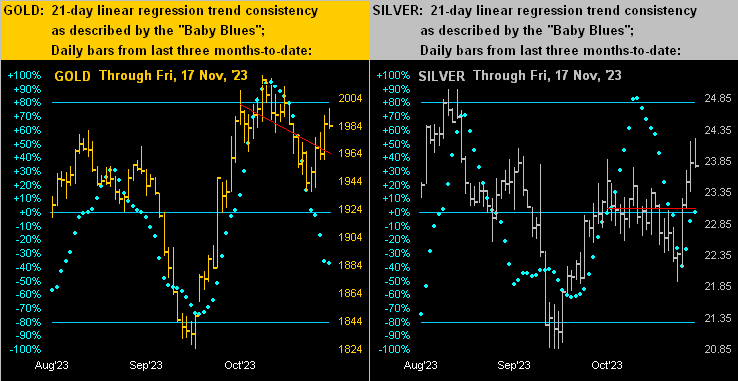

Gold’s pop: per the opening bullet point, this past week saw Gold pop back and settle above the green 1980-1922 support zone, price as noted now 1984, the week’s high en route being 1996 (i.e. just 93 points below the 07 August 2020 All-Time High of 2089). To Gold’s weekly bars from one year ago-to-date we go, the blue-dotted parabolic Long trend firmly in place with a lot of underlying safe space: