Now beyond the world of reality, the S&P 500 is going giddy! Or at least those following it are. On Monday: “The S&P gained +1.2%!” Then Tuesday: “The S&P added another +0.6%!” Wednesday: “The S&P is soaring, +1.1%!” Thursday “The S&P is straight up +1.9%!” Friday: “The S&P is all bullish, up yet again +0.9%!”

And thus for the week the S&P garnered growth of +5.9%. Cue the late, great Howard Cosell: “Looook at it GO!”

Here’s to where we saw it go: merely back to now 4358 as ’twas three weeks ago. Thus predictably, you know the next sentence. “Change is an illusion whereas price is the truth.” In other words, (’tis our turn to say): “Nothing to see here.”

In the midst of it all, ‘natch, is Q3 Earnings Season. And for the S&P 500, of the 381 constituents having so far reported, 65% have made more dough than in Q3 a year ago.

But shouldn’t they all be making more? After all, this is the S&P 500, the top-tier, best-of-the-best. And when it does not all go right, valuation is the plight. Thus our honestly-calculated “live” price/earnings ratio for the S&P went from 34.0x on Monday to 40.5x come Friday’s settle. For you WestPalmBeachers down there, that means if you buy the S&P right now, you’re willing to pay $40.50 for something than earns $1. Further, the cap-weighted dividend yield for the S&P is but 1.625%. Do not reprise ![]() “Bargain”

“Bargain”![]() –[The Who, ’71]. Worth reprising: the U.S. three-month T-Bill annualized yield is now 5.253%.

–[The Who, ’71]. Worth reprising: the U.S. three-month T-Bill annualized yield is now 5.253%.

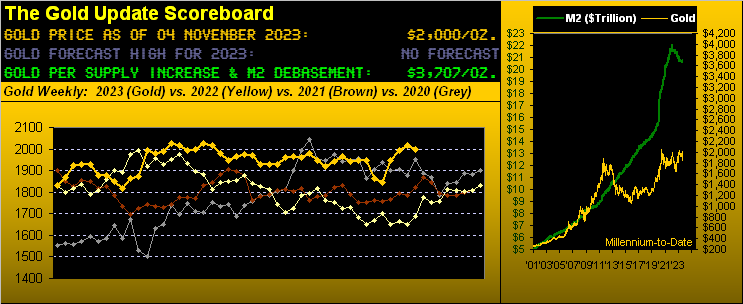

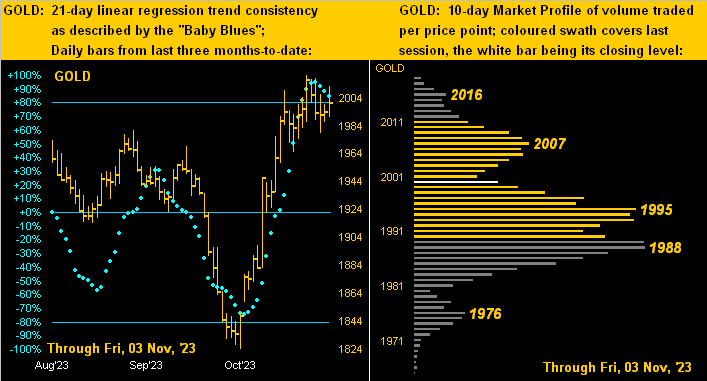

Then there’s Gold, which as aforementioned can rise +85% just to reach its current Dollar debasement value. (Remember: given historically such eventually happens, this is not a difficult decision). And although price may languish near-term in post-geopolitical recoil, we don’t expect it to come well off the boil, (on which is has been for nearly a month).

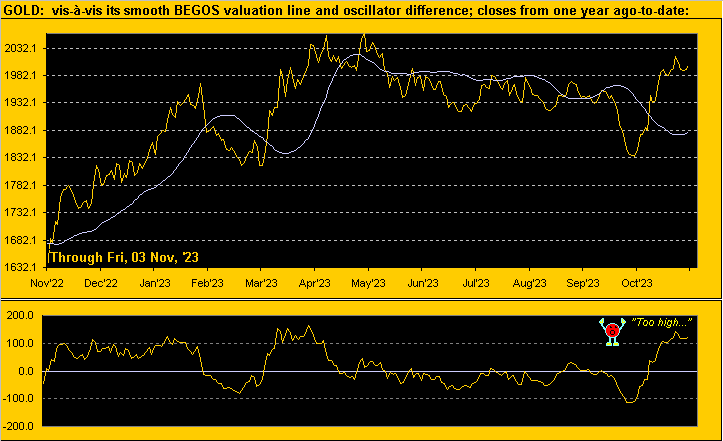

So to Gold’s two-panel graphic we go with the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. Especially note the baby blue dots of trend consistency. Barring price imminently/rapidly rising, those “Baby Blues” shall cross beneath the key +80% axis: such has occurred twice within the past year resulting in subsequent point drops (within 21 days) of -67 and -20 respectively; and that reasonably aligns with the underlying 1980-1922 support structure noted earlier. Specific to trading support, by the Profile the 1995-1988 zone may be the first to go toward further below:

So with our expectations for Gold getting a post-geopolitical pullback — but still more broadly maintain an uptrend — we’ll wrap it up here with this from the “Is the FinMedia Really Running the Fed? Dept.” To wit:

As you all know, the FOMC per this past Wednesday’s Policy Statement unanimously voted to maintain the Bank’s FedFunds target range as 5.25%-5.50%. But did they really need to have their traditional two-day meeting? After all, we were informed the previous Friday (27 October) by Dow Jones Newswires that:

“Inflation Trends Keep Fed Rate Hikes on Pause–Underlying inflation picked up in September, government data showed, keeping the Federal Reserve on track to hold short-term interest rates steady at its next meeting.”

Therefore: why meet at all? Even as the recent inflation data we herein recounted a week ago clearly justified the Fed raising rates, the FinMedia already had decided “No no, Jerome” and that was that. (One wonders if they have to sign non-disclosure agreements. Just a passing thought…)

Regardless of who’s running the Fed show, pullback or not, don’t pass on Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro