“But mmb, those PPI annualized percents are in line with the Fed’s target…”

Duly noted, Squire. If that Producer Price Index is truly leading, then we ought see the other inflation percents stall, if not fall, although the Fed does have a lean toward those Core Personal Consumption Expenditures. As well, Minneapolis FedPrez Neel “Cash n’ Carry” Kashkari per Dow Jones Newswires “…is not convinced rate hikes are over…” Or to reprise the great Bonnie Raitt from back in ’88: ![]() “It’s just too soon to tell…”

“It’s just too soon to tell…”![]()

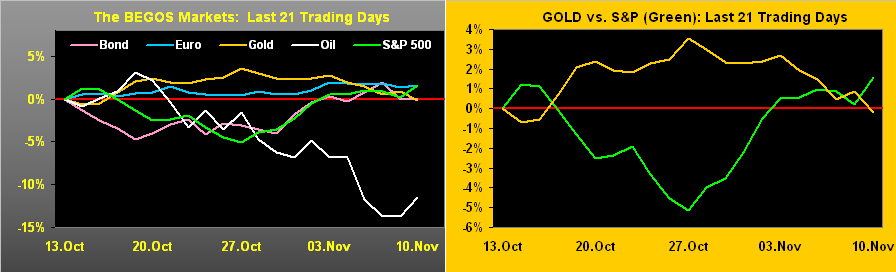

In the midst of all this, we read the Fed’s interest-rate increases of the past two years being deemed as “historic”. Again, the Fed’s Effective Funds Rate is presently 5.33% (i.e. the targeted 5.25% + 5.50% ÷ 2). Hardly is that “historic”. Anyone remember the Prime Rate at 22% back in 1980? We do. (What would be today’s FinMedia adjective for that? “Steroidic”?)

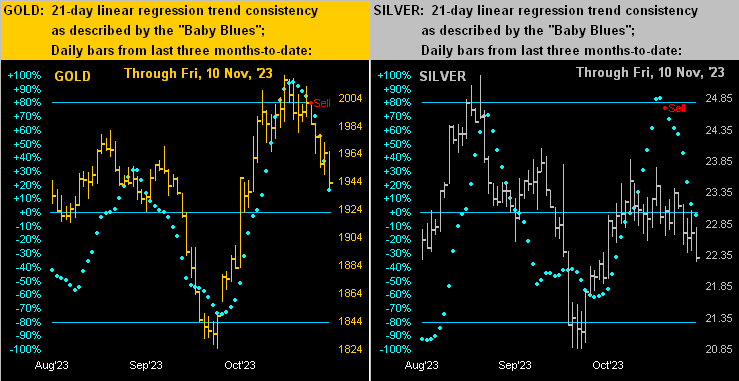

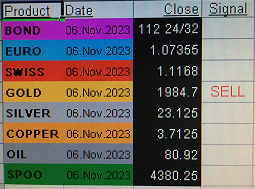

Specific to the precious metals this past week, a more apt adjective would be “atrophic” as next we’ve the two-panel display of Gold’s daily bars for the past three months-to-date at left and same for Silver at right. As aforementioned for Oil, here we’ve the “Baby Blues” signaling “Sell” in both metals’ current cases upon the dots having slipped below their respective +80% axes. Again we commend “The trend is your friend” even if it must descend:

Indeed with respect to Gold, we tweeted (@deMeadvillePro) this graphic last Monday, reflective of the “Baby Blues” heading south:

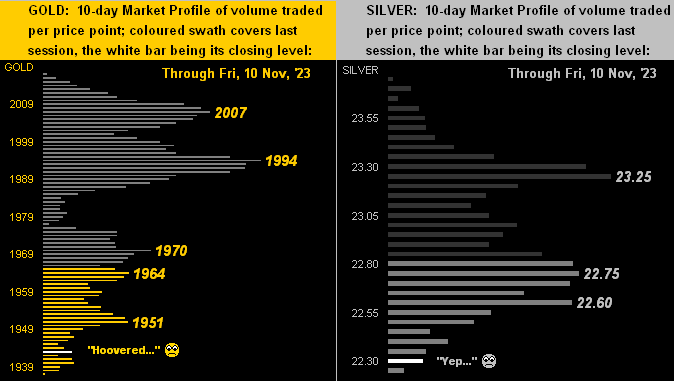

And so in turn we go to the 10-day Market Profiles for Gold (below left) and Silver (below right). Simply stated from high-to-low, the word “hoovered” is apropos, with all labeled lines now overhead trading resistance. As for their two-week percentage changes, Gold’s from top-to-bottom is -4.0% whilst that for Silver is -6.3%. Is it any wonder the Gold/Silver ratio — now 87.1% — is at its second-highest level since last March? No ’tisn’t. Reprise: Do not forget Sister Silver!

Toward the wrap, here’s the stack.

The Gold Stack

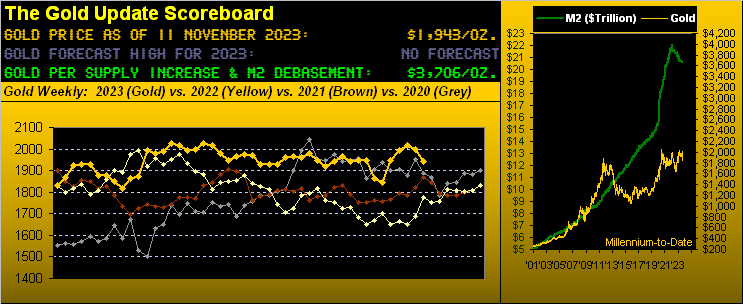

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3706

Gold’s All-Time Intra-Day High: 2089 (07 August 2020)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar ’22); 2085 (04 May ’23)

2023’s High: 2085 (04 May)

Gold’s All-Time Closing High: 2075 (06 August 2020)

10-Session “volume-weighted” average price magnet: 1985

Trading Resistance: 1951 / 1964 / 1970 / 1994 / 2007

Gold Currently: 1943, (expected daily trading range [“EDTR”]: 24 points)

Trading Support: none by the Profile

10-Session directional range: down to 1922 (from 1980) = -81 points or -4.0%

The Gateway to 2000: 1900+

The 300-Day Moving Average: 1883 and rising

The Weekly Parabolic Price to flip Short: 1846

2023’s Low: 1811 (28 February)

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

In sum, Gold is definitely getting the anticipated post-geopolitical pullback. Does it continue? Per the website’s Gold and/or Market Values page, recall that price a mere week ago was +120 points above its smooth valuation line; that deviation has since been reduced to now +39 points. Yet even as Gold’s “Baby Blues” are accelerating lower, again note the cited structural support bases: 1922, 1914 and 1901, the notion thus being that Gold is “safe” above the 1800s.

‘Course, given Gold’s valuation by Dollar debasement is now 3706, ’tis clearly requisite toward maintaining one’s bridge to wealth security.

Thus: don’t be that guy…

…rather consider that Gold today is THE bang-on attractive Buy!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro