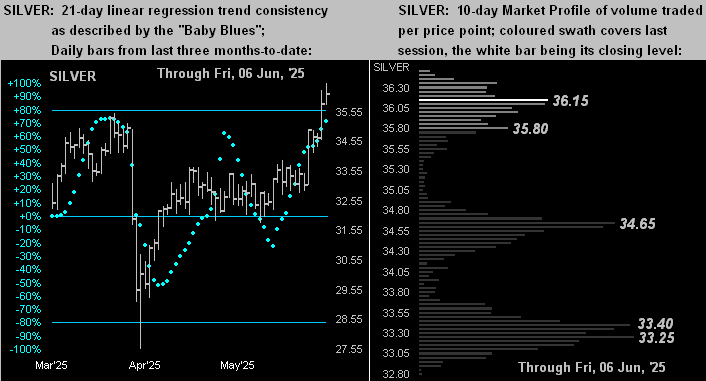

Gold is the sole BEGOS Market at present outside (below) its Neutral Zone for today; session volatility is light. As we look toward tomorrow’s 815th consecutive Saturday edition of The Gold Update, the yellow metal looks to continue its weekly parabolic Short trend, even as price is higher (3299) than when it began (3220); too for Gold, the weekly MACD has provisionally crossed to negative, and price this week has slipped below both its Market Value and Market Magnet; too by Market Trends, Gold’s linreg looks en route to rotating to negative during next week. The event of the day is May’s “Fed-favoured” PCE data, other incoming Econ Baro metrics including the month’s Personal Income/Spending. And should the Spoo be priced above 6198 (currently 6211) upon the commencement of StateSide RTH trading, the S&P 500 would print an all-time high at the open.

Mark

Mark

26 June 2025 – 08:47 Central Euro Time

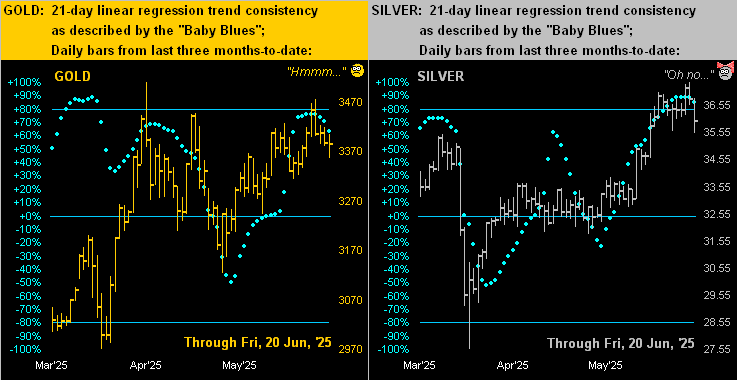

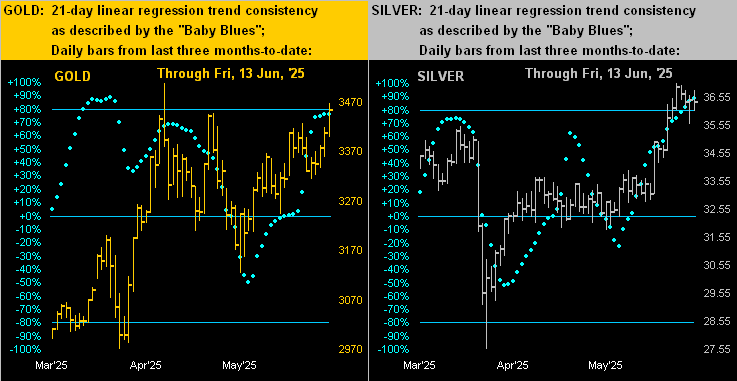

As was the case at this time yesterday, all eight BEGOS Markets are within today’s Neutral Zones; session volatility, whilst light, is rangier than ’twas 24 hours ago. Seems “all are waiting” for tomorrow’s “Fed-favoured” inflation data via May’s PCE. At Market Rhythms, we note on the 24-test basis the pure swing consistency of late for the Bond’s 15mn MACD, the median duration of each swing being some 4-to-5 hours. Per Market Trends, all eight components are in positive linreg, however the “Baby Blues” of trend consistency are dropping for Gold, Silver and Oil; those for Copper have curtailed their fall: the red metal’s daily Parabolics appear poised to flip from Short-to-Long in the next few days, barring a sudden price decline. Incoming Econ Baro metrics include May’s Durable Orders and Pending Home Sales, plus the final read on Q1 GDP.

25 June 2025 – 08:44 Central Euro Time

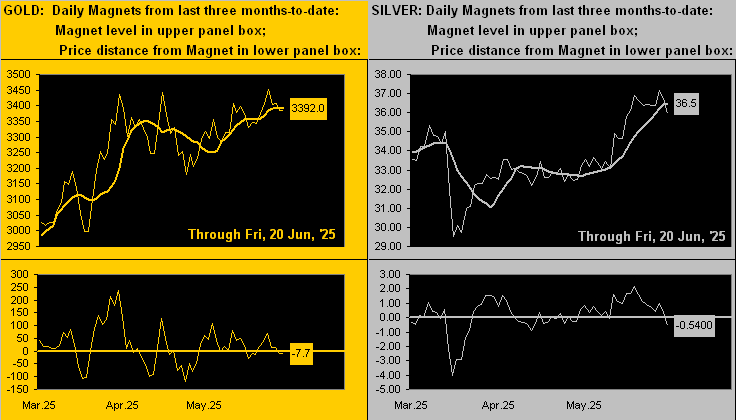

The BEGOS Markets are comparatively quiet across the board given the recent events/ceasefire in the Mid-East: at present, all eight components are within today’s Neutral Ranges and volatility is very light, the average EDTR (see Market Ranges) tracing just 24% to this point. Going ’round the Market Values horn for the five primary components, there are not any overly extreme deviations: in real-time, the Bond shows as -0^30 points “low” beneath its smooth valuation line, the Euro +0.009 points “high”, Gold -45 points “low”, Oil +1.67 points “high”, and the Spoo +121 points “high”, the latter’s EDTR being 82 points. At Market Trends, the “Baby Blues” of linreg consistency for both Gold and Oil confirmed dropping below their key +80% axes, indicative of still lower prices near-term. And the Econ Baro awaits May’s New Home Sales.

24 June 2025 – 08:36 Central Euro Time

Concerns over the Mid-East conflict have basically been absorbed by the BEGOS Markets as a “ceasefire” comes to the fore. The Euro, Swiss Franc and Spoo are at present above their respective Neutral Zones for today, whilst below same are both Gold and Oil; session volatility is firmly moderate. From yesterday’s Oil high of 78.40 to today’s low (thus far) of 64.38 is a -17.9% drop. Copper has been resilient even as its “Baby Blues” (see Market Trends) continue lower still; the red metal’s cac volume is moving from July into that for September as too shall be the case for Silver over the next day or two. The Spoo (on a continuous cac basis) has today tapped 6140, the all-time high being 6167 on 19 February. Today’s incoming Econ Baro metrics are June’s Consumer Confidence and Q1’s Current Account Deficit.

23 June 2025 – 08:21 Central Euro Time

Some five hours following release of The Gold Update came the States’ sortie over IRN; however, to look this morning at the BEGOS Markets, they appear as a fairly normal start to the week, save for volatility being moderate-to-robust; Oil is the only component at present outside (above) its Neutral Zone for today, currently +1.4%; early on, ’twas up as much as +5.9%. Gold presently is -0.4%, The Gold Update suggesting the weekly Short trend becoming “elongated”, notably with the “Baby Blues” (see Market Trends) rolling over to the downside. And the Spoo is -0.2%. The deteriorating Econ Baro has 13 metrics scheduled for this week, commencing with May’s Existing Home Sales.

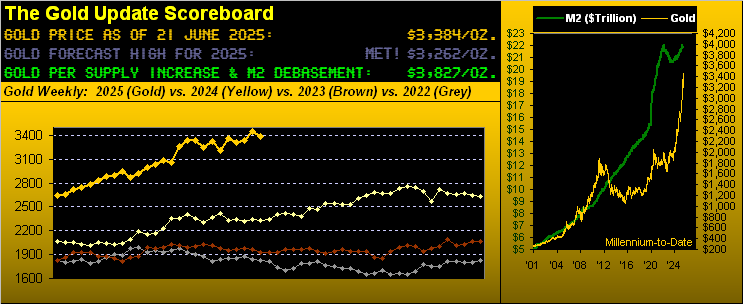

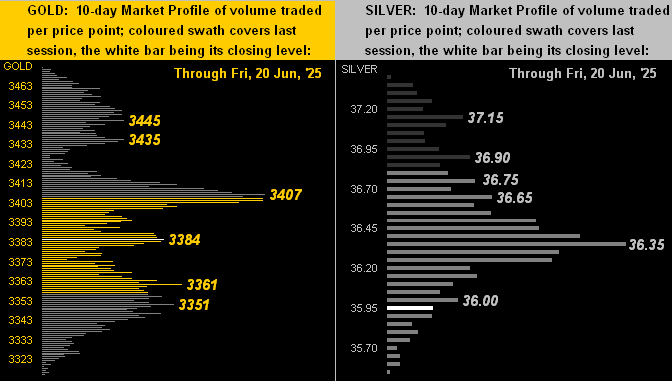

The Gold Update: No. 814 – (21 June 2025) – “Economy Mis-Read by Fed, but Gold’s Rally Turning Red?”

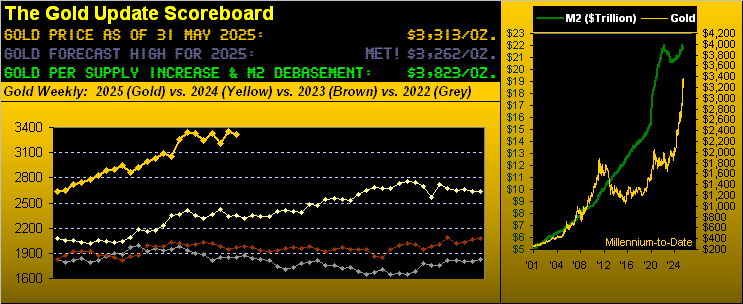

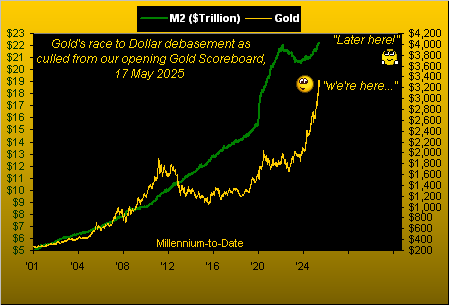

In sum, a bit more pullback in the precious metals ought not be of much concern, (that courtesy of the “Markets Don’t Move in a Straight Line Dept.”) even as we’ve key leading indicators that suggest a bit of a near-term a slip. With 3384 Gold today — a -12% discount to the opening Scoreboard’s Dollar debasement value of 3827 — price’s best days remain well up the Golden Road. Indeed, to eclipse the key 3476 level in the new week — and thus flip the weekly trend from Short back to Long — from here is a distance of +92 points. Gold’s expected weekly trading range? 151 points. Clearly doable, especially should another dose of geo-political jitters ensue. Otherwise, some pullback looks due.

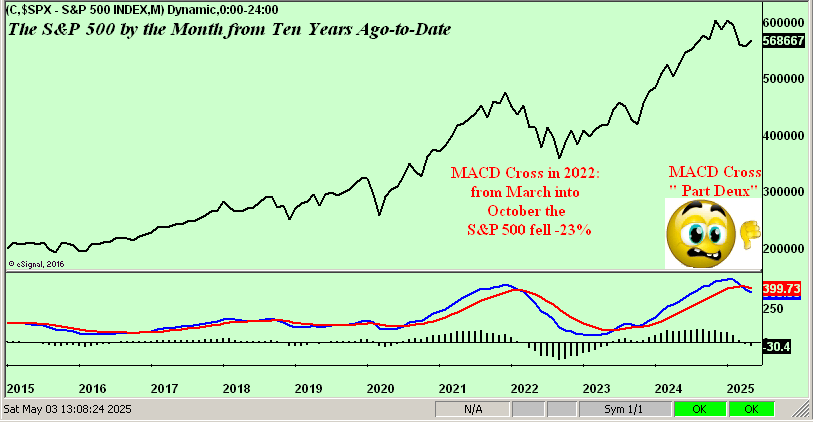

To close, we query: “Do you scare easily?” If you’re invested in equities, the following fearful graphic arguably suggests running for cover. Recall the disconnect with which we opened between the plunging Econ Baro and the flying S&P 500? Scary. More broadly for the S&P, really scary! Such “Casino 500” today at 5968 is some +33% above the top of the yellow regression channel and the “trailing twelve months” price/earnings ratio of 43.5x essentially double any historical norm, (let alone practically triple Jerome B. Cohen’s “…in bull markets the average [price/earnings] level would be about 15 to 18 times earnings…”).

As a fine friend said over coffee this morning “Next year’ll be a disaster for the stock market”, to which we quizzically responded “What about next week?” Scary indeed:

The good news of course is that all such “scariness” is mitigated given economics no longer have meaning, as neither do earnings. Employing math is a thing of the past! Or to reprise what a seasoned investor said to us here back in April: “Nobody at Goldman [today] has ever experienced a down market.” Then to close out the FinMedia week came this yesterday from Dow Jones Newswires: “The Stock Market Has Taken a Lot of Pain for Not Much Gain.” Look at the top of the above graphic. They’ve no concept of what market pain is.

Either way, don’t you get mis-read; get Gold instead!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

20 June 2025 – 08:42 Central Euro Time

The two-day session continues, at present finding the Bond, Euro and Swiss Franc above their Neutral Zones and all three elements of the Metals Triumvirate below same; volatility (as is typical in accounting for two days) is mostly robust. The Spoo yesterday traded below its “low if a down day” (5979), price having since rebounded nearly all the way back up. As anticipated, Copper is weaking as its “Baby Blues” (see Market Trends) drop further still; too, those for both Silver and Gold are curling over to the downside: more on it all in tomorrow’s 814th consecutive Saturday edition of The Gold Update. Oil’s recent strength given the Mid-East strife finds price (in real-time) +12.30 points above its smooth valuation line (see Market Values). And the best correlation currently amongst our five primary BEGOS components is positive between the Bond and Gold, albeit the latter has been coming off a bit. The Econ Baro finishes its week with June’s Philly Fed Index and May’s Leading (i.e. given the Baro, “lagging”) Indicators.

19 June 2025 – 08:47 Central Euro Time

Given the StateSide holiday, ’tis a two-day session for the BEGOS Markets with settlement on Friday. At present, we’ve the the two EuroCurrencies, Metals Triumvirate and Spoo all below their respective Neutral Zones for today, whilst above same is Oil; volatility thus far is moderate, the largest EDTR (see Market Ranges) tracer being Gold at 71%; of note, the yellow metal’s weekly Parabolic trend still is Short and would end the week as such, barring a rally from here (3366) of some +114 points (3480 being the flip-to-Long price) by Friday. As for Copper, its “Baby Blues” (see Market Trends) fallout continues without price (as yet) having materially let go to the downside; however today, Copper has marginally slipped below its most dominant volume price supporter (see Market Profiles) at 4.815. The various trading halts for the holiday commence at 17:00 GMT.

18 June 2025 – 08:34 Central Euro Time

At present we’ve the Euro, Silver and Copper above today’s Neutral Zones, whilst below same is Oil; session volatility for the BEGOS Markets is mostly light, the largest EDTR (see Market Ranges) tracing to this point being 50% for both Gold and Copper. Specific to the red metal, Copper’s “Baby Blues” (see Market Trends) continue their fall as the consistency of price’s uptrend breaks down. Looking at Market Magnets, save for Oil (which yesterday settled 8.73 points above its Magnet) the balance of the BEGOS Bunch are basically at their respective Magnet levels. Due to tomorrow’s StateSide holiday, the Econ Baro today (rather than Thursday) receives the prior week’s Initial Jobless Claims; due too are May’s Housing Starts/Permits. And late in today’s session comes the FOMC’s “no change” Policy Statement, although the plunging Econ Baro and benign (by May) inflation ought be substance for an eventual FedFunds rate cut.

17 June 2025 – 08:37 Central Euro Time

As internally texted last evening, the markets appear to have “priced-in” the Mid-East conflict and now are “on hold” ahead of the Fed on Wednesday: at present, seven of the eight BEGOS Markets are within their respective Neutral Zones for today (Silver being just a tad above same), and session volatility is light-to-moderate. At Market Trends, all eight components are in positive linreg, although the consistency of that for Copper is notably weakening. Oil, which as it did yesterday spiked up and then retreated, still finds by Market Values current price (70.46) +9.65 points “high” above its smooth valuation line; too, the Spoo is at present +151 points “high” by the like measure. ‘Tis quite the cavalcade of incoming metrics due today for the Econ Baro, including June’s NAHB Housing Index, May’s Retail Sales, Ex/Im Prices and IndProd/CapUtil, plus April’s Business Inventories.

16 June 2025 – 08:32 Central Euro Time

Despite Mid-East turmoil, the BEGOS Markets by change appear rather disinterested. Both the Bond and Gold are at present below today’s Neutral Zones, whilst above same are both Copper and the Spoo; session volatility however is moderate-to-robust, primarily as Oil spiked higher at the open to 75.50 but since retreated to now 71.78. The Gold Update acknowledges the weekly parabolic Short trend as having survived another week even as price has been rising throughout: the hurdle for the trend to flip to Long in the new week is 3480, the high today already 3476 before price having since pulled back to now 3436. Cac volume for the Spoo is rolling from June into September with +54 points of fresh premium; (as noted on Friday, Oil’s cac volume is moving from July into August). And 14 metrics come due for the Econ Baro this week, including for today June’s NY State Empire Index.

The Gold Update: No. 813 – (14 June 2025) – “Gold’s Short Strut Has Been Anything But”

Because this Short trend technically (barely) is still in force, we again acknowledge the 2973-2844 support zone. Nonetheless, the distance to flip the Short trend back Long is a mere +27 points above here at the 3840 level. And given Gold’s expected weekly trading range is 152 points, (the daily alone now 62 points) the flip ought come quickly, even per an opening up gap on Monday should geo-political tensions escalate through this weekend. Thus we’re just about there.

“But as you usually say, mmb, price spikes on geo-politics don’t last very long…”

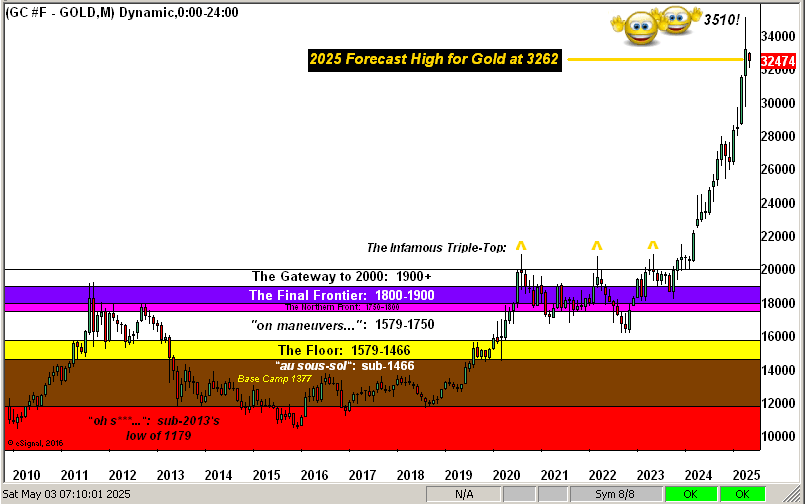

True enough, Squire. Yet should the trend flip to Long in the new week, reflipping it back to Short wouldn’t initially occur until 3123 trades, some -330 points below present price. More importantly: an imminent flip to Long puts a fresh All-Time High above 3510 squarely on the near-term table for Gold: ’tis just +57 points from here. So much for the Shorts singin’ ![]() “I’m struttin’ my stuff, y’all…”

“I’m struttin’ my stuff, y’all…”![]() –[Elvin Bishop, ’75]. (Albeit we ought not disparage the Shorts as they accommodate taking the other side of the trade).

–[Elvin Bishop, ’75]. (Albeit we ought not disparage the Shorts as they accommodate taking the other side of the trade).

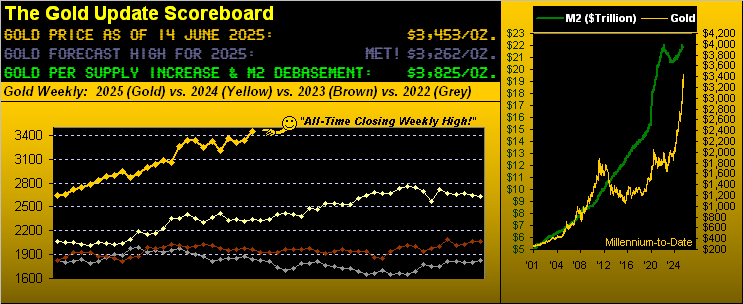

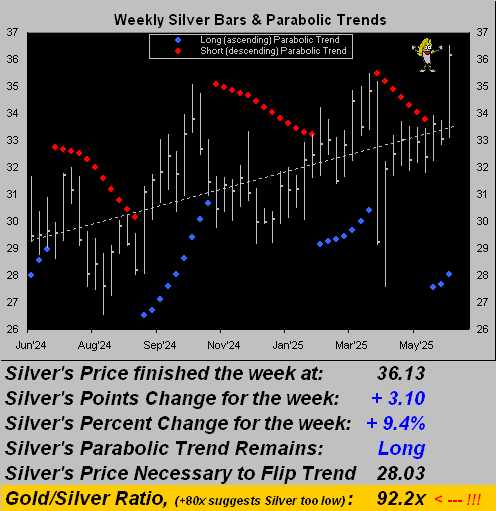

Further for those of you scoring at home, through this year’s 24 trading weeks-to-date, Gold is now +31%, this last week’s gain being third-best by both percentage (+3.7%) and points (+122 points) as depicted in the above graphic. Too, per the website’s “Gold” and “Market Rhythms” pages, Gold’s best Rhythm through its last ten iterations from 03 April-to-date has been the MACD (moving average convergence divergence) on price’s eight-hour series. (But try not to get carried away).

If anything ought be carried away (on a stretcher) ’tis the Economic Barometer. As herein penned a week ago: “…the Econ Baro reached its lowest level in nearly 16 years…”

Still, we’ve this from the “Taking the Good with the Bad Dept.”: as the economy by the Baro is slowing — indeed outright shrinking — inflation for May as measured by the Bureau of Labor Statistics cooled; (May’s “Fed-favoured” PCE is not due until 27 June). Thus the “s” word “stagflation” is not (as yet?) being made “officially” apparent, even if ’tis evident by your own personal engagement in commerce. We certainly sense it: the base cost of our triannual purchase of popping corn from the States (as ever so detailed in Gold Update No. 803 from this past 05 April) just increased +10.1% before shipping, tariff and value-added tax. Yet at least The University of Michigan’s “Go Blue!” Sentiment Survey for June reached a three-month high, (but we can’t see why):

And so toward the wrap here’s The Gold Stack: what can be better than that?

The Gold Stack

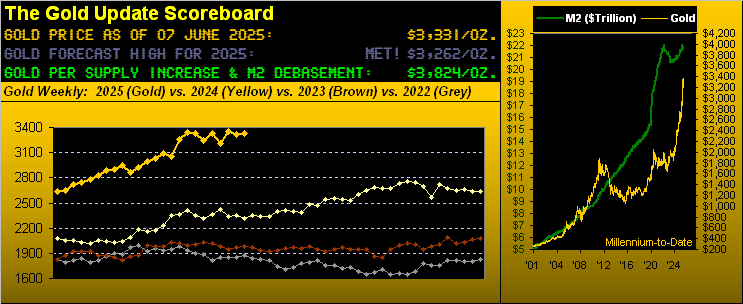

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3825

Gold’s All-Time Intra-Day High: 3510 (22 April 2025)

2025’s High: 3510 (22 April 2025)

The Weekly Parabolic Price to flip Long: 3480

10-Session directional range: up to to 3467 (from 3314) = +153 points or +4.6%

Gold’s All-Time Closing High: 3453 (13 June 2025)

Trading Resistance: none per the Profile

Gold Currently: 3453, (expected daily trading range [“EDTR”]: 62 points)

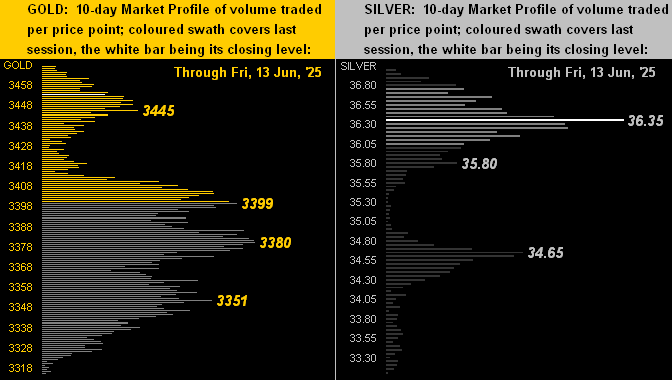

Trading Support: notables by the Profile 3445 / 3399 / 3380 / 3351

10-Session “volume-weighted” average price magnet: 3385

The 300-Day Moving Average: 2721 and rising

2025’s Low: 2625 (06 January)

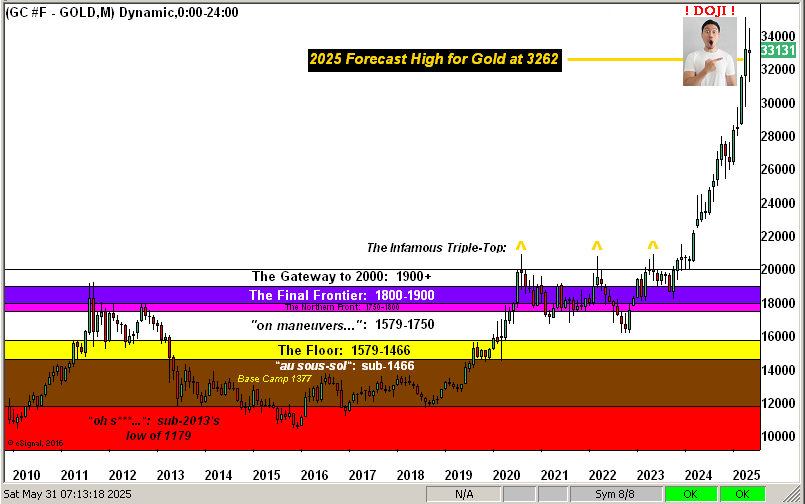

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Come this Wednesday (18 June), the Federal Open Market Committee delivers its next Policy Statement. Expectations call for the FOMC voting to continue maintaining the target range for its Funds Rate at 4.25%-to-4.50% regardless of the faltering Econ Baro and Q1 annualized GDP shrinkage of -0.2%. However as you no doubt recall, the bugaboo coupled to that latter figure was the Q1 Chain Deflator of +3.7% … Ouch! May’s inflation may have cooled, but given economic shrinkage, is there still stagflation linkage? Perhaps rather than order popcorn by the pack, we ought do so by the pallet…

…and thus keep more Gold and Silver in the wallet!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

13 June 2025 – 08:29 Central Euro Time

The overnight Mid-East offensive has made robust the volatility of the BEGOS Markets: notable movers are Oil having traced 443% of its EDTR (see Market Ranges), the Spoo 156%, the Euro 113% and Gold 109%. Presently above today’s Neutral Zones are the Bond, Gold and Oil, whilst below same are the Euro, Copper and the Spoo. Gold is getting the geo-political bid (sans Silver) in having traded to as high as 3467, which is not enough to flip the weekly parabolic Short trend to Long (were 3487 to trade today); more of course in tomorrow’s 813th consecutive Saturday edition of The Gold Update. The Euro’s “Baby Blues” (see Market Trends) in the new week may move below their key +80% axis which would point to lower price levels near-term; the Dollar is firming today (+0.4%) even as Gold is up (+1.1%). The EuroCurrencies’ cac volumes are rolling from June into those for September; watch same for Oil from July into August toward Monday. And the Econ Baro wraps its week with UofM’s Sentiment Survey for June.

12 June 2025 – 08:33 Central Euro Time

Presently, the Euro and Swiss Franc are above today’s Neutral Zones, whilst below same is Oil; BEGOS Markets’ volatility is mostly moderate. At Market Trends, all eight components are in positive 21-day linreg, which reflects the downturn in the Dollar Index from 100.840 a month ago to now 98.360. However, going ’round the Market Values horn in real-time, we’ve the Bond -2^05 points “low” vis-à-vis its smooth valuation line; for the other primary components, the Euro shows as essentially in synch with such valuation, Gold as +50 points “high”, Oil as +5.99 points “high” and the Spoo as +185 points “high”. Today’s incoming metrics for the Econ Baro include wholesale inflation per May’s PPI.

11 June 2025 – 08:42 Central Euro Time

All eight BEGOS Markets are presently within their respective Neutral Zones for today and session volatility is light. Looking at Market Rhythms on a 10-test basis the current leaders are the Spoo’s 12hr Parabolics and Gold’s 6hr MACD; on a 24-test basis we’ve (yet again) the non-BEGOS Yen’s daily Price Oscillator, plus the Euros 2hr Parabolics and the Swiss Franc’s 1hr MACD. By Market Trends, in real-time the “Baby Blues” for both the Euro and Swiss Franc are kinking lower for the first time in some three weeks, an early indication that their recent rallies are running out of puff; the Spoo’s “Baby Blues” have stalled their descent, but have not reversed back upward. The Econ Baro looks to May’s retail inflation via the CPI; and late in the session come’s the month’s Treasury Budget.

10 June 2025 – 08:42 Central Euro Time

Silver is the sole BEGOS Market at present outside (below) its Neutral Range for today; session volatility is pushing toward moderate, following a fairly narrow day yesterday; indeed by Market Ranges, all eight BEGOS components have seen plunging EDTRs over the last month. At Market Trends, only the Bond is in negative linreg, however ’tis rotating toward positive; and in real-time, the “Baby Blues” of trend consistency are rising across the board including ~barely~ for the Spoo, the latter’s having been in descent for some three weeks without price (as yet) succumbing per se. Regardless, the S&P 500 continues its significant overvaluation, the “live” (futs-adj’d) P/E currently 47.0x and yield a wee 1.282% vs. 4.240% annualized for the 3mo. U.S. T-Bill. Nothing is due today for the Econ Baro ahead of inflation data into the balance of the week.

09 June 2025 – 08:37 Central Euro Time

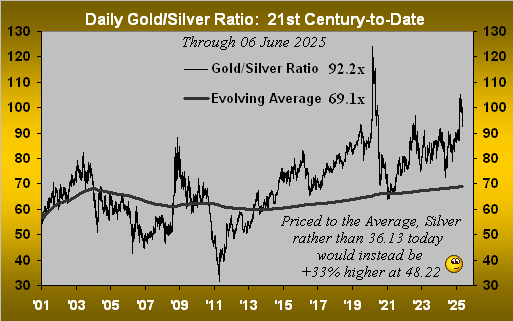

The Euro, Swiss Franc and Silver are all at present above today’s Neutral Zones; none of the other BEGOS Markets are below same, and session volatility is light. The Gold Update highlights Silver’s +9.4% net gain for last week, whereas that for Gold was just +0.5%; and yet with the Gold/Silver ratio now 91.9x, relative to the yellow metal, the white metal nonetheless remains cheap given the century-to-date average ratio of 69.1x. Per Market Values, Gold is essentially on its smooth valuation line; the Spoo however is +258 points above same; and yes, the Spoo’s “Baby Blues” (see Market Trends) are lower yet again without price having materially fallen, albeit such leading indicator suggests the selling is coming. For the Econ Baro — the negative divergence of which from the S&P 500 is stunning — the week begins with April’s Wholesale Inventories.

The Gold Update: No. 812 – (07 June 2025) – “Gold Lies Low Whilst Silver Steals the Show”

Regardless, Gold intra-week had been up as much as +3.5% before basically ![]() “…giving it all away…”

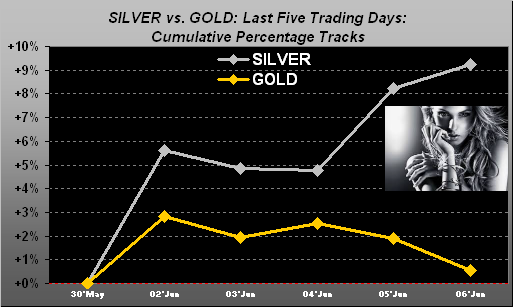

“…giving it all away…”![]() –[Roger Daltery, ’73]. Thus the Short trend continues from which an ascent up through 3487 in the new week would initiate a new Long streak. Such level is +156 points higher from here, which is not that unrealistic as Gold’s expected weekly trading range is presently 151 points. But should the Short trend stubbornly persist, we remain mindful of the underlying 2973-2844 support zone as maintained on the above graphic. Either way, for these past five days, the spotlight has shown upon Sweet Sister Silver per her cumulative percentage track versus that for Gold:

–[Roger Daltery, ’73]. Thus the Short trend continues from which an ascent up through 3487 in the new week would initiate a new Long streak. Such level is +156 points higher from here, which is not that unrealistic as Gold’s expected weekly trading range is presently 151 points. But should the Short trend stubbornly persist, we remain mindful of the underlying 2973-2844 support zone as maintained on the above graphic. Either way, for these past five days, the spotlight has shown upon Sweet Sister Silver per her cumulative percentage track versus that for Gold:

All-in-all, a stunning and well-overdue super week for Silver. And again, relative to Gold, Silver is still a bargain. But the inexorable passage of time marches ever onward, the ensuing week’s StateSide highlights being both retail and wholesale inflation readings for May. Consensii for the Consumer Price Index sense same or an uptick from April’s pace, whilst the Producer Price Index is expected to have swung from DEflationary back to inflationary. We therefore graphically query:

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

06 June 2025 – 08:30 Central Euro Time

Into week’s end finds Silver — having yesterday made a 13-year high — at present above its Neutral Zone for today as is the Spoo, whilst below same is the Swiss Franc; BEGOS Markets’ volatility is light. And yes, despite the Spoo being higher, its “Baby Blues” of linreg consistency (see Market Trends) are lower for an 11th consecutive session; per Market Values, the Spoo (in real-time) is +252 points “high” over it smooth valuation line, whilst the S&P 500 itself is “textbook overbought” with a P/E (“live” 46.3x) basically double the historical multiple. By Market Profiles, overhead Spoo resistance shows in the 5978-5982 zone, and underlying support from 5923 to 5915. The Econ Baro awaits the data for May’s Payrolls, plus late in the session comes April’s Consumer Credit. Obviously we’ll salute Sister Silver in tomorrow’s 812th consecutive Saturday edition of The Gold Update.

05 June 2025 – 08:37 Central Euro Time

As was the case at this point yesterday, all eight BEGOS Markets are within today’s Neutral Zones; session volatility is very light. The fallout continues in the Spoo’s “Baby Blues” of trend consistency such that we still anticipate (as first mentioned back on 26 May) a near-term move down into the lower 5700s/5600s, whereas presently price is 5974 and is in real-time by Market Values +291 points above the smooth valuation line. The best correlation amongst the five primary BEGOS components continues to be positive between the Euro and Gold; the latter remains in its weekly parabolic Short trend even as price has been quite resilient throughout the past three weeks. Incoming metrics today for the Econ Baro include April’s Trade Deficit and the revisions to Q1’s Prod/CapUtil.

04 June 2025 – 08:41 Central Euro Time

Presently, all eight BEGOS Markets are within today’s Neutral Zones and volatility is light. In assessing the best Market Rhythms for pure swing consistency: on a 10-test basis we’ve Gold’s 6hr MACD, the Euro’s 1hr MACD, and the Bond’s 12hr Parabolics; for the 24-test basis the leaders are the non-BEGOS Yen’s daily Price Oscillator and that for 1hr, plus Gold’s 1hr MACD and 4hr Parabolics. As regularly noted of late, the Spoo’s “Baby Blues” continue to fall (see Market Trends) with price yet to cave. And for the BEGOS bunch at large, all — save for the Bond — are in linreg uptrends, albeit weakening as just cited for the Spoo as well as for Oil. The Econ Baro looks to May’s ADP Employment data and ISM(Svc) Index. Then late in the session comes the Fed’s Tan Tome.

03 June 2025 – 08:35 Central Euro Time

Following a sharp up day for the Metals Triumvirate, all three elements are at present below their respective Neutral Zones for today, as is the Spoo; the balance of the BEGOS Markets are within same, and volatility is again moderate. At Market Trends, the Spoo’s “Baby Blues” are yet again further falling as the linreg consistency of the uptrend continues to weaken, whilst at Market Values the Spoo (in real-time) is +298 points above its smooth valuation line; and by Market Profiles, the most dominantly-traded price of the past fortnight is 5915; the “live” P/E for the S&P 500 itself is 47.0x. The Econ Baro is basically at its lowest level since 22 August, and due today are April’s Factory Orders.

02 June 2025 – 08:34 Central Euro Time

The sole BEGOS Market at present within today’s Neutral Zone is the Bond; below same is the Spoo and the balance of the bunch are above same; session volatility is moderate, and Copper notably already has traced 125% of its EDTR (see Market Ranges). The Gold Update sees price as having been more in a stall than a fall, albeit the weekly parabolic Short trend is entering its fourth week. The Spoo’s “Baby Blues” (see Market Trends) of linreg consistency continue to drop, whilst those for the Bond on Friday confirmed moving up above their -80%, suggesting further near-term recovery for price combined with some yield softening. The Econ Baro beings a fairly busy week with May’s ISM(Mfg) Index and April’s Construction Spending.

The Gold Update: No. 811 – (31 May 2025) – “Gold Doesn’t Fall So Much As Stall”

And just like that, five months of 2025 already are gone. Or as a fine friend over in the States is wont to say, as we age: “It goes quickly.”

But back in the late 18th century, the sixth President of the Commonwealth of Pennsylvania (one Benjamin Franklin) lived to be 84 years of age, far more than double the male longevity expectancy of then just 36 years. And “quickly” or otherwise, ol’ Ben is still going in continuing to grace the face of today’s $100 Federal Reserve Note. ‘Course in 1928, he already was on the Treasury’s $100 Bill, which as a Gold Certificate was thereto redeemable. In those days, Gold was fairly fixed-priced at $20.67/ounce, the $100 Bill thus convertible into 137 grams of Gold…

…whereas today’s $100 fetches less than one gram, (0.85 grams or 0.03 ounces).

Therefore: a lot can happen in less than 100 years. Shall your potentially centenarian children have enough to survive a century? Reprise: “Got Gold?“

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

30 May 2025 – 08:29 Central Euro Time

The Euro, Gold and Silver are presently below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility is light. Gold — barring turning ’round into an up day — is en route to recording a fourth down week in the last six, albeit price hasn’t (yet?) materially succumbed to the recently new weekly parabolic Short trend; more of course in tomorrow’s 811th consecutive Saturday edition of The Gold Update. Yesterday was a “failure day” for the Spoo, the entirety of its intra-day +82 gain being hoovered away; still, the S&P MoneyFlow has been robust across all three of our timeframes (see S&P 500/Moneyflow), and technically, the Spoo’s daily parabolics just flipped from Short-to-Long at today’s open; either way, the overvaluation of the S&P remains critical. The Econ Baro wraps the week, indeed the month, with May’s Chi PMI and revised UofM Sentiment Survey, plus April’s Personal Income/Spending and (the BIG event) “Fed-favoured” PCE inflation data. “Sell in May and go away”? On verra…

29 May 2025 – 08:38 Central Euro Time

The Bond, Euro and Swiss Franc all are at present below today’s Neutral Zones, whilst above same are Silver, Oil and the Spoo; session volatility is moderate-to-robust, the Spoo notably having already traced 103% of its EDTR (see Market Ranges). By Market Values, the Spoo (in real-time) is now +449 points above its smooth valuation line and the futs-adj’d P/E of the S&P 500 is 47.1x; by Market Trends, the Spoo’s “Baby Blues” of linreg consistency have yet again slipped in spite of this up session. Looking at correlations for the five primary BEGOS Markets, the best continues to be positive between the Euro and Gold; too of note is the negative correlation between Gold and the Spoo. Amongst today’s incoming metrics for the Econ Baro are April’s Pending Home Sales and the first revision to Q1 GDP.

28 May 2025 – 08:32 Central Euro Time

Both the Euro and Copper are at present below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility is light. Gold is picking up +27 points of fresh premium as the cac volume rolls from June into that for August; too, the Bond’s cac volume is moving from June into September. Despite yesterday’s strength in the Spoo (+2.2%), the “Baby Blues” of trend consistency are lower still today in real-time, again suggesting a return (as previously noted) into the low 5700s/5600s, (barring the Blues getting a grip). Looking at Market Rhythms, on a 10-test basis our current leaders for pure swing consistency are Gold’s 6hr MACD, the Spoo’s 12hr Parabolics, the Bond’s 15mn EMA, and the non-BEGOS Yen’s 1hr EMA; on a 24-test basis, we’ve the Yen’s daily Price Oscillator, the Euro’s 30mn MACD and Gold’s 4hr Parabolics along with its 30mn MACD. Nothing is due today for the Econ Baro. And late in the session come the FOMC minutes from the 06/07 May meeting.

27 May 2025 – 08:30 Central Euro Time

The two-day GLOBEX/BEGOS Markets’ session continues, now finding the Bond, Euro and Spoo above their respective Neutral Zones, whilst below same are Gold and Copper; session volatility is firmly moderate, the Bond notably having traced 119% of its EDTR (see Market Ranges). By Market Trends, three are sporting positive linregs: Silver, Oil and the Spoo; however with respect to the latter, as noted yesterday the Spoo’s “Baby Blues” have fallen below their +80% axis, despite the current session’s up strength. Per the Spoo’s 10-day Market Profile, the overheard dominant volume resistors (price currently 5883) are 5908, 5938, and 5959. And by Market Rhythms, for the Spoo’s pure swing consistency, its current best study is the 12hr Parabolics. The Econ Baro awaits May’s Consumer Confidence and April’s Durable Orders.

26 May 2025 – 08:41 Central Euro Time

The StateSide holiday elicits a two-day session (with Tuesday settle) for the GLOBEX/BEGOS Markets. Thus far we’ve both the Bond and Gold below today’s Neutral Zones, whilst above same are both the Euro and Spoo; session volatility is mostly moderate. The Gold Update cites the very firm week (+4.8%) for the yellow metal, however reminds that the weekly parabolic trend is Short. The Spoo is off to a robust start for this week (at present +1.2%); yet as suggested in Friday’s comment, by Market Trends, the Spoo’s “Baby Blues” of linreg trend consistency have now (provisionally in real-time) fallen below the key +80% axis, indicative of lower levels near-term, perhaps into the lower 5700s/5600s by price structure; indeed the Spoo by Market Values is (in real-time) +377 points above its smooth valuation line. 11 incoming metrics are due for the Econ Baro as the week unfolds, notably April’s “Fed-favoured” PCE come Friday.

The Gold Update: No. 810 – (24 May 2025) – “Gold’s Bull Snorts and Boffs the Shorts”

So in a nugget: Gold’s daily trend is up within a weekly trend that is down. And during the ensuing holiday-shortened trading week come 11 metrics for the Econ Baro, included as noted “Fed-favoured” inflation data per the PCE. Where shall Gold be, let alone the S&P? To speak fundamentally, the former remains undervalued whilst the latter severely overvalued. (So much for the ol’ “EMH” Efficient Market Hypothesis). For today, less yield (S&P 1.321%) is better than more yield (T-Bill 4.230%). “But Gold is yield-less!” they say. And yet ‘from 2001, ’tis outperformed the S&P (including dividends) by nearly three times! Gold wins.

Speaking of sports, tomorrow (Sunday) is race day here. Hat-tip Steinmetz Diamonds: how about a Gold, diamond-encrusted F1 car?

Whereas in racing ’tis best not to venture beyond the edge of adhesion, go for the Gold with all due reason!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

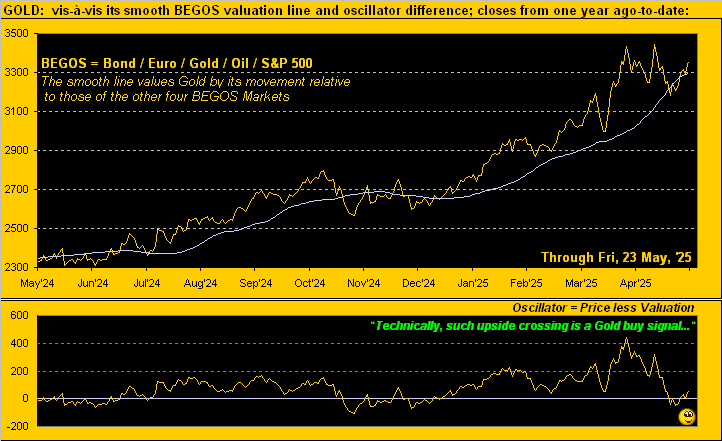

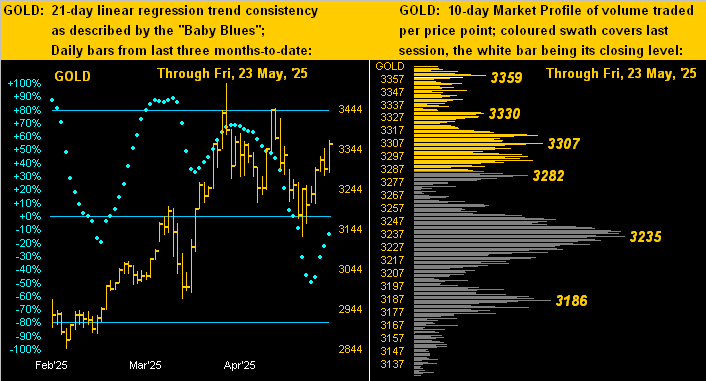

23 May 2025 – 08:33 Central Euro Time

At present the Euro, Swiss Franc, Gold and Silver are above today’s Neutral Zones, while below same is the Spoo; session volatility for the BEGOS Markets is light. Gold — currently in the first week of its fresh parabolic Short trend — had seen its daily parabolics flip to Short effective 01 May: yesterday that study reversed to Long; obviously the broader measure (weekly) carries more price swing import, and we’ll of course further assess the situation in tomorrow’s 810th consecutive Saturday edition of the Gold Update. The Spoo’s daily MACD appears poised to make a negative crossover into early next week; (note the five-hour Spoo trading halt during Monday’s StateSide observance of Memorial Day); too, the Spoo’s “Baby Blues” (see Market Trends) are curling over such that a breach of the +80% axis looks to occur early in the new week. And the Econ Baro wraps its own week today with April’s New Home Sales.

22 May 2025 – 08:34 Central Euro Time

Both Gold and Copper are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility is moving toward moderate. Topping Market Rhythms for pure swing consistency we’ve (on a 10-test basis) both the non-BEGOS Yen’s 1hr Price Oscillator and 1hr EMA (the Yen now higher for an eighth consecutive day), along with Gold’s 6hr MACD and the Spoo’s 12hr Parabolics (which flipped to Short yesterday at 12:00 CET; too in real-time, the Spoo by Market Values is +387 points above its smooth valuation line); plus (on a 24-test basis) we’ve the Yen’s daily Price Oscillator, Copper’s 4hr Parabolics along with Gold’s 4hr Parabolics, and the Bond’s 1hr Price Oscillator. Included in today’s metrics for the Econ Baro are Existing Home Sales for April.

21 May 2025 – 08:22 Central Euro Time

Gold, despite its now being in a weekly parabolic Short trend, nonetheless is having a very firm week thus far, currently +108 points from last Friday’s settle; the yellow metal for today is at present above its Neutral Zone, as too are the Euro, Swiss Franc and Oil; below same are both the Bond and Spoo. Volatility for the BEGOS Markets is moderate, Oil itself having already traded 102% of its EDTR (see Market Ranges). The non-BEGOS Yen is rising for a seventh consecutive day, a streak which has occurred but once this decade-to-date, (following which it swiftly took a -3% tumble in early December 2022). Amongst the five primary BEGOS components, the best current correlation is positive between the Euro and Gold. And the quiet week continues for the Econ Baro, again with no metrics due today.

20 May 2025 – 08:38 Central Euro Time

The “life-cycle” of the Moody’s StateSide debt downgrade was short-lived, the S&P 500 concluding yesterday in the black: the Index is now 16 consecutive trading days “textbook overbought” and the Spoo in real-time +497 points above its smooth valuation line, even as at present the Spoo along with Gold and Copper are below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is mostly light. By Market Trends, the Euro’s “Baby Blues” of linreg consistency have provisionally curled up above their -80% axis; confirmation by settle would be indicative of still higher Euro levels near-term, although structurally there does not appear to be that much room to move materially up: currently 1.1270, there is Market Profile resistance in the 1.1370 to 1.1390 zone. Nothing is due today for the Econ Baro, which nonetheless has taken a bit of a hit of late.

19 May 2025 – 08:43 Central Euro Time

The Bond, Oil and Spoo are all at present below their respective Neutral Zones for today, whilst above same are the Euro, Swiss Franc, Gold and Silver; BEGOS Market’s volatility is pushing toward moderate. The Gold Update points to the yellow metal’s weekly parabolic trend having flipped from Long-to-Short, with 2973-2844 as a support zone reasonably to be tested. The “late to the party” Moody’s downgrade of U.S. credit is nonetheless getting the safe havens the bid to begin the week; regardless, the Dollar Index (albeit -0.5% today) still hovers above the 100 handle. Support for the Spoo by its 10-day Market Profile initially shows at 5909, followed by 5864. And ’tis a very quiet week for the Econ Baro with just four metrics due, beginning today with April’s Leading (i.e. “lagging) Indicators, which by the “leading” Baro we already “know” ought be negative.

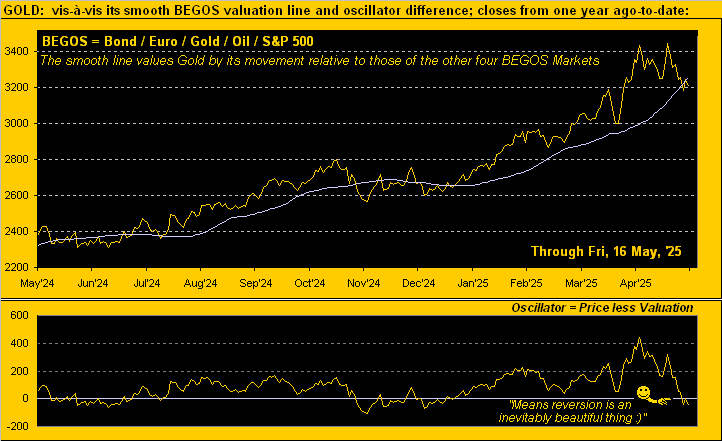

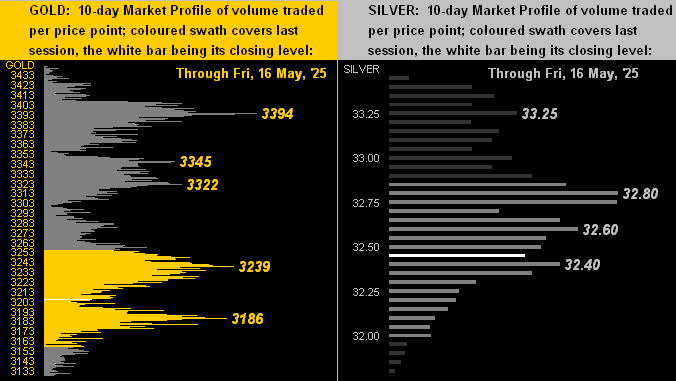

16 May 2025 – 08:39 Central Euro Time

Into week’s end we’ve at present the Bond, Euro and Swiss Franc above today’s Neutral Zones, whilst below same are both Gold and Silver; BEGOS Markets’ volatility is light. Of note by Market Ranges, Gold’s EDTR is 89 points (vs. 35 a year ago) whilst that for Silver is 0.88 points (not that far from 0.75 points a year ago); the Gold/Silver ratio is 99.0x (vs. the century-to-date average of 69.0x); more on it all in tomorrow’s 809th consecutive Saturday edition of The Gold Update. Meanwhile for the S&P 500, its “live” P/E (futs-adj’d) is 45.8x and the yield 1.313% vs. the U.S. T-Bill’s risk-free annualized yield of 4.258%. The Econ Baro looks to these incoming metrics in concluding the week: April’s Housing Starts/Permits and Ex/Im Prices, along with May’s UofM Sentiment Survey. Today wraps up Q1 Earnings Season for 2025, which for year-over-year quarterly improvement specific to S&P 500 constituents has essentially been average.

15 May 2025 – 08:25 Central Euro Time

Both the Euro and Swiss Franc are at present above today’s Neutral Zones, whilst below same are Gold, Silver, Oil and the Spoo; session volatility for the BEGOS Markets is pushing toward moderate. Gold confirmed a negative crossing of its smooth valuation line (see Market Values): this is of course a Short signal, albeit as we regularly quip “Shorting Gold is a bad idea”; still, a run from here (3137) down to 3000 wouldn’t seen untoward, price having established a plateau there back in February. Oil’s cac volume is rolling from June into that for July. And the Econ Baro is poised to take in 11 metrics today, amongst which are May’s NY State Empire Index, Philly Fed Index and NAHB Housing Index, along with April’s Retail Sales, PPI and IndProd/CapUtil, plus March’s Business Inventories.

14 May 2025 – 08:46 Central Euro Time

Both Gold and Silver are at present below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is quite light. Gold has nearly closed the long-running deviation above its smooth valuation line (see Market Values): in real-time, price is now just +10 points over the line, after having been as much (on a closing basis) as +440 points “high” back on 21 April; (and as previously noted, Gold’s weekly parabolic trend provisionally has flipped from Long-to-Short). Gold’s best Market Rhythm for pure swing consistency on a 10-test basis is currently the 6hr MACD; on a 24-test basis ’tis the 4hr parabolics. Nothing is due today for the Econ Baro ahead of a barrage featuring 16 incoming metrics from tomorrow into Friday; of note per yesterday’s CPI data, inflation’s pace increased during April.

13 May 2025 – 08:34 Central Euro Time

As posted yesterday on ‘X’, Gold’s weekly parabolic trend has provisionally flipped from Long-to-Short; barring Gold improbably making an All-Time High this week (above 3510), the new Short trend shall confirm upon Friday’s settle. At present, both Gold and Silver, along with the Euro and Swiss Franc are above their respective Neutral Zones for today, whilst below same is the Spoo; session volatility is light. Yesterday’s gap-up open for the S&P 500 was by points the largest in its 68-year history; the Index through the past 11 days is “textbook overbought” and the Spoo (in real-time) is +384 points above its smooth valuation line (see Market Values); the futs-adj’d “live” P/E for the Index is 44.3x. The Econ Baro looks to the first report of April’s inflation via the CPI.

12 May 2025 – 08:39 Central Euro Time

Copper is the sole BEGOS Market at present within its Neutral Zone for today; below same are the Bond, Euro, Swiss Franc, and Gold, whilst above same are Silver, Oil and the Spoo; volatility is mostly moderate. The Gold Update gives evidence to the yellow metal’s great rally potentially having run out of puff: purported progress of tariff resolution issues is drawing money from the safe havens into equities and the Dollar. Were the S&P 500 to open at this instant, the Spoo as adjusted for fair value places the Index +1.5%, (and the “live” P/E at 43.6x); the Spoo in real-time is +297 points above its smooth valuation line, see Market Values). The Econ Baro begins it busy week of 19 incoming metrics with April’s Treasury Budget due late in the session. And this is the final week of Q1 Earnings Season.

The Gold Update: No. 808 – (10 May 2025) – “Gold Regains Ground (albeit Stumbles Around…)”

In sum, its emotive hype aside, we still anticipate a bit lower Gold near-term; (indeed a most-valued colleague here suggested yesterday — over a delightful rosé — that 2400 is in the offing). That’s a bit out of range (-24%) from our perspective; however, Gold obviously has corrected by at least such percentage, notably during 2006-to-2008, certainly so post-2011’s All-Time High through 2015, as well as during 2019-to-2020. ‘Tis merely what the world’s major liquid financial markets on occasion do.

Next week also brings the calendar conclusion to Q1 Earnings Season, which to this point for the S&P 500 constituents is “average” for year-over-year quarterly improvement. ‘Course as you saw earlier in the Economic Barometer, the S&P 500’s price/earning ratio is an inane 43.0x. Thus earnings are on balance improving, but their overall level remains far too low to continue supporting price; (how’s that 1.359% annualized dividend yield workin’ out for ya?)

And specific to the Econ Baro, a huge load of 19 metrics are scheduled for the ensuing week. Shall the Baro live up to the Fed’s “solid pace” perception of the economy? As ever, we’ll mind the math…

…whilst you, rather than stumble around, mind — indeed mine — your Gold and Silver fine!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

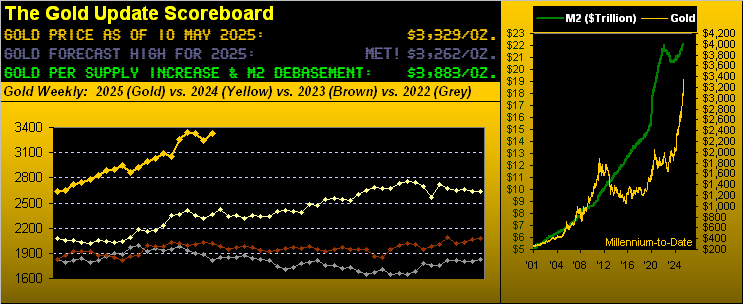

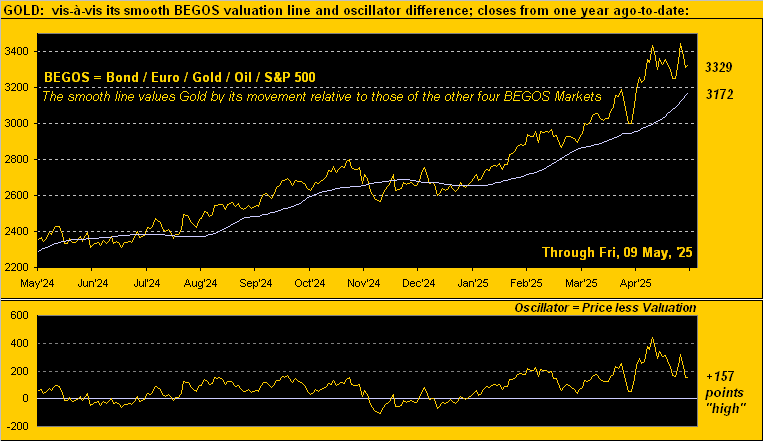

09 May 2025 – 08:42 Central Euro Time

Into week’s end we’ve at present Gold above its Neutral Zone for today and Copper below same; session volatility for the BEGOS Markets is pushing toward moderate. At Market Trends, our “Baby Blues” of linreg consistency are falling for all eight BEGOS components, albeit the only two currently with actual declining trends are the Swiss Franc and Oil. By Market Values for the five primary entities in real-time time: the Bond is 2^09 points “low” vis-à-vis its smooth valuation line, the Euro just 0.001 points “high”, Gold +155 points “high”, Oil -4.77 points “low” and the Spoo +220 points “high”. The S&P 500 is now textbook overbought through the past nine trading days. With one week still to run for Q1 Earnings Season, 427 S&P 500 constituents have reported of which 66% (282) have beaten their EPS of their like quarter a year ago. Nothing is due for the Econ Baro, it having concluded its week yesterday. Tomorrow brings our 808th consecutive Saturday edition of The Gold Update.

08 May 2025 – 08:20 Central Euro Time

The Swiss Franc is at present below its Neutral Zone for today, whilst above same are Silver, Copper, Oil and the Spoo; BEGOS Markets’ volatility is light-to-moderate. Amongst correlations of the five primary BEGOS components, that for Gold is notably positive with the Euro, however negatively so with the Spoo. Oil’s 12hr MACD embarked on a flip from Short-to-Long effective yesterday at12:00 (CET): year-to-date this has been a very respectable Market Rhythm, and in real-time by Market Values, Oil is -6.92 points below its smooth valuation line. The Econ Baro rounds out its week today, incoming metrics including March’s Wholesale Inventories and Q1’s initial read of Productivity and Unit Labor Costs.

07 May 2025 – 08:26 Central Euro Time

The Swiss Franc, Gold and Copper are all presently below today’s Neutral Zones, whilst above same are both Oil and the Spoo; session volatility for the BEGOS Markets to this hour continues as moderate. Looking at Market Rhythms at those currently displaying the best pure swing consistency: on a 10-test basis we’ve the Spoo’s 12hr Parabolics as well as its 4hr Moneyflow, plus the non-BEGOS Yen’s daily Price Oscillator; on a 24-test basis ’tis again the same for the Yen, along with Gold’s 2hr Parabolics. At Market Magnets, both the Euro and Silver yesterday confirmed positive crossings of price above Magnet, suggestive of higher levels near-term. Late in the session, the Econ Baro looks to March’s Consumer Credit, preceded an hour earlier by the week’s highlight of the FOMC’s Policy Statement, the consensus for which is no change in the Bank’s Funds rate.

06 May 2025 – 08:43 Central Euro Time

Both the Bond and Swiss Franc are at present below their Neutral Zones for today; above same are Gold, Silver and Oil, and BEGOS Markets’ volatility is yet again moderate to this point of the session. Gold has gained some +130 points since our querying (at 3247) about its great run being done: presently 3371, price is “only” -139 points below the 3510 All-Time High; by its Market Profile, Gold’s most dominant volume support price is 3324; and the yellow metal’s best Market Rhythm for pure swing consistency (10-test basis) is its 6hr MACD, in which hindsight vacuum $57k/cac has been generated since late February, and which swung from Short to Long yesterday at 12:00 (CET). The Econ Baro awaits March’s Trade Deficit.

05 May 2025 – 08:38 Central Euro Time

The Euro, Gold and Silver are all at present above today’s Neutral Zones; below same is the Spoo, and volatility for the BEGOS Markets is again moderate. The Gold Update queries as to the yellow metal’s great run being done (for now): price is within a day’s range of flipping the weekly parabolic trend from Long to Short (effective 3209); Gold’s EDTR (see Market Ranges) is 83 points.; and by Market Values (in real-time) Gold remains +164 points above its smooth valuation line. Q4 Earnings Season still has some two weeks to run: with 337 S&P 500 constituents having reported, 220 have bettered their bottom lines from Q1 a year ago; such 65% rate of improvement is a bit below the typical 66% pace. The Econ Baro begins a light week with April’s ISM(Apr) Index. And Wednesday brings the FOMC’s next policy statement for which consensus sees no change in.

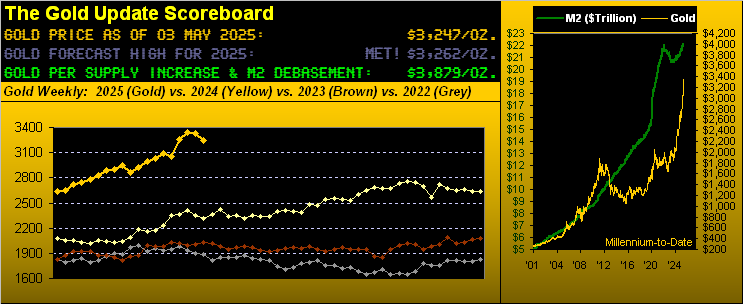

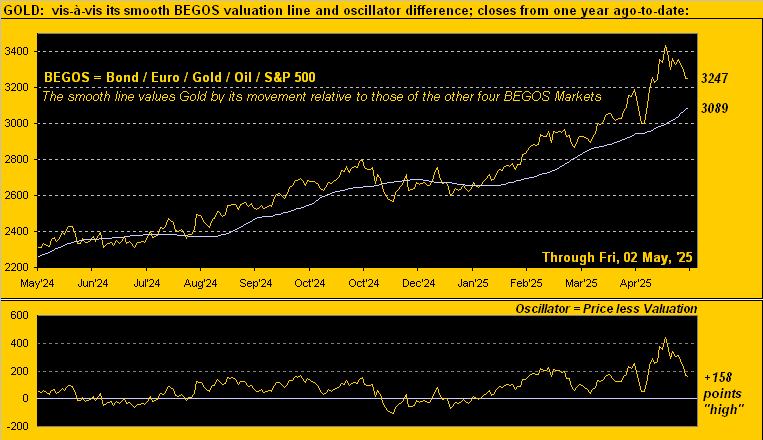

The Gold Update: No. 807 – (03 May 2025) – “Is Gold’s Great Run Finally Done (for now…)?”

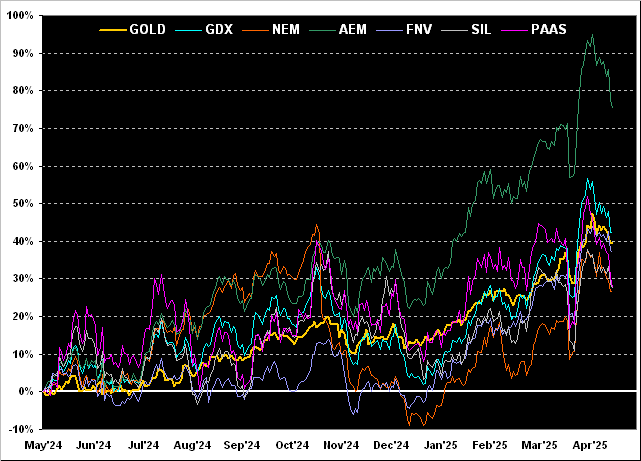

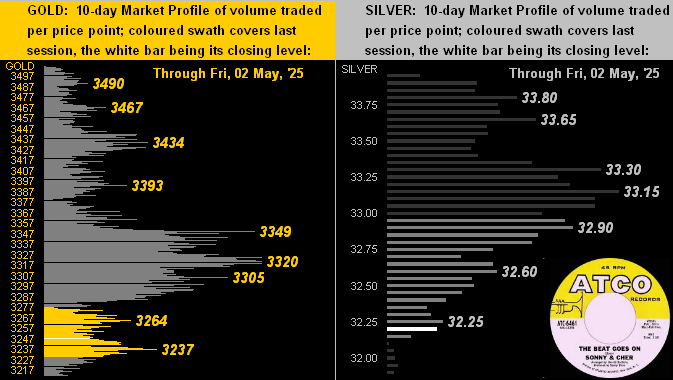

Further for the precious metals, here next are the 10-day Market Profliles for Gold on the left and Silver on the right. With present prices for the yellow and white metals all but at the bottom of their respective Profiles, both have taken a bit of a beat-down. Either way, as crooned the darling duo Sonny & Cher back in ’67, ![]() “The beat goes on…”

“The beat goes on…”![]() :

:

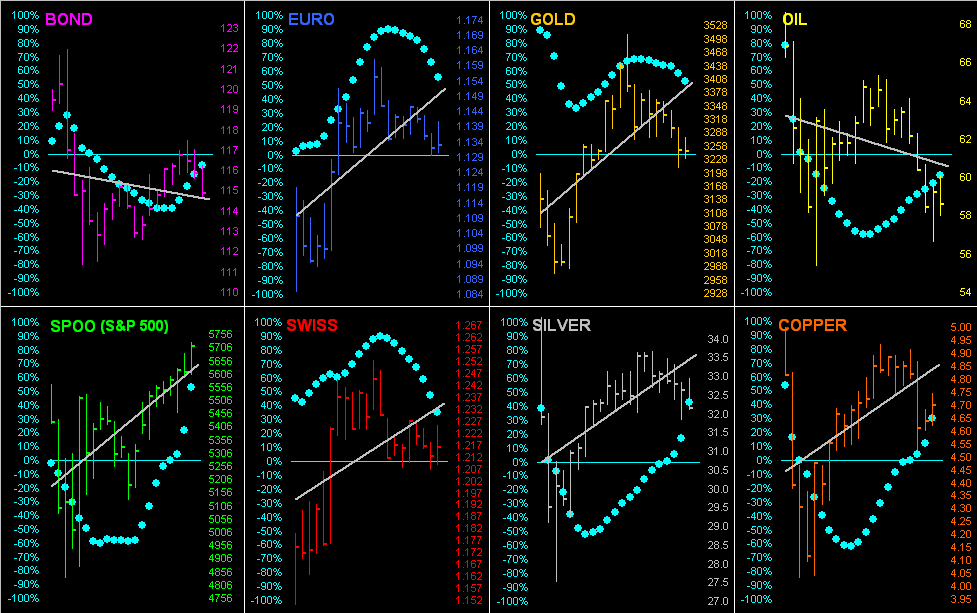

Regardless, ‘twould appear Wall Street sees inflation as having ceased, and per CNBC, “…stocks claw back tariff losses…” you see. Thus: let the Fed cut sans impunity, if you please! What do the BEGOS Markets see? Let’s go ’round the horn for all eight BEGOS components across their past 21 trading days (one month) with their respective grey trendlines and our famous “Baby Blues” of day-to-day regression trend consistency. And as the Dollar returns to getting a bit of a bid, note the blue dots rolling over to the downside for the Euro, Swiss Franc and Gold. All together now: ![]() “Follow the Blues instead of the news, else lose yer shoes”

“Follow the Blues instead of the news, else lose yer shoes”![]() :

:

“But mmb, in B-school they said stocks are a hedge against inflation, just like gold, eh?“

True enough, Squire. However, we were also taught (to yet again reprise Jerome B. Cohen): “…in bull markets the average [price/earnings] level would be about 15 to 18 times earnings…” Today, ridiculously beyond rationality, the “live” (i.e. trailing 12-months) p/e for the S&P settled the week yesterday at 43.9x(!) In other words: with stock prices unsupported by earnings, GDP shrinking, the economy showing signs of stagflation, and a liquid money supply that can only cover 44% of the “money” currently invested in the S&P 500, ’tis not the time to say to stocks “Buy-Buy!”, but rather “Bye-Bye!”

As for the slipping precious metals, think “Dip-Buy!”

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

02 May 2025 – 08:38 Central Euro Time

Save for the Bond which at present is inside its Neutral Zone for today, the seven other BEGOS Markets are above same; session volatility is moderate. Going ’round the Market Values horn in real-time for the five primary BEGOS components: the Bond shows as essentially on its smooth valuation line, the Euro as +0.0393 points “high”, Gold as +180 points “high”, Oil as -6.56 points “low” and the Spoo as +160 points “high”. The S&P 500 itself week-to-date remains “textbook overbought” and the futs-adj’d “live” p/e is 43.0x; on the S&P’s monthly chart, its MACD confirmed a negative crossing as May got underway: the last such negative crossover occurred in April 2022 leading to a more than -1,000 points (-14.5%) decline into November. ‘Tis April’s Payrolls day for the Econ Baro, along with March’s Factory Orders.

01 May 2025 – 08:42 Central Euro Time

The Euro, Gold and Silver are all at present below their respective Neutral Zones for today; above same is Copper, and session volatility for the BEGOS Markets is light-to-moderate. Indeed, the Euro’s “Baby Blues” (see Market Trends) of trend consistency confirmed crossing below the +80%; we’re anticipating the low 1.12s from here, perhaps even the upper 1.11s as the Dollar is showing a bit of resilience with a positive MACD swing on the Buck’s daily chart. Gold continues to work toward closing the gap down to its smooth valuation line (see Market Values), price in real-time however still +167 points “high”. For correlation amongst the five primary BEGOS components, the current best is positive between Gold and the Euro. And included in today’s incoming metrics for the Econ Baro are April’s ISM(Mfg) Index and March’s Construction Spending.