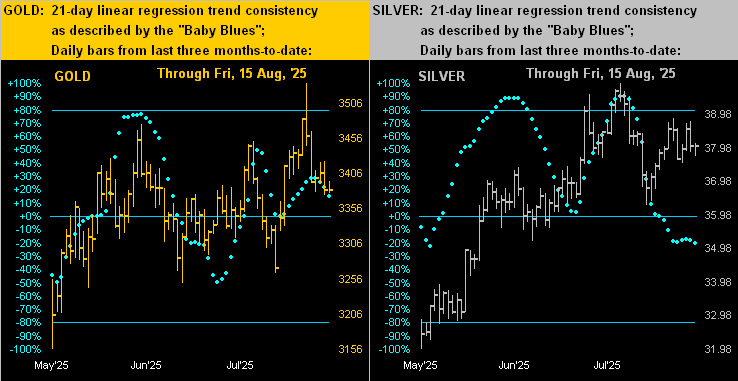

In commencing the week we’ve at present both the Bond and Swiss Franc below today’s Neutral Zones; the rest of the BEGOS Markets are within same, and session volatility is light. The Gold Update cites the yellow metal having just recorded its narrowest trading week of the year-to-date, even in the euphoria of an “assumed” FedFunds cut come 17 September, our stance to which is far more skeptical as inflation seemingly is increasing: next Friday’s PCE report for July may instill discouragement for the S&P which rallied last week to within two points (6479) of the all-time high (6481). ‘Tis a fairly busy week for the Econ Baro, beginning today with July’s New Home Sales.

Mark

Mark

The Gold Update: No. 823 – (23 August 2025) – “Gold Gains a Little; Dollar Drools Spittle; Powell Non-Committal”

To wrap, ’tis the Stack.

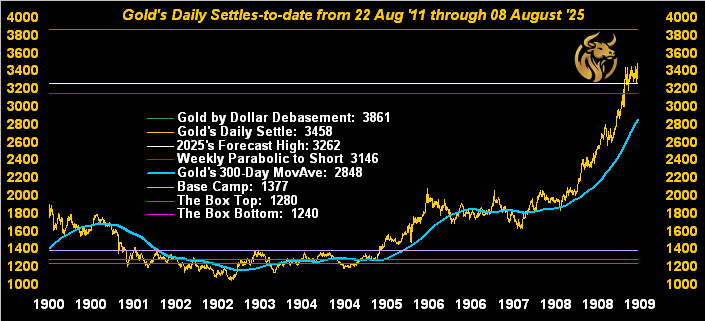

The Gold Stack (continuous contract pricing):

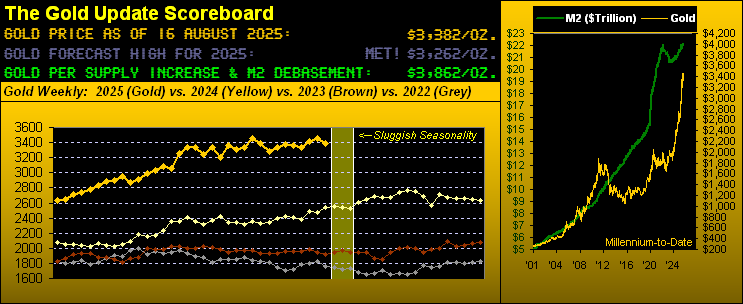

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3864

Gold’s All-Time Intra-Day High: 3534 (08 August 2025)

2025’s High: 3534 (08 August 2025)

Gold’s All-Time Closing High: 3483 (07 August 2025)

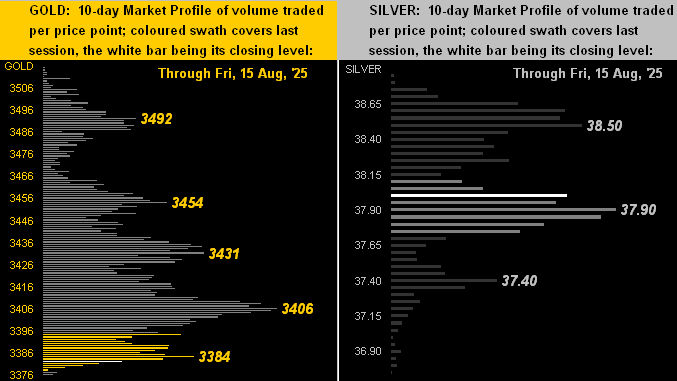

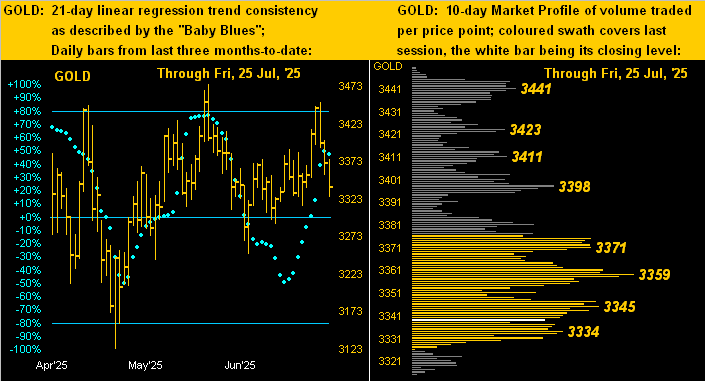

Trading Resistance: by the Profile, none of note

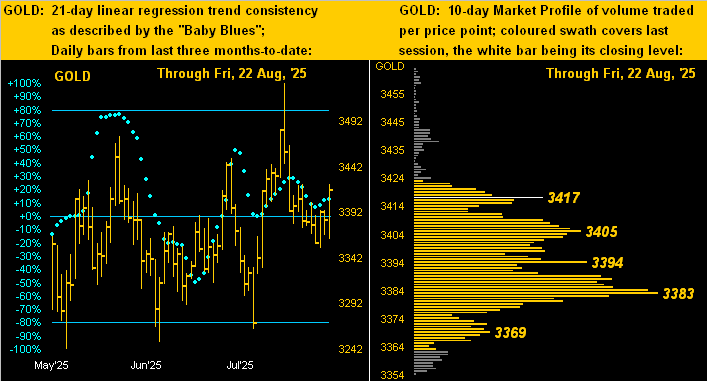

Gold Currently: 3417, (expected daily trading range [“EDTR”]: 44 points)

Trading Support: by the Profile 3417 / 3405 / 3394 / 3383 / 3369

10-Session “volume-weighted” average price magnet: 3394

10-Session directional range: down to to 3354 (from 3465) = -111 points or -3.2%

The Weekly Parabolic Price to flip Short: 3176

The 300-Day Moving Average: 2883 and rising

2025’s Low: 2625 (06 January)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Next we’ve Summer’s final snoozer week for August … but for the Econ Baro robust? Or a just a bust? 12 incoming metrics are scheduled including as aforementioned on Friday “The Big One”: July’s PCE. What shall it be? One can wait and see…

Or garner more Gold if you please!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

22 August 2025 – 08:28 Central Euro Time

Presently we find the Euro along with Gold below their respective Neutral Zones for today, the Dollar continuing to get a bid throughout the week; the rest of the BEGOS Markets are within their Neutral Zones, and volatility — not surprisingly ahead of the FedChair’s address (14:00 ET) — is quite light. Equities may not take kindly to lack of affirmation for a FedFunds rate cut; clearly July’s PPI spike is an inflationary concern upon which we’ll again address in tomorrow’s 823rd consecutive Saturday edition of The Gold Update. Should the S&P 500 “let go” over the ensuing trading days, there is a structural support “island” spanning from 6059 down to 5767, the mid-point of which is 5913; instead should the FedChair put a rate cut on the table, we’d expect the S&P to resume rallying. The Econ Baro concluded its week yesterday, as posted on its page.

21 August 2025 – 08:33 Central Euro Time

Both the Swiss Franc and Gold are presently below today’s Neutral Zones; the other BEGOS Markets are within same, and volatility is very light. Despite the S&P 500 having made “lower lows” for three days in a row, the Index nonetheless remains technically “textbook overbought”, and obviously by any fundamental yardstick, dangerously overvalued, the fut’s-adj “live” P/E now 44.8x. Do mind an eye on the S&P MoneyFlow page: the outflow in recent days has been notably larger than the decline in the Index itself, the cumulative regressed differential for the past five sessions being -282 more flow points than actual S&P points lost; again, this is a valued leading indicator for lower levels ahead. Our best correlation amongst the five primary BEGOS components is currently positive between the Euro and Gold. And the Econ Baro concludes its own week today with metrics including August’s Philly Fed Index, plus July’s Existing Home Sales and Leading (i.e. “lagging”) Indicators.

20 August 2025 – 08:07 Central Euro Time

Presently, only the Spoo is outside (below) its Neutral Range for today; volatility for the BEGOS Markets to this time of day remains lights. Ahead of the “Friday Fed”, the S&P 500 is seemingly a bit worried of a rate cut not being soon on the table, unless July’s PPI spike was a “one-off”; the Spoo (6417) has found its Market Profile support area ’round 6414 basically holding; should 6400 break, the next volume-supportive area is 6372-6368. By our Market Rhythms for pure swing consistency, the best on a 10-test basis are currently the Bond’s 30mn Parabolics, the Swiss Franc’s daily Price Oscillator and Silver’s 4hr MACD, whilst on a 24-test basis we’ve Silver’s 1hr Price Oscillator, the Bond’s 15mn MACD and Oil’s 8hr MACD. Nothing is due for the Econ Baro; then late in the session we’ve the FOMC’s Minutes from its 29-30 July meeting.

19 August 2025 – 08:30 Central Euro Time

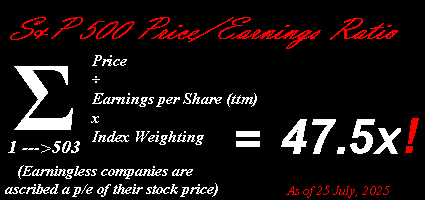

Silver is presently the sole BEGOS Market outside (below) its Neutral Zone for today; session volatility is again light, as has become the overall state of the BEGOS components throughout the trading day: first they’ve been on hold for UKR at White House, then for UKR allies at White House, and next at week’s-end for FedChair at Jackson Hole; thus again, the Dog Days of August are in full swing. For the Spoo (currently 6459) by its Market Profile, the volume-dominant overhead resistor is 6468, whereas it appears as “nothing but air” from here down to 6414, were some selling to ensue, albeit we don’t see much directional impetus either way until the Friday’s Fed is out of the way. Still, the S&P 500 remains beyond extremely overvalued, the “live” (fut’s adj’d) P/E 46.2x at this moment. July’s Housing Starts/Permits come due for the Econ Baro.

18 August 2025 – 08:31 Central Euro Time

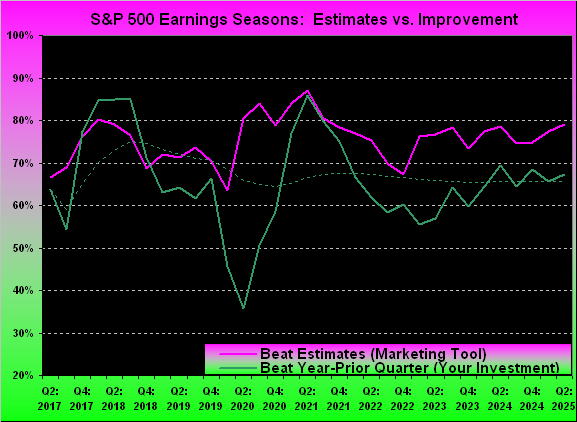

The week begins with, at present, all eight BEGOS Markets inside their respective Neutral Zones for today; session volatility is light. The Gold Update speaks to its typical “seasonal sluggishness” as we now laze through the Dog Days of August; both the weekly and daily parabolic trends for Gold remain Long, however the latter has little downside room with which to work: currently 3393, the daily “flip-to-Short” price for today is 3365, well within range given’s Gold’s EDTR (see Market Ranges) of 48 points. Q2 Earnings Seasons has concluded: for the S&P 500, whilst 79% of the constituents beat estimates, 67% actually improved from Q2 a year ago; that’s a pip above the average of 66% generally improving from 2017-to-date. For the Econ Baro ’tis a fairly muted week, starting today with August’s NAHB Housing Index.

The Gold Update: No. 822 – (16 August 2025) – “Gold Sensing Seasonal Sluggishness”

To wrap, we’ve already reviewed inflation’s “Whopper of the Week“. Let us thus close with our favourite “Headline of the Week“, courtesy of Bloomy just last evening. Ready?

- “Wall Street Wrestles With Hedging Conundrum as Valuations Swell”.

Cue a pet quip of ours: “They’re just figuring this out now?” ‘Tis to laugh, but let’s try to help those floundering in Manhattan’s financial canyons. The S&P 500 settled yesterday at a near-record high 6450 with the aforementioned p/e ratio of 46.3x and paltry yield of 1.201%. What that means for you WestPalmBeachers down there is in purchasing the S&P right now, you are paying $46.30 for something that earns $1, (plus some dividend change for your usage of gas station toilets), along with the thrill of your $46.30 being halved upon the next -50% market “correction”; (recall we’ve already had two such “corrections” thus far this century). Instead, one can opt for the U.S. Treasury’s 3-month Bill currently yielding an annualized 4.112% and return of the Bill’s face value. So what’s the conundrum, eh?

“Well, you’d have to trust the U.S. Treasury’s solvency, mmb…”

Good point, Squire. So alternatively…

Got yours?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

15 August 2025 – 08:20 Central Euro Time

Both the Euro and Spoo are at present above today’s Neutral Zones; none of the other BEGOS Markets are below same, and volatility is again light. The Spoo has made another all-time high this morning such that should the current area hold, ‘twould pull the S&P 500 up to a record high at its open. The Bond’s “Baby Blues” (see Market Trends) of linreg consistency confirmed closing below their key +80% axis: we thus sense a run from here (114^31) down at least into the very low 114s if not the mid-113s: July’s very inflationary PPI ought make it clear for no rate cut perhaps through the balance of this year. By correlations amongst the five primary BEGOS components, the best currently is negative between the Euro and Oil, the latter for which cac volume is rolling from September into that for October. 9 metrics come into the Econ Baro today, notably including August’s NY State Empire Index and the UofM Sentiment Survey, July’s Retail Sales, Ex/Im Prices and IndProd/CapUtil, plus June’s Business Inventories. Too, ’tis the final day of Q2 Earnings Season.

14 August 2025 – 08:24 Central Euro Time

At present, all eight BEGOS Markets are within their respective Neutral Zones for today, and session volatility is light. Yesterday, further all-time highs were recorded by both the Spoo (6503) and S&P 500 (6480). By Market Rhythms (10-test basis) our top five for pure swing consistency currently Silver’s 4hr MACD, 4hr Parabolics and 1hr Price Oscillator, plus the Euro’s 2hr Price Oscillator and 30mn Parabolics. Following Gold’s Swiss tariff “Spike n’ Plunge” last Friday-Monday, trade of the yellow metal has been extremely subdued in terms of daily range: Gold’s EDTR (see Market ranges) for today is 51 points; however, Tuesday’s actual range was only 32 points and yesterday’s just 30 points. Incoming metrics for the Econ Baro today include wholesale inflation for July via the PPI.

13 August 2025 – 08:08 Central Euro Time

All-time highs have been recorded for both the Spoo (6475) and S&P 500 (6447), the latter’s “live” futs-adj’d P/E now 47.1x. Presently we’ve the same BEGOS Markets’ status as was the case ’round this time yesterday: Silver is above today’s Neutral Zone, whilst the other seven components are within same, and volatility again is quite light, (again with Silver posting the largest EDTR [see Market Ranges] tracing of 52% to this point, the average for the whole bunch being but 27%). Looking at Market Values for the five primary BEGOS entities in real-time: the Bond is +1^07 points “high” above its smooth valuation line, the Euro basically in sync with same, Gold +47 points “high” despite its recent pullback (both the daily and weekly parabolic trends still being Long), Oil +4.30 points “low” and the Spoo +159 points “high”. Nothing is due today for the Econ Baro ahead of 12 incoming metrics Thursday through Friday; and three days remain in Q2 Earnings Season.

12 August 2025 – 08:17 Central Euro Time

Silver is the sole BEGOS Market presently outside (above) its Neutral Zone for today; session volatility is quite light: the largest EDTR (see Market Ranges) tracing to this point indeed being that for Silver at 58%, the average for all the BEGOS components thus far just 29%. At Market Trends, the Bond’s “Baby Blues” have in real-time just kinked lower, albeit are still above the key +80% axis: a break below that level would likely bring still lower prices; too, the Spoo’s “Baby Blues” continue to weaken despite the on balance positive price track since last week’s low (6240); by Market Values, the Spoo in real-time at 6402 is +103 points above its smooth valuation line. And today the Econ Baro gets its own week underway with July’s retail inflation via the CPI, plus late in the session comes the Treasury Budget, (which for June was a surplus, but is expected for July to have returned to deficit status).

11 August 2025 – 08:18 Central Euro Time

At present we’ve both the Euro and Swiss Franc above today’s Neutral Zones, whilst below same are both Gold and Silver; BEGOS Markets’ volatility is light. The Gold Update highlights the weekly parabolic Long trend having now been joined by the daily parabolic Long trend; however Friday’s Swiss tariff price spike pierced Gold’s upper BollBand, such that some natural price retraction (as already we’ve seen) is natural prior to price moving on toward its next All-Time High, which by the December contract would be above 3586; and by Market Trends, Gold’s “Baby Blues” of linreg trend consistency are higher still in real-time. The Econ Baro, although quiet today, awaits 15 metrics as the week unfolds. And Q2 Earnings Season moves into its final week.

The Gold Update: No. 821 – (09 August 2025) – “Double Shot of that Golden Love”

Back in ’63, Dick Holler & the Holidays crooned a tune (penned by Don Smith and Cyril Vetter) entitled ![]() “Double Shot (Of My Baby’s Love)”

“Double Shot (Of My Baby’s Love)”![]() . The catchy piece has since been covered ‘twould seem some 5,000 times, similar to Gold’s being recognized as real money for some 5,000 years. Be that exaggerative or otherwise, we’ve just been gifted a

. The catchy piece has since been covered ‘twould seem some 5,000 times, similar to Gold’s being recognized as real money for some 5,000 years. Be that exaggerative or otherwise, we’ve just been gifted a ![]() “Double Shot of that Golden Love”

“Double Shot of that Golden Love”![]() as follows:

as follows:

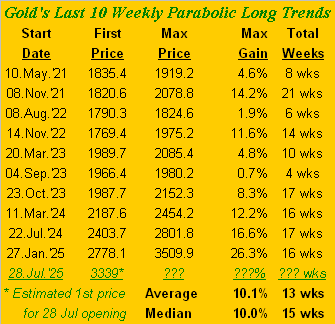

- Shot One: as you regular readers already know, just back on 25 July, Gold’s weekly parabolic trend formally flipped from Short-to-Long;

- Shot Two: price’s settle this past Thursday (3483) in turn confirmed Gold’s daily parabolic trend also flipping to Long.

“I’m feelin’ the love there, mmb!”

As well we ought, Squire. Toward settling yesterday (Friday) at 3458, Gold’s “continuous contract” en route made an All-Time High at 3534, albeit that needs a bit of qualification, by which again we bullet-point three types:

- Spot Gold: is the de facto hard-money resource, the official All-Time High for which is 3500 as traded this past 22 April;

- Continuous Gold: is the chaining together of futures contracts (Gold’s most liquid trading form) such as to present (per our weekly bars graphic) a continuous history of the futures price, its new All-Time High just achieved as noted yesterday at 3534;

- December Gold: is the current so-called “front-month” futures contract, its All-Time High too achieved back on 22 April at 3586 (when June was then the “front-month”, with its 3510 high).

Regardless of which All-Time High you prefer to apply, what we now see as key is December’s 3586 being relatively short-lived (no pun) given the timing of this fresh “Double Shot of that Golden Love”, should price evolve similarly as it has by both the various weekly and daily parabolic Long trends across the past 10 years.

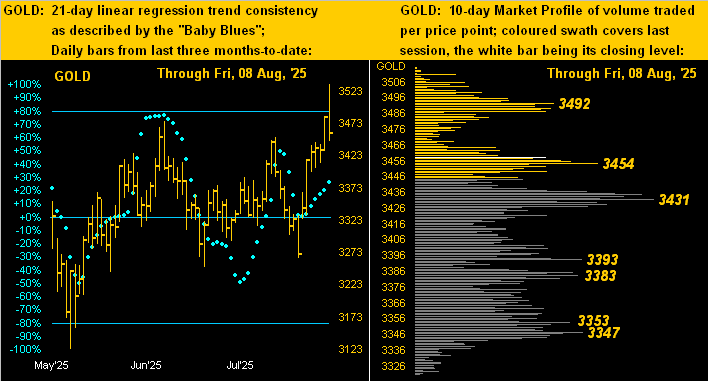

Recall from two missives ago our historical table of Gold’s prior 10 weekly parabolic Long trends having produced average upside price follow-through of +10%, which applied to this stint would find Gold well up into the 3600s. And per our Market Rhythms’ analyses, Gold’s best study for pure swing consistency is its daily parabolics, presently ranked (on a 24-test basis) at No.1 of the 405 rhythms tested nightly.

All of which in an encapsulated Golden nugget means we anticipate still higher highs through these ensuing weeks.

That stated, even the best markets’ analyses are no holy grail, provably as signals can — and do — fail. To wit, beware of John Bollinger and his Band(s). The following graphic depicts December Gold by the day from this past April-to-date. The two encircled rightmost wee blues dots are, of course, the commencement of this new daily parabolic Long trend for Gold. However, we’ve also applied the two violet Bollinger Bands, the upper through which — at Friday’s open — price penetrated (thank you StateSide tariff on Swiss Gold … see our close). Therein, note price’s imminent decline per the white lines after such prior upside penetrations:

As teased, let’s close with the high-drama event of the week: the evoking of “Tariff Terror!” on Gold bars of both one kilogram and 100 ounces imported from Switzerland into the U.S. And with the utmost respect for our beloved Swiss family to the north of us, we had to chuckle. We don’t know how many folks StateSide regularly engage in buying 1kg bars of Swiss Gold (currently $122k/bar + 39% tariff = $170k/bar), let alone nearly triple that for a 100/oz. bar. Regardless, our mobile phone here lit up with chaotic panic over the 39% imposition, (for which ’tis now said may be misinterpreted).

‘Course, unlike today’s FinMedia, the late great Paul Harvey would have additionally reported to us “the rest of the story”. To be sure, after having settled Thursday at 3482, four minutes into Friday’s session found Gold having spiked +1.5% to the aforementioned new “continuous contract” All-Time High of 3534. But “left out of the story” was that 31 minutes into the session, Gold was back down to where it had ended Thursday. Further, the Swiss Franc was completely docile over it all, trading just 54% of its EDTR (“expected daily trading range”) on Friday. As for Gold, here is Friday’s first hour of trading by the minute, courtesy of the “If You Blinked, You Missed It Dept.”:

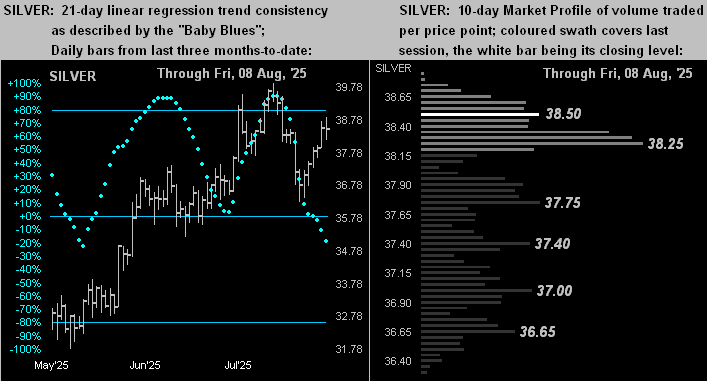

Either way, our double-shot bottom line is: do not miss out in owning Gold, and Silver too with $40/oz. in view!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

08 August 2025 – 08:25 Central Euro Time

As expected, Gold confirmed its daily Parabolics flipping to Long per yesterday’s close, following which at this morning’s open price briefly swiftly spiked from 3488 to 3534, which by the “continuous contract” is a new All-Time High; more of course in tomorrow’s 821st consecutive Saturday edition of The Gold Update. For the present, Gold is above its Neutral Zone for today, whilst below same is the Euro; session volatility for the BEGOS Markets is pushing toward moderate, aided by Gold having already traced 111% of its EDTR (see Market Ranges). Yesterday’s MoneyFlow into the S&P 500 was +1.5% vs. the actual Index’s change of just +0.1%: this has been a hallmark of Q2 Earnings Season wherein “estimates” quite regularly are being beaten, even as actual earnings improvement has been but average; there remains one more week to run for Q2 results. As noted yesterday, the Econ Baro already has concluded its week., which on balance was negative.

07 August 2025 – 08:28 Central Euro Time

Gold, Silver and Oil all are at present above today’s Neutral Zones; none of the other BEGOS Markets are below same, and session volatility is light. For the Precious Metals, Gold (3449) is above its most volume-dominant Market Profile supporter (3431), whilst Silver (38.25) is just below its most volume-dominant Market Profile resistor (38.30); on a broad-term basis, the white metal remains attractively priced vis-à-vis the yellow metal give the Gold/Silver ratio now 90.1x; on a 10-test basis for pure Market Rhythm swing consistency the best for Gold currently is its 15mn Price Oscillator, whereas for Silver ’tis her 4hr MACD. Our best overall Market Rhythm on a 10-test basis is the Swiss Franc’s 6hr Moneyflow, and on a 24-test basis ’tis Gold’s daily Parabolics which likely confirm a flip from Short-to-Long at tonight’s settle. The Econ Baro concludes its week today (Thursday) with five incoming metrics, notably including Q2’s Productivity and Unit Labor Costs along with Wholesale Inventories for June; then late in the session comes that month’s Consumer Credit.

06 August 2025 – 08:28 Central Euro Time

We’ve presently both Oil and the Spoo above today’s Neutral Zones; the rest of the BEGOS Markets are within same, and volatility is very light, the average EDTR (see Market Ranges) tracing to this point just 26%. At Market Trends, 3 of the 8 BEGOS Components are in 21-day linreg up trends: the Bond and Gold with reinforcement as their “Baby Blues” of trend consistency too are rising, along with the Spoo, albeit there the “Baby Blues” continue to drop; the other five markets are thus in downtrends. As to the Bond’s rally of late, by both Market Values and Market Magnets, price is better than 1.5 points above those measures, although that is not what we’d consider an “extreme” deviation; but the Bond has been getting the bid given its far better yield over the S&P 500 which price-wise we consider to view as close to the edge. Nothing is due today for the Econ Baro; and this “average” (by improvement) Q2 Earnings Season has another 8 trading days to run.

05 August 2025 – 08:18 Central Euro Time

Both the Euro and Swiss Franc are presently below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility is light. EDTR (see Market Ranges) tracings to this moment range from 47% for the Swiss Franc down to just 10% for Copper. Amongst the five primary BEGOS components, the best correlation currently is positive between the Bond and Gold: per their Market Rhythms on a 10-test basis, the Bond’s best for pure swing consistency is presently the 12hr MACD, whilst for Gold ’tis the 30mn MACD; and by Market Values, both the Bond and Gold are above their smooth valuation lines. The Econ Baro looks to July’s ISM(Svc) Index, plus June’s Trade Deficit.

04 August 2025 – 08:20 Central Euro Time

The Bond, Euro and Swiss Franc are presently below today’s Neutral Zones, whilst above same is the Spoo; session volatility for the BEGOS Markets is moderate. The Gold Update reviews the recent turbulence within The Metals Triumvirate, plus assesses if the S&P 500 has at long last reached a significant turning point to substantively lower levels, albeit as noted the Spoo is rising thus far today even as its “Baby Blues” of trend consistency are in full plunge (see Market Trends); currently 6291, the Spoo’s Market Profile support is 6264 with major overhead volume-dominant resistors at 6345, 6371 and 6406. Two weeks remain in Q2 Earnings Season with year-over-year quarterly improvement just a tad below average. And ’tis a relatively quiet week for the Econ Baro, beginning today with June’s Factory Orders.

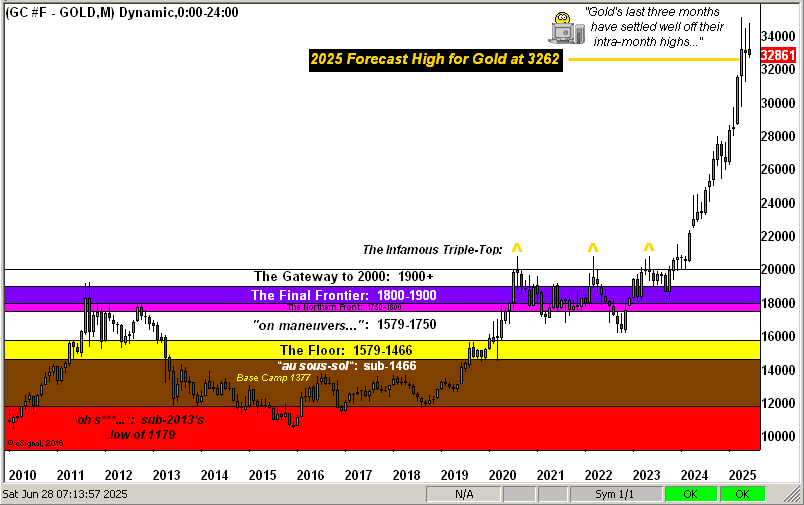

The Gold Update: No. 820 – (02 August 2025) – “Turbulence in The Metals Triumvirate”

Naturally it being month-end, plus one trading day, here is the monthly Gold Structure for the past 15 years. The rightmost green bar is merely Friday (yesterday) alone, it having been 01 August. ‘Tis been quite the run for Gold across this time frame, ‘specially after only just two-to-four years ago when Gold’s infamous Triple-Top pricing was ![]() “Dancing on the ceiling…”

“Dancing on the ceiling…”![]() , –[Lionel Richie, ’86]:

, –[Lionel Richie, ’86]:

Metals turbulence notwithstanding, next week is a bit more benign for the Econ Baro with just eight metrics due, including improved (purportedly) Productivity for Q2. Are you productively maintaining a sound supply of Gold?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

01 August 2025 – 08:22 Central Euro Time

The Swiss Franc is the sole BEGOS Market at present outside (below) its Neutral Zone for today; session volatility is light. Although the S&P 500 recorded a third consecutive modest down day yesterday, per our page of the Index’s MoneyFlow, such measure remains positively robust, despite our overwhelming sense of a significant correction being nigh. In real-time at Market Trends, the Spoo’s “Baby Blues” have again broken below the key +80% axis: recall their last so doing (18-22 July) was an unusual “failed signal” for this otherwise reliable leading indicator of near-term market direction. As for correlation within the five primary BEGOS components, our best at present is negative between the Euro and Oil. The Econ Baro concludes its busy week with July’s Payrolls data, ISM Index and revised UofM Sentiment Survey, plus June’s Construction Spending. And with essentially two weeks remaining in Q2 Earnings Season, S&P 500 year-over-year quarterly improvement is now up to 66%, which is an average rate, the fly in the ointment of course being the harrowingly-high “live” P/E at a futs-adj’d 47.5x.

31 July 2025 – 08:26 Central Euro Time

Copper is further falling this morning: netting a loss yesterday of -18.3% following tariff implications, the red metal is now down an additional -5.1%, obviously below its Neutral Zone for today, as is Oil; above same are the Bond, Euro, Swiss Franc, Gold and the Spoo; BEGOS Markets’ volatility is moderate. Going ’round the Market Values horn of the five primary BEGOS components in real-time: we’ve the Bond basically in sync with its smooth valuation line, the Euro as -0.026 points “low”, Gold as -13 points “low”, Oil as +1.84 points “high”, and the Spoo as +258 points “high”; the S&P 500 itself is now 26 consecutive days “textbook overbought” and the futs-adj’d P/E now a whopping 48.0x. ‘Tis a key inflation day for the Econ Baro featuring for June “Fed-Favoured” PCE data, plus Personal Income/Spending; too due is July’s Chi PMI and Q2’s Employment Cost Index.

30 July 2025 – 08:29 Central Euro Time

As was the case ’round this hour yesterday, all eight BEGOS Markets are presently within today’s Neutral Zones; volatility is light. By Market Trends, yesterday both Silver and Copper confirmed their “Baby Blues” of trend consistency having fallen below the key +80% such that we anticipate lower prices near-term. Per Market Rhythms for pure swing consistency, our best on a 10-test basis currently is the Swiss Franc’s 6hr Moneyflow, whilst on a 24-test basis ’tis Gold’s daily Parabolics. The S&P 500 despite yesterday’s mild down session nonetheless recorded a fourth consecutive day as being “extremely textbook overbought”: with so much on the table through the balance of this week, we expect the Index to crack at any time. And today, the Econ Baro looks to July’s ADP Employment data, June’s Pending Home Sales, plus the first peek at Q2 GDP, which — give the steep decline in the Baro notably for April and May data — shan’t be up to the +2.5% consensus expectation. Then come 18:00 GMT is the FOMC’s Policy Statement within which there shan’t be a FedFunds’ rate change.

29 July 2025 – 08:27 Central Euro Time

All eight BEGOS Markets are at present within their respective Neutral Zones for today, and session volatility is very light with 18 Econ Baro metrics plus the FOMC in the balance of the week. Gold’s cac volume is rolling from August into that for December with +57 points of fresh premium. The S&P 500 is now “textbook overbought” through its last 24 sessions, indeed “extremely” so for the past 3: we sense the Index is very close to a significant correction, especially with all that’s on the able as noted over these next four days; the futs-adj’d “live” P/E of the S&P is currently 47.7x and the yield 1.204% vs. the 3-month T-Bill’s annualized 4.235%. The Econ Baro gets its data parade rolling today with July’s Consumer Confidence.

28 July 2025 – 08:41 Central Euro Time

Presently the Euro and Swiss Franc are below today’s Neural Zones, whilst above same are both Oil and the Spoo; session volatility for the BEGOS Markets is firmly moderate. The Spoo gapped up some +21 points at the open on tariff resolution: that puts the “live” futs-adj’d P/E at of the S&P at now 47.7x. The Gold Update confirms price’s weekly parabolic trend as having flipped from Short-to-Long, the opening price of the new stint effective this morning’s opening trade at 3321; acknowledged therein is Gold’s negative MACD stance also on the weekly timeframe, but that its performance has been a net failure per the last five signals, whereas the last five parabolic Long trends have been a net success. ‘Tis a very busy week for the Econ Baro with 18 metrics due, however none for this session.

The Gold Update: No. 819 – (26 July 2025) – “Gold Ends Its Short Spell; But Then Falls Pell-Mell”

And to be sure, there’s a lot on the mid-summer table to affect the price of Gold. Most imminently, next Wednesday (30 July) brings The Big Double-Whammy of StateSide Q2 Gross Domestic Product followed by the Federal Open Market Committee’s Policy Statement. Then two days hence brings 01 August and the introduction of more “Trump Tariffs!”

Too, there’s this from the “Oh By The Way Dept.” ‘Tis time for the U.S. Treasury to spritely come up with $7T to pay its noble holders of maturing Bills, Notes and Bonds. According to “AI” (“Assembled Inaccuracy”), as of this year’s Q1, operating cash amounted to about $406B, which combined with other monetary assets totaled a tad over $1T for 2024. Thus by your six-year-old’s first grade arithmetic, the Treasury is about -$6T short of its looming funding requirements.

So who or what is going to buy all this requisite new debt? Here’s a thought: remember that (as we herein mathematically constructed) “all” $7T of the COVID monetary “creation” essentially found its way into the S&P 500. So, why not have the Treasury thus promote a “group sell” of $7T in stocks with the proceeds moving into debt at its currently attractive rates? ‘Tis so easy, a WestPalmBeacher can do it.

“But mmb, that might crash the stock market…”

The stock market, Squire, is so overdue for a harrowing crash, be it driven fundamentally, technically and/or quantitatively, a “group sell” to save the U.S. Treasury would be the perfect crash catalyst.

But with respect to Gold (and barring such selling of stocks), should the ensuing Treasury auctions be feeble, ‘twould fall to the Fed being forced to make that next BIG accounting entry to buy up the difference. And Gold, in turn, would go upside gonzo nuts (again, a technical term).

Speaking of stocks, we’ve run out of ways to indeed express (purposeful repeat) how we’ve run out of ways to describe the LooneyTunes overvaluation of the S&P 500. During recent years, we’ve herein detailed in-depth (using what is today an unknown science called “math”) sensible scenarios for the “Look Ma! No Earnings!” crash and the “Look Ma! No Money!” crash. Now let’s add to those the “That’s All, Folks!” crash, wherein upon it all going wrong, the market doesn’t so much crash as instead ’tis just closed, (rather akin to the “Look Ma! No Money!” crash). Then again the Fed can create the difference and ’tis more upside gonzo nuts for Gold.

As to the current state of the S&P, ’tis now 23 consecutive trading days “textbook overbought”, as well as having arrived at our “extremely overbought” classification with a sub-par Q2 Earnings Season in process. Oh yes, we saw the CNBC[S] end-of-week headline last evening: “S&P 500 posts fifth straight record close this week, powered by solid earnings”. Hardly are earnings “solid”. To wit:

In this era of dumbing-down earnings estimates to dirt, ’tis super easy to beat ’em: so far for Q2, we’ve 149 S&P 500 constituents having reported, of which 79% have exceeded expectations! Why typically, only 76% so do! Sadly however, here’s where the “solid” earnings hocus-pocus loses focus. In an average Earnings Season, 66% of the constituents improve their bottom lines over the like quarter of a year earlier. To this point for Q2, such rate has slowed to 63%. ‘Course that shan’t be on CNBS, Bloomy nor FoxyB. But ’tis why the following multiple has gone beyond stoopid:

Again, don’t argue nor ask “AI“; just do the math. And per last week’s piece, yes, we still sense “The Sell” shall be ever-intense.

As to the math that makes up the Economic Barometer, as anticipated, ’twas well ahead of last Monday’s lagging indicator known as the Conference Board’s “Leading Indicators”. So severe had been June’s Econ Baro plunge, we knew the consensii for just -0.1% shrinkage in the June reading was too timid: rather, it came in (no surprise) at -0.3%. Too, the month’s Existing Home Sales slowed and Durable Orders shrank. But bailing the Baro out by just the wee-est of bits was growth in June’s New Home Sales, plus a reduction in the prior week’s Initial Jobless Claims. So below, we’ve the whole picture from one year ago-to-date. Duly therein note the insert of the S&P 500 futures chart for the past month (21 trading days): we made such a song-n’-dance a week ago about the baby blue dots of trend consistency being finally in decline … but they’ve suddenly lurched back up (per the three red dots). “Perfect timing ain’t easy…”:

We see next week as pivotal for both Gold and the S&P. Inclusive of the GDP, the FOMC and the renewed tariffs spree come 18 metrics for the Econ Baro’s scrutiny. As well, Gold’s contract volume rolls from that for August into that for December with better than +50 points of fresh premium, merci! Where might your money be?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

25 July 2025 – 08:39 Central Euro Time

Gold is presently below its Neutral Zone for today; the other BEGOS Markets are within same, and again volatility is light. The Spoo continues to make all-time highs, today (to this point) having reached 6421; currently at 6414, accounting for Fair Value (+36) would pull the S&P 500 higher still at its opening to 6378, just short of its all-time high yesterday of 6381. The S&P is now “extremely textbook overbought” meaning that each of its BollBands, RSI and Stochastics are stretched as such; this last occurred just on 03 July, the following trading day (07 July) then finding a intraday -78-point drop in the S&P. Tomorrow’s 819th consecutive Saturday edition of The Gold Update shall cite the weekly parabolic trend as having flipped from Short-to-Long despite price intraweek having dropped nearly -100 points high-to-low. And the Econ Baro closes out its mild week with June’s Durable Orders.

24 July 2025 – 08:39 Central Euro Time

Both Gold and Silver are presently below today’s Neutral Zones, whilst above same are both Copper and Oil; BEGOS Markets’ volatility is light. Currently our best correlation amongst the five primary BEGOS components is positive between the Bond and Gold. We continue to monitor Market Trends’ “Baby Blues” for the Spoo which have popped back above the key +80% axis: but by Market Values, the Spoo is (in real-time) +269 points above its smooth valuation line, whilst the S&P 500 itself is now “textbook overbought” through its last 21 days; the futs-adj’d “live” P/E is 47.0x even as Q2 Earnings are thus far underperforming their average year-over-year pace of improvement. Today’s Econ Baro incoming metrics include June’s New Home Sales.

23 July 2025 – 08:33 Central Euro Time

Gold’s weekly parabolic Short trend has — after 10 weeks — provisionally flipped to Long as 3449 traded early on at 00:21 GMT; confirmation comes at Friday’s settle, (barring 3123 unlikely trading in the interim). Presently, we’ve the Bond, Euro and Swiss Franc all below their respective Neutral Zones for today; the other BEGOS Markets are within same, and volatility is pushing toward moderate. For the S&P 500, not recognizable in yesterday’s +0.1% gain was a cap-weighted -$62B drain alone from NVDA: mind our S&P Moneyflow page. At Market Trends, the Spoo’s “Baby Blues” of linreg consistency have exceptionally in real-time lurched from +76% to +81%: however, they soon ought well sink sub-80% toward price selling off. Looking at Market Rhythms, on a 10-test basis our leader in the non-BEGOS Yen’s 2hr Parabolics, whilst on a 24-test basis we additionally note the Spoo’s 15mn Parabolics and Gold’s 6hr MACD. June’s Existing Home Sales come due for the Econ Baro.

22 July 2025 – 08:32 Central Euro Time

Apologies as there was a delay in getting yesterday’s commentary posted; ’tis been resolved and is there now. On to today, our key thought is ’tis amazing that 34 of the past 39 monthly Leading Indicators reports have been negative, the pace of earnings improvement weakening, and yet the S&P 500 is making all-time highs: fairly startling stuff. At present this Tuesday, Gold is the only BEGOS Market outside (below) today’s Neutral Zone; session volatility is light. The Spoo’s “Baby Blues” (see Market Trends) of linreg consistency continue to slip, however slightly, the real-time reading now +76%: as regular followers know, having gone beneath the +80% axis generally leads to lower prices near-term. Nothing is due today for the Econ Baro. And as to the noted weakening Q2 Earnings Pace, for the 47 S&P constituents having thus far reported, just 62% have bettered their bottom lines from the like quarter a year ago; such improvement through the years averages 66%. We sense the S&P is quite near “The Sell”.

21 July 2025 – 08:47 Central Euro Time

Into a light economic data week we go with at present the Bond, Gold and Copper above today’s Neutral Zones; none of the other BEGOS Markets are below same, and volatility is pushing toward moderate. The Gold Update describes price as being in a shell these many weeks, the weekly parabolic flip from Short-to-Long now at 3449; too, we emphasize the Spoo’s “Baby Blues” (see Market Trends) as having fallen below the key +80% level: they are lower still today thus far in real-time, such that lower prices ought well appear near-term; the Spoo is currently +246 points above its smooth valuation line (see Market Values). The Econ Baro awaits June’s Leading (i.e. “lagging”) Indicators, which not surprisingly are expected to remain negative, albeit the Baro had a record-setting boost in the past two weeks (as cited in The Gold Update).

The Gold Update: No. 818 – (19 July 2025) – “Gold Stuck in Its Shell; Here Comes the S&P’s Sell”

With Gold’s weekly parabolic trend still Short — uncannily so given there’s not been a wit of substantive price decline throughout — we open with British band Ace from back in ’75: ![]() “How lonnng… has this been goin’ onnn…”

“How lonnng… has this been goin’ onnn…”![]() , such pop hit reaching Billboard’s Hot 100 No. 3 slot on Saturday, 05 April of that year, with Gold having settled the day before at 174.

, such pop hit reaching Billboard’s Hot 100 No. 3 slot on Saturday, 05 April of that year, with Gold having settled the day before at 174.

Fast forward to Gold having settled yesterday (Friday) at 3356 and ’tis a 50-year price increase of +1,829% … just in case you’re scoring at home.

‘Course, compared to the 1¢ cost in 1975 for one piece of Bazooka Bubble Gum, such piece today is bulk-marketed for 24¢, an increase of +2,300%: thus Gold is lagging bubble gum inflation.

“And mmb, by the money supply, it’s about that too, eh?”

Similarly so, Squire. The StateSide “M2” money supply for April 1975 was $935B. From then to today at $22T, ’tis +2,253%. So by either measure, “Got Gold?”

But as to our query via Ace for the duration of Gold’s current weekly parabolic Short trend, note a 10th rightmost red dot having now appeared on the weekly bars from a year ago-to-date. Indeed, Gold appears ever so stuck it its shell of late:

So with Gold still stuck in its shell but the S&P poised for a sell, let’s look at the Stack, for ’tis just swell:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3853

Gold’s All-Time Intra-Day High: 3510 (22 April 2025)

2025’s High: 3510 (22 April 2025)

Gold’s All-Time Closing High: 3453 (13 June 2025)

The Weekly Parabolic Price to flip Long: 3449

10-Session directional range: up to to 3389 (from 3291) = +98 points or +3.0%

Trading Resistance: by the Profile 3359 / 3370 / 3381

Gold Currently: 3356, (expected daily trading range [“EDTR”]: 46 points)

Trading Support: by the Profile 3345 / 3334 / 3320 / 3311

10-Session “volume-weighted” average price magnet: 3342

The 300-Day Moving Average: 2798 and rising

2025’s Low: 2625 (06 January)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Into the new week can the Econ Baro seek a further peak? Probably not, although neither should it succumb much, if at all: just five metrics come due, Monday most notably bringing for June the Conference Board’s lagging indicator known as “Leading Indicators”. Expectations are for the reading to remain negative as ’twas for May: no argument here.

As for our anticipated S&P 500 correction, here are a few P/E nuggets to bear in mind:

- The day before the Garzarelli Crash of ’87 the P/E was 20.3x;

- The day before commencement of the DotComBomb of ’00-’02 the P/E was 29.3x;

- The day before the start of the FinCrisis of ’07-’09, the P/E was 18.7x.

As aforementioned, ’tis now 46.9x, the S&P yielding less than one-third that of the “riskless” U.S. T-Bill.

Note: math-challenged “AI” (“Assembled Inaccuracy”) puts the S&P’s P/E at 25.9x … wrong. (Just wait until “AI” gets its hands on your discretionary portfolio. Reprise: Whoopsie!)

So to wrap:

Query One: “Do you know where your stocks’ stops are?”

Query Two (again): “Got Gold?“

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

18 July 2025 – 09:21 Central Euro Time

The Euro, Silver and Copper are at present above today’s Neutral Zones; the other BEGOS Markets are within same, and volatility is mostly light. The Spoo’s “Baby Blues” (see Market Trends) are basically on their key +80% axis: an up day likely keeps the Short signal at bay through today; both the Spoo and S&P 500 itself yesterday recorded all-time highs both intra-day as well as for settles; the S&P is 17 days “textbook overbought” through yesterday, and the futs-adj’d P/E is presently 46.9x; per usual, the “Baby Blues” shall alert us to the next downside move. Whilst there’s quite a bit of jubilation early on in Q2 Earnings Season over companies having beaten estimates (85% thus far for S&P 500 constituents), only 64% (a below average pace) have actually bettered their bottom lines from the like quarter a year ago. The Econ Baro wraps its robust upside week with July’s UofM Sentiment Survey, plus June’s Housing Starts/Permits.

17 July 2025 – 08:43 Central Euro Time

Presently, the Euro, Swiss Franc and Gold all are below today’s Neutral Zones; none of the other BEGOS Markets are above same, and session volatility is pushing toward moderate. Amongst the five primary BEGOS components, the best correlation currently is positive between the Bond and Euro. Per yesterday’s comment, the Spoo’s “Baby Blues” (see Market Trends) are in real-time down to the +80% axis: confirmation of breaking below that level reasonably suggests a near-term run into the lower 6100s, (current price 6310); of note, the “live” P/E of the S&P 500 (futs-adj’d) is 46.5x. And ’tis a very busy day for the Econ Baro with eight metrics due, including July’s Philly Fed and NAHB Housing Indices, June’s Retail Sales and Ex/Im Prices, plus May’s Business Inventories.

16 July 2025 – 08:21 Central Euro Time

Gold is the sole BEGOS Market at present outside (above) today’s Neutral Zone; session volatility is very light. Per Market Rhythms, our current leaders for pure swing consistency are (on a 10-test basis) Gold’s 6hr Parabolics, and (on a 24-test basis) Oil’s 15mn MACD, Gold’s 6hr MACD, and the non-BEGOS Yen’s 2hr Parabolics. Although both the S&P 500 and Spoo yesterday reached intra-day all-time highs, the Spoo’s “Baby Blues” (see Market Trends) are slipping in real-time to the +83% level: should they settle below the key +80% axis level come tomorrow or Friday, ‘twould be an outright sell signal; too, the anticipated price declines as herein noted are in progress given recent like signals for the Bond, Euro and Swiss Franc. Oil’s cac volume is rolling from August into that for September. The Econ Baro awaits June’s PPI and IndProd/CapUtil. And late in the session is the release of the Fed’s Tan Tome.

15 July 2025 – 08:25 Central Euro Time

The Euro, Gold and the Spoo are at present above their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and session volatility is mostly light, save for Gold having traced 52% of its EDTR (see Market Ranges). The Spoo is teasing an all-time high toward 6336: the “live” (futs-adj’d) P/E of the S&P 500 is 46.2x with a yield of 1.228%; that for the 3mo. U.S. T-Bill annualized is 4.228%. The Spoo by Market Values in real-time is +216 points above its smooth valuation line and the S&P itself is now “textbook overbought” through the last 14 trading days. The Econ Baro gets its busy week underway with July’s NY State Empire Index, plus June’s CPI which is expected to have heated up.

14 July 2025 – 08:40 Central Euro Time

The week is off and running with at present the Euro and Spoo below today’s Neutral Zones, whilst above same is Silver, the star of The Gold Update; BEGOS Markets’ volatility is light-to-moderate. As anticipated, the Swiss Franc’s “Baby Blues” (see Market Trends) of linreg consistency confirmed on Friday having fallen beneath their key +80% axis, as had those for the Euro a day earlier; should the Franc get some downside momentum, we’d initially target 1.25050, (current price being 1.26285); too for the Euro (currently 1.17065) we’re seeking at least 1.16855, (the signal having originated from 1.17510). The Econ Baro is quiet today with 18 incoming metrics then due in the week’s balance. And Q2 Earnings Season picks up its reporting pace as the week unfolds: ’twill be interesting to see how year-over-year profitability has fared given the marked decline in the Econ Baro through Q2.

The Gold Update: No. 817 – (12 July 2025) – “Gold May Be Boring, but Silver is Soaring!”

And so we close with this from the “Hype of the Week Dept.” featuring Nvidia (NVDA). (Even as we “don’t do stocks”, this was too good to avoid the curiosity of doing the math). Ready?

The mighty video card maker turned “AI” chipster now tops the S&P 500 market capitalization at just over $4T. Thus for these last couple of days we’ve been hearing time and again that “Wow! Nvidia’s worth over $4T!!” … except such use of the vernacular is incorrect. ‘Tis worth nowhere near $4T.

Rather, by the company’s balance sheet as recorded at the end of this past Q1, the net worth is $84B. In other words, the amount of money invested in Nvidia as marked-to-market today is 48x what the company actually is worth; (that shan’t be on Bloomy, nor FoxyB, nor CNBS, neque alii). Such stat is actually quite similar to that for Apple (AAPL)’s 47x; however, far more conservative is Microsoft (MSFT)’s 12x, even as its net worth is some four times greater than that of Nvidia.

Still, for those of you scoring at home with a marked-to-market investment at present of, say, $10,000 in Nvidia, were the company to instantly (in theory) liquidate, you’d receive (if lucky after the bondholders) about $200, i.e. only 2% of “what you thought you had”. Have a nice day.

‘Course the lesson for you WestPalmBeachers down there is: when you buy shares in a publicly-traded company, it doesn’t get the money; it goes to the seller. So try not to get carried away…

And congrats if not having forgotten Soaring Sister Silver!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

11 July 2025 – 08:38 Central Euro Time

Both Gold and Silver are at present above today’s Neutral Zones, whilst below same are both Copper and the Spoo; volatility is moderate for the BEGOS Markets, save for Oil which has traced but 21% of its EDTR (see Market Ranges). With Friday left in the balance, Gold may be en route to recording its narrowest trading week of the year: more, ‘natch, in tomorrow’s 817th consecutive Saturday edition of The Gold Update. The Euro confirmed its “Baby Blues” (see Market Trends) of linreg consistency have settled below their +80% axis; the Swiss Franc appears to do same come today’s close. Too, the Euro is now paired with Gold for the best current correlation — in this case negative — amongst the five primary BEGOS components, (reminding us once again that Gold plays no currency favourites). The Econ Baro finishes its muted week late in the session with June’s Treasury Budget.

10 July 2025 – 09:22 Central Euro Time

At present all three elements of the Metals Triumvirate are above their respective Neutral Zones for today, whilst below same is the Spoo; BEGOS Markets’ volatility is pushing toward moderate. Given the recent hem-n-haw of late, we’ve no outstanding Market Rhythms for pure swing consistency; however from the “fade” (i.e. “anti-rhythm”) category, the best 10-test “fade” has been the non-BEGOS Yen’s 4hr EMA; for the 24-hour basis, the best “fade” has been Oil’s daily MACD. By Market Profiles, Gold’s most volume-dominant overhead resistor is 3347, whereas for Silver, her best volume-dominant underlying supporter is 36.65. For the EuroCurrencies, the “Baby Blues” (see Market Trends) of both the Euro and Swiss Franc continue to curl over to the downside such that by week’s end, one if not both shall confirm sell signals (upon the Blues falling below the +80% axis). The only metric due today in this quiet stint for the Econ Baro is last week’s Initial Jobless Claims.

09 July 2025 – 08:44 Central Euro Time

Copper yesterday recorded its largest percentage gain from prior close-to-high (+17.8%) so far this century, the day’s net gain (+10.1%) ranking third-most. This morning, the red metal is at present +3.3% and ’tis the only BEGOS Market above its Neutral Zone; below same is Gold, and session volatility is mostly light, save for Copper having thus far traced 148% of its EDTR (see Market Ranges). Going ’round the Market Values horn for the five primary BEGOS components in real-time: the Bond shows as -2^01 points “low” vis-à-vis its smooth valuation line, the Euro as +0.0098 points “high”, Gold as -120 points “low”, Oil as +1.14 points “high”, and the Spoo as +164 points “high”. Q2 Earnings Season is underway. The Econ Baro looks to May’s Wholesale Inventories. And late in the session come the FOMC’s Minutes from its 17-18 June Meeting.

08 July 2025 – 06:41 Central Euro Time

Very early on this morning as we go into motion, the Euro, Swiss Franc and Spoo all are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light, given the hour. As anticipated, Oil’s “Baby Blues” (see Market Trends) of linreg consistency have just slipped below their 0%, indicative of the trend having rotated to negative. Too, those for both the Euro and Swiss Franc are showing the initial signs of rolling very after having been “on the ceiling” of late. Our best Market Rhythm for the Bond (by which a profit target is sought rather than a pure swing) is its daily MACD having confirmed a negative crossing to start the session: better than 3 fully points of gain have followed 7 of the past 10 crossovers. And late in the session for the Econ Baro comes May’s Consumer Credit.

07 July 2025 – 08:47 Central Euro Time

The two-day (04 and 07 July) trading session continues, now finding Gold, Silver, Copper, Oil and the Spoo all below their respective Neutral Zones; the Bond and EuroCurrencies are within same, and volatility for the BEGOS Markets is moderate albeit Silver has traced 111% of its EDTR (see Market Ranges). The Gold Update depicts the last week having recorded both a lower high and a lower low, yet finishing with a net weekly gain, a phenomena not having occurred since last October; regardless, Gold’s weekly parabolic trend remains Short through the past eight weeks; Gold at present is the sole BEGOS component sporting a negative linreg (see Market Trends): however those for both Silver and Oil appear poised to rotate from positive to negative as the week unfolds. Just four metrics are due for the Econ Baro this week, none being on the slate for today.

The Gold Update: No. 816 – (05 July 2025) – “Gold’s ‘Weak’ Up Week … and What We Bespeak”

Thus as the U.S. concludes its third holiday-shortened trading week of the last six (they’re getting a bit like France in that respect), Monday ’tis back to work right up to Labor Day (01 September). But for the Econ Baro, next week brings really encouraging news: just a wee four metrics are due such that the Baro likely doesn’t get bruised. Thus let the complacency keep all enthused as The Investing Age of Stoopid continues! Just don’t lose your shoes…

Dem dogs r’ Gold-Smart!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

04 July 2025 – 08:42 Central Euro Time

The BEGOS Markets commence a two-day session for Monday settlement such as to bridge the gap of the StateSide Holiday. And at present we’ve the Euro, Swiss Franc and Gold above their respective Neutral Zones, whilst below same are both Copper and the Spoo; session volatility is pushing toward moderate. Gold looks poised to post an up week, albeit with likely both a lower high and lower low than a week ago; more of course in tomorrow’s 816th consecutive Saturday edition of The Gold Update. The S&P 500 settled its week at yet another all-time high (6279 at close) and with a trailing 12 months’ P/E of 45.1x; the Index is now in an extreme “textbook overbought” condition; and specific to the Spoo (which is trading today until the 17:00 GMT holiday halt) is in real-time +218 points above its smooth valuation line (see Market Values). Happy 4th to those of you across The Pond!

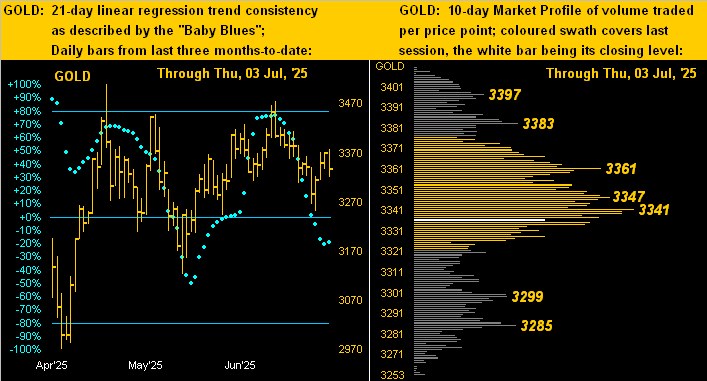

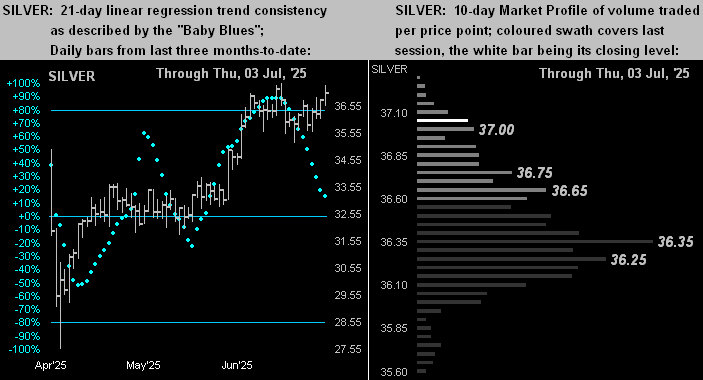

03 July 2025 – 08:43 Central Euro Time

At present we’ve only Silver outside (above) its Neutral Zone for today; BEGOS Markets’ volatility is again light. Looking at correlations amongst the five primary BEGOS components, our best currently is positive between the Euro and Spoo, both of which have firmly been relentlessly up month-over-month; indeed at Market Trends, the “Baby Blues” of linreg consistency for both markets are essentially “crawling across the ceiling”. The “live” P/E of the S&P 500 is (futs adj’d) 44.9x and the yield 1.237% vs. 4.223% annualized on the U.S. 3mo T-Bill; too, the S&P is now seven consecutive trading days “textbook overbought”. Given the StateSide holiday tomorrow, we’ve eight incoming metrics for the Econ Baro, including June’s Payrolls data and ISM(Svc) Index, plus May’s Factory Orders and Trade Deficit. The BEGOS Markets resume trading at their usual time tonight, but with settlement for Monday, (07 July), inclusive of the trading halt late tomorrow.

02 July 2025 – 08:39 Central Euro Time

The Euro is at present below its Neutral Zone for today whilst above same is the Spoo; session volatility for the BEGOS Markets is light. Gold is leading our Market Rhythms for pure swing consistency: on a 10-test basis is the yellow metal’s 6hr MACD; on a 24-test basis are both the 4hr and 8hr Parabolics; Gold had a firm start to the week, however its 21-day linreg trend continues to rotate more negatively, the “Baby Blues” of such trend’s consistency furthering their fall (see Market Trends). Following the ISR/IRN conflict, Oil’s day-to-day range has narrowed considerably, the last five trading sessions having spanned less than two points/day vs. the EDTR (see Market Ranges) of currently 3.44 points. And the Spoo continues its move up into record territory, albeit the S&P’s MoneyFlow yesterday was far more negative than the slight down change in the Index itself. The Econ Baro looks to June’s ADP Employment data.

01 July 2025 – 08:36 Central Euro Time

Both Gold and Copper are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility is moving toward moderate. At Market Trends, Gold is the sole component in negative linreg, even as price is bouncing a bit; by Market Ranges, Gold’s EDTR is now 56 points, (of which 54% has traded thus far today); Copper already has traded 90% of its EDTR (0.114 points); the red metal is having a solid up run despites its “Baby Blues” of trend consistency weakening some two-to-three weeks ago; Copper’s best Market Rhythm currently for pure swing consistency on our 10-test basis is its 30mn Parabolics. For the Econ Baro we’ve June’s ISM(Mfg) Index and May’s Construction Spending.

30 June 2025 – 08:35 Central Euro Time

This first day of the week and last day of Q2 finds at present Gold, Silver and the Spoo above today’s Neutral Zones; the other BEGOS Markets are within same, and volatility is moderate. The Gold Update takes a near-term bearish view, especially given the highly-visible weekly MACD having confirmed a cross to negative, (and the weekly parabolic Short trend having completed a seventh week); too, Gold’s 21-day linreg trend has rotated to negative; price at present is 3301, however has traded thus far this morning to as low as 3251. The Spoo (6254) is sufficiently up at the moment for the S&P 500 to open above 6200, (“fair value” is +50 points). And the Econ Baro looks to June’s Chi PMI.

The Gold Update: No. 815 – (28 June 2025) – “Gold –> The (Short) Saga Continues…”

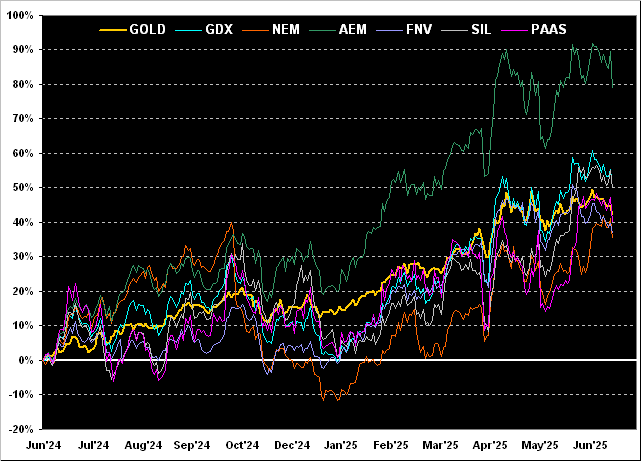

To wrap it up, ‘twouldn’t be month-end (less a day) without the BEGOS Markets’ Standings. And through these six months, our Metals Triumvirate has dominated the podium: none of the other markets thus far have fared better than fourth position. For June, swapping the first two spots from May are Gold by Copper, the red metal having just recorded its fourth best week (+4.8%) of the year. Meanwhile the non-earnings supportive S&P 500 miraculously clings to a +5.0% gain, oblivious to its pending pain, (yes ’tis coming with a vengeance by any historical means-reversion measure of earnings multiples, the “live” price/earnings ratio at present 44.6x). Moreover as earlier teased: pity the poor Dollar! The Dollar Index is -10.5% through the first half of this year. That is Dixie’s worst first six months’ percentage drop since coming on line as a futures product 40 years ago! Again cue the late, great “Bullet” Bill King: “Holy Toledo!!”

But barring anything untoward (i.e. renewed geo-political jitters, an equity market collapse, the inevitable loss of confidence in the financial system), we shan’t be surprised to find Gold working lower through here. Yet one can buy Gold’s dip to stay financially fit!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro