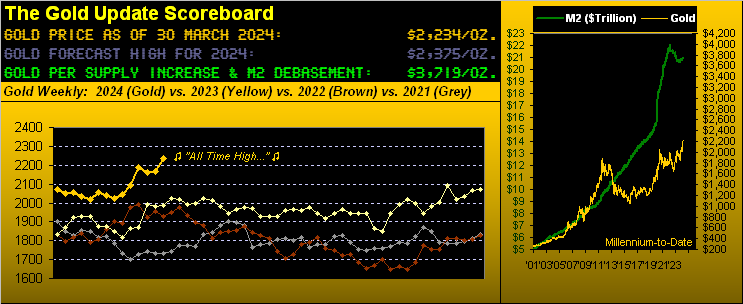

Welcome one and all to the 750th consecutive Saturday edition of The Gold Update. Having missed nary a Saturday since our first missive (20 November 2009) with Gold then 1151, price since has nearly doubled (+94%), toward settling this past shortened trading week on Thursday at the latest All-Time High of 2234. Thus we’ve a milestone price for Gold in synch with this milestone missive.

To be sure across the same stint, Gold supply’s tonnage has increased +23% for which we rightly account in the above Scoreboard valuation of 3719; but the U.S. liquid money supply (“M2”) has far more overwhelmingly increased +147% (that’s 2.5x for those of you scoring at home). ‘Tis reason right there to make sure you own Gold!

So as we turn to Gold’s weekly bars and parabolic trends from one year ago-to-date, let’s again cue Rita Coolidge from back in ’83 with ![]() “All Time High”

“All Time High”![]() :

:

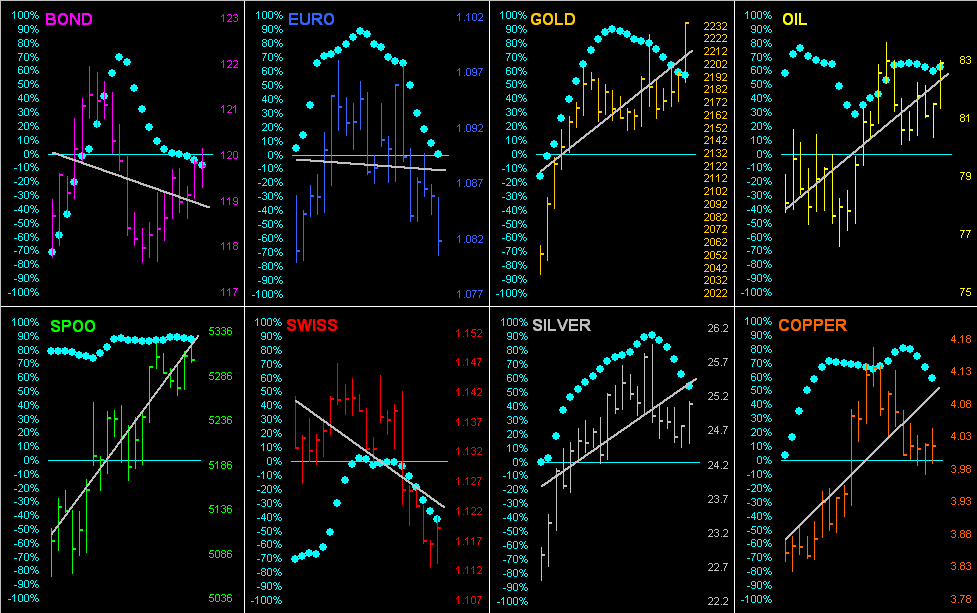

To close — given that the yellow metal is at an All-Time High — nothing could be more appropriate to wrap than with The Gold Stack, with the June contract but one row below debasement valuation:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3719

JUNE Gold Currently: 2255, (expected daily trading range [“EDTR”]: 30 points)

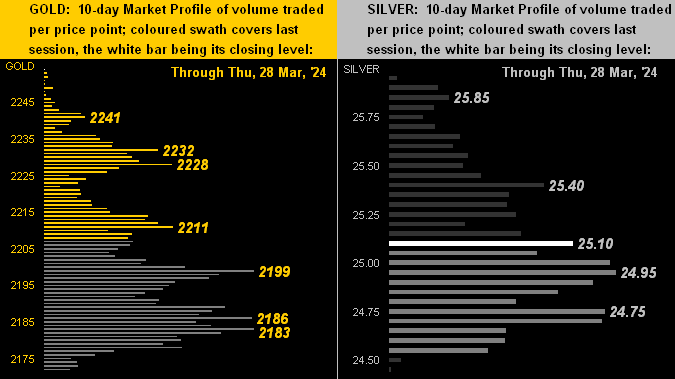

Trading Support (basis June): 2241 / 2232 / 2228 / 2211 / 2199 / 2186 / 2183

Gold’s All-Time Intra-Day High: 2234 (28 March 2024)

2024’s High: 2234 (28 March)

10-Session directional range: up to 2234 (from 2149) = +85 points or +4.0%

Gold’s All-Time Closing High: 2234 (28 March 2024)

Trading Resistance: (none)

10-Session “volume-weighted” average price magnet (basis June): 2202

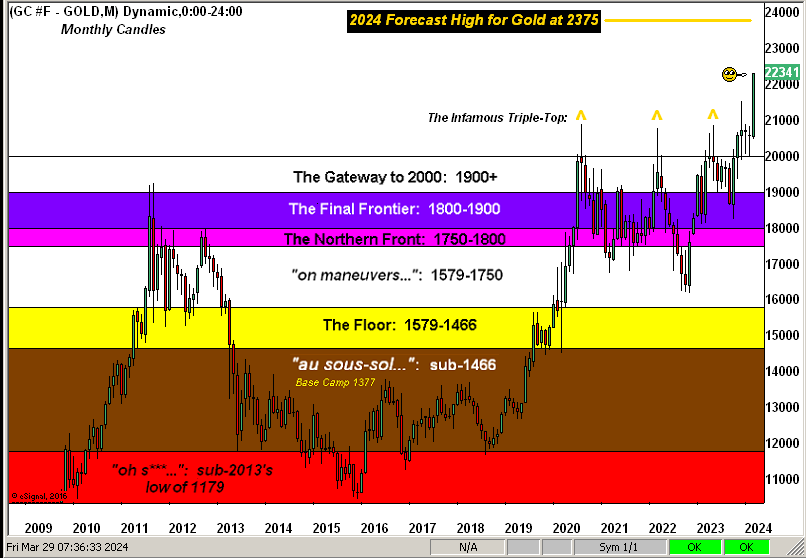

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Weekly Parabolic Price to flip Short: 2023

2024’s Low: 1996 (14 February)

The 300-Day Moving Average: 1983 and rising

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

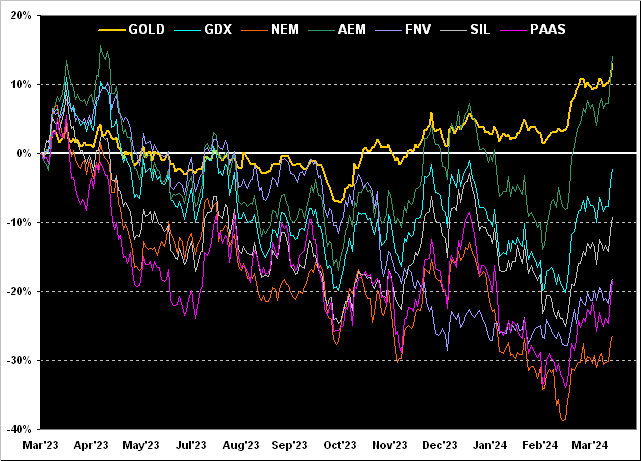

So there we’ve missive No. 750 as magnificently aligned with a Gold All-Time High. Will it get any better? ‘Course ’twill! Just make sure you make your move with Gold!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro