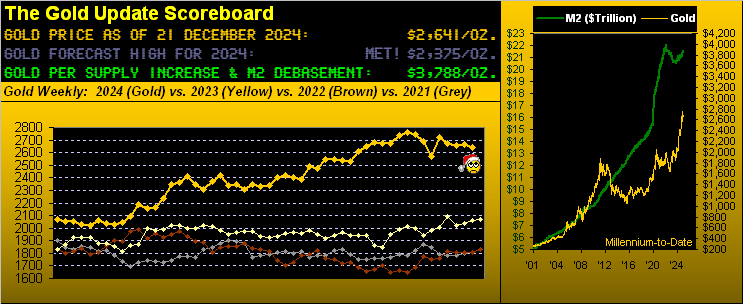

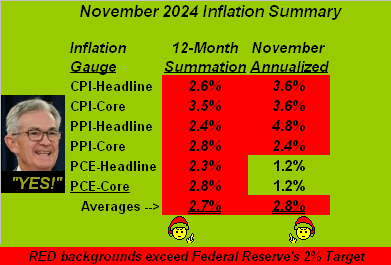

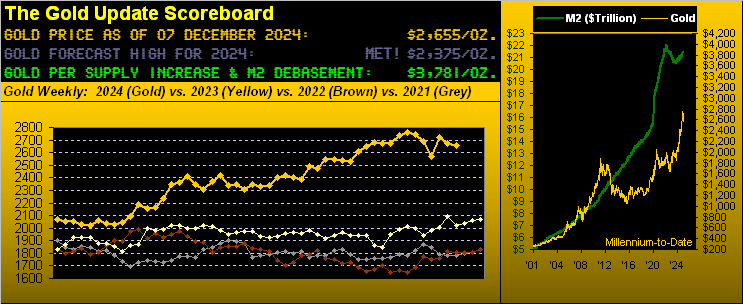

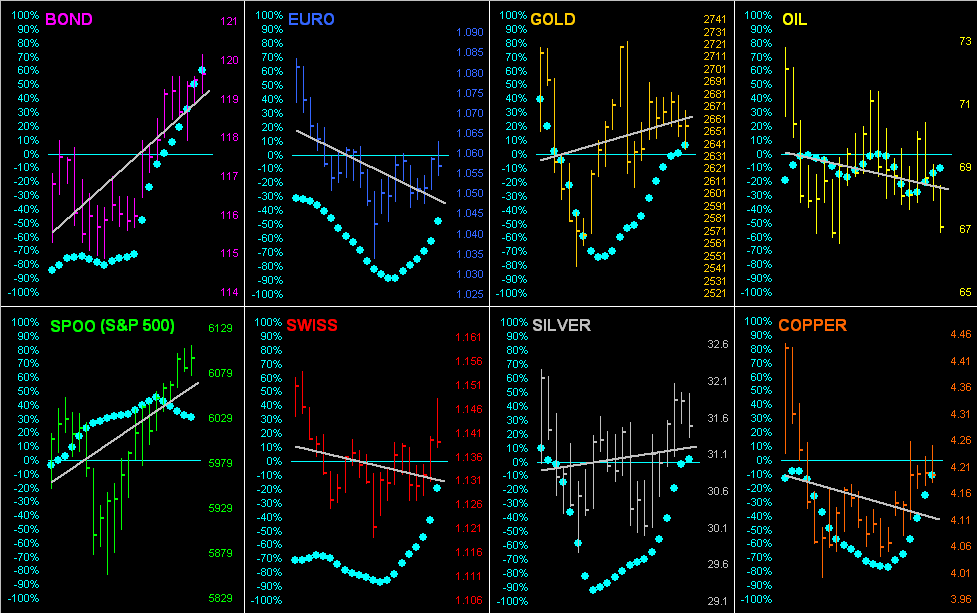

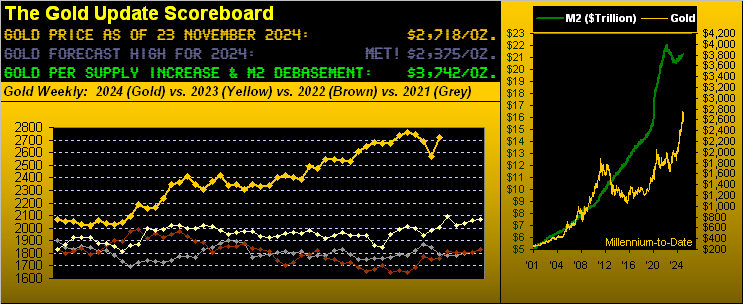

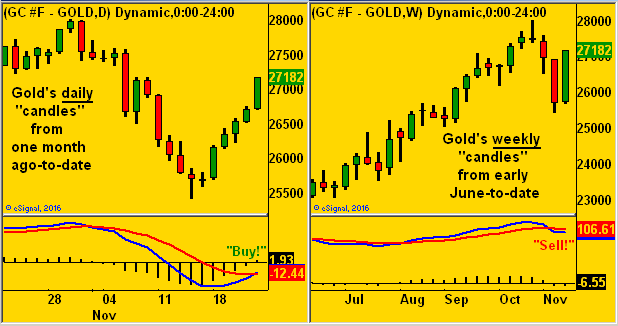

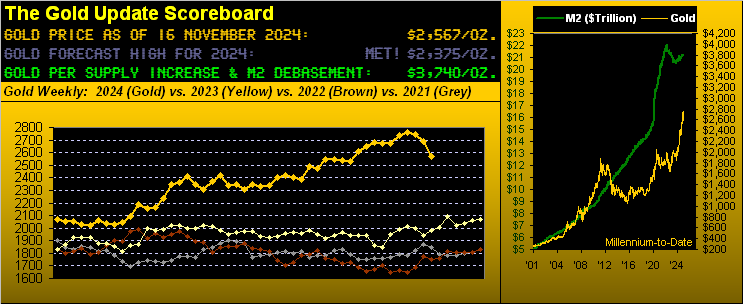

2025’s trading commences finding all eight BEGOS markets at present in the black, those notably above today’s Neutral Zones being the Swiss Franc, Gold, Silver and the Spoo; session volatility is moderate-to-robust. As we’ll see in the next Gold Update for this Saturday, the yellow metal was the best BEGOS performer of 2024, +27.4%. The futs-adj’d “live” P/E of the S&P 500 is 46.4x and the yield 1.274% versus 4.208% annualized for the risk-free 3-month U.S. T-bill, (albeit as mentioned in the current edition of The Gold Update, “Old Yeller” faces an ‘event of default’ come mid-month barring another Congressional bailout). The Bond (113^28) has just climbed above 113^26, its most dominantly-traded price across the past fortnight: as mentioned in Tuesday’s comment, there’s room for the Bond to move up into the 116s. The Econ Baro get’s 2025 underway, today’s incoming metrics including November’s Construction Spending.

Mark

Mark

31 December 2024 – 08:41 Central Euro Time

Into the year’s final stint we go, with at present both the Bond and Oil above their respective Neutral Zones for today; none of the other BEGOS Markets are below same, and volatility again is light. We’d noted yesterday the Bond’s being quite extended below its smooth valuation line (see Market Values) such that a rise into New Year wouldn’t be untoward: mind at Market Trends the Bond’s “Baby Blues” of trend consistency to support a higher price upon their eclipsing up through the -80% axis; (in real-time they are -91%); for price itself currently 114^16, by its Market Profile there is room to move all the way up to volume resistance at 116^08. The S&P 500 enters its last trading day of the year with a “live” (futs-adj’d) P/E of 46.0x, still dangerously high by any historical yardstick. On to 2025, et Bonne Anneé à Tous!

30 December 2024 – 08:46 Central Euro Time

Both Gold and the Spoo are presently below today’s Neutral Zones; the balance of the BEGOS Markets are within same. and volatility is light. The Gold Update points to price’s ongoing technical negativity, however stating it being more hesitant than in a downtrend; too from a century-to-date perspective (23 completed years), Gold has a tendency to trade net higher for the final two days of the year, whereas the S&P 500 has a tendency to trade net lower. At Market Trends, with the exception of Oil, the seven other BEGOS components are all in negative linreg trends from a month ago-to-date. An interesting trade for which to watch into New Year is the Bond: ’tis (in real-time) nearly -5 full points below its smooth valuation line (see Market Values); typical downside deviation extends to around -3 points. With nothing on its slate for tomorrow, the Econ Baro completes its year today with December’s Chicago PMI and November’s Pending Home Sales.

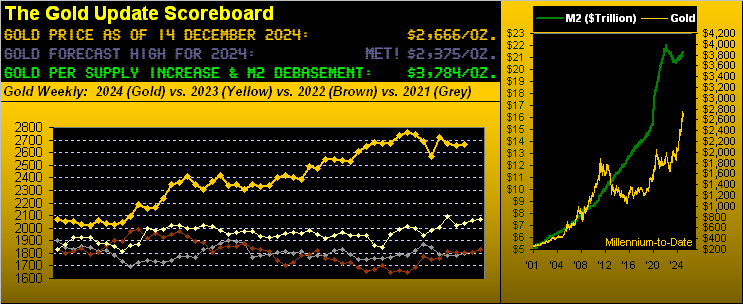

The Gold Update: No. 789 – (28 December 2024) – “Gold’s Weak Wend Toward Year-End”

The upper panel for each market tracks its daily closing price (thin line) from three months ago-to-date; the thick line is the Magnet. The lower panels are the oscillative difference of price less Magnet. And what is evident in all three cases is price now poised to penetrate Magnet to the upside, suggesting a rally for the metals into New Year. (Again, you can monitor such daily progression at the website).

Meanwhile, struggling for further upside progression — albeit duly holding its own through autumn — is the Economic Barometer. This past week was very muted for the Baro given the wee slate of just four incoming metrics. Therein of note, December’s Consumer Confidence declined on the heels of November’s Durable Orders having shrunk; however, that month’s New Home Sales did increase. So ![]() “When the Econ Baro comes bob-bob-bobbin’ along…”

“When the Econ Baro comes bob-bob-bobbin’ along…”![]() –[hat-tip Harry Woods, ’26], there appears little impetus for the Federal Open Market Committee’s voting to again nudge lower its Bank’s FundsRate come the 29 January Policy Statement. Moreover as herein depicted a week ago, StateSide inflation is still running a bit hot for the Fed’s liking. Either way, here’s the Baro:

–[hat-tip Harry Woods, ’26], there appears little impetus for the Federal Open Market Committee’s voting to again nudge lower its Bank’s FundsRate come the 29 January Policy Statement. Moreover as herein depicted a week ago, StateSide inflation is still running a bit hot for the Fed’s liking. Either way, here’s the Baro:

To close, we’ve two full trading days remaining for 2024. Conventional wisdom presumes “Oh this is gonna happen!” and “Oh that is gonna happen!” as year-end market hysteria unfolds. From our purview, we don’t think much at all is “gonna happen”.

To break it down a bit for those of you scoring at home:

- Notwithstanding Gold’s weak wend toward year-end, century-to-date with just two trading days left in the balance, price’s median percentage change either way has been 0.7%. The bias is to the upside, 18 of those 23 yearly finishes being higher for the two days.

- But as to the S&P 500 with just two trading days left in the balance, its median percentage change either way has been 0.6%, the bias being to the downside as 14 of those 23 two-day finishes were lower.

“So mmb, at Monday’s open we go Long Gold and Short the S&P for two days, eh?”

Tempting as ’tis, Squire, the best way always to go is with prudent cash management.

Regardless, as you know, the old saying is “As goes January so goes the year.” And the month’s Main Event commences 14 January upon U.S. Secretary of the Treasury Janet “Old Yeller” Yellen begging for dough upon which to draw to pay obligations on the nation’s debt. As was so brilliantly scripted in Paramount’s ’64 feature “Paris When It Sizzles”, the Secretary’s performance shall be that “Ultimate and inevitable moment. The final, earth-moving, studio-rent-paying, theatre-filling, popcorn-selling” plea to Congress for “extraordinary measures” to avoid default.

‘Course, the best anti-default asset is Gold!

Next week we’ll have 2024’s final standings of the BEGOS Markets (Bond, Euro/Swiss, Gold/Silver/Copper, Oil, S&P 500) along with your favourite month-end graphics, (plus two trading days into 2025). Until then:

Happy Sizzlin’ New Year and Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

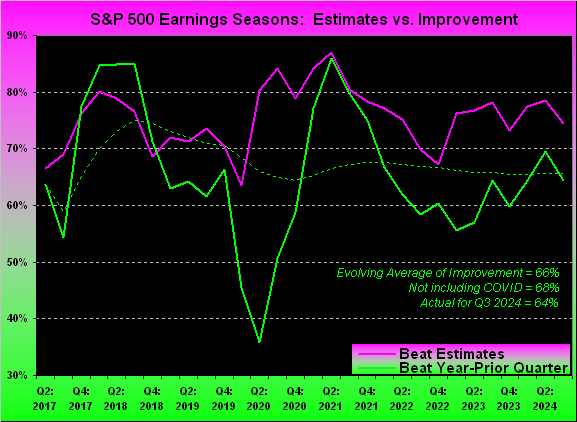

and now on “X”: @deMeadvillePro

27 December 2024 – 08:40 Central Euro Time

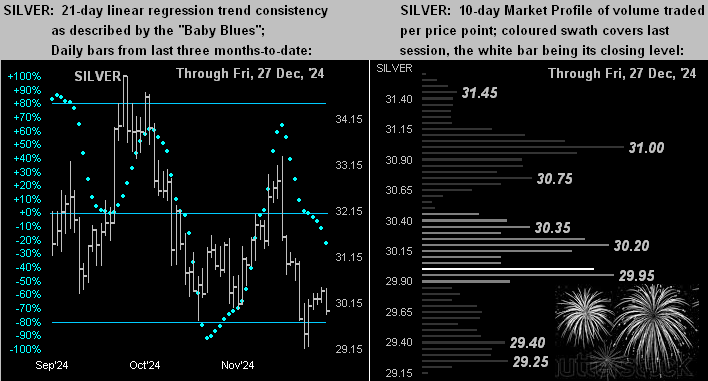

At present, the Swiss Franc is the only BEGOS Market outside (below) its Neutral Zone for today; session volatility to this hour continues quite light. By Market Rhythms, the current best for pure swing consistency are — on a 10-test basis — the non-BEGOS Yen’s daily Parabolics and daily Price Oscillator, Gold’s 8hr Parabolics, and the Spoo’s 15mn Moneyflow, whilst — on a 24-test basis — we’ve again those same two Yen and Spoo studies, plus Gold’s 1hr Parabolics and the Swiss Franc’s 2hr MACD. The Market Magnets of all three elements of the Metals Triumvirate appear poised for penetration to the upside, meaning prices may get a lift into New Year: we’ll take at look at those in tomorrow’s 789th consecutive Saturday edition of The Gold Update.

26 December 2024 – 08:18 Central Euro Time

Gold is the sole BEGOS Market at present outside (above) today’s Neutral Zone; session volatility is again very light. That notwithstanding, Tuesday’s +1.1% gain for the S&P 500 now places the “live” P/E (futs-adj’d) at an amazing 48.7x: ’tis double what might be considered an acceptable modern-day norm, and triple that taught in B-school for the norm during a bull market; again, the +$7T printed to counter the negative effects of COVID fungibly found its way into the S&P, the market-cap for which increased by same. True, risk-free U.S. debt is yielding triple that of the S&P’s paltry 1.234%, but risk-full stocks remain the “sexy” place to be; mind too our S&P 500 “Valuations & Rankings” page. The Econ Baro wraps its week today with last Saturday’s Initial Jobless Claims.

24 December 2024 – 08:40 Central Euro Time

The abbreviated trading session presently finds all eight BEGOS Markets within their respective Neutral Zones for today, and session volatility is very light. Looking at Market Rhythms for pure swing consistency, on a 10-test basis the leaders currently are the non-BEGOS Yen’s daily Price Oscillator and Parabolics, plus Gold’s 8hr Parabolics; for the 24-test basis ’tis the same two Yen studies along with Gold’s 4hr Moneyflow, notably which just flipped to Short at today’s open. At Market Trends (in real-time) six of the eight BEGOS Components are in negative linregs, the only two positive being for Copper and Oil. And at Market Values, two notable deviations are the Bond’s being nearly -4 points below its smooth valuation line and the Euro -0.018 points below same. No incoming metrics are due today for the Econ Baro. Joyeux Noël d’ici à Tous !

23 December 2024 – 08:19 Central Euro Time

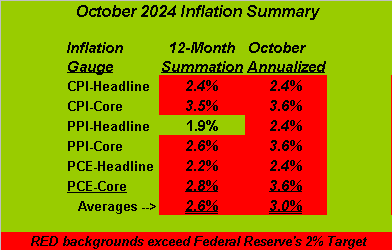

As the first of two abbreviated trading weeks begins, we’ve at present both Silver and the Spoo above today’s Neutral Zones; none of the other BEGOS Markets are below same, and volatility is light. The Gold Update points to the disparate inflation reads wherein the BLS reads it as increasing whilst the BEA sees it as decreasing; Gold itself remains in its weekly parabolic Short trend, perhaps en route to test the upper 2400s given the expanding negativity of the weekly MACD. Moneyflow into the S&P 500 continues to be robust, our page thereto so showing for each of the weekly, monthly and quarterly charts, even as the “live” P/E remains an unsustainable 47.3x. The Econ Baro kicks off its subdued week with December’s Consumer Confidence, plus November’s Durable Orders and New Home Sales.

The Gold Update: No. 788 – (21 December 2024) – “Gold Seeks Charisma ‘Round Inflation’s Enigma”

In turn challenged by it all, Gold is doing its darnedest to seek some charisma. Despite price’s rampant volatility, Gold settled the week at 2641, “net net” again being little changed as we’d seen the week prior. Two weeks ago, Gold traced 112 points for a net change of only +11; now this past week, Gold traced 87 points for a net change of only -25. Thus Gold’s net two-week change is but -14 points. Reprise Chris Isaak’s tune from back in ’95: ![]() “Goin’ Nowhere“

“Goin’ Nowhere“![]()

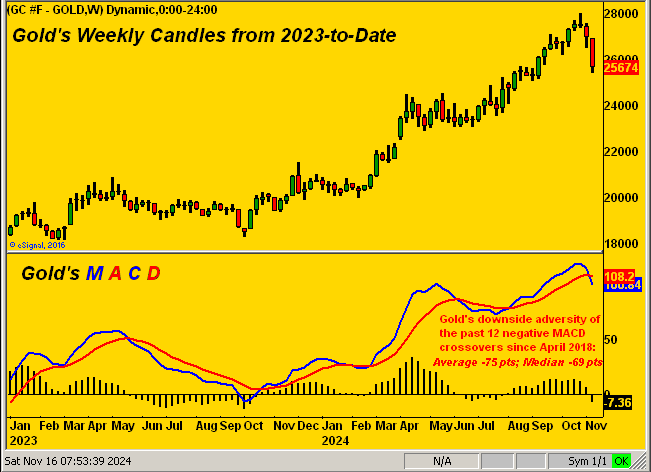

That warbled, Gold has wobbled on balance a bit lower within the context of its ongoing parabolic Short trend per the weekly bars as next shown from a year ago-to-date. Indeed, this past week’s low — 2597 — was the lowest level traded since 2569 back on 18 November. Further upon this Short parabolic trend’s commencement, you may recall our penned suggestion of “…Gold revisiting the upper 2400s on this run…” given the weekly MACD (moving average convergence divergence) also then having crossed to negative, which since has continued to deteriorate. Rather anti-charismatic, that. To the bars and rightmost red-dotted Short trend, now six weeks in duration:

Thus as we glide into winter and the first of two back-to-back abbreviated trading weeks, let’s assess the state of The Stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3788

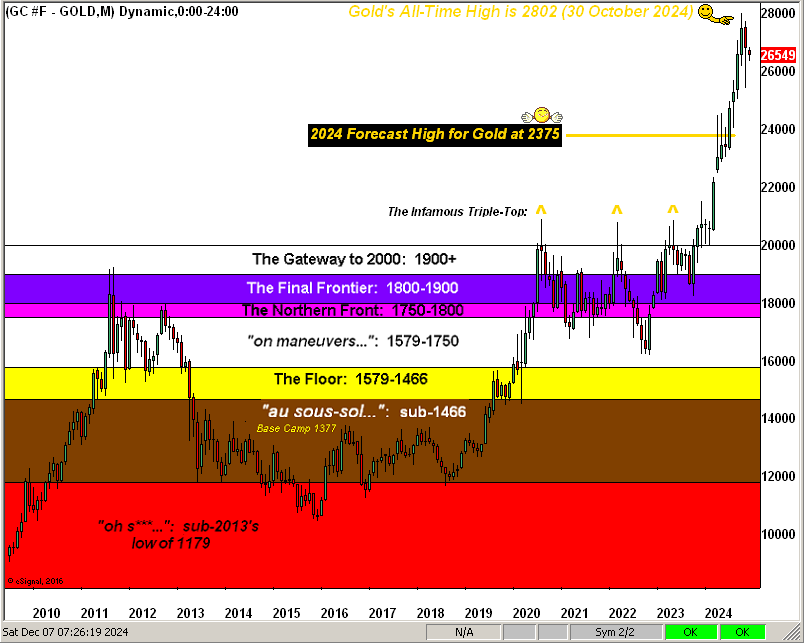

Gold’s All-Time Intra-Day High: 2802 (30 October 2024)

2024’s High: 2802 (30 October 2024)

Gold’s All-Time Closing High: 2799 (30 October 2024)

The Weekly Parabolic Price to flip Long: 2777

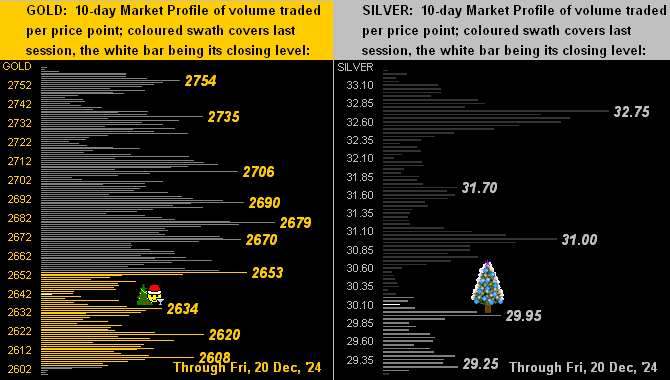

10-Session “volume-weighted” average price magnet: 2681

Trading Resistance: notable nearby Profile nodes 2653 / 2670 / 2679 / 2690

Gold Currently: 2641, (expected daily trading range [“EDTR”]: 44 points)

Trading Support: 2634 / 2620 / 2608

10-Session directional range: down to 2599 (from 2761) = -162 points or -5.9%

The 300-Day Moving Average: 2329 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

In sum, Gold whilst seeking some charisma at least technically still looks to falter a bit; but fundamentally as the late great Richard Russell would remind us, there’s never a bad time to buy it. This gem to wit, courtesy of The Royal Mint:

Indeed, Merry Everything to Everybody Everywhere and don’t forget the Gift of Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

20 December 2024 – 08:44 Central Euro Time

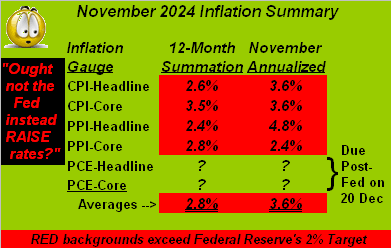

Gold is presently above its Neutral Zone for today, whilst below same is the Spoo; BEGOS Markets’ volatility is light-to-moderate. Looking at correlations amongst the five primary BEGOS components, the best currently is positive between the Euro and the Spoo; the latter’s linear regression trend (see Market Trends) appears poised to rotate from positive to negative, if not today, then come Monday; again, prior to the S&P 500’s Wednesday rout, the daily Parabolics on the March Spoo already had flipped from Long to Short effective last Monday’s open. November’s Leading Indicators indeed came in as positive despite the “consensus” for a negative reading: as herein penned yesterday, they “…are supposed to be mildly negative, but an “unch” or mildly positive read wouldn’t surprise us given the Baro’s recent resilience”; ’tis why we regularly refer to them as “lagging” indicators given the Baro leads them. And for today, incoming metrics include November’s Personal Income/Spending along with the “Fed-favoured” inflation read via the Core PCE. Our November inflation table shall thus be complete for tomorrow’s 788th consecutive Saturday edition of The Gold Update.

19 December 2024 – 08:46 Central Euro Time

Following an across-the-board down day for all eight BEGOS Markets, we’ve at present the Euro, Swiss Franc, Gold, Silver and Spoo all above their respective Neutral Zones for today; the other three components are within same, and volatility is moderate-to-robust, Gold notably already having traded 90% of today’s EDTR (see Market Ranges). Prior to yesterday’s downdraft for the S&P, we’d herein penned early Tuesday that “…for the S&P … ’tis so overcooked to this point both fundamentally and technically that some degree of downside hoovering awaits; perhaps ’twill be a ‘sell the priced-in’ Fed announcement…” which indeed resulted: ’twas the S&P’s fifth-worst one-day points slide (-178) in its history and on a percentage basis (-2.9%) in nearly the 99th percentile of worst one-day losses. In midst of it all, by Market Values, the Spoo reached back down to its smooth valuation line. Incoming metrics for the Econ Baro today include Q3’s final GDP read, December’s Philly Fed Index, plus November’s Existing Home Sales and Leading (i.e. “lagging”) indicators: that latter are supposed to be mildly negative, but an “unch” or mildly positive read wouldn’t surprise us given the Baro’s recent resilience.

18 December 2024 – 08:38 Central Euro Time

Copper is at present below its Neutral Zone for today, whilst above same is the Spoo; BEGOS Markets’ volatility is quiet ahead of the Fed. The S&P 500 is now 29 trading days “textbook overbought” and indeed so through 44 of the past 48; the “live” P/E (futs-adj’d) is at this instant 48.4x; technically, the daily Parabolics on the March Spoo are into their fourth Short day, and the 12hr MACD continues to sink, now at its lowest level since the negative crossover was confirmed from 09 December; and by Market Values, the Spoo in (real-time) is +163 points above it smooth valuation line; the other four primary BEGOS Markets are reasonably near their own like metric. Even as inflation is increasing, the Fed is expected to cut its Funds Rate by -25bps, the FOMC Policy Statement due at 19:00 GMT, prior to which the Econ Baro receives November’s Housing Starts/Permits and Q3’s Current Account Balance.

17 December 2024 – 08:16 Central Euro Time

Copper is presently below its Neutral Zone for today; the balance of the BEGOS Markets are within same, and volatility is again light. Per our MoneyFlow page, the S&P 500 has received substantive inflow across all three of our time measures (weekly, monthly. quarterly): the inference thus is bullish for the S&P; however, ’tis so overcooked to this point both fundamentally and technically that some degree of downside hoovering awaits; perhaps ’twill be a “sell the priced-in” Fed announcement tomorrow; as noted yesterday, the Spoo’s daily Parabolics have just flipped to Short. For the Econ Baro today we’ve December’s NAHB Housing Index, November’s Retail Sales and IndProd/CapUtil, plus October’s Business Inventories.

16 December 2024 – 08:37 Central Euro Time

The busy week begins with the Swiss Franc at present the sole BEGOS Market outside (above) its Neutral Zone for today; session volatility is light. The Gold Update graphically depicts last week’s “Spike n’ Sink”, price initially driven up geopolitically and on the CPI, then back down on the PPI and a bit of Fed doubt; highlighted therein is inflation being back on the increase, the Dollar in turn getting the bid throughout last week. As to notions of an S&P 500 “Santa Claus Rally”, across the past 44 years for these seven trading days leading up to Christmas ’tis not occurred in 13 of them (i.e. ’tis not automatic); indeed the Spoo’s daily Parabolics flipped to Short effective today’s open. Cac volume for the Spoo is rolling from December into that for March, and for Oil from January into February. For the Econ Baro there are 19 metrics due this the week, 10 of which arrive prior to Wednesday’s FOMC Policy Statement; today brings December’s NY State Empire Index.

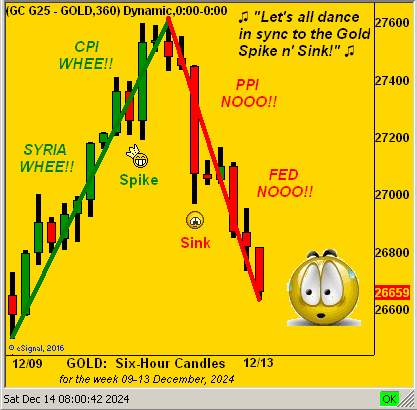

The Gold Update: No. 787 – (14 December 2024) – “Gold Does the Spike n’ Sink”

Thus into a very busy “Fed Week” we go during which 19 metrics come due for the Econ Baro, 10 that are scheduled prior to the FOMC’s Policy Statement late Wednesday. Since the FinMedia have assured us the Fed will cut, is that already priced into Gold? But then again, hearsay has it the Bank come 29 January shall “pause” post-Santa Claus; so hold any applause.

And always make sure you’ve some Gold in your claws!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

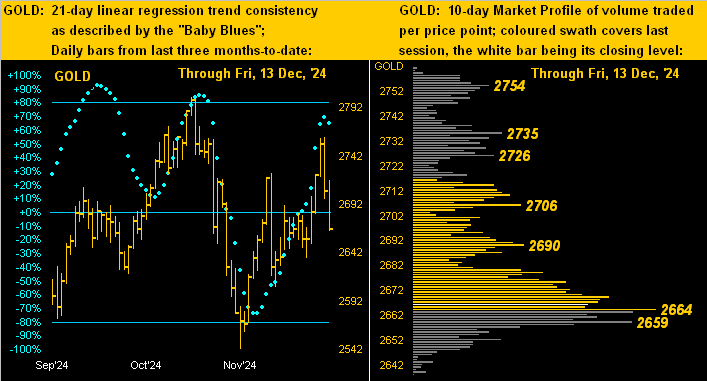

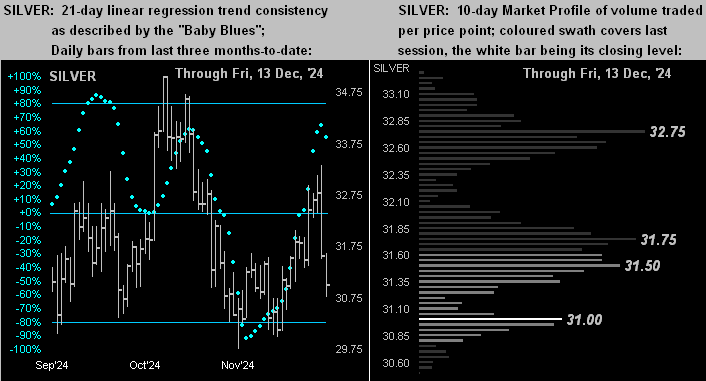

13 December 2024 – 08:24 Central Euro Time

All eight BEGOS Markets are presently within today’s Neutral Zones, and volatility is very light. The Yen’s Long signal herein cited on 03 December is provisionally failing: ’tis based upon the daily Price Oscillator dominating the Market Rhythms for pure swing consistency (on a 24-test basis); such signal would now swing to Short. The S&P 500 yesterday produced a “Hobson Close” in settling on its low level for the session: this last occurred on 26 August 2022, following which the S&P some seven weeks later was down by more than -13%, albeit we don’t give such events predictive shrift, whereas the futs-adj’d “live” P/E for the S&P is an unsustainable 46.4x. ‘Tis rollover for the currencies from the December cacs to those for March. And the Econ Baro wraps its week with November’s Ex/Im Prices.

12 December 2024 – 08:20 Central Euro Time

The Euro, Silver and Copper are at present all above their respective Neutral Zones for today; none of the other BEGOS Markets are below same, and volatility is mostly light. Yesterday’s +0.8% rise in the S&P 500 is “media-credited” to the CPI — whilst yet again above the Fed’s desired pace — having met “expectations” in turn “guaranteeing” a rate cut come the FOMC’s 18 December Policy Statement; (yes, ’tis nonsensical). Looking at current correlations amongst the five primary BEGOS components, the best is negative between the Euro and Oil; notably, Oil yesterday confirmed a close above its Market Magnet, suggestive of still higher prices near-term, perhaps a breakout above the mid-71s top from two weeks ago. Included in today’s incoming Econ Baro metrics we’ve November’s wholesale inflation reads per the PPI.

11 December 2024 – 08:40 Central Euro Time

Both the Euro and Swiss Franc are presently below today’s Neutral Zones; none of the other BEGOS Markets are above same, and volatility is mostly moderate, save for the Spoo, for which the EDTR (see Market Ranges) has been been swiftly narrowing: two weeks ago ’twas 67 points, today ’tis set for 47 points. Looking at Market Rhythms, on a 10-test basis the consistency swing leader is Silver’s 8hr Price Oscillator, followed by the non-BEGOS Yen’s daily Parabolics which flipped to Short effective today’s open, counter to the Yen’s daily Price Oscillator: that study on the 24-test basis is Long. The Econ Baro gets its first dose of November’s inflation data at the retail level via the CPI; too, late in the session comes the month’s Treasury Budget.

10 December 2024 – 08:40 Central Euro Time

Gold is the sole BEGOS Market outside (above) its Neutral Zone for today; session volatility for the BEGOS Markets is quite light. Gold has been getting a bid as the week unfolds, albeit ‘twould “appear” to be geopolitically-driven: as you regular readers know, such impetus for Gold rallies generally sees price return back down from whence it initially came; again, the parabolic weekly trend for Gold remains Short. As to the Spoo, its 12hr MACD confirmed a negative crossover effective today’s open: this has been an excellent Market Rhythm for the the Spoo with the last 10 such crossovers (to Long or Short) all following-through with at least an additional 76 points; thus basis the March cac (which opened today at 6134) a move down to at least 6058 would be reasonable, barring first an all-time high above 6179. The Econ Baro awaits the revisions to Q3’s Productivity and Unit Labor Costs.

09 December 2024 – 08:24 Central Euro Time

At present we’ve the Euro below its Neutral Zone for today, whilst above same is Gold; BEGOS Markets’ volatility is light-to-moderate. The Gold Update cites the narrowing of price’s trading range such that ’tis anticipated the current parabolic Short trend shall carry on for at least another week; provided as well is evidence of the S&P 500’s extreme “textbook overbought” condition, both technically and fundamentally. Amongst Market Rhythms, we’re minding the Spoo’s 12hr MACD as ’tis been a solid signaling performer from August-to-date: its next stance would be from Long-to-Short within a day or two, barring price resuming its upside breakout. Metrics are due every day this week for the Econ Baro, starting today with October’s Wholesale Inventories.

The Gold Update: No. 786 – (07 December 2024) – “Gold Boring; S&P Warning”

“But mmb, you said at the beginning something about a 26% fall in the S&P…”

So here’s the skinny, Squire.

Going away back to the days of AvidTrader (and indeed by this measure since the year 1980), when the S&P 500 gets a bit far afield from itself — either up or down — we quantitatively couch it as mildly, moderately or extremely “textbook overbought” or “textbook oversold”.

Through yesterday’s (Friday’s) S&P 500 settle at 6090, ’twas the eighth consecutive day of being extremely “textbook overbought”. And across the past 45 calendar years, on a mutually-exclusive basis, such eight-day run has only occurred 14 other times. Doesn’t sound like much right?

But wait, there’s more: the last time this current condition came to fruition was in November 2021 from which the S&P’s fall within one year was -26%, (inclusive of recession fears — and the Econ Baro today is significantly lower than ’twas then). The prior occurrence came in 2019 from which the fall within one year was -25%, (inclusive of the 2020 COVID mini-crash).

And yet the inevitable next time ’round, a like percentage drop might actually be considered small. Why? Don’t forget: had COVID never happened, the S&P today would at best be around 3000 and all would be as happy as clams. Instead, today ’tis at 6000 with the honestly-calculated price/earnings ratio now 46.9x, which is double the norm, and triple what was taught as “acceptable” in B-school. For you WestPalmBeachers down there, that means company earnings haven’t increased commensurate with stocks prices. To wit we update this closing graphic of the S&P 500 across the past 50 years with the extrapolated regression channel had COVID never happened. Fortunately however, earnings are no longer meaningful for stocks’ pricing:

‘Course, your “expert” all-in equites money manager has the appropriate protection in place, right? (Pssst … and given the current $53T market cap of the S&P is supported by a liquid U.S. money supply of “only” $22T, broker-issued IOUs will be made available, right?)

“Got Gold?”

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

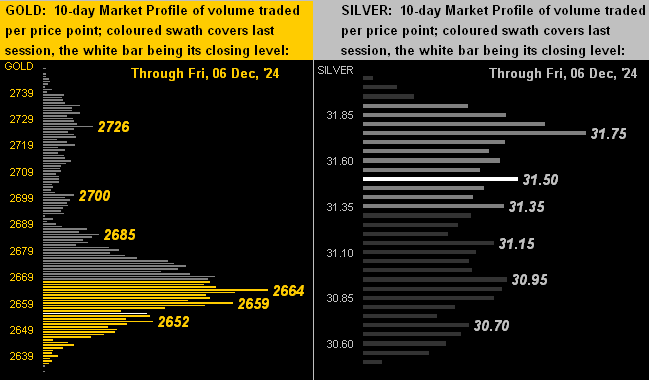

06 December 2024 – 08:43 Central Euro Time

Presently, all eight BEGOS Markets are within their respective Neutral Zones for today, and volatility to this point of the session is light-to-moderate. The Metals Triumvirate is thus far getting the most play, the EDTR (see Market Ranges) tracings being 68% for Silver, 71% for Copper and 77% for Gold. As anticipated, both the Euro and Swiss Franc have moved higher since their “Baby Blues” (see Market Trends) climbed above their -80% axes coming out of last week. And going ’round the Market Values horn for the five primary BEGOS components we’ve (in real-time) the Bond as better than +3 points “high” above its smooth valuation line, the Euro -0.012 points “low”, Gold -20 points “low”, Oil -1.43 points “low” and the Spoo +229 points high. The S&P 500 has been at an “extreme” level of being “textbook overbought” now for seven consecutive trading days, a condition not seen since early November 2021, following which the Index “corrected” by better than -22% over the ensuing eight months. The Econ Baro concludes its week with December’s UofM Sentiment Survey, November’s Payrolls and late in the session October’s Consumer Credit.

05 December 2024 – 08:27 Central Euro Time

The Euro is the sole BEGOS Market outside (above) its Neutral Zone for today; session volatility is very light. Gold’s 12hr Parabolics flipped to Long effective today’s open: of the 405 Market Rhythms run each evening, this one ranks in the top ten and has produced a minimum of 17 points of follow-through (either Long or Short) in nine of the past 10 signals; of course, the more dominant weekly Parabolic trend remains Short; too, (inclusive of real-time), Gold’s 21-day linear regression trend is neutral, its “Baby Blues” (see Market Trends) smack on their 0% axis, but themselves rising. For the S&P 500, its “live” (futs-adj’d) P/E is now 46.6x, the Index now overbought through 35 of the past 39 trading days, and at our “extreme” level through the past six. Today’s incoming metrics for the Econ Baro include November’s Trade Deficit.

04 December 2024 – 08:36 Central Euro Time

At present, all eight BEGOS Markets are within their respective Neutral Zones for today, and session volatility is light. In looking at Market Ranges, notably narrowing of late include those for the Bond, Silver, Copper, Oil, and to some extent the Spoo. As to Market Rhythms’ pure swing consistency, on a 10-test basis the current leaders are Oil’s 15mn Moneyflow, Silver’s 1hr MACD and 8hr Price Oscillator, plus the non-BEGOS Yen’s daily Parabolics; on a 24-test basis the current best are Gold’s 2hr MACD, and as has been mentioned in multiple commentaries, the non-BEGOS Yen’s daily Price Oscillator. The Econ Baro looks to November’s ADP Employment data, ISM(Svc) Index and October’s Factory Orders. Then late in the session comes the Fed’s Tan Tome.

03 December 2024 – 08:42 Central Euro Time

At present below today’s Neutral Zones are the Bond and Swiss Franc; above same are Silver and Copper, and session volatility is light-to-moderate. The non-BEGOS Yen’s daily Price Oscillator — which has be dominating the top of our Market Rhythms runs on a 24-test basis for pure swing consistency — confirmed flipping from Short to Long at today’s open: currently 0.0066815, ‘twould be well within historical performance range to see an ascent up to at least .0068940 into year-end; (the average full swing duration of this Rhythm over the past three years is some seven trading weeks). Also for currencies, just as yesterday we cited the Swiss Franc’s having (by Market Trends) its “Baby Blues” cross above the key -80% axis, so too now has that measure for the Euro; the Dollar’s weakening over the past two weeks looks to further strengthen these attendant currencies. ‘Tis a quiet day for the Econ Baro which yesterday benefitted by both the ISM(Mfg) Index and Construction Spending.

02 December 2024 – 08:32 Central Euro Time

Save for Oil, ’tis a red start to December for the seven other BEGOS Markets, each one (except for the mildly negative Spoo) at present below their respective Neutral Zones for today; volatility is firmly moderate, likely pushing toward robust as the day unfolds. The S&P 500’s “textbook overbought” stance is at our “extreme” reading: indeed ’tis been overbought for 17 consecutive trading days and in total for 32 of the last 36; the “live” (futs-adj’d) P/E is presently a whopping 45.5x and the yield 1.228%; that annualized for the risk-free 3-month T-Bill is 4.373%. On Friday, the Swiss Franc’s “Baby Blues” (see Market Trends) confirmed crossing above the key -80% axis, indicative of still higher prices: currently 1.1327, a near-term push to at least 1.1442 wouldn’t be untoward. The Econ Baro begins December with November’s ISM(Mfg) Index and October’s Construction Spending.

29 November 2024 – 08:48 Central Euro Time

The two-day abbreviated session for the BEGOS Markets continues with just the Swiss Franc at present outside (below) its Neutral Zone; volatility for the combined session is moderate. Of note from our Market Magnets page, those for both the Euro and Swiss Franc have been price penetrated to the upside, whilst for Gold to the downside: such penetrations are indicative of continued near-term direction. The Spoo suggests a higher open for the S&P 500, its “textbook overbought” streak to be further extended. Early BEGOS Market’s closures are as follows (all GMT): the Bond 18:15, EuroCurrencies 19:45, Metals Triumvirate 19:45, Oil 19:45, and the Spoo 19:15. As stated in the still current edition of The Gold Update, tomorrow’s edition shall be quite brief given our writing remotely this time ’round.

28 November 2024 – 08:26 Central Euro Time

Whilst StateSide ’tis the Thanksgiving holiday, the BEGOS Markets are active for two abbreviated sessions combined into Friday settlement. And at present below their Neutral Zones are the Euro, Swiss Franc and Silver; the balance of the components are within same, and volatility is light. Going ’round the Market Values horn of the five primary BEGOS elements, we’ve (in real-time) the Bond as some +1.2 points “high” above its smooth valuation line, the Euro -0.018 points “low”, Gold as -51 points “low, Oil as -1.24 points “low” and the Spoo as 206 points “high”. Yesterday, the S&P 500 completed its 16th consecutive trading days as “textbook overbought”, indeed its 31st of the past 35. Today’s GLOBEX trading halts commence from 18:00 GMT for the Spoo through the usual 22:00 GMT for the currencies.

27 November 2024 – 08:02 Central Euro Time

Save for the mildly lower Euro, Oil and Spoo, the balance of the BEGOS Markets are higher; notably above their Neutral Zones at present are the Swiss Franc and Metals Triumvirate; session volatility is light ahead of a large load of incoming EconData. Our top two current Market rhythms for pure swing consistency are (on a 10-test basis) Copper’s 15mn Parabolics and Silver’s 8hr Price Oscillator; too (on a 24-test basis) remains the non-BEGOS Yen’s daily Price Oscillator, plus Gold’s 30mn Price Oscillator. StateSide, ’tis the final full trading day of the week. And for the Econ Baro, incoming metrics today include October’s Personal Income/Spending, “Fed-favoured” Core PCE Prices Index, Durables Orders and Pending Home Sales, plus the second peek at Q3 GDP.

26 November 2024 – 08:30 Central Euro Time

Presently, all eight BEGOS Markets are in the red and all (save for the Bond) below today’s Neutral Zones; volatility is mostly moderate. The S&P 500 continues its “textbook overbought” stance: however, yesterday’s MoneyFlow belied the Index’s up day of +0.3%, citing it ought instead have been -2.0%; the MoneyFlow of the S&P is a leading indicator (see The S&P 500, MoneyFlow); the three most negative cap-weighted outflows came from NVDA, TSLA and NFLX; indeed, the outflow from NVDA was sufficient for it to lose top spot in the largest cap-weighted constituents (see too Valuations & Rankings). The best directional correlation amongst the five primary BEGOS Markets currently is positive between Gold and Oil. The Econ Baro awaits November’s Consumer Confidence and October’s New Home Sales. Also late in the session we’ve the FOMC Minutes from the 06-07 November meeting.

25 November 2024 – 08:32 Central Euro Time

All eight BEGOS Markets are at present outside of their respective Neutral Zones for today: above are the Bond, Euro, Swiss Franc, Copper and Spoo; below are Gold, Silver and Oil; session volatility is moderate-to-robust. Gold has already given back as much as 38% of last week’s +151 points gain: The Gold Update highlights Gold’s stellar week as nonetheless a contra-trend rally within the fresh weekly parabolic Short trend; key to assess this week shall be Wednesday’s PCE data for October; too, Gold is whipsawing ’round its smooth valuation line (see Market Values), today having crossed back below it. Well up thus far today is the Bond: we’d of late written our anticipation of a such a move, notably as the Bond’s “Baby Blues” (see Market Trends) have twice crossed above their -80% axis since 11 November. And Q3 Earnings Season concluded on Friday, the sub-par performance seeing 64% of S&P 500 constituents bettering their bottom lines over Q3 a year ago: the average such improvement since 2017 is 66%, and ex-COVID, 68%. The “live” (futs adj’d) P/E of the S&P is presently 44.9x.

The Gold Update: No. 784 – (23 November 2024) – “Gold’s Contra-Trend Rally; S&P’s Earnings(less) Tally”

So into the StateSide Thanksgiving week we go: 11 metrics come due for the Econ Baro, including 10 packed into Monday through Wednesday, the PCE data surely to get the lion’s share of interest.

Moreover: we’ve this heads-up for next Saturday’s edition of The Gold Update. We shall be once again “in motion”, this time through the treasured beauty of Tuscany. Thus akin to the occasional “Gold in 60 Seconds”, next week’s piece shall be quite brief. True, ’tis is a month-end edition, normally graphics-rich. However, we’ll like save most of those for the ensuing 07 December missive. Either way, Gold’s reaction to next Wednesday’s PCE shall be key.

As we thus prepare to embark for Golden Tuscany, ensure your tally totals a Golden Destiny!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

22 November 2024 – 08:32 Central Euro Time

Both Gold and Silver are at present above today’s Neutral Zones, whilst below same is Copper; the balance of the BEGOS Markets are calm, and session volatility remains light to this point. Gold has had a firm contra-trend rally this week even as the weekly parabolic trend just flipped from Long-to-Short a week ago: more of course in tomorrow’s 784th consecutive Saturday edition of The Gold Update. At Market Trends, the sole BEGOS component with a positive linreg is the Spoo. The S&P’s “textbook overbought” streak continues, the sub-par Q3 Earnings Season (which concludes today) in turn maintaining a stratospherically high “live” P/E of 45.4x (futs-adj’d for real-time). Bitcoin appears poised to tap 100,000 today, (high 99,820). And the Econ Baro concludes its quiet week with the monthly revision to November’s UofM Sentiment Survey.

21 November 2024 – 08:38 Central Euro Time

Both Gold and Silver are at present above their respective Neutral Zones for today, whilst below same is the Spoo; volatility is again light. Looking at Market Values in real-time for the five primary BEGOS Markets, we’ve the Bond as -1.50 points “low” vis-à-vis its smooth valuation line, the Euro -0.024 points “low”, Gold -16 points “low”, Oil -0.99 points “low” and the Spoo +131 points “high”. The S&P 500 is now 11 consecutive trading days “textbook overbought” and further is 26 days as such across the past 30. The “Baby Blues” (see Market Trends) for the Precious Metals are starting to curl upward, albeit their linregs remain well negative. And for the Econ Baro, incoming metrics include November’s Philly Fed Index, plus October’s Existing Home Sales and Leading (i.e. “Lagging”) Indicators.

20 November 2024 – 08:38 Central Euro Time

Save for Oil and the Spoo, the other six BEGOS Markets are lower, notably with the Bond, Euro, Swiss Franc, Gold and Silver at present below today’s Neutral Zones; the Spoo is above same, and volatility is light. The Bond’s “Baby Blues” (see Market Trends) have — for the second time in as many weeks — moved above their key -80% axis: thus we look to still higher Bond prices near-term following Friday’s low of 115^09 (present price is 116^12). In looking at Market Rhythms, on a 10-test basis our current leaders for pure swing consistency are Oil’s 8hr Moneyflow, Silver’s 8hr Price Oscillator and the Spoo’s 1hr Moneyflow; the lone leader on a 24-test basis continues to the non-BEGOS Yen’s daily Price Oscillator. Nothing is due today for the Econ Baro. And with the “live” futs-adj’d P/E of the S&P now 45.2x, we’ve three days left to run in this sub-par Q3 Earnings Season.

19 November 2024 – 08:21 Central Euro Time

The Euro is at present below its Neutral Zone for today, whilst above same is Gold; ’tis a bit ironic given our best current correlation amongst the five primary BEGOS Markets is positive between the Euro and Gold, albeit market dynamics continually shift; session volatility is quite light. Gold has moved back above 2600, however our anticipated move lower into the 2400s remains very viable, the weekly parabolic trend being newly Short along with the negative MACD crossover; still, Gold has cleared the 2615 handle which by the Market Profile is the most dominantly-traded price of the past fortnight; mind, too, Gold’s price vis-à-vis its smooth valuation line (see Market Values): in real-time, price is presently -57 points “low”. Meanwhile, the S&P 500 continues its “textbook overbought” streak, the “live” futs-adj’d P/E now 44.8x. The Econ Baro looks to October’s Housing Starts/Permits.

18 November 2024 – 08:01 Central Euro Time

At present, all eight BEGOS Markets are in the black, with the Metals Triumvirate and Spoo currently above their respective Neutral Zones for today; session volatility is mostly moderate. The Gold Update acknowledges our anticipated pullback in price, with potentially lower levels at least near-term as the weekly MACD confirmed a negative crossing at week’s close such that the upper 2400s would not be untoward. For the Spoo, price on Friday confirmed piercing to the downside its Market Magnet, suggestive of still lower levels; by Market Values (in real-time), the Spoo shows as +140 points “high”; and despite last week’s selling, the S&P 500 itself remains “textbook overbought” through 23 of the past 27 trading days; the futs-adj’d “live” P/E is presently 44.0x. For the Econ Baro ’tis a fairly light week, beginning today with November’s NAHB Housing Index. And Q3 Earnings Season continues into its final week.

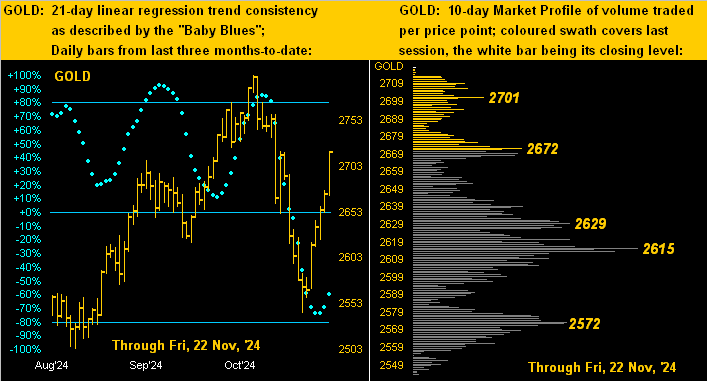

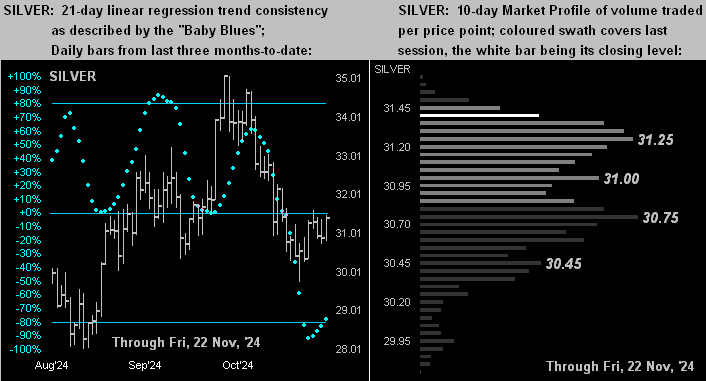

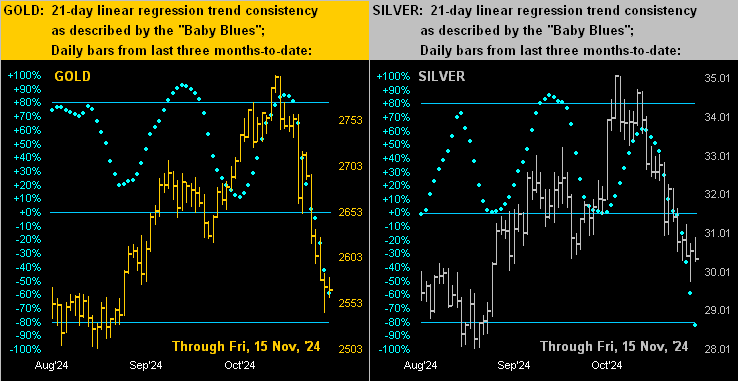

The Gold Update: No. 783 – (16 November 2024) – “ ‘Tis No Surprise, Gold’s Current Demise ”

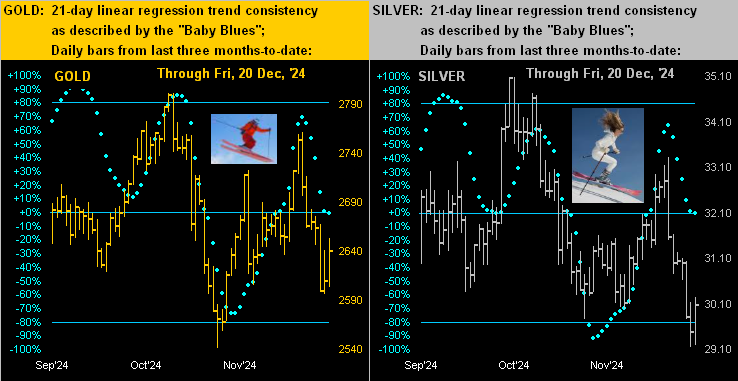

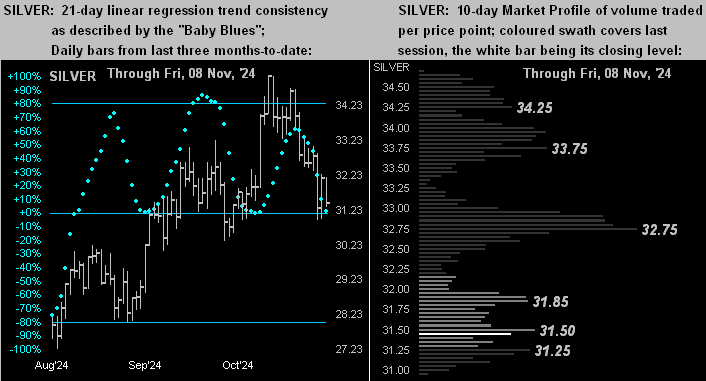

Further as noted, when the Buck gets the bids, “everything else” goes on the skids, including ‘natch the precious metals. ‘Tis not the happiest of two-panel displays, but here next are the last three months-to-date of daily bars for Gold on the left and for Silver on the right, along with their respective baby blue dots of trend consistency. Cue our lead (pun intended) conductor with ![]() “Follow the Blues instead of the news, else lose yer shoes…“

“Follow the Blues instead of the news, else lose yer shoes…“![]() :

:

And so to wrap, let’s go with The Stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3740

Gold’s All-Time Intra-Day High: 2802 (30 October 2024)

2024’s High: 2802 (30 October 2024)

The Weekly Parabolic Price to flip Long: 2802

Gold’s All-Time Closing High: 2799 (30 October 2024)

10-Session “volume-weighted” average price magnet: 2656

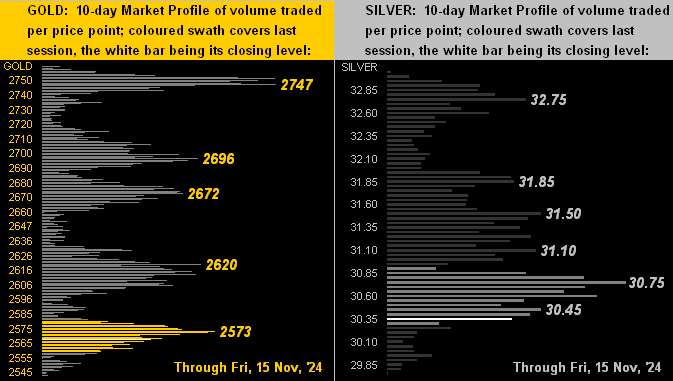

Trading Resistance: notable Profile nodes 2573 / 2620 / 2672 / 2696 / 2474

Gold Currently: 2567, (expected daily trading range [“EDTR”]: 43 points)

10-Session directional range: down to 2542 (from 2759) = -253 points or -7.9%

Trading Support: none notable per the Profile

The 300-Day Moving Average: 2268 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

‘Tis a fairly light, ensuing week for incoming Econ Baro metrics, the most attention-getting one to be the Conference Board’s compiled negative reading of October’s Leading Indicators, (which as led by the Baro we instead refer to as “Lagging”). Too, ’tis the final week of Q3 Earnings Season, which as you know (should you follow its page and/or read the Prescient Commentary) is sub-par compared to average quarterly year-over-year improvement. But as we’ve quite a bit quipped, earnings today are irrelevant to equities’ investing: else the S&P 500 would be at but half its current level.

Otherwise, notwithstanding some further near-term demise, Gold remains ever so cheap for the wise … the bottom line thus being:

Got Gold? Don’t be a chicken! Get yourself some real nuggets and win!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

15 November 2024 – 08:26 Central Euro Time

Ahead of a significant load of incoming Econ Baro data, we find the BEGOS Markets fairly mixed, the Euro and Swiss Franc at present above today’s Neutral Zones, whilst below same are Oil and the Spoo; session volatility is mostly moderate. Yesterday the S&P 500 — even being down — posted its 22nd of the past 26 trading days as “textbook overbought”; specific to the Spoo, (for which its all-time high is 6053 per this past Monday), price appears on a downward bent to at least test the prior 17 October high of 5927; the Spoo’s daily MACD seems headed for a negative crossing early into the ensuing week, although by Market Trends, the Spoo’s “Baby Blues” still are in ascent. Again, we’re extending our coverage of Q3 Earnings Season an extra week: thus far for the S&P, 65% of bottom lines have been better over Q3 of a year ago: that is a below-average rate of improvement. Of note, Gold yesterday reached down to the “average” adversity level of 2555 that was mused in last Saturday’s Gold Update; tomorrow brings edition No. 783. And as to the busy Baro, it looks to November’s NY State Empire Index, October’s Retail Sales, Ex/Im Prices and IndProd/CapUtil, plus September’s Business Inventories.

14 November 2024 – 08:16 Central Euro Time

‘Tis red across the board for all eight BEGOS Markets, albeit not at present below today’s Neutral Zones are both the Bond and Oil; volatility is mostly moderate. Our best current correlation amongst the five primary BEGOS components is positive between the Bond and Euro. The S&P 500 yesterday reached our “extreme” level of being “textbook overbought”, meaning price has become excessively high by its BollBands, RSI and Stochastics; and the Spoo in real-time is +228 points above its smooth valuation line (see Market Values); too by Market Trends, the Spoo is the sole market (of all eight) sporting a positive 21-day linear regression trend. The Dollar Index today has reached its firmest level (106.695) since 01 November 2023. And included in today’s incoming metrics for the Econ Baro we’ve October’s wholesale inflation (PPI), expectations there for an increase over the September data by both the headline and core readings.

13 November 2024 – 08:08 Central Euro Time

We’ve at present the Euro, Swiss Franc, Copper and Spoo all below today’s Neutral Zones; none of the other BEGOS Markets are above same, and volatility is light. The buying into the S&P 500 of late has been substantive given our MoneyFlow page: both the one week and one month differentials are positive, whilst the quarterly measure has significantly reduced its negative stance; ‘course the Index nonetheless remains vastly overvalued both fundamentally (lack of supportive earnings) and certainly so near-term (technically). Our BEGOS Market Rhythms’ leaders for best swing consistency are (on a 10-test basis) Oil’s 8hr Moneyflow, the Euro’s 30mn Moneyflow, and for Silver its 8hr and 2hr Price Oscillators, plus its 1hr Moneyflow; too (on a 24-test basis) we’ve still the non-BEGOS Yen’s daily Price Oscillator, along with Copper’s 30mn Parabolics. And October’s retail inflation (CPI) comes due for the Econ Baro as well as (purportedly) the month’s Treasury Budget.

12 November 2024 – 08:29 Central Euro Time

The elements of the EuroCurrencies and Metals Triumvirate all are at present below their respective Neutral Zones for today; the other BEGOS Markets are within same, and volatility is pushing toward moderate. As anticipated through recent weeks, Gold finally let go yesterday to the downside: price’s intra-day drop by both points (-76) and percentage (-2.8%) ranked fifth-weakest year-to-date. In turn, Gold’s weekly parabolic trend has provisionally flipped from Long to Short, whilst price has moved below its smooth valuation line (see Market Values). That for the Spoo is (in real-time) +247 points above same: the S&P 500 itself with its “live” P/E of 46.4x is now “textbook overbought” through 19 days of the past 23. We’re extending our coverage of Q3 earnings out an additional week (through 22 November) given some key constituent S&P stragglers still therein to report. Again the Econ Baro is quiet today with 14 metrics due Wednesday through Friday.

11 November 2024 – 08:33 Central Euro Time

The week’s underway with — at present — the Euro, Swiss Franc and Gold below today’s Neutral Zones; above same is the Spoo, and volatility is light. The Gold Update points to two pending negative crossings for price: should it pierce sub-2650 this week, the weekly parabolic Long trend shall flip to Short; and by Market Values, Gold in real-time is only +13 points above today’s smooth valuation line, the penetration of which then would also suggest lower levels near-term. Too, in real-time, Silver’s “Baby Blues” (see Market Trends) have provisionally moved below their 0% axis, with those for Gold within a day or so of doing same, barring a firm rally. The Econ Baro is quiet both today and tomorrow, the balance of the week highlighted by metrics for inflation and retail sales. And ’tis the final week of an on-balance below-par Q3 Earnings Season for the S&P 500, for which the “live” P/E (futs-adj’d) is presently 46.7x.

The Gold Update: No. 782 – (09 November 2024) – “Gold Trumped, Dumped”

The good news is — even upon Gold’s weekly parabolic trend eventually flipping from Long to Short — that the prior three such Short stints (since the week ending 29 September 2023) have each been but three weeks in duration: that’s it. The intervening Long trends respectively have lasted 17 weeks, 16 weeks, and the current one now 17 weeks. Perhaps a bit too much perfection there, but as crooned Steve “The Joker” Miller back in ’73 ![]() “I get my lovin’ on the run“

“I get my lovin’ on the run“![]() and certainly for Gold, such a run ’tis been!

and certainly for Gold, such a run ’tis been!

As for the StateSide economy, ’tis been on balance rather run down, albeit the Economic Barometer has bounced and since stabilized from its August low. You tell ’em there, Jay:

Trumped if not dumped, in sum, we analytically expect both Gold and Silver to weather this near-term dip. Either way, your key with them clearly is to maintain a Presidential grip!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

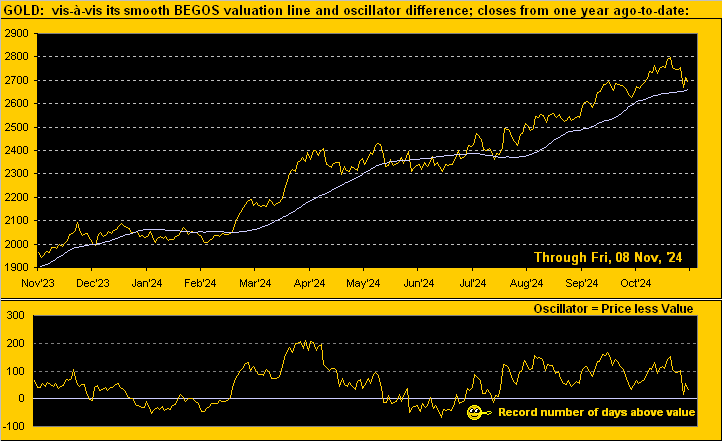

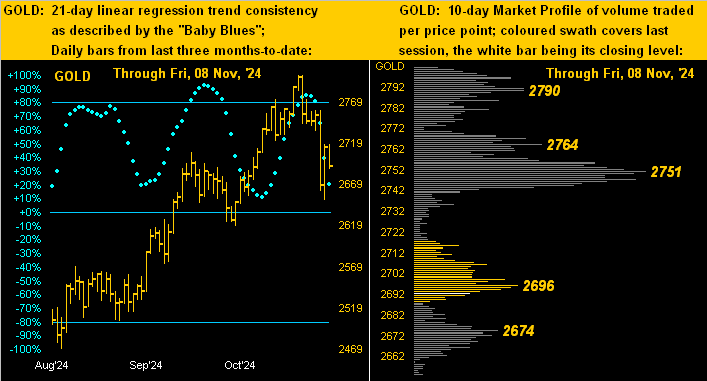

08 November 2024 – 08:39 Central Euro Time

Early on, down is the watchword across the BEGOS Markets, the sole exception being the Bond +1 pip; otherwise, only the Swiss Franc and Spoo are not at present below today’s Neutral Zones, and volatility is pushing toward moderate. With one week plus a day to run in Q3 Earnings Season, 65% of the S&P 500’s constituent’s have bettered their bottom lines from Q3 a year ago, which across the past seven years (ex-COVID’s 2020 quarters) is below the 68% improvement average. The futs-adj’d “live” P/E of the S&P at this instant is 44.4x and the yield 1.234%; the three-month U.S. T-Bill’s annualized yield is 4.420%. The Spoo, now over 6000, is by Market Values (in real-time) +226 points above its smooth valuation line. And the S&P itself is now “textbook overbought” through 17 of the past 21 trading days. The Econ Baro rounds out its week with November’s UofM Sentiment Survey.

07 November 2024 – 08:44 Central Euro Time

The BEGOS Markets are returning to a more orderly condition post-election: at present above their respective Neutral Zones for today are the Bond, Euro, Swiss Franc and Copper; the balance of the bunch are within same, and volatility — after having been extremely robust — is now moderate. Yesterday, Gold’s “Baby Blues” confirmed settling below their key +80% axis, suggestive of further near-term selling from which (as you regular readers know) had been an ongoing near-term overvalued stance: indeed by Market Values, Gold (in real-time) is but +14 points “high” above its smooth valuation line, the penetration of which would also suggest further downside, all of which we’ll assess in Saturday’s Gold Update. As for other Market Values’ deviations: the bond shows as nearly -5 points “low”, the Euro -0.018 points, “low”, Oil basically “in-line”, and the Spoo +186 points “high”. The day’s incoming Econ Baro metrics include September’s Wholesale Inventories and Consumer Credit, plus the initial read on Q3 Productivity and Unit Labor Costs. And come 19;00 GMT, the FOMC releases its Policy Statement for which expectations are a -25bp FedFunds rate cut.

06 November 2024 – 08:41 Central Euro Time

As anticipated in yesterday’s comment given the StateSide election, overnight volatility in the BEGOS Markets was both thin and very volatile: the average EDTR (see Market ranges) tracing thus far across the eight BEGOS components is an extreme 216 points. The Spoo is the sole market above today’s Neutral Zone; the other seven components are below same. Were the S&P to open at this instant, ‘twould “instantly” gap to a record-high 5891, (the current all-time high being 5878). By Market Rhythms on a 10-test basis for pure swing consistency, our leaders (through yesterday’s session) are Oil’s 8hr Moneyflow, Silver’s 8hr Price Oscillator, and Copper’s 8hr Moneyflow, (a lot of commonality there for measuring on an 8hr time frame); for the 24-test basis, we still highlight the non-BEGOS Yen’s daily Price Oscillator, plus the Euro’s 15mn MACD. Nothing is due today for the Econ Baro. And the FOMC commences its two-day meeting, their Policy Statement scheduled for release tomorrow.

05 November 2024 – 08:41 Central Euro Time

Both the Euro and Copper are at present above today’s Neutral Zones; below same is Oil, and BEGOS Markets’ volatility is light. In both our Prescient Commentary and the current edition of the Gold Update we’ve anticipated near-term rises for the Euro and Copper, and indeed that has come to pass at least to the point, the impetus being the up movements in their respective “Baby Blues” (see Market Trends) from having been below their -80% axes. Looking at correlations amongst the five primary BEGOS components, the best at present is negative between Oil and the Spoo. For the Econ Baro we’ve October’s ISM(Svc) Index and September’s Trade Deficit. Too, StateSide, ’tis Election Day, after which overnight trading conditions may be quite thin and volatile.

04 November 2024 – 08:01 Central Euro Time

‘Tis black across the board to start the week for all eight BEGOS Markets, with seven of them at present above today’s Neutral Zones, the sole one within being Gold; volatility already is moderate-to-robust with the StateSide election (Tuesday) and FOMC Policy Statement (Thursday) in the week’s balance. The Gold Update continues pointing to the yellow metal being overvalued near-term, yet undervalued long-term; and our inflation table therein highlights the pickup in the “Fed-Favoured” Core PCE Prices Index. By Market Values, Gold (in real-time) is +99 points above its smooth valuation line. Otherwise, ’tis a fairly light week of incoming metrics for the Econ Baro, beginning today with September’s Factory Orders.