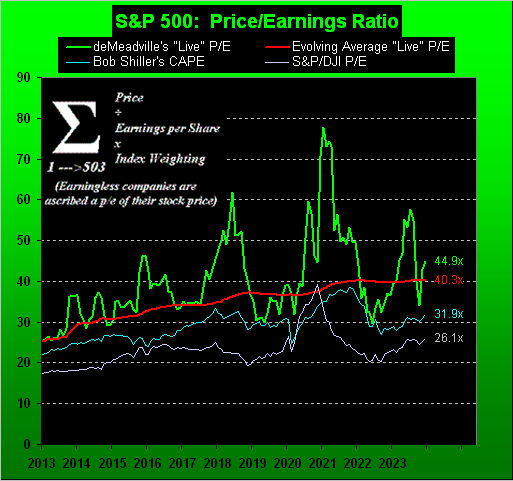

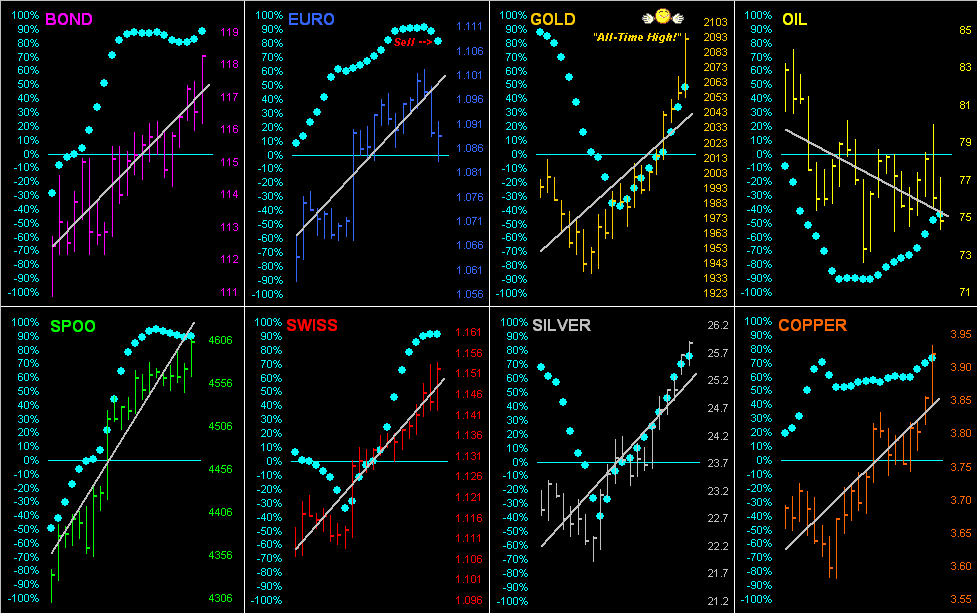

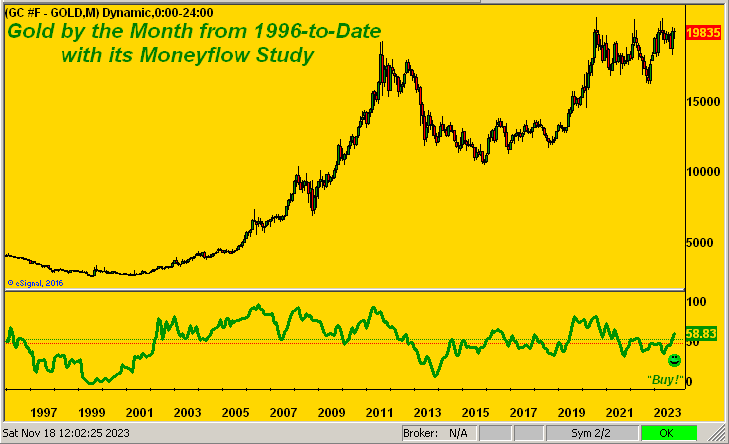

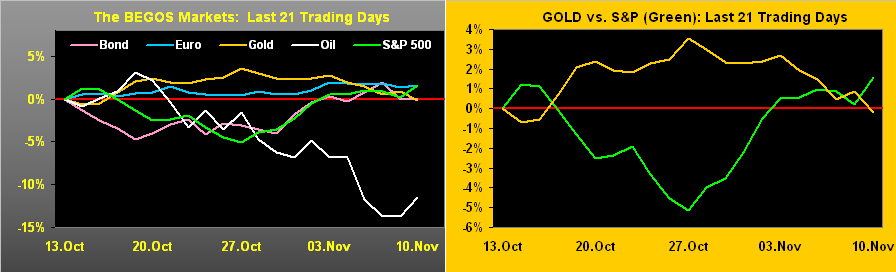

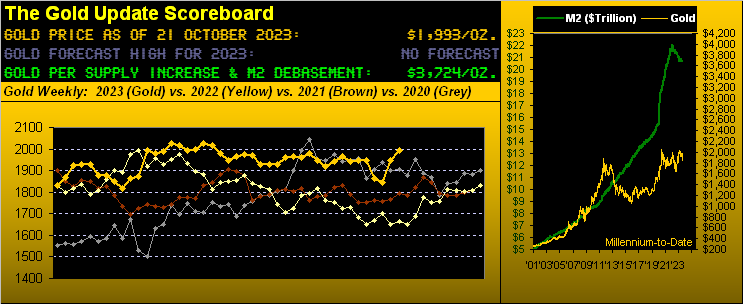

At present we’ve the Bond, Euro and Copper above today’s Neutral Zones; the other BEGOS Markets are within same, and volatility remains light, (save for non-BEGOS Yen which already has traced 121% of its EDTR [see Market Ranges for the BEGOS components]). At Market Ranges we continue to watch for the Bond’s “Baby Blues” to let go to the downside: however, they’ve remained pasted to the ceiling for better than a full month as price continues to rise. The “live” P/E of the S&P 500 (fut’s-adj’d) is 45.8x and the Index’s “textbook oversold” condition now enters its 30th consecutive trading day. The Econ Baro looks to Novembers’ Housing Starts/Permits.

Mark

Mark

18 December 2023 – 08:59 Central Euro Time

Both the Euro and Spoo are at present above their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility is again light. The Gold Update emphasizes the dangerously high level of the S&P 500 by a whole host of measures; whereas Gold itself whilst weathering some post All-Time-High pullback nonetheless remains in a more broadly bullish stance. At Market Rhythms, the most consistent on a 10-test basis is Gold’s 8hr MACD, and a 24-test basis the Yen’s (not yet an official BEGOS Market) 2hr MACD. The Econ Baro begins its busy week (17 incoming metrics!) with December’s NAHB Housing Index.

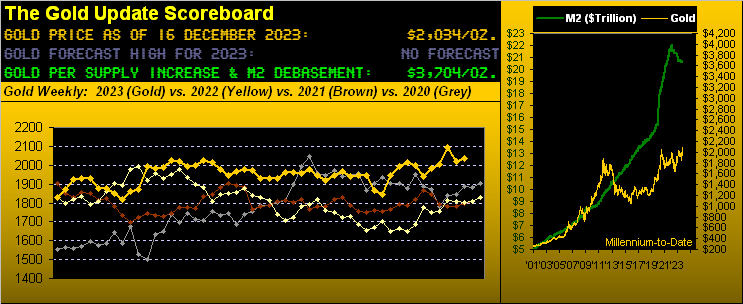

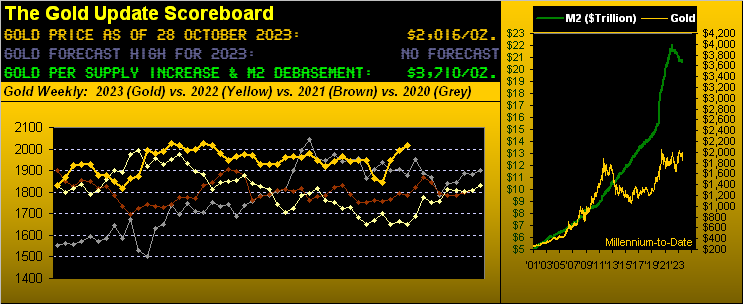

The Gold Update: No. 735 – (16 December 2023) – “Gold’s Upside Fruition; Stocks’ Suicide Mission”

Yes, ’tis The Gold Update, but we’re compelled (as occasionally is our wont) to start with stocks’ suicide mission, given Gold in upside fruition (albeit still vastly undervalued) is doing just fine, thank you very much.

What is with this stock market, eh? As a great friend (with a long stint at basically the very top of a household-name investment bank … but we’ll maintain anonymity in this case) here recently remarked: “The stupidest people on Wall Street are the pension fund managers.”

Ya think? Pros and rubes alike are throwing money like Pavlov’s drooling dogs on steroids into an S&P 500 index that is so beyond overvalued, further adjectives escape us. ‘Course as we’ve tweeted (@deMeadvillePro): mind the website’s S&P 500 MoneyFlow page to assess if the buying actually has substance.

Still, we hear that apps with names like “Robinhood” allow for incredibly easy stock market access such that everyone’s gonna keep on buying and thus stocks shall only go even higher. To us that sounds more like being “robbed in the hood” as when the selling starts, the compounding of such shall overwhelm anything Wall Street and the World have ever seen. Because as you regular readers know: “The money isn’t there.”

By the numbers:

- A dozen years ago in 2011, the market capitalization of the S&P 500 exceeded the U.S. liquid “M2” Money Supply by +29%; as of yesterday, that excess is +100%, the market cap now $41.3T versus an M2 of but $20.7T. (Wanna cause The Crash? Fax that last sentence over to CNBS for all the rubes watching their boob tubes).

- Per yesterday’s (Friday’s) S&P settle at 4719, ’tis precisely -100 points (or just -2.1%) below the all-time intraday high of 4819 set on 04 Janaury 2022; the current “expected daily trading range” for the S&P is now 34 points, meaning a new all-time high can be reached within 3 trading days, just in time for Christmas.

- The number of consecutive trading days the S&P has been “textbook overbought” (a 44-year concoction of John Bollinger’s Bands, along with Relative Strength and Stochastics) is now 28 which is in the 93rd percentile of all such overbought conditions since the year 1980.

- Present all-risk S&P 500 annualized dividend yield: 1.475%. Present no-risk U.S. 3-Month annualized T-Bill yield: 5.225%. (Why is this so hard to grasp?) “Because, mmb, T-Bills aren’t gonna double in price…” Just like stock’s can’t get halved, eh Squire? (‘Preciate the tee-up).

- The “live” price/earnings ratio of the S&P settled the week at 44.9x; that is essentially double the 66-year average P/E of 22.8x (Shiller “CAPE” into deMeadville post-2012) and +77% up from when our “live” deMeadville version was instituted those 11 years ago at 25.4x:

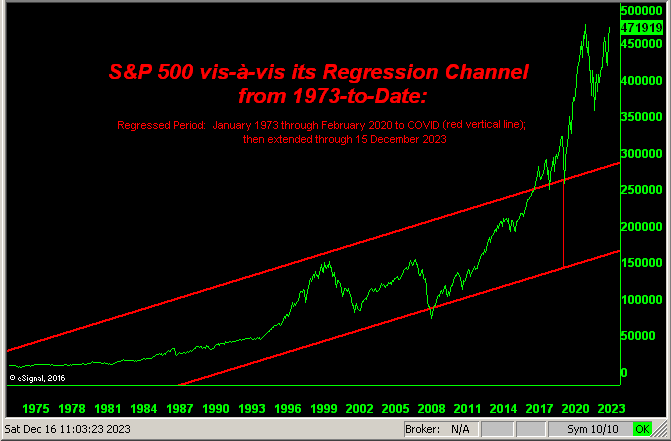

- Next, too, we’ve the S&P’s 50-year regression channel as plotted from 1973 up to COVID (the red vertical line) from which the channel’s trend is extended-to-date, suggesting the S&P “ought” today be at best sub-3000 rather than the current 4719:

By the numbers indeed, the most daunting being lack of price-supportive earnings — and far worse — the lack of money when it all goes wrong.

The good news is: irrespective of the S&P’s ominous (understatement) overvaluation, the market is never wrong. The bad news is: the market always reverts to its broadest measures of mean. And should your use your trusty Pickett slide rule to do such reversion math, an S&P “correction” of -50% wouldn’t be untoward a wit. We merely await the FinMedia coming up with the catalyst, of which there are a multitude from which to choose, (see our 09 July missive that cited “Stocks’ 10 Crash Catalysts”), or to quote Bill Cowper from away back in 1785: “Variety is the spice of life”. And our sense remains “Look Ma! No Money!” shall be the ultimate crash driver. The Federal Reserve can then double the money supply to cover what the investment banks cannot credit to you after having sold your stock, the price of Gold at least doubles beyond where it already “ought” be (see the opening Gold Scoreboard), and on we go.

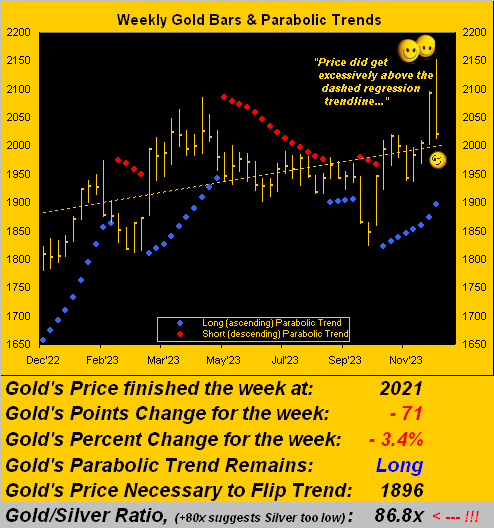

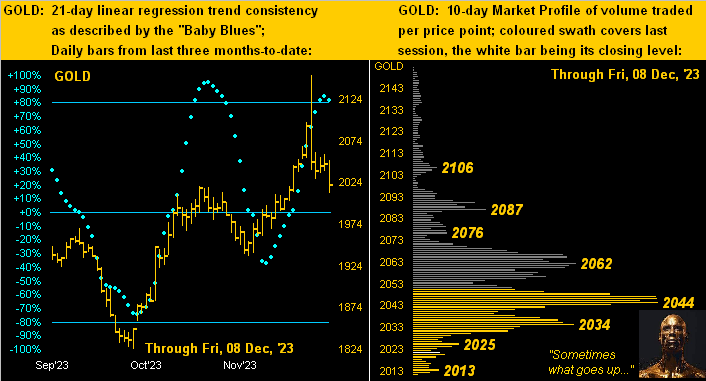

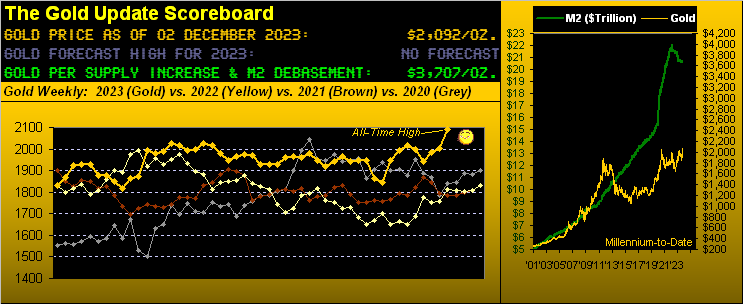

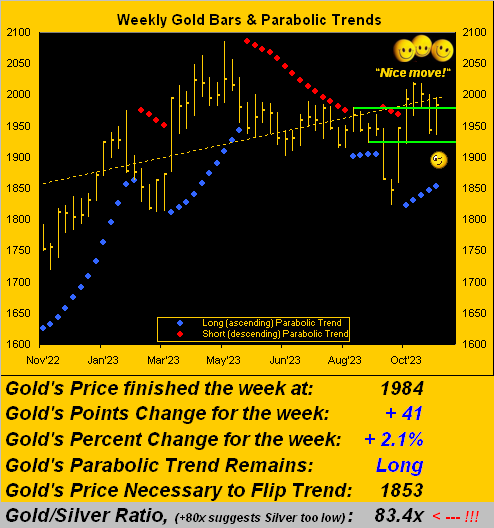

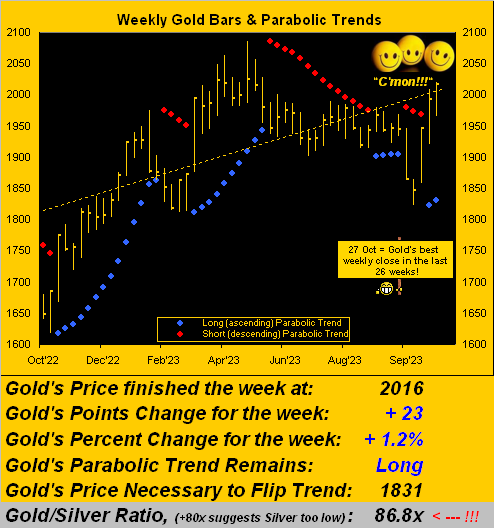

And thus to Gold let’s Go! In settling this past week at 2034, Gold is -118 points below its 04 December All-Time High of 2152. Regardless, price just completed its fourth up week of the last five, such fruition from the foresight to be “in” rather than face being fried upon stocks’ suicide. Here we’ve Gold’s weekly bars from one year ago-to-date, the current parabolic Long trend now nine weeks in duration. But don’t worry, should you deem that as too long: the longest such Long trend this century lasted 26 weeks back in 2005, which was preceded by a like 25-week stint in 2004 and later by a 24-week run in 2019. In fact from the year 2001-to-date, Gold has recorded eight parabolic Long trends of 20 or more weeks. Which is why we say: “When Gold goes, it Goes!” To the graphic with Sly we go:

But wait, there’s more: for can the Economic Barometer also go higher? Hat-tip Media Research Center in canvassing ABC News to discover that we’re wrong, for President Biden’s economy “is really wonderful” … even as the StateSide Treasury Deficit for November alone rocketed +26% “on higher interest costs”. Do we again cue BTO’s ![]() “You Ain’t Seen Nothing Yet”

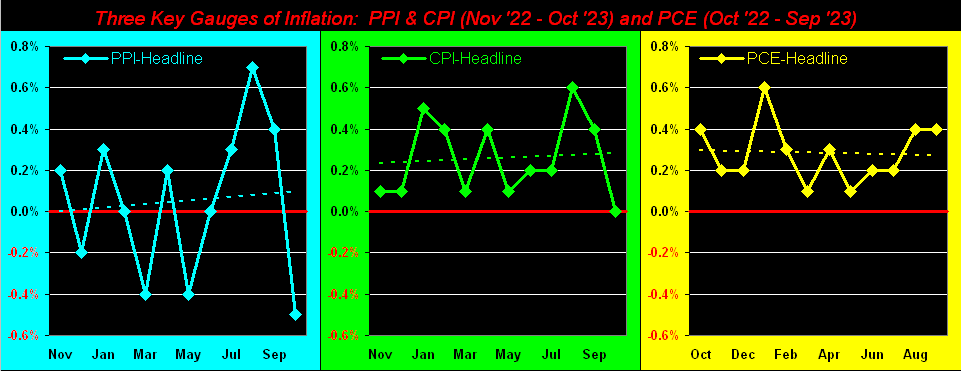

“You Ain’t Seen Nothing Yet”![]() –[’73]? How about the month’s core retail inflation increasing from a +0.2% clip in October to now +0.3%? Fortunately favouring the Fed’s rate cut musings, the New York State Empire Index faceplanted from November’s +9.1 reading to -14.5 for December: “Smunch!” Here’s the Econ Baro representing the whole bunch:

–[’73]? How about the month’s core retail inflation increasing from a +0.2% clip in October to now +0.3%? Fortunately favouring the Fed’s rate cut musings, the New York State Empire Index faceplanted from November’s +9.1 reading to -14.5 for December: “Smunch!” Here’s the Econ Baro representing the whole bunch:

Time we go to wrap with:

The Gold Stack

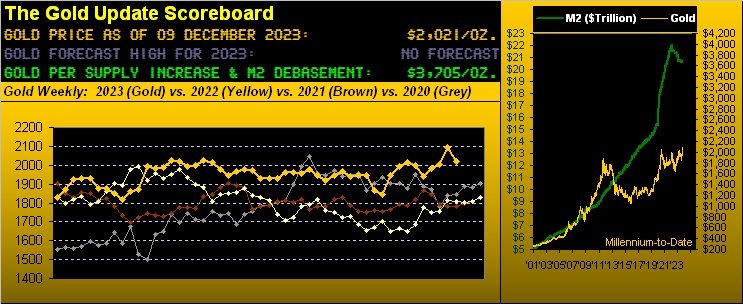

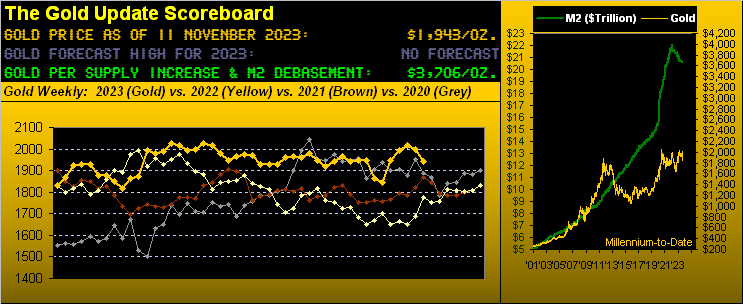

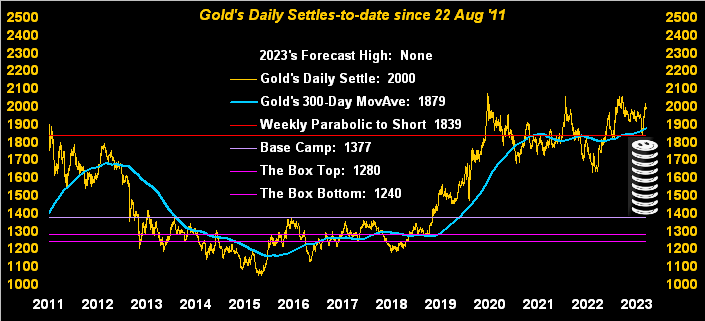

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3704

Gold’s All-Time Intra-Day High: 2152 (04 December 2023)

2023’s High: 2152 (04 December)

Gold’s All-Time Closing High: 2092 (01 December 2023)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar ’22); 2085 (04 May ’23)

Trading Resistance: 2047 / 2087 / 2016

10-Session “volume-weighted” average price magnet: 2042

Gold Currently: 2034, (expected daily trading range [“EDTR”]: 33 points)

Trading Support: 2021 / 2012 / 1997

10-Session directional range: down to 1988 (from 2152) = -164 points or -7.6%

The Weekly Parabolic Price to flip Short: 1917

The 300-Day Moving Average: 1909 and rising

The Gateway to 2000: 1900+

2023’s Low: 1811 (28 February)

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

And please do not fall afoul of the following … ’tis coming:

Go with your Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

15 December 2023 – 09:29 Central Euro Time

The Euro is at present below today’s Neutral Zone whilst above same are both Copper and the Spoo; BEGOS Markets volatility is mostly light. The S&P 500 looks to open at about 4730, some -90 points below the all-time high (4819); the “live” P/E (fut’s-adj’d) is now 45.0x. ‘Tis volume rollover today from December to March for the EuroCurrencies. Looking at Market Values for the five primary BEGOS components: the Bond shows as nearly 9 points “high” above the smooth valuation line; the Euro is about -0.01 points “low”; Gold is +47 points “high”; Oil is -7 points “low”, and the Spoo is (deep breath) +310 points “high”. The Econ Baro wraps its week with December’s NY State Empire Index along with November’s IndProd/CapUtil.

14 December 2023 – 09:07 Central Euro Time

The Bond, Copper and Spoo are at present above today’s Neutral Zones; the other BEGOS Markets are within same, and volatility is moderate. Yesterday’s S&P 500 rally again did not have full MoneyFlow support (Index +1.4% vs. Flow +1.0%); too the S&P is now quite frothy as the Flow factor to move the S&P by 1 point is notably diminishing. Gold’s firm up push yesterday moved our top three Market Rhythms for consistency (10-test basis) as follows (all for Gold): the 12hr Parabolics, 6hr Price Oscillator and same study for 4hr. Oil’s cac volume is moving from January into that for February. The Econ Baro looks to November’s Retail Sales and Ex/Im Prices, plus October’s Business Inventories.

13 December 2023 – 09:13 Central Euro Time

The Bond at present is above today’s Neutral Zone; both Copper and Oil are below same, and BEGOS Markets volatility is again light with the FOMC’s Policy Statement in the balance. The S&P 500 completed its 25th consecutive trading day as “textbook overbought”; the “live” P/E (futs-adj’d) is 44.5x; at 4644, the Index stands -174 points (-3.8%) below its 4819 all-time high (04 January 2022); the Spoo (including the recent +55 points of fresh March premium) is nonetheless +260 points above its smooth valuation line (see Market Values). Ahead of the Fed comes November’s wholesale inflation per the PPI.

12 December 2023 – 09:03 Central Euro Time

We’ve strength this morning in the Bond and EuroCurrencies, with session volatility notably light, save for the Swiss Franc having already traced 53% of its EDTR (see Market Ranges). Both the Swiss Franc and Gold confirmed their “Baby Blues” (see Market Trends) slipping below their +80% axes, suggestive of still lower prices near-term. Despite yesterday’s +0.4% rise in the S&P 500, its MoneyFlow (regressed into S&P points) fell -0.8%, reflected in the developing negative slant we’re seeing at the MoneyFlow page; too, the Index is now “textbook overbought” through the past 24 trading days. The Econ Baro awaits November’s CPI and Treasury Budget.

11 December 2023 – 09:08 Central Euro Time

Save for Oil (+0.6% at 71.67), the other seven BEGOS Markets are all at present in the red; session volatility is light. The Gold Update sees safe downside for the yellow metal toward 1975 without causing any concern for the overall uptrend(s); still by Market Trends, Gold’s “Baby Blues” are in real-time dropping below their key +80 axis, warranting a price move sub-2000. Of greater concern is misfortune in the making for the S&P which remains inanely overextended both fundamentally (unsupportive earnings) and technically (beyond “overbought”). Spoo volume today is rolling from the December cac into that for March, with an additional +52 points of fresh premium. The Econ Baro is quiet, albeit with an ample load of metrics as the balance of the week unfolds.

The Gold Update: No. 734 – (09 December 2023) – “Gold-Record’s Calamity; Stocks’ Stark Misfortune-to-Be”

We’ll close it here with another FinMedia bemusement. The once-mighty now ratings-floundering CNN ran on Gold’s record-high Monday with: “Gold has never been this expensive.” With all due respect to the network’s writers and editorial staff, Gold remains extraordinarily cheap. “Expensive” was back in 2011 when Gold’s price growth was outpacing U.S. Dollar debasement, (recall our then writing about “Gold having gotten ahead of itself”). But for the chump news-droolers out there, the price of Gold last Monday reached its highest level ever at 2152 … yet valued today at 3705, Gold is cheap! What’s inanely “expensive” (understatement) is the stock market. And thus we wrap with this favourite graphic:

Stay with your Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

08 December 2023 – 09:12 Central Euro Time

‘Tis StateSide November Payrolls day for the Econ Baro, and at present seven of the eight BEGOS Markets are within their Neutral Zones, the only outlier being Oil above same; the latter appears trying to firm ’round the 70 handle. Session volatility is light, (except again for the non-BEGOS component Yen which has traced 119% of its EDTR as the BOJ interest rate play continues). The S&P 500 is now “textbook overbought” through the past 22 trading days and the “live” P/E is 43.3x; however, the recent MoneyFlow deterioration has (for the moment) righted itself, indicative of money being thrown at a terrifically expensive stock market. In addition to jobs data, the Baro also looks to December’s UofM Sentiment Survey.

07 December 2023 – 09:11 Central Euro Time

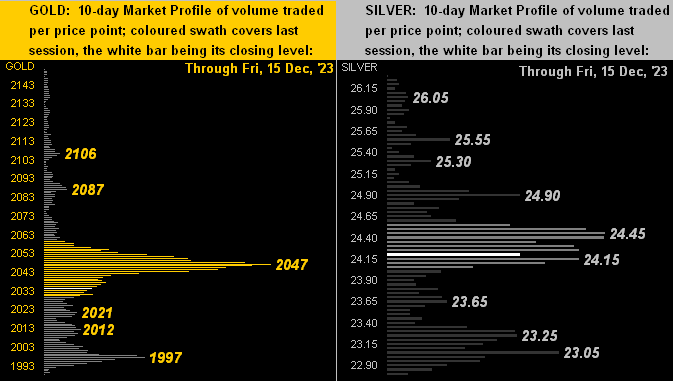

The Bond is at present below its Neutral Zone for today, whilst above same is Copper; BEGOS Markets volatility is again mostly light with the non-BEGOS exception of the Yen which already has traced 145% of its EDTR (see Market Ranges for the standard BEGOS components). Gold has calmed from its wild Monday ride: currently 2047, by the Market Profile we’ve resistance notably in the 2062-2065 zone, with supports right round current price, plus at 2036-2034, 2023 and 2014. A day ahead of Payrolls data for the Econ Baro, today’s metrics include October’s Wholesale Inventories and Consumer Credit.

06 December 2023 – 09:13 Central Euro Time

Gold, Copper and the Spoo are at present above today’s Neutral Zones; the other BEGOS Markets are within same, and volatility is mostly light. Going ’round the horn for the five primary BEGOS components at Market Values, we’ve (in real-time): the Bond +6.5 points “high” above its smooth its smooth valuation line, the Euro “in line”, Gold +57 points “high”, Oil -9.5 points “low” and the Spoo +206 points “high”. The S&P 500 is now “textbook overbought” through the last 20 trading days; the “live” P/E is 42.3x. For the Econ Baro we’ve November’s ADP Employment data, October’s Trade Deficit, and the revision to Q3’s Productivity and Unit Labor Costs.

05 December 2023 – 08:59 Central Euro Time

After achieving an All-Time High yesterday at 2152, Gold’s subsequent -113 intraday points drop ranks 5th-worst century-to-date; however the -5.3% drop ranks just 34th worst intraday. At present, the Euro, Copper and Spoo are below today’s Neutral Zones; none of the other BEGOS Markets are above same, and volatility has returned to mostly light. Our most consistent Market Rhythm at present (10-test swing basis) is Gold’s 4hr Price Oscillator. As anticipated, the Euro’s “Baby Blues” (see Market Trends) confirmed falling below the key +80% axis, indicative of lower prices near-term. And the Econ Baro looks to November’s ISM(Svc) Index.

04 December 2023 – 09:12 Central Euro Time

After setting an All-Time High on Friday (to 2096, settle 2092), Gold spiked overnight some +50 points, only to since return below Friday’s settle. At present ’tis red across the board for all eight BEGOS Markets, and volatility is robust. More details on to where the yellow metal can go near-to-medium term in The Gold Update, (which too outlines the case for an S&P “crash”). Note at the website the S&P 500 Moneyflow differential beginning to weaken, oft a precursor to lower price levels. Due for the Econ Baro is October’s Factory Orders.

The Gold Update: No. 733 – (02 December 2023) – “Gold: Finally!”

If you caught last Tuesday’s tweet (@deMeadvillePro, Gold then 2042) you saw where this was going: “Santa clearly is contemplating a new all-time Gold high by Christmas. ‘Twould be 2075 spot a/o 2089 FebFuts. (On verra…)”

And so for Gold, as the expression goes, “Santa came early this year.” In settling the week yesterday (Friday) at 2092, February Gold (the current “front month”) en route traded to as high as 2096, +7 points above the prior “front month” 2089 All-Time High that had been in place since 07 August 2020. Spot Gold, too, exceeded its prior All-Time High of 2074 in trading as high as 2076. Finally! ‘Tis a beautiful thing.

‘Course, you astute readers of The Gold Update fully realize that this year we did not forecast a specific high price, (which for you WestPalmBeachers down there is why the above Gold Scoreboard has stated “No Forecast” throughout 2023). Nonetheless, early in the year we expressed our anticipation of Gold by year-end at least achieving a new All-Time High: ![]() “Whoomp! (There It Is)”

“Whoomp! (There It Is)”![]() –[Tag Team, ’93]

–[Tag Team, ’93]

To wit, as herein penned back on New Year’s Day: “…how do we forecast a high for 2023? Linearly we don’t … as for uncharted territory above Gold’s All-Time High (2089 of 07 August 2020) that’s for the Fibonacci-obsessed.”

True, we from time-to-time dabble in “fib retracement” for establishing trading targets. However, we avoid the Sybilistic art of future “fib extension”: for us ’tis too Timothy Leary, to whom President Nixon in ’70 purportedly referred as “the most dangerous man in America”, (only to then to nix the Gold standard a year later). That from the “Now Look Who’s Talkin’ Dept.” … but we digress.

Given Gold’s fresh All-Time High is finally in hand, let’s take a realistic crack at “How high from here?” for the yellow metal. After all, new highs in major financial markets tend to draw in the “mo-mo” crowd, albeit for Gold, its notorious triple top across the past three years ain’t drawn squat. And let’s be honest: Gold’s new high at present is marginal at best.

“But it’s only been one day, mmb…”

‘Twouldn’t be a landmark missive without our beloved Squire. Still, such marginal high can cue the Gold Shorts, which from the “Party Pooper Dept.” may swiftly remind us that following the aforementioned 2089 high came the 2079 high on 08 March 2022 and then the 2085 high this past 04 May. Thus in the Shorts’ words, “There’s nothing to see here” in their anticipation of it again all going wrong for Gold.

Yet as we’ve oft quipped of late, “triple tops are meant to be broken”. And marginally or otherwise, that just happened. Moreover as herein penned one week ago regarding December’s monthly net changes: “…the last six [have been]: +2.6%, +4.5%, +3.4%, +6.4%, +2.9% and +3.8% from 2017 through 2022 respectively…” That is an average net December change of +3.9%, which from November’s 2056 futures settle would bring 2136 by New Year.

But wait, there’s optimistically more. Century-to-date Gold has recorded 5,767 trading days, 252 of which have elicited All-Time Highs. Now obviously it doesn’t “feel” like Gold averages a new high every 23 trading days: indeed therein the standard deviation is 155 days, the longest stint between All-Time Highs being 2,237 days from 06 September 2011 to 27 July 2020 (whew!) even as the U.S. Money Supply (“M2”) simultaneously increased +90.2% (whoa!)

Nevertheless to our point: for those 252 All-Time High days, the average maximum increase in the price of Gold within the enusing three months is +8.9%; or if you prefer, the median maximum price increase is +7.9%. Either way, “in that vacuum” from the present 2092 level would put Gold in the 2257-2278 range by February’s end, (just in case you’re scoring at home). ‘Course, hardly is “average” reality, but it at least gives us some measure of reasonable upside guidance for Gold through these next three months.

Of greater import however is that Gold’s new high remains peanuts vis-à-vis its currency debasement valuation, depicted in the opening Scoreboard as now 3707, i.e. +77% above here, even accounting for the increase in the supply of Gold itself. Which got us to question: how long does it typically take for the price of Gold to double? Here’s the answer from one price’s “century mark” to the next:

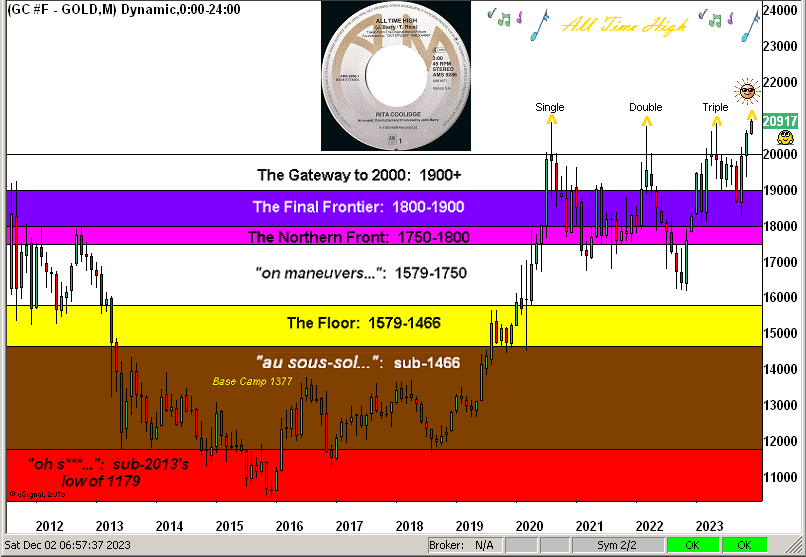

Naturally it being month-end plus a December day, here is Gold’s Structure by the monthly bars for the past 12 years. And yes, Virginia, just as there is a Santa Claus, so too as noted are triple tops meant to be broken. Et voilà. Thus in turn Gold is at an![]() “All Time High”

“All Time High”![]() –[Rita Coolidge, ’83]:

–[Rita Coolidge, ’83]:

To wrap this rather epic edition of The Gold Update, “We have breaking news…”

“Bring it on, mmb…”

Thank you, Squire. Direct from the “We’re Completely Gobsmacked Dept.” here ’tis:

Last evening we were all eyes on Gold when at precisely 18:28 GMT price recorded the new All-Time High of 2089.3, surpassing 2089.2 which as you well-know had been in place as the prior high since 07 August 2020. Some three-and-one-half hours later at 22:00 GMT price settled also at an All-Time Closing High of 2091.7.

Curious as to how our FinMedia friends would portray this great event, we went to Bloomy’s home page, obviously expecting it to be the lead story. But it wasn’t there. Worse, it was no where to be found their home page! So we instead zoomed over to Dow Jones Newswires’ Marketwatch home page. It must be at the top, right? Wrong! Rather, the lead stories were on “The Dow”, “Bitcoin” and “GameStop”. Where is the Gold story? We enabled a MW home page search for “Gold”: first find was Goldman; second find was again Goldman; third find was “Gold” … buried deep down the page amongst the “click-bait” ads for chumps, with the barest of mention of the new high.

But we really and truly learned something from this: Gold now is of no material media importance whatsoever. Who cares, right? The sad part is: when they finally figure it out (upon everyone morphing from marked-to-market millionaires to marked-to-reality impoverisheds) ’twill be too late.

Still, perhaps the late Leary would have gotten it:

“But his was of the Acapulco type, mmb…”

Likely the case there, Squire. As for the real thing, ’tis at an All-Time High and yet it remains unspeakably undervalued. That’s really all you need to know.

Got Gold? Got Silver? Got a wealth-preserved Future!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

01 December 2023 – 09:16 Central Euro Time

All eight BEGOS Markets are at present within their respective Neutral Zones for today, and volatility is light. Gold appears rather hesitant just below record-high territory: FedFuts are 2060; the record high is 2089; but by Market Values, price is (in real-time) +73 points above its smooth valuation line; still by Market Trends, Gold is firmly in an uptrend, the “Baby Blues” therein continuing to climb; again a comprehensive assessment in tomorrow’s Gold Update. The S&P 500 is now “textbook overbought” through 17 consecutive trading sessions: the “live” P/E is a futs-adj’d 43.0x. The Econ Baro concludes its week with November’s ISM(Mfg) Index and October’s Construction Spending.

30 November 2023 – 09:21 Central Euro Time

At present, just Copper is the only BEGOS Market outside (above) its Neutral Zone for today; volatility again is light-to-moderate. As tweeted (@deMeadvillePro) on Tuesday: “Santa clearly is contemplating a new all-time Gold high by Christmas. ‘Twould be 2075 spot a/o 2089 FebFuts. (On verra…)” Price since has reached 2073 (FebFuts); more in this coming Saturday edition of the Gold Update. Looking at Market Rhythms, the most consistent at present are (on a 10-test basis) the Yen’s (not yet an official BEGOS component) 1hr Price Oscillator and 2hr Moneyflow, and Gold’s 4hr Price Oscillator; on a 24-test basis we’ve the Yen’s 15mn MACD along with Gold’s 30mn MACD and 30mn Price Oscillator. ‘Tis a busy day for the Econ Baro, including November’s Chi PMI, plus October’s Pending Home Sales, Personal Income/Spending, and the “Fed-favoured” Core PCE Index.

29 November 2023 – 09:17 Central Euro Time

The Bond is the sole BEGOS Market at present outside (above) its Neutral Zone; session volatility is light-to-moderate. After flipping from Long-to-Short, the Bond’s daily parabolics whip-sawed back to Long: however, we’re minding the Bond’s “Baby Blues” (see Market Trends) for their breaking below the key +80% axis. Going ’round the Market Values horn for the primary BEGOS components, in real-time we’ve the Bond nearly +6 points “high” above the smooth valuation line, the Euro +0.0316 points “high”, Gold +64 points “high”, Oil -7.17 points “low”, and the Spoo a whopping +253 points “high”. The Econ Baro awaits the second peek at Q3 GDP. And late in the session comes the Fed’s Tan Tome.

28 November 2023 – 09:15 Central Euro Time

All eight BEGOS Markets are at present within their respective Neutral Zones for today; session volatility is light. Gold’s cac volume is rolling from December into February, with +20 points of premium; other rollovers in process include Silver, Copper and the Bond, all from December into March. As anticipated, the Bond’s “Baby Blues” (see Market Trends) are teasing their +80% axis: confirmation below that level is suggestive of weaker prices near-term; too, the Bond’s daily Parabolics confirmed flipping from Long to Short effective today’s open. For the Econ Baro we’ve November’s Consumer Confidence.

27 November 2023 – 09:17 Central Euro Time

Both Gold and Silver are at present above today’s Neutral Zones: the white metal, (which has been lagging Gold’s performance), has provisionally flipped its weekly parabolic from Short to Long; confirmation should come at next Friday’s settle. The Spoo is at present below its Neutral Zone. And BEGOS Markets volatility is again moderate. The “textbook overbought” streak of the S&P itself is now through 13 sessions. The Gold Update (brief as planned) is price-bullish, especially given the yellow metal having recorded net gains for the six past Decembers. The Econ Baro starts a week of 12 incoming metrics with October’s New Home Sales.

The Gold Update: No. 732 – (25 November 2023) – “Basking Under Gold”

So there we are ever so briefly — yet hopefully saliently — for this week. Mind too your favourite Gold information at the website: simple select “Gold” under the BEGOS Markets menu and all the price-leading information is there: Gold’s Market Value, Trend, Profile, Magnet, Range, and the currently-highlighted Market Rhythm featuring the 12-hour parabolic study. We’ll therefore see you in a week’s time with the usual graphics-rich end-of-month edition. Until then:

Bask under your Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

24 November 2023 – 08:35 Central Euro Time

The second day of the otherwise abbreviated trading session finds the Bond at present below its Neutral Zone; the rest of the BEGOS Markets are within same, and volatility is moderate. The Bond’s “Baby Blues” appear poised to begin their descent in the ensuing week; and by Market Values, the Bond in real-time is nearly +5 points above its smooth valuation line. As for the Spoo, ’tis +265 points above same, and the fut’s-adj’d live P/E of the S&P is 44.2x. We’ve early closures today across all the components and the Econ Baro is complete for the week.

22 November 2023 – 07:13 Central Euro Time

Just brief and early this morning, (our going into motion across the next few days): only Copper is at present outside (below) its Neutral Zone for today; BEGOS Markets volatility is light. Yesterday’s S&P 500’s down move nonetheless maintains a “textbook overbought” rating for the Index, however now “moderate” rather than “extreme”; (such condition can take days, even weeks, to unravel). And metrics to close out the week for the Econ Baro include October’s Durable Orders. Happy T-Day to you StateSiders and fellow USAers ’round the globe.

21 November 2023 – 09:22 Central Euro Time

The Bond, Swiss Franc, Gold and Silver are all at present above their respective Neutral Zones for today; the other BEGOS Markets are within same, and volatility is leaning toward moderate, (the non-BEGOS Yen having again exceeded 100% of its Expected Daily Trading Range). The S&P 500 is now “textbook overbought” through the past 10 sessions, the last five of which are at an extreme overbought reading: the “live” P/E (futs-adj’d) is 44.7x, essentially double the 66-year historical mean. The Econ Baro awaits October’s Existing Home Sales; and late in the session comes the FOMC’s 31 Oct/01 Nov meeting minutes.

20 November 2023 – 09:17 Central Euro Time

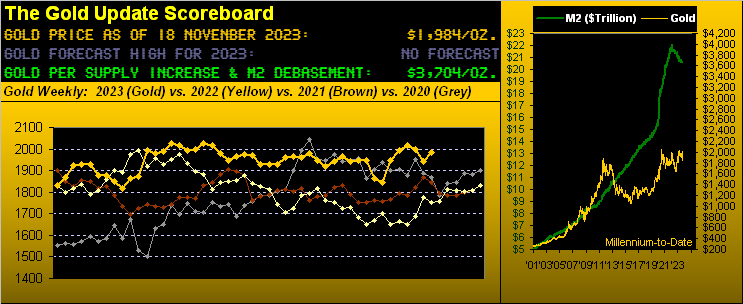

The abbreviated trading week gets going with the Swiss Franc and Oil at present above today’s Neutral Zone; below same is the Bond: recall our noting to mind the Bond’s “Baby Blues” (at either the Bond or Market Trends page); the Blues in real-time are beginning to roll over (albeit still are above their key +80% level). BEGOS Markets volatility is moderate; indeed for the Yen (not yet officially a BEGOS component), it has already traced 120% of its EDTR (see Market Ranges). The Gold Update cites price having moved back above successfully tested support, in concert with inflation having purportedly come to a halt and the Econ Baro recording its 10th worse 12-day stint since the Baro’s inception back in 1998. The Baro today looks to October’s leading (i.e. “lagging”) indicators, one of just five metrics due for this week.

The Gold Update: No. 731 – (18 November 2023) – “Gold Pops as Inflation Stops and the Economy Flops”

In sum, Gold again has a chance to go for an All-Time High. The S&P by any and all rights is due for a dive (understatement). And certainly both “ought be” similarly priced right ’round “3000” … at least if you do the math. (What a rare concept, eh?)

We’ll close it here with this logistical note:

Next week’s 732nd consecutive Saturday edition of The Gold Update is planned to be quite brief as we shall be “in motion”: just straight to the point with a salient graphic or two along with our view. In any event, don’t be a turkey, given what can ensue…

…rather, keep your eyes (and wealth) on the Golden prize clearly due!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

17 November 2023 – 08:57 Central Euro Time

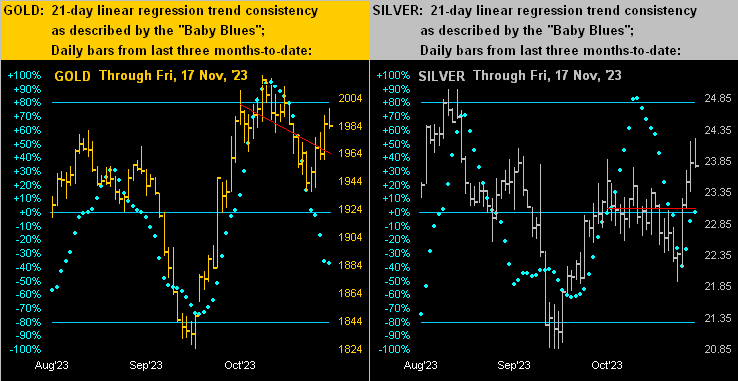

‘Twould appear to be a quiet Friday in the making: all eight BEGOS Markets are at present within their respective Neutral Zones, and volatility is very light. October’s Housing Starts/Permits come due for the Econ Baro, which itself has had quite the torrid week (https://demeadville.com/economic-barometer/); more on that in tomorrow’s 731st edition of The Gold Update. In real-time at Market Trends, the 21-day linreg trends are now perfectly flat for both the Swiss Franc and Silver, (the latter nonetheless getting a boost from the aforementioned daily Parabolics having flipped to Long). ‘Tis the final day of Q3 Earnings Season, for which the S&P 500 constituents finds 64% having improved their bottom lines of a year ago.

16 November 2023 – 08:58 Central Euro Time

Both the Bond and Gold are at present above today’s Neutral Zones; the rest of the BEGOS Markets are within same, and volatility is mostly light ahead of a busy day for incoming EconData. Silver’s daily Parabolics flipped to Long effective today’s open (23.510): the average maximum follow-though of the past 10 such studies (either Long or Short) is 1.695 points. At Market Trends, the Bond’s “Baby Blues” are above the key +80% axis; upon their eventual decline below that level, we’d then anticipate lower price levels. Included amongst today’s seven incoming metrics for the Econ Baro are November’s Philly Fed and NAHB Housing Indices, along with October’s Ex/Im Prices and IndProd/Cap/Util.

15 November 2023 – 08:59 Central Euro Time

October’s CPI indeed was “center stage” (per yesterday’s comment), the headline retail level coming in “unch”. In turn the Dollar dove and the BEGOS Markets unimpededly rose. Today ahead of wholesale inflation we’ve both Gold and Silver at present above their respective Neutral Zones for today; the other BEGOS components are within same, and volatility is light. Yesterday’s S&P 500 +1.9% rise now finds the Spoo (in real-time) +216 points above its smooth valuation line (see Market Values): historically such extreme deviation leads on average to price descending by well over -100 points within the ensuing weeks such that we may soon see the S&P below where ’twas prior to the inflation data (4411 vs. now 4491); too there’s the “live” P/E of the S&P now 44.9x. Overall today for the Econ Baro we’ve November’s NY State Empire Index, October’s PPI and Retail Sales, plus September’s Business Inventories.

14 November 2023 – 09:08 Central Euro Time

The Bond is the sole BEGOS Market at present outside (above) its Neutral Zone for today; session volatility is very light, the Econ Baro awaiting October’s CPI to take center stage. Heading our Market Rhythms for trading consistency are (on a 10-test basis) the Euro’s daily Moneyflow, Oil’s 30mn Parabolics and Silver’s daily Parabolics, (too, whilst not a BEGOS component, the Yen’s 1hr Moneyflow also qualifies). The “live” (futs-adj’d) p/e of the S&P 500 is now 42.9x and the yield 1.569% whereas that for the “riskless” U.S. three-month T-Bill is an annualized 5.260%. And in real-time, the Spoo is +127 points above its smooth valuation line, the S&P itself now “textbook overbought” through the past five sessions.

13 November 2023 – 09:04 Central Euro Time

Both Silver and Oil are at present below today’s Neutral Zones; above same is Copper, and BEGOS Markets volatility is pushing toward moderate. The Gold Update confirms our anticipated typical post-geopolitical price pullback: visually therein on the Weekly Bars graphic we’ve placed the 1980-1922 support structure, (expandable to 2001-1901 if need be); and in real-time, Gold is now just +35 points above its smooth valuation line (see Market Values) after having been some +120 points above it. ‘Tis a very busy week for the Econ Baro with 18 metrics due, beginning (again purportedly) today with October’s Treasury Budget. Too, ’tis the final week of a “so-so at best” Q3 Earnings Season.

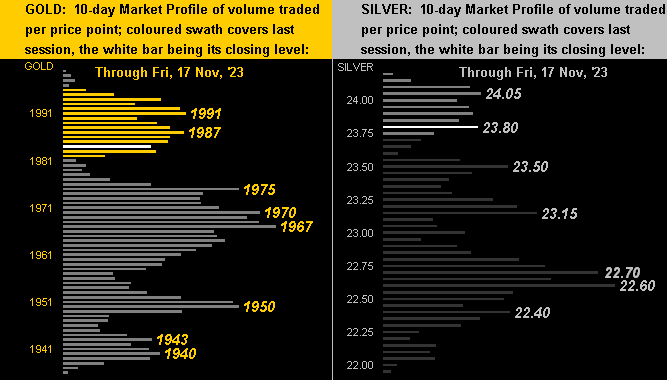

The Gold Update: No. 730 – (11 November 2023) – “Gold’s Bang-On-Time Dive”

“But mmb, those PPI annualized percents are in line with the Fed’s target…”

Duly noted, Squire. If that Producer Price Index is truly leading, then we ought see the other inflation percents stall, if not fall, although the Fed does have a lean toward those Core Personal Consumption Expenditures. As well, Minneapolis FedPrez Neel “Cash n’ Carry” Kashkari per Dow Jones Newswires “…is not convinced rate hikes are over…” Or to reprise the great Bonnie Raitt from back in ’88: ![]() “It’s just too soon to tell…”

“It’s just too soon to tell…”![]()

In the midst of all this, we read the Fed’s interest-rate increases of the past two years being deemed as “historic”. Again, the Fed’s Effective Funds Rate is presently 5.33% (i.e. the targeted 5.25% + 5.50% ÷ 2). Hardly is that “historic”. Anyone remember the Prime Rate at 22% back in 1980? We do. (What would be today’s FinMedia adjective for that? “Steroidic”?)

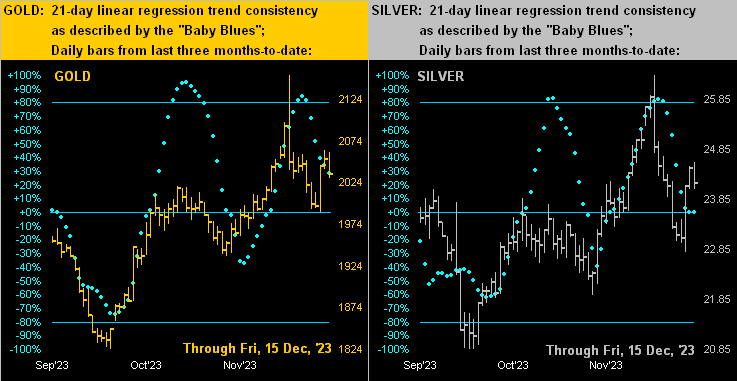

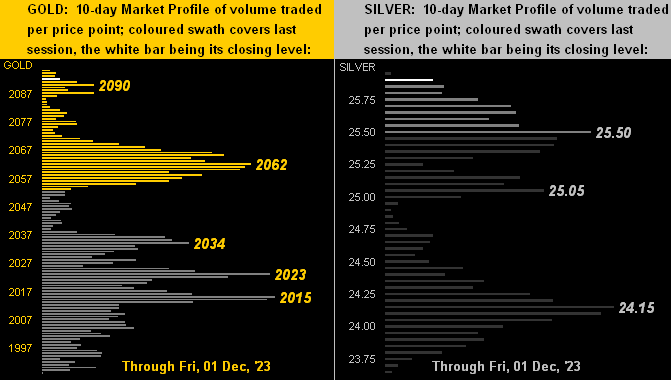

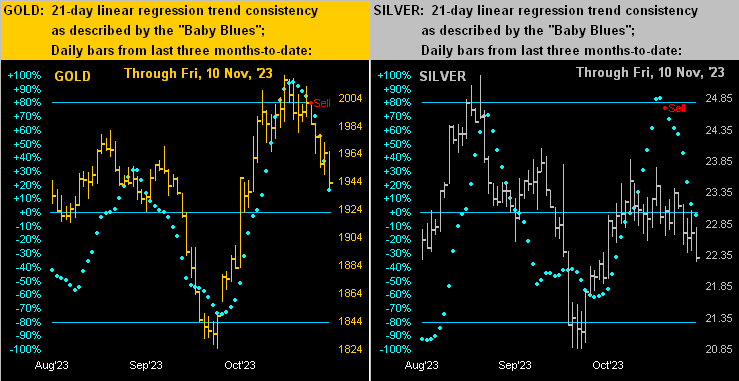

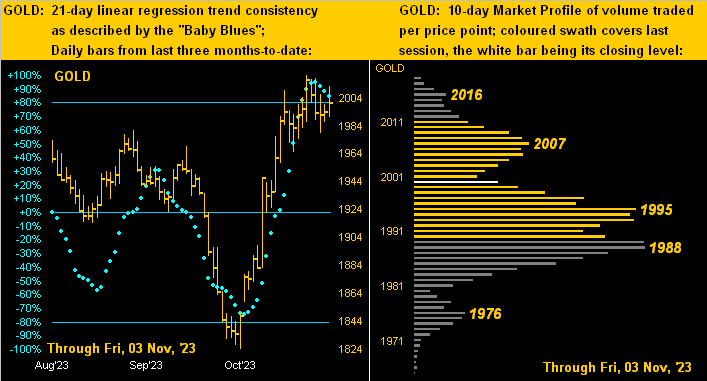

Specific to the precious metals this past week, a more apt adjective would be “atrophic” as next we’ve the two-panel display of Gold’s daily bars for the past three months-to-date at left and same for Silver at right. As aforementioned for Oil, here we’ve the “Baby Blues” signaling “Sell” in both metals’ current cases upon the dots having slipped below their respective +80% axes. Again we commend “The trend is your friend” even if it must descend:

Indeed with respect to Gold, we tweeted (@deMeadvillePro) this graphic last Monday, reflective of the “Baby Blues” heading south:

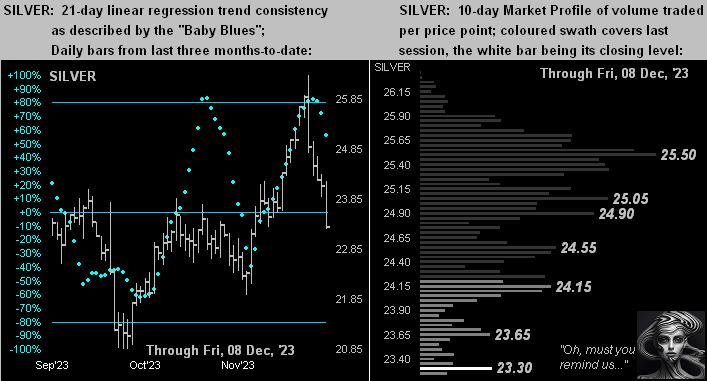

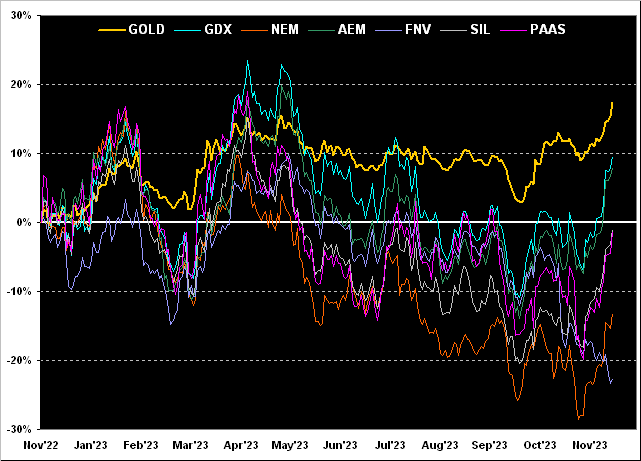

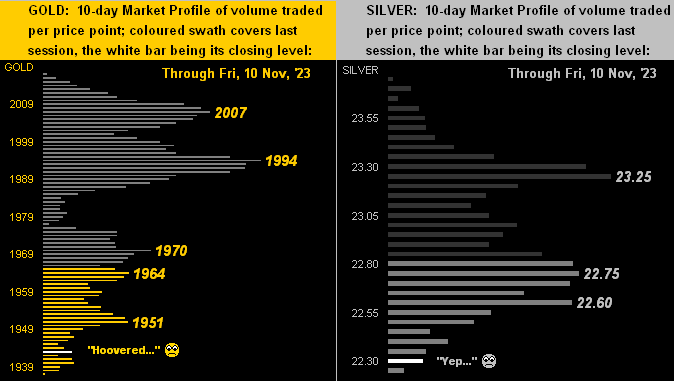

And so in turn we go to the 10-day Market Profiles for Gold (below left) and Silver (below right). Simply stated from high-to-low, the word “hoovered” is apropos, with all labeled lines now overhead trading resistance. As for their two-week percentage changes, Gold’s from top-to-bottom is -4.0% whilst that for Silver is -6.3%. Is it any wonder the Gold/Silver ratio — now 87.1% — is at its second-highest level since last March? No ’tisn’t. Reprise: Do not forget Sister Silver!

Toward the wrap, here’s the stack.

The Gold Stack

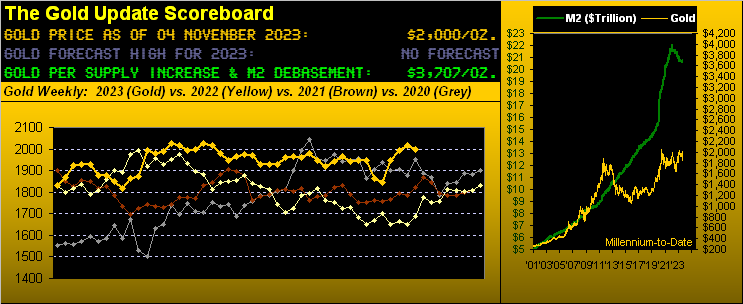

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3706

Gold’s All-Time Intra-Day High: 2089 (07 August 2020)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar ’22); 2085 (04 May ’23)

2023’s High: 2085 (04 May)

Gold’s All-Time Closing High: 2075 (06 August 2020)

10-Session “volume-weighted” average price magnet: 1985

Trading Resistance: 1951 / 1964 / 1970 / 1994 / 2007

Gold Currently: 1943, (expected daily trading range [“EDTR”]: 24 points)

Trading Support: none by the Profile

10-Session directional range: down to 1922 (from 1980) = -81 points or -4.0%

The Gateway to 2000: 1900+

The 300-Day Moving Average: 1883 and rising

The Weekly Parabolic Price to flip Short: 1846

2023’s Low: 1811 (28 February)

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

In sum, Gold is definitely getting the anticipated post-geopolitical pullback. Does it continue? Per the website’s Gold and/or Market Values page, recall that price a mere week ago was +120 points above its smooth valuation line; that deviation has since been reduced to now +39 points. Yet even as Gold’s “Baby Blues” are accelerating lower, again note the cited structural support bases: 1922, 1914 and 1901, the notion thus being that Gold is “safe” above the 1800s.

‘Course, given Gold’s valuation by Dollar debasement is now 3706, ’tis clearly requisite toward maintaining one’s bridge to wealth security.

Thus: don’t be that guy…

…rather consider that Gold today is THE bang-on attractive Buy!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

10 November 2023 – 09:04 Central Euro Time

The Bond is at present above its Neutral Zone for today; the Swiss Franc is below same, and BEGOS Markets volatility is mostly light. Looking at Market Profile resistors for the Spoo (presently 4372) we’ve the 4381-4384 area followed more dominantly by 4396; whilst by Market Trends the Spoo’s linreg in real-time has just rotated to positive, there is broader structural resistance running from 4341 up to 4431; and by Market Values, the Spoo is now +59 points above its smooth valuation line; for the S&P itself, ’tis now “textbook overbought” through these past three trading days. The Econ Baro concludes its quiet week with November’s UofM Sentiment Survey and (purportedly) October’s Treasury Budget.

09 November 2023 – 08:54 Central Euro Time

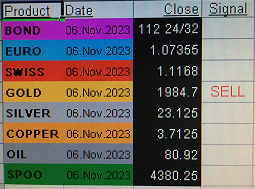

Copper is the sole BEGOS Market at present outside (below) its Neutral Zone for today; session volatility is light, save for Copper which has traced 57% of its EDTR (see Market Ranges). As Gold’s “Baby Blues” continue to descend, price has thus far traded to as low as 1953: recall from the current edition of the Gold Update the mention of 1951 as a mid-structural support level; currently priced at 1955, Gold is now +58 points above its smooth valuation line (see Market Values) after having been better than +100 above it through recent days. Indeed for Gold, Silver and the Swiss Franc, their “Baby Blues” all having fallen below the key +80% level have in turn seen lower price levels. As the Econ Baro’s subdued week continues, only due today are the usual weekly Jobless Claims.

08 November 2023 – 09:01 Central Euro Time

The Bond and EuroCurrencies are at present below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light. At Market Ranges, the recent EDTR widenings for the Bond, Gold, Silver, Oil and the Spoo appear for now to have peaked. Following Gold’s “Baby Blues” falling below their key +80% level, price (now 1974) has since weakened to as low as 1963 yesterday; the Blues in real-time continue to drop as do those for the Swiss Franc, Silver and Oil. The “live” (fut’s adj’d) P/E of the S&P is now 42.5x and the Gold/Silver ratio a very “Silver-attractive” 87.4x despite the present Blues negativity. The Econ Baro awaits September’s Wholesale Inventories.

07 November 2023 – 09:03 Central Euro Time

All eight BEGOS Markets are in the red and all at present (save for the Bond) are below their respective Neutral Zones for today; volatility is mostly moderate. Gold confirmed its “Baby Blues” (see Market Trends) dropping below their key +80% level; priced now at 1976, we can see 1946 trading near-term, well within the context of the support zone described in the current edition of The Gold Update. By Market Rhythms, the most consistent on a 10-test basis is the Euro’s daily Moneyflow which has been near or at the top of all 405 studies now for some time; on a 24-test basis, both the Bond’s 15mn Parabolics and Moneyflow studies top the list, along with the Spoo’s 15min Parabolics. The Econ Baro’s rather “un-busy” week looks to September’s Trade Deficit and Consumer Credit.

06 November 2023 – 08:33 Central Euro Time

The BEGOS Markets’ volatility is light-to-moderate as the new week unfolds. At present, Copper is above its Neutral Zone for today, whilst Gold is below same. The Gold Update anticipates a typical post-geopolitical price pullback is nigh; indeed at Market Trends, Gold’s “Baby Blues” are in real-time slipping below their key +80% axis, (as have Silver’s already so done); confirmation of the “Baby Blues” settling below that level generally leads to lower prices near-term; too, Gold by Market Values is (in real-time) +106 points above its smooth valuation line. Despite all the excitement over the S&P’s recent rally, price has merely returned to where ’twas three weeks ago, the P/E ratio accelerating last week now to 40.9x as Q3 Earnings Season remains rather average at best; (’twas 39.0x those three weeks ago). Nothing is due today for the Econ Baro as it faces a fairly light load this week with just six metrics due through Friday.

The Gold Update: No. 729 – (04 November 2023) – “Gold’s Post-Geopolitical Pullback”

Now beyond the world of reality, the S&P 500 is going giddy! Or at least those following it are. On Monday: “The S&P gained +1.2%!” Then Tuesday: “The S&P added another +0.6%!” Wednesday: “The S&P is soaring, +1.1%!” Thursday “The S&P is straight up +1.9%!” Friday: “The S&P is all bullish, up yet again +0.9%!”

And thus for the week the S&P garnered growth of +5.9%. Cue the late, great Howard Cosell: “Looook at it GO!”

Here’s to where we saw it go: merely back to now 4358 as ’twas three weeks ago. Thus predictably, you know the next sentence. “Change is an illusion whereas price is the truth.” In other words, (’tis our turn to say): “Nothing to see here.”

In the midst of it all, ‘natch, is Q3 Earnings Season. And for the S&P 500, of the 381 constituents having so far reported, 65% have made more dough than in Q3 a year ago.

But shouldn’t they all be making more? After all, this is the S&P 500, the top-tier, best-of-the-best. And when it does not all go right, valuation is the plight. Thus our honestly-calculated “live” price/earnings ratio for the S&P went from 34.0x on Monday to 40.5x come Friday’s settle. For you WestPalmBeachers down there, that means if you buy the S&P right now, you’re willing to pay $40.50 for something than earns $1. Further, the cap-weighted dividend yield for the S&P is but 1.625%. Do not reprise ![]() “Bargain”

“Bargain”![]() –[The Who, ’71]. Worth reprising: the U.S. three-month T-Bill annualized yield is now 5.253%.

–[The Who, ’71]. Worth reprising: the U.S. three-month T-Bill annualized yield is now 5.253%.

Then there’s Gold, which as aforementioned can rise +85% just to reach its current Dollar debasement value. (Remember: given historically such eventually happens, this is not a difficult decision). And although price may languish near-term in post-geopolitical recoil, we don’t expect it to come well off the boil, (on which is has been for nearly a month).

So to Gold’s two-panel graphic we go with the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. Especially note the baby blue dots of trend consistency. Barring price imminently/rapidly rising, those “Baby Blues” shall cross beneath the key +80% axis: such has occurred twice within the past year resulting in subsequent point drops (within 21 days) of -67 and -20 respectively; and that reasonably aligns with the underlying 1980-1922 support structure noted earlier. Specific to trading support, by the Profile the 1995-1988 zone may be the first to go toward further below:

So with our expectations for Gold getting a post-geopolitical pullback — but still more broadly maintain an uptrend — we’ll wrap it up here with this from the “Is the FinMedia Really Running the Fed? Dept.” To wit:

As you all know, the FOMC per this past Wednesday’s Policy Statement unanimously voted to maintain the Bank’s FedFunds target range as 5.25%-5.50%. But did they really need to have their traditional two-day meeting? After all, we were informed the previous Friday (27 October) by Dow Jones Newswires that:

“Inflation Trends Keep Fed Rate Hikes on Pause–Underlying inflation picked up in September, government data showed, keeping the Federal Reserve on track to hold short-term interest rates steady at its next meeting.”

Therefore: why meet at all? Even as the recent inflation data we herein recounted a week ago clearly justified the Fed raising rates, the FinMedia already had decided “No no, Jerome” and that was that. (One wonders if they have to sign non-disclosure agreements. Just a passing thought…)

Regardless of who’s running the Fed show, pullback or not, don’t pass on Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

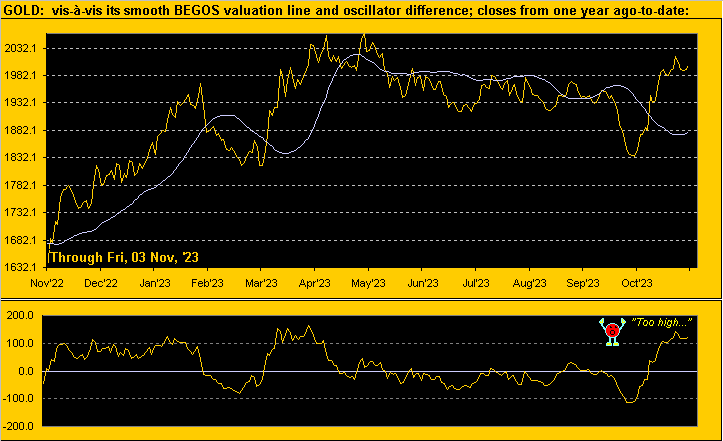

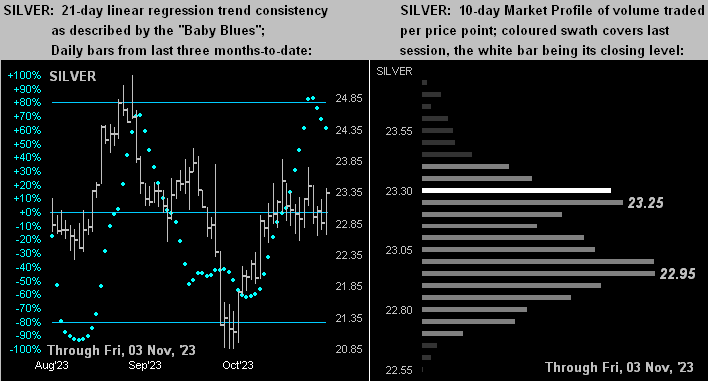

03 November 2023 – 09:02 Central Euro Time

Silver is the only BEGOS Market at present outside (below) today’s Neutral Zone; session volatility is light with October’s Payrolls data in the balance. Yesterday’s +1.9% S&P 500 rise was sufficient to fully unwind the “textbook oversold” stance that had been in place since 23 October; too on Thursday, the S&P’s P/E rose from 34.7x to now 38.8x: with still some 100 Q3 earnings reports due for the S&P, fully one-third thus far have not improved their year-over-year bottom lines; (as penned in last Saturday’s edition of The Gold Update, for the S&P we’re seeing that “…bounce before the next trounce…”); and by Market Values, this bounce has lifted the Spoo up to its smooth valuation line, price back to where ’twas two weeks ago. In addition to the Econ Baro’s incoming jobs data, we’ve also October’s ISM(Svc) Index.

02 November 2023 – 09:01 Central Euro Time

Post-Fed the EuroCurrencies are getting a bid, both the Euro and Swiss Franc at present above their respective Neutral Zones for today, as is Copper; the other BEGOS Markets are within same, and volatility is light-to-moderate. Silver confirmed its “Baby Blues” (see Market Trends) moving below the key +80% level, indicative of lower prices near-term: we are eying 22.18 (current is 23.10) barring geo-political price-rise resumption. As the S&P 500 works through Q3 Earnings Season, with 318 constituents having thus far reported, 65% have bettered their bottom lines from a year ago; however more broadly, only 52% have improved. For the Econ Baro, today’s incoming metrics include the initial read of Q3 Productivity and Unit Labor Costs, plus September’s Factory Orders.

01 November 2023 – 09:00 Central Euro Time

As Mid-East headlines fall a bit from above the fold, so too falling are the precious metals’ prices: both Gold and Silver are at present below their Neutral Zones for today; the other BEGOS Markets are within same, and volatility is light with the FOMC’s Policy Statement in the balance. By Market Profiles, Gold is testing its 1989 trading support, the next such level being 1963; for Silver, its key 23.00 level is being tested. Also by Market Trends, Gold’s “Baby Blues” have started to roll over to the downside, and moreover, those for Silver (in real-time) have provisionally dropped below their +80% level suggestive of lower prices near-term. The Econ Baro looks to October’s ADP employment data and ISM Index, plus September’s Construction spending.

31 October 2023 – 08:59 Central Euro Time

The Bond is at present above its Neutral Zone for today; the balance of the BEGOS Markets are within same, and volatility is again light-to-moderate; thereto of note, whilst not (yet) a BEGOS component, the Yen has traced 235% of its EDTR (see Market Ranges for those of the BEGOS Markets) as the BOJ maintains its long-term debt rate of 0% (as opposed to going negative). StateSide, the S&P 500 yesterday gained +1.2%: however the MoneyFlow was only +0.5%, indicative of the relief rally (from the Index’s still “textbook oversold” condition) lacking substance. Going ’round the Market Values page (in real-time) for the primary BEGOS Markets, we’ve the Bond nearly +3 points “high” above its smooth valuation line, the Euro +0.016 points “high”, Gold +131 points “high”, Oil -4.89 points “low” and the Spoo -143 points “low”. The Econ Baro awaits October’s Chicago PMI and Consumer Confidence, plus Q3’s Employment Cost Index.

30 October 2023 – 09:05 Central Euro Time

The “textbook oversold” S&P 500 looks to get a boost at the open, the Spoo at present above today’s Neutral Zone; below same are both Gold and Oil, and volatility is light-to-moderate. The Gold Update reiterates the yellow metal still as “range-bound” rather than “moon-bound”: 1989 is dominant trading support by the 10-day Market Profile; we’re wary as well that by Market Values, Gold (in real-time at 2005) is +131 points above its smooth valuation line. Leading the Market Rhythms for consistency (10-test basis) is Silver with a variety of studies: its daily Parabolics, 12hr MACD, 8hr Price Oscillator, and both the 6hr Price Oscillator and Moneyflow; too, is the Euro’s daily Moneyflow. ‘Tis a busy week for the Econ Baro with 15 metrics on the table, (none due today).

The Gold Update: No. 728 – (28 October 2023) – “S&P Squirms; Gold Firms”

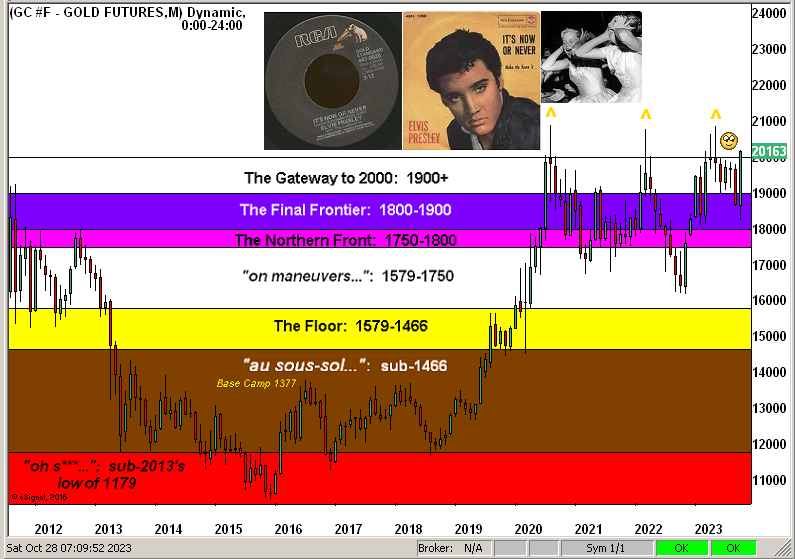

So with but two trading days remaining in October, here now is our stratified Gold Structure by the month across these past dozen years. As oft previously shown, now courtesy of the “Here We Go Again Dept.” we’ve Gold’s triple top which “is meant to be broken” as highlighted by the three Golden arrows. Moreover, we’ve anticipated on occasion throughout this year’s missives that Gold shall record a fresh All-Time High in 2023: obviously the momentum is there, barring a post-geo-political price retrenchment (as is the rule rather than the exception). Nonetheless, let’s cue Elvis from back in ’60 with ![]() “It’s now or never…”

“It’s now or never…”![]() :

:

Through these 10 months we’ve emphasized the importance of doing the math to get to the truth of such critical metrics as economic inputs, p/e calculations, and so forth. And whilst nothing light can be made of the horrific Mid-East mayhem, as this past week unfolded a mathematical “challenge” shall we say “came to light” over at the United States Department of State. Hat-tip ExecutiveGov which reported: “The Department of State has issued an advisory cautioning United States citizens against travel to more than 200 countries amid rising geopolitical tensions and conflict.” ‘Course, you can see where this is going, given (hat-tip Quora) stating: “Today, there are 197 countries in the world…“ The bottom line here being: if you’re in the States, you’re sorta stuck from going anywhere, nor beyond! Best therefore not to squirm; rather stay firm and stuck in Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro

27 October 2023 – 09:01 Central Euro Time

The Bond is at present below its Neutral Zone for today, whilst above same are Copper, Oil and the Spoo; BEGOS Market’s volatility is mostly light. As tweeted (@deMeadvillePro) last evening, we’re finally seeing some “fear” in the Flow, the S&P 500 falling -1.2% yesterday, but its MoneyFlow regressed into S&P points was -2.4%; still, the Index for the present is “textbook oversold”, so perhaps some bounce to unwind that condition, followed then by lower levels sub-4000 (S&P at present is 4137). At Market Trends, the Swiss Franc’s “Baby Blues” have (in real-time) provisionally slipped below their +80% level, suggestive of lower prices near-term, which coincident with a Fed rate hike would further foster Dollar strength. Indeed ahead of next Wednesday’s FOMC Policy Statement, the Econ Baro’s incoming metrics for today include the “Fed-favoured” Core PCE Price Index along with the month’s Personal Income/Spending.

26 October 2023 – 09:03 Central Euro Time

At present we’ve the Metals Triumvirate higher and the EuroCurrencies lower. Notably for the second straight session (to this point), both Gold and the Dollar are gaining, (“Gold plays no currency favourites”). The Spoo continues to work lower: as we’ve (yet) to see “fear” in the S&P’s MoneyFlow, (when otherwise Flow falls at a faster rate than the Index itself), this feels mildly reminiscent of the old so-called “Gentlemen’s Crash”, although hardly has price fallen nearly to any crash proportion. These next two days have key incoming metrics for the Econ Baro ahead of next Wednesday’s FOMC Policy Statement: today we await the first peek at Q3’s GDP, along with other reports including September’s Durable Orders and Pending Home Sales.

25 October 2023 – 09:07 Central Euro Time

At present, all eight BEGOS Markets are within their respective Neutral Zones for today, and volatility is at best light. In looking at Market Rhythms on a 10-test basis, the most profitably consistent through yesterday are Silver’s 8hr Price Oscillator, 12hr MACD, 6hr Moneyflow and daily Parabolics, plus Oil’s 4hr Moneyflow, the Euro’s daily Moneyflow, and the Swiss Franc’s daily MACD. On a 24-test basis, the best is Gold’s 1hr Price Oscillator. By our S&P MoneyFlow page, we’ve still yet to detect any real fear, even as our “live” P/E (futs-adj’d) is now 36.9x. The Econ Baro gets its back-loaded week underway with September’s New Home Sales.

24 October 2023 – 09:02 Central Euro Time

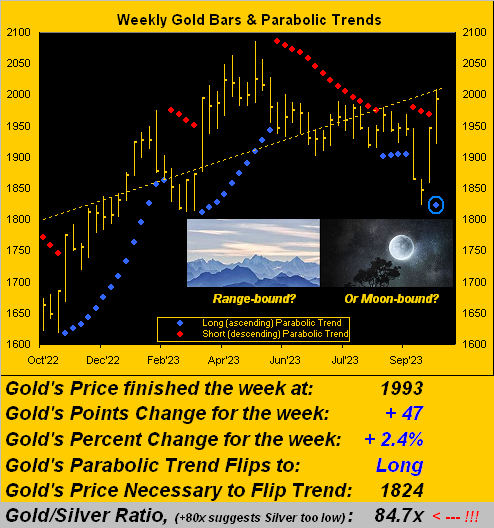

The Bond, Gold and Copper are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light, save for Copper having already traced 67% of its EDTR (see Market Ranges). By Market Values we’ve Gold in (real-time) +107 points above its smooth valuation line. In tandem with the Dollar having weakened across the past two weeks, by Market Trends the linregs for Gold, Silver, the Euro and Swiss Franc all have rotated to positive; those for the other four BEGOS components remain negative. Yet Silver is still a laggard to Gold, the G/S ratio at 86x vs. the century-to-date average of 68x: as we from time-to-time quip in The Gold Update: “Don’t forget the Silver!”

23 October 2023 – 09:24 Central Euro Time

Save for the Spoo, the other seven BEGOS Markets are in the red, all at present below their respective Neutral Zones for today; session volatility is pushing toward moderate. The Gold Update sees the yellow metal as remaining “range-bound” until the All-Time High (2089 vs. the current 1986) is eclipsed, (from which Gold then becomes “moon-bound”, ideally to its present Dollar debasement value of 3724). The Econ Baro is back-loaded this week from Wednesday on, key reports including Q3 GDP and the “Fed-favoured” Core PCE Index. And thus far, Q3 earnings by year-over-year comparison is relatively weak: mind our Earnings Season page.

The Gold Update: No. 727 – (21 October 2023) – “Gold: Range-Bound? Or Moon-Bound?”

So: is Gold remaining range-bound? Or is it finally moon-bound? Let’s start with the former.

For the bazillionth time we postulate that “change is an illusion whereas price is the truth”. Whilst the low-information, short-attention span, instant gratification crowd have recently been yanked to and fro through Gold’s plunge before its ![]() “Going to a Go-Go”

“Going to a Go-Go”![]() –[Miracles, ’65], let’s focus on price, the truth to know. To wit:

–[Miracles, ’65], let’s focus on price, the truth to know. To wit:

Today’s 1993 price also traded during 34 of the prior 168 weeks going all the way back to that ending 31 July 2020. And as anyone who is paying attention knows, Gold’s infamous triple top (2089/2079/2085) has yet to be broken, (which they are meant to so do). Thus until the next All-Time High is achieved, price remains range-bound, for 1993 today ain’t anything over which to bray “Olé!” Here is price (i.e. “truth”) via the monthly candles from 2020-to-date, denoting the triple-top:

Neither is it easy for the S&P, given both the geo-political climate and the Index’s ongoing overvaluation, our “live” price/earnings ratio settling the week at 36.2x. And speaking of earnings, (or lack thereof), have you been following their Q3 season? Specific to the S&P 500, 68 constituents have thus far reported: just 34 (50%) of those bettered their bottom lines from a year ago. More broadly? ‘Tis worse: with 134 companies’ (of some 1800 to eventually report) results in hand, just 44% have bettered. Too as tweeted (@deMeadvillePro) this past Thursday, “Flow leads dough…” per our S&P MoneyFlow page depicting a more negative stance.

And again from the “They’re Just Figuring This Out Now? Dept.”, iconic ol’ Morgan Stanley finds U.S. Treasuries attractive at 5%. (‘Course you readers of The Gold Update have known for months that the T-Bill’s been yielding at least 5% since 18 April.) Oooh and this quick update: the market capitalization of the S&P 500 per Friday’s settle is now down to $36.9T; but the liquid money supply (“M2”) of the U.S. is only $20.8T. It doesn’t add up very well, does it? No it doesn’t.

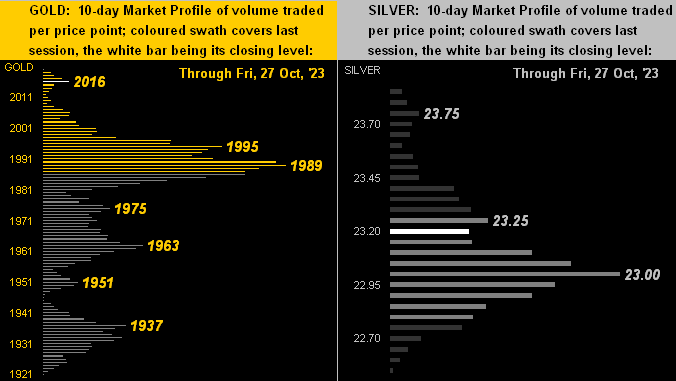

But ’tis adding up quite nicely for Gold as we next go to its two-panel display of daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. The baby blue dots of trend consistency have only just crossed above their 0% axis, suggesting the uptrend has more ![]() “Room to Move”

“Room to Move”![]() –[Mayall, ’69] in spite of near-term technicals being somewhat stretched. Thus given some natural price retraction, we can see the key underlying support levels as labeled in the Profile:

–[Mayall, ’69] in spite of near-term technicals being somewhat stretched. Thus given some natural price retraction, we can see the key underlying support levels as labeled in the Profile:

To sum up, ’twas a great week for Gold and a poor one both for equities and the StateSide Economic Barometer, the latter in the new week looking to the first peek of Q3 Gross Domestic Product and that “Fed-favoured” Core Personal Consumption Expenditures metric for September.

And with geo-politics continuing to dominate the airwaves whilst the lousy Q3 Earnings Season unfolds, one ought expect more of the same at least near-term, albeit liquid markets don’t move in a straight line. But the “Baby Blues” at the website’s Market Trends page tend to keep one on the correct side of it all.

Indeed all-in-all — at least until Gold posts a new All-Time High above 2089 — we still see price as more range-bound than moon-bound. But again, as Jackie points out to Alice:

Or as we time-to-time say: “Tick tick tick goes the clock clock clock…” Got your precious metals?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro