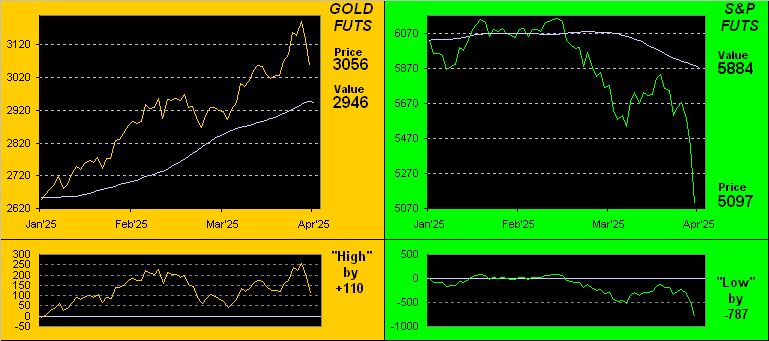

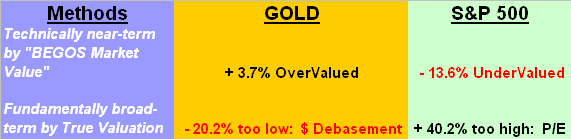

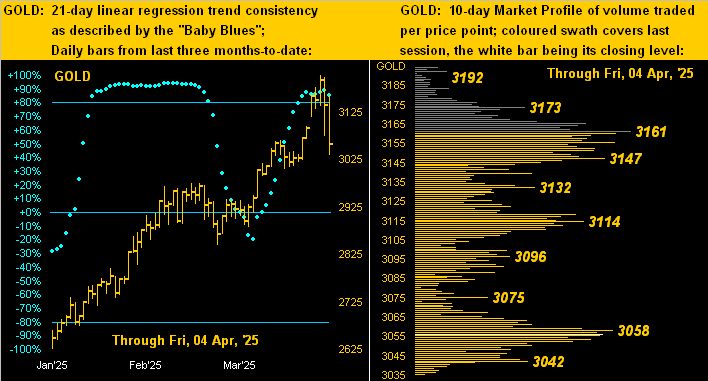

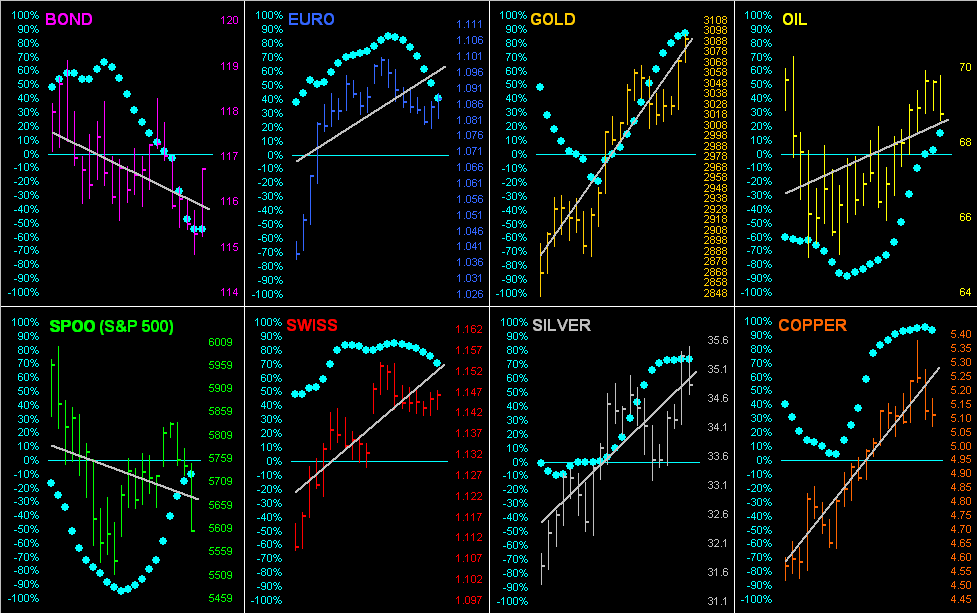

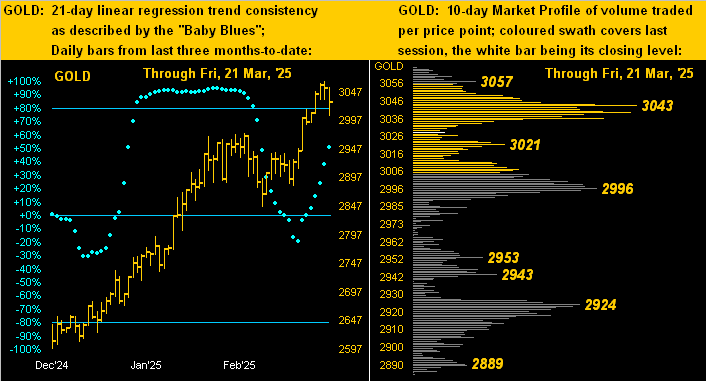

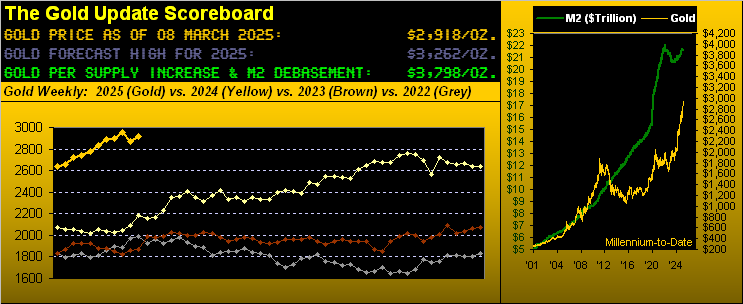

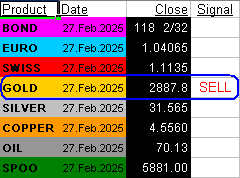

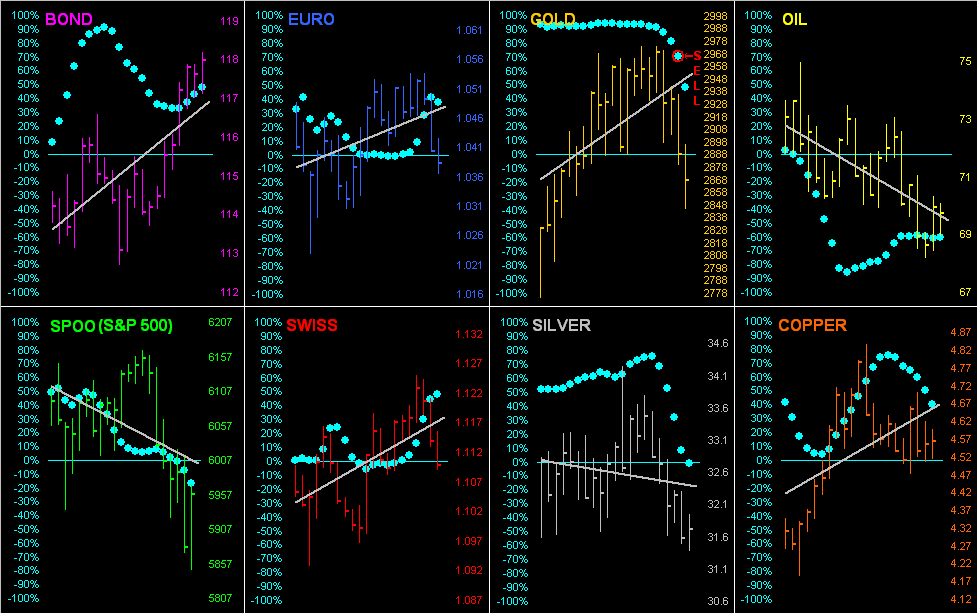

The BEGOS Markets at present find the Euro, Swiss Franc, Gold, Oil and the Spoo above their respective Neutral Zones for today; none of the other three components are below same, and volatility is moderate, albeit in the context that EDTRs (see Market Ranges) have substantively widened in recent sessions: for example, a year ago today the Spoo’s EDTR was 51 points (price then 5257) whereas for today (price currently 5174) ’tis 165 points. Gold’s “Baby Blues” (see Market Trends) of trend consistency yesterday broke below the key +80% axis, making us anticipative of still lower price levels: by Market Values in real-time, Gold still is +79 points above its smooth valuation line; the Spoo however is -681 points below same, even as the S&P 500 itself fundamentally remains quite overvalued give its “live” (futs-adj’d) P/E at 37.1x. Nothing is due today for the Econ Baro, however as previously noted, Q1 Earnings Season has commenced, which you can follow day-by-day on that page.

Mark

Mark

07 April 2025 – 08:45 Central Euro Time

Selling of equities looks to continue: adjusting the Spoo at present to Fair Value, the S&P 500 (were the StateSide market to open at this instant) would trade sub-5000 for the first time since 25 April a year ago. ‘Tis worth noting with the Spoo -4.4%, the -7% “lock limit” would apply at 4740. At present along with the Spoo below their respective Neutral Zones are both Gold and Oil; above same are the Bond, Euro, Swiss Franc and Silver; volatility for the BEGOS Markets is again firmly moderate and then some: both Silver and Copper (the latter at present back inside today’s Neutral Zone) have traced in excess of 200% of their EDTRs (see Market Ranges). The Gold Update cites the yellow metal still as being technically overbought near-term but fundamentally undervalued broad-term, whilst ’tis the opposite cases for the S&P 500, (technically oversold, fundamentally overvalued). The Econ Baro looks late in the session to February’s Consumer Credit. And Q1 Earnings Season gets underway.

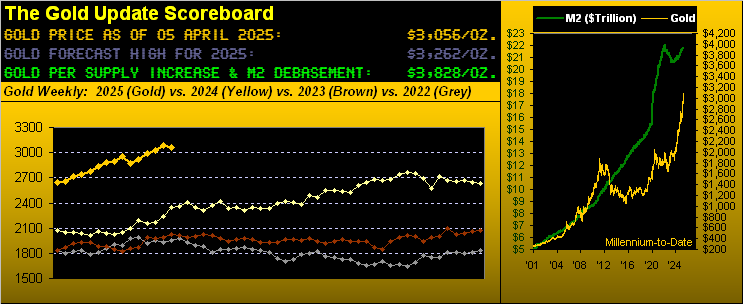

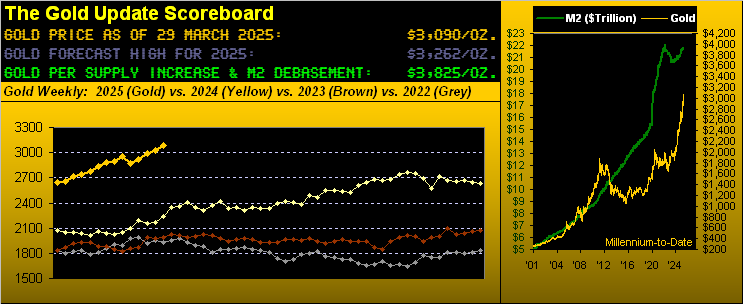

The Gold Update: No. 803 – (05 April 2025) – “Gold Comes Off; Stocks Finally Boffed”

We’ll wrap up here for this week with a little personal experience tariff talk.

We (on the very rare occasion) make a purchase that is shipped from the United States. Our most recent case was $99 worth of a specific popping corn we simply cannot find on this side of The Pond. The shipping charge was $25, and thus the all-in cost paid to the exporter was $124.

Then came the fun part in order to take receipt of the shipment.

A customs tariff of €28 ($29) was levied along with the beloved value-added tax of €35 ($37) for an all-in cost of $190 for $99 worth of popping corn. Ex-shipping, 40% of the cost went to tariff and tax.

No wonder the “Leader of the Free world” is fired up. Just don’t let ’em get your Gold!

A team player, our Squire. Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

04 April 2025 – 08:50 Central Euro Time

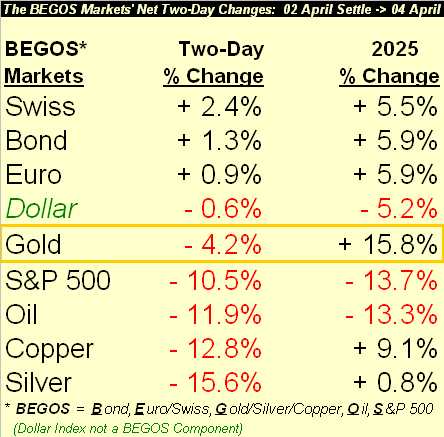

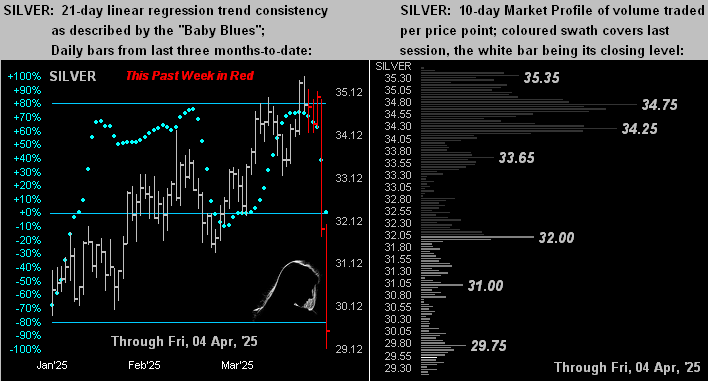

Sister Silver suffered the worst yesterday amongst the BEGOS Markets: her -8.8% net loss was the white metal’s worst since 11 August 2020; more on the metals and markets in tomorrow’s 803rd consecutive Saturday edition of The Gold Update. Following yesterday’s beat-down, (save for the Bond and EuroCurrencies), we’ve at present both the Bond and Swiss Franc above today’s Neutral Zones, whilst below same are again the Metals Triumvirate and Oil; (the Spoo is within same); session volatility is firmly moderate, the Swiss Franc notably having traced 110% of its EDTR (see Market Ranges). Given yesterday’s material moves, the five primary BEGOS components are positioned (in real-time) as follows vis-à-vis their respective smooth valuation lines (see Market Values): the Bond is just over +3 points “high”, the Euro +0.039 points “high”, Gold (despite its being sold) +170 points “high”, Oil -2.95 points “low”, and the Spoo deeply oversold by this metric at -471 points “low”; of course, for the S&P 500 itself, its “live” P/E (futs-adj’d) still remains up in the silly zone at 37.1x; thus there’s rightly still a long way to fall. The Econ Baro closes its weeks with March’s Payrolls.

03 April 2025 – 08:35 Central Euro Time

The Spoo is presently positioned such that were the S&P 500 to open at this instant, ‘twould immediately fall -3.0%; the last time the S&P completed a session down by at least that much was on 13 September 2022 (-4.3%). The Dollar Index is down to its lowest level (102.425) since 09 October. The Bond and EuroCurrencies are currently above today’s Neutral Zones, whilst below same are the Metals Triumvirate, Oil, and Spoo; session volatility is robust with five of the eight BEGOS Markets tracing in excess of 100% of their EDTRs (see Market Ranges). Silver is getting notably sold, -4.8%, in turn pushing the Gold/Silver ratio up to 94.2x; Gold itself is -1.5% and by its Market Value is (in real-time) nonetheless +197 points “high” above its smooth valuation line. Amongst today’s incoming metrics for the Econ Baro are March’s ISM(Svc) Index and February’s Trade Deficit.

02 April 2025 – 08:44 Central Euro Time

The Bond is at present the sole BEGOS Market outside (below) its Neutral Zone for today; session volatility is light. Looking at Market Rhythms for pure swing consistency, on a 10-test basis our best are the non-BEGOS Yen’s daily Price Oscillator, both Silver’s 8hr Parabolics and 2hr Price Oscillator, plus Copper’s 8hr Price Oscillator; on a 24-test basis we’ve again the Yen’s daily Price Oscillator plus its daily Parabolics and 15mn MACD, along with the Bond’s daily Moneyflow and the Swiss Franc’s 2hr Moneyflow. As anticipated, Copper’s “Baby Blues” (see Market Trends) have in real-time provisionally crossed under their +80% axis suggestive of still lower prices near-term. The Econ Baro awaits March’s ADP Employment data plus February’s Factory Orders. And 20:00 GMT brings the StateSide tariffs address.

01 April 2025 – 08:38 Central Euro Time

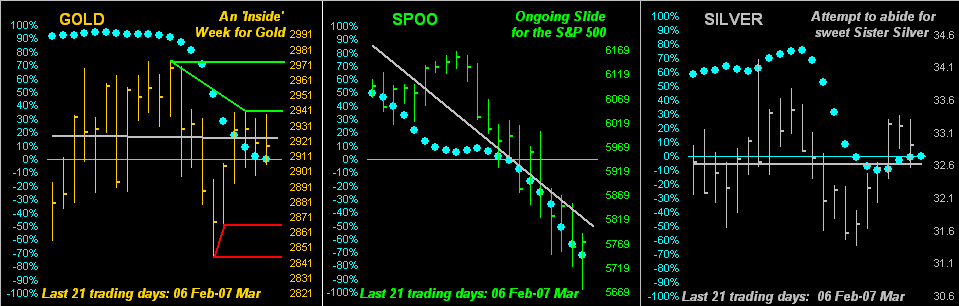

Gold (basis June) has made yet another All-Time High at 3177, albeit price has now pulled back to presently be within today’s Neutral Zone; the only BEGOS Market outside (above) of same is the Bond, and volatility is light-to-moderate. The Bond yesterday pierced up through its Market Magnet, whilst Copper has moved below same; Copper’s “Baby Blues” (see Market Trends) are rolling over such that they many breach below the key +80% by mid-week, then suggestive of still lower price levels. Oil has furthered our anticipation of its rising, now up into the 71s. Q1 kicks off for the Econ Baro with March’s ISM(Mfg) Index and February’s Construction Spending.

31 March 2025 – 08:33 Central Euro Time

The Bond, Gold, Silver and Oil are all above today’s Neutral Zones, whilst below same is the Spoo; session volatility is moderate-to-robust, Gold notably already having traced 129% of its EDTR (see Market Ranges). The Gold Update underscores the yellow metal’s remarkable rally, yet remains wary for some material degree of pullback to unwind the near-term overbought state of price, which in (real-time) is +228 points above its smooth valuation line (see Market Values); moreover the Update also depicts the inconsistant inflation readings, and sees significantly lower levels for the S&P 500 as the year unfolds, with the 4000s in the offing, (which from its present level is only some -10% lower). For the Econ Baro today we’ve March’s Chi PMI.

The Gold Update: No. 802 – (29 March 2025) – “Gold Aware, Stocks Beware”

Well! Can we all say “Gold 3100!” After all, why stop at 3000? For this past Thursday as Gold’s contract volume rolled from April into that for June came +29 points of fresh price premium and (per Tag Team from ’93): ![]() “Whoomp! There It Is!”

“Whoomp! There It Is!”![]() as 3100 June Gold traded, indeed yesterday (Friday) to as high as 3124!

as 3100 June Gold traded, indeed yesterday (Friday) to as high as 3124!

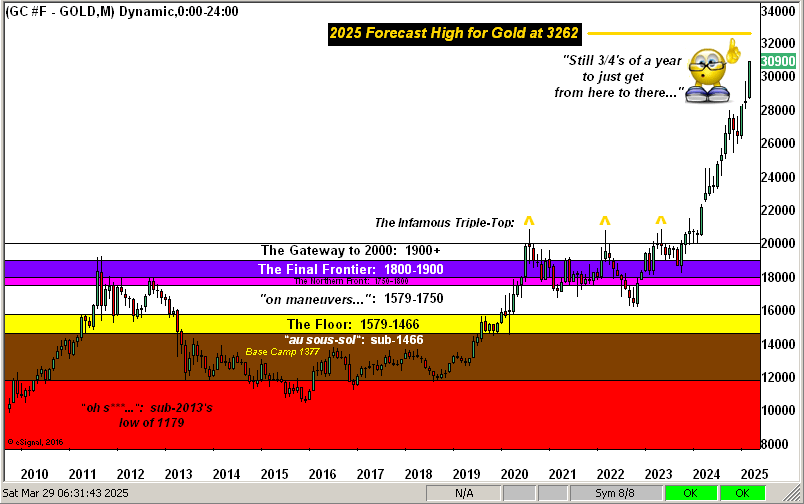

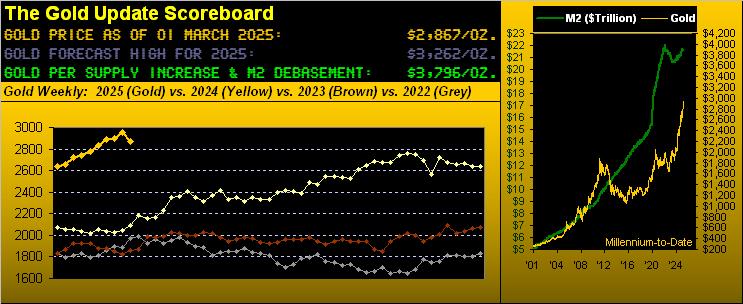

‘Course, from the “Nitty-Picky Dept.”, spot Gold didn’t quite get there, reaching up to only 3085, with the April contract going off the board at 3090. Yet given our year’s Golden Goal Three forecast high of 3262, (let alone the above Scoreboard’s Dollar debasement Gold valuation of 3825), ’tis merely a matter of time for spot 3100… and beyond!

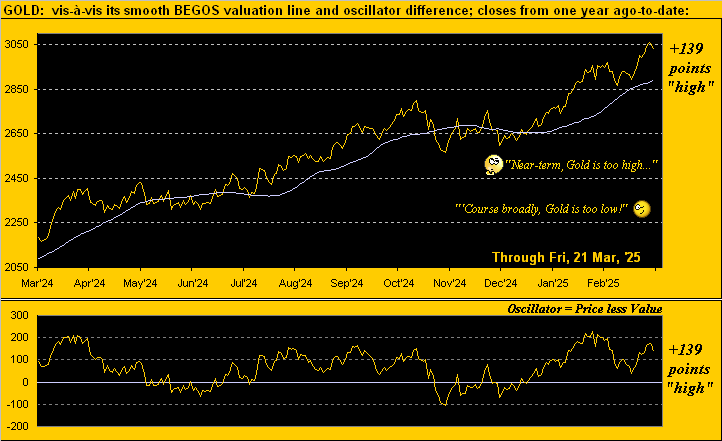

Regardless (and you knew this was coming): all the new-found Gold euphoria aside, yes, we remain expectant for some material degree of price decline. ‘Tis technically so by our BEGOS valuation of Gold depicting it as +173 points “high” (price then always reverting to valuation). ‘Tis fundamentally so by inflation’s inability to efface toward a “Fed-favoured” pace. Let’s have a look.

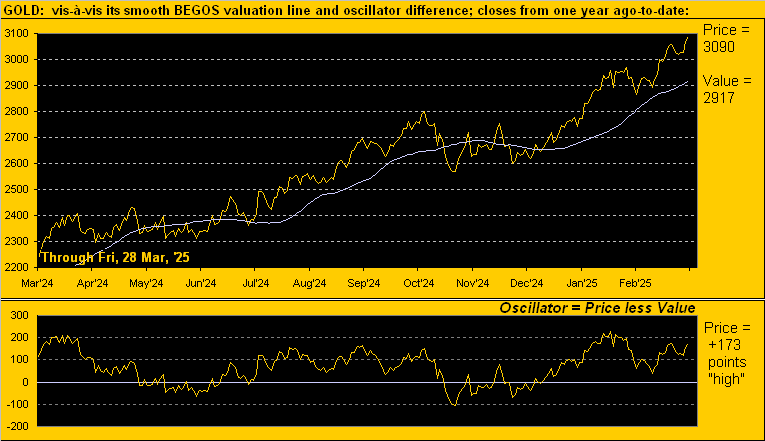

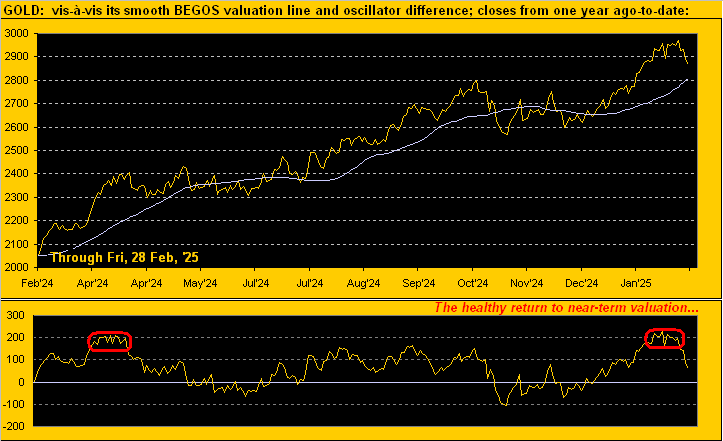

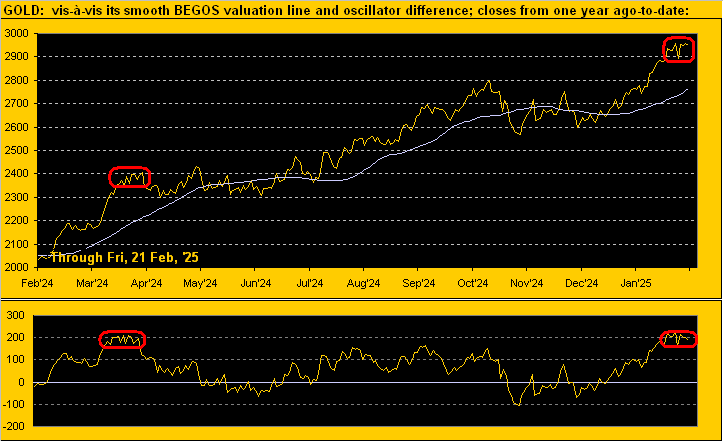

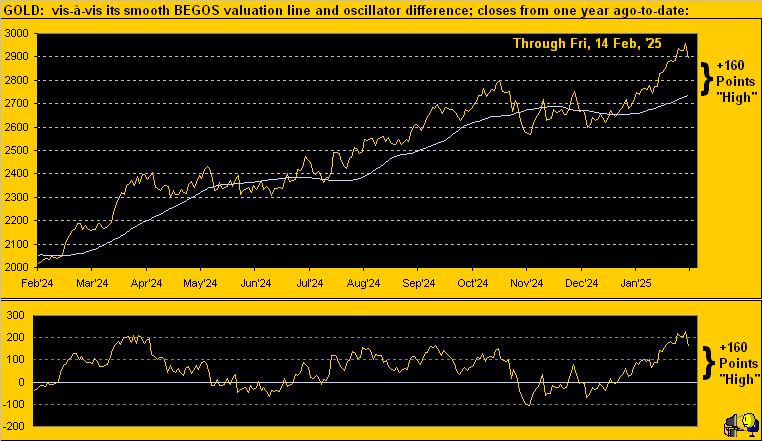

Technically we’ve our year ago-to-date chart of price’s daily closes vis-à-vis the smooth valuation line which assesses Gold’s movement relative to those of the four other primary BEGOS Markets, namely the Bond, Euro, Oil and S&P 500. As shown, Gold is presently priced at 3090, but the valuation line is 2917: thus we’ve the +173-point difference which will get closed, aided as well by the smooth line itself being on the rise:

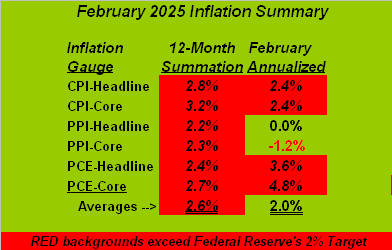

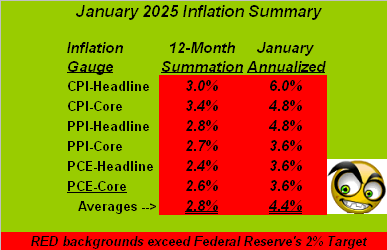

Fundamentally for inflation through February, ’tis said you can “pick your poison” per our puke-green table below, wherein:

- Should you side with The Bureau of Labor Statistics (which calculates both the Consumer Price Index and Producer Price Index), the pace of inflation slowed for the month, the core PPI itself being deflationary;

- If instead to go with the Fed, The Bureau of Economic Analysis‘ Personal Consumption Expenditures data came in well-ahead of the Federal Reserve’s preferred annualized rate of +2.0%.

But: to average the six annualized measures for February, ’tis magically spot-on at +2.0% So if you’re an Open Market Committee member, query: Who to believe? What to do? Lower, maintain, or raise? (To be sure, ’tis FinMedia-verboten to even mention the phrase “Fed rate raise”). Yet what? No cut? Cue King Crimson crooner Greg Lake from ’69: ![]() “Confusion will be my epitaph…”

“Confusion will be my epitaph…”![]() as here’s the table:

as here’s the table:

So as tomorrow we slide EuroSide to summer hours, let’s close it out for this week with (yet another) shocking stat for the S&P 500. ‘Course, you regular readers know the two “ongoing-in-perpetuity” shocks of 1) the “live” price/earnings for the S&P now at 40.2x — yes, that’s after Friday’s -2.0% fall — and 2) the current market cap of the S&P now $49.1T versus a “readily available” M2 money supply of less than half that at $21.8T. (Is your brokerage preparing its IOUs?)

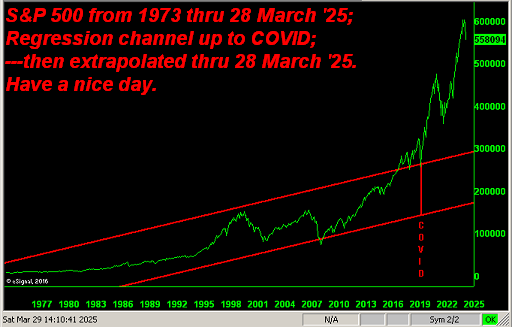

Here’s our next shock. Per the aforeshown BEGOS Markets Standings, again the worst year-to-date loser is the S&P -5.1%. If we regress by the day from New Year the track of the S&P’s closing price (which currently is 5581), and extrapolate such trend to year-end, the Index then first settles in the 4000s come 12 August, on track to finish the year -25% at 4386. This varies a bit from Goldman’s 6200, but we tend to notice little things like that.

Because we don’t forget big things like this:

28 March 2025 – 08:38 Central Euro Time

Both the Bond and Gold are at present above their respective Neutral Zones for today; none of the other BEGOS Markets are below same, and session volatility is light-to-moderate. Gold has achieved yet another All-Time High this morning, the June cac thus far trading up to 3124: by Market Values, price is (in real-time) +176 points “high” above its smooth valuation line, a very extreme deviation which can begin to be closed should the “Fed-favoured” inflation of PCE data not be indicative of slowing; ’twill arrive later today for the Econ Baro, and of course, more on it all in tomorrow’s 802nd consecutive Saturday edition of The Gold Update. As for the other primary BEGOS components’ deviations from Market Values, we show both the Bond and Oil as basically right on their valuation lines, the Euro as +0.0312 points “high” and the Spoo as -200 points “low”. As for Copper’s recent robust rally to all-time highs, by Market Trends, the red metal’s “Baby Blues” of trend consistency are depicting the early signs of having run out of puff. EuroSide, we move forward Sunday to summer hours.

27 March 2025 – 08:42 Central Euro Time

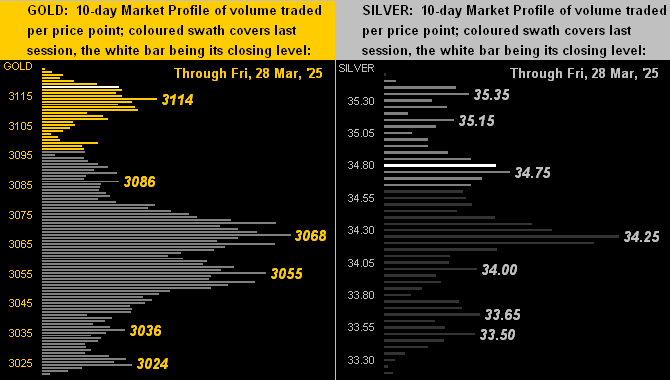

At present we’ve Gold above today’s Neutral Zone, whilst Oil is below same, (but not before having yesterday reached up into our low 70s’ target area); volatility for the BEGOS Markets is moderate. Gold’s cac volume is moving from April into that for June, with +29 points of fresh premium (in turn inducing a “faux” new All-Time High). As anticipated, by Market Trends the Swiss Franc’s “Baby Blues” of linreg trend consistency confirmed falling below the key +80% axis: thus we look for lower price levels near-term. Silver at present is spot-on its most volume-dominant price (34.25) of the past fortnight, (see Market Profiles). And a day ahead of the “Fed-favoured” PCE inflation data, today’s incoming Econ Baro metrics include February’s Pending Home Sales and the final read on Q4 GDP.

26 March 2025 – 08:41 Central Euro Time

As was the same case at this time yesterday, Copper is the only BEGOS Market at present outside (above) its Neutral Zone for today; by Market Ranges, the red metal already has traced 125% its EDTR to an all-time high at 5.3740; overall session volatility is otherwise light. For our Market Rhythms on a 10-test basis, the current standouts are Gold’s 2hr Moneyflow and both the non-BEGOS Yen’s daily price Oscillator and 30mn MACD; on a 24-test basis, our current leaders are again the Yen’s daily price Oscillator along with its daily Parabolics, plus both the Bond’s daily Moneyflow and 15mn Parabolics. We’ve previously mentioned the Euro’s “Baby Blues” (see Market Trends) having broken below the key +80% axis; now provisionally doing the same are those for the Swiss Franc. And for the Econ Baro we await February’s Durable Orders.

25 March 2025 – 08:29 Central Euro Time

At present, the only BEGOS Market outside (above) today’s Neutral Zone is Copper; session volatility is quite light with to this point just an average EDTR (see Market Ranges) tracing of 28%. The Euro yesterday confirmed its “Baby Blues” (see Market Trends) of linreg trend consistency having broken below their key +80% axis, indicative of lower levels to come. The S&P 500, after having been 19 consecutive trading sessions “textbook oversold” finally unwound that condition yesterday; the +1.8% relief rally has now put the “live” (futs-adj’d) P/E up to 42.9x; lurking for April/May is a MACD negative crossover on the S&P’s monthly candles, broadly suggestive of further Index lows as the year unfolds. The Econ Baro gets back into gear today with March’s Consumer Confidence and February’s New Home Sales.

24 March 2025 – 08:10 Central Euro Time

The week starts to find the Bond at present below its Neutral Zone for today, whilst above same are the Euro, Silver, Copper and the Spoo; volatility for the BEGOS Markets is light. The Gold Update applauds the yellow metal’s wonderful uptrend — incorporating yet another All-Time High (3065) this past Thursday — however reiterates our wariness for price to pullback by a few hundred points, typical in the past of similar technical near-term “overvaluations”; (of course fundamentally broad-term, Gold remains well-undervalued). As anticipated, the Spoo is getting a good bid such that the S&P 500 may open nearly a full 1% higher: regardless, the futs-adj’d “live” P/E is 40.0x and the yield (1.347) less than one-third that of the annualized 3mo U.S. T-Bill (4.185%). Too continues Oil’s recent recovery: by its BEGOS Market Value, ‘twould appear price shall move up through its smooth valuation line as the week unfolds towards the anticipated low 70s. ‘Tis a again quiet day for the Econ Baro, the week’s highlight arriving Friday with the “Fed-favoured” PCE reading for February.

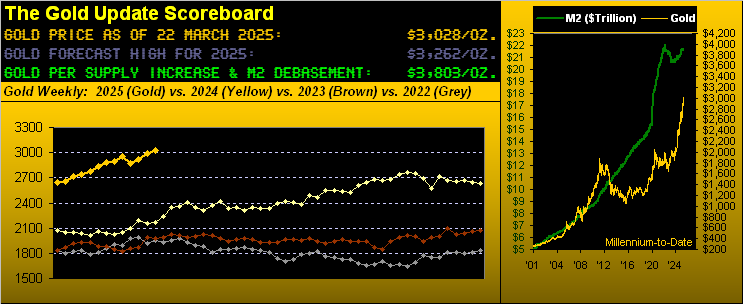

The Gold Update: No. 801 – (22 March 2025) – “Gold’s Year of the Bid”

Thus far in 2025, ’tis been the year of the Gold bid. Folks who are clueless on Gold are abashedly asking about it. “How much is it?” “How do I buy it?” “How much is in Fort Knox?” “How do I store it?” “How much is it taxed?” “How do I get it outta the UK?”

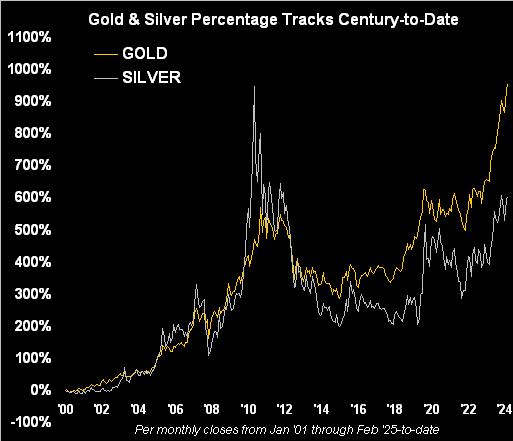

Indeed, we too query: has our having penned 800 Gold Updates finally made the world Gold crazy? That century-to-date — although the S&P 500 is + 329% (from 1320 to 5668) — that Gold’s growth is triple that at +1,005% (from 274 to 3028)? ‘Tis clear that this year the Golden lightbulb has suddenly gone aglow and everybody’s excited to give Gold a bid, even wee London:

Gold’s Year of the Bid indeed! We’re a bit surprised to see the yellow metal moving so swiftly toward Golden Goal Three of 3262. Through the year’s first 12 weeks, only one has been down: such stints of 11 up weeks in 12 have only occurred (as a mutually-exclusive basis) on five other occasions so far this century. The average price fallout following those five instances within the ensuing three months? -9%, which again “suggests” similar downside to the aforeshown currently streaking Market Value’s “price over valuation differential” that has historically then led to an average -7% drop. But as we on occasion caution: “Average is not Reality” especially given Gold’s strong bid this year. Still as stated, we shan’t be surprised to see Gold revisit the 2700s, etc.

And in Gold’s year of the bid if such pullback must be, better it indeed be prior to our 3262 Golden Goal Three!

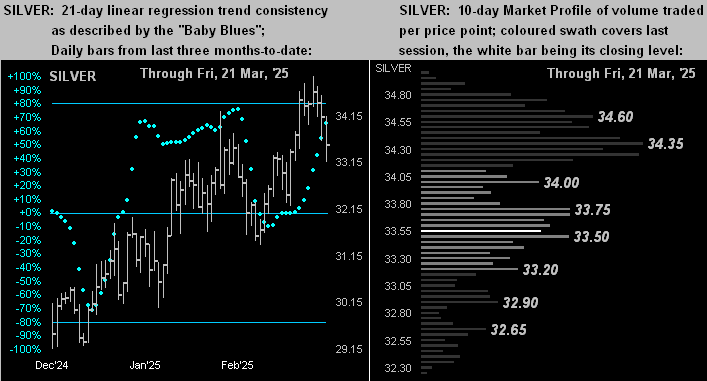

21 March 2025 – 08:35 Central Euro Time

When all eight BEGOS Markets are down, we know the Dollar is up; of note across the sea of red, we’ve the Euro, Swiss Franc, Gold and Silver all at present below their respective Neutral Zones for today; session volatility is moderate. Specific to the Spoo, its “Baby Blues” (see Market Trends) of linreg trend consistency confirmed closing above their key -80% axis: this portends (by fib) a run up to at least the 5800s and potentially the 5900s should the February high-March low have a full Golden Ratio retracement; too, the S&P 500 itself remains “textbook oversold” near-term. For Oil, per its “Baby Blues” and Market Magnet, as anticipated, price has moved from the 65s to now being in the 68s with the 69s-low 70s reasonably in the balance. Nothing is due for the Econ Baro until Tuesday, this week’s 16 incoming having flat-lined the economic track rather than see it further weaken; more on it all in tomorrow’s 801st consecutive Saturday edition of The Gold Update.

20 March 2025 – 08:47 Central Euro Time

The Euro at present is below its Neutral Zone for today, whilst above same is the Spoo; session volatility for the BEGOS Markets remains light to this hour. Our best correlation currently amongst the five primary BEGOS components is positive between Oil and the Spoo. The “live” P/E of the S&P 500 has (futs-adj’d) moved back above 40 (now 40.2x); the Index’s yield is 1.353% vs. the risk-free 3-month T-Bill’s 4.190%; technically the S&P is now 17 consecutive trading days “textbook oversold” despite fundamentally remaining dangerously overvalued. The Econ Baro concludes its week today with a busy schedule of incoming metrics which include March’s Philly Fed Index, February’s Existing Home Sales and Leading (i.e. “lagging”) Indicators, and Q4’s Current Account Deficit.

19 March 2025 – 08:43 Central Euro Time

At present, the Euro is below its Neutral Zone for today, whilst above same is Copper; otherwise, BEGOS Markets’ volatility is again light to this time of the session. Oil’s “Baby Blues” (see Market Trends) confirmed crossing above their -80% axis, so as already noted yesterday with respect to its Market Magnet, we anticipate higher Oil levels near-term perhaps up into the low 70s; Oil’s best Market Rhythm for pure swing consistency on a 10-test basis is its 2hr MACD. Elsewhere on that basis, our best currently are the non-BEGOS Yen’s daily Price Oscillator as well as that study for 1hr Silver; on a 24-test basis, we’ve again the Yen’s daily Price Oscillator plus the daily Parabolics, along with the Bond’s daily Moneyflow. Nothing is due today for the Econ Baro. Then at 18:00 GMT comes the “no change” FOMC Policy Statement.

18 March 2025 – 08:50 Central Euro Time

A day ahead of the Fed, the Econ Baro has of late gone into a skid; to the extent the Fed reacts to fresh data is doubtful such that they likely stand pat as their stance of late is “there is no race to lower rates”. For today at present we’ve Gold, Silver and Oil above today’s Neutral Zones, the balance of the BEGOS Markets being within same, and session volatility is again light. Oil’s Market Magnet yesterday confirmed upside penetration by price such that we expect higher levels near-term, albeit there are various structural resistors from 69-73. Too, Oil’s “Baby Blues” (see Market Trends) continue to modestly climb from having been below their-80% axis, so that, too, lends some bullishness to the picture. The 2-day S&P rally has not been kept pace with by the Moneyflow, although the Index remains now 15 days “textbook overbought”; rhus once that unwinds, we may see the next spillover. More February metrics hit the Econ Baro today, specifically Housing Starts/Permits, Ex/Im Prices, and IndProd/CapUtil.

17 March 2025 – 08:28 Central Euro Time

The Spoo is the sole BEGOS Market presently outside (below) its Neutral Zone for today; session volatility is light. The Gold Update celebrates its 800th consecutive Saturday edition, still wary of near-term price pullback even as the weekly parabolic trend remains firmly Long; vis-à-vis its smooth valuation line Gold is (in real-time) +123 points “high” (see Market Values). At Market Trends, only Oil and the Spoo are in negative linreg; specific to their cac volumes, that for Oil is moving from April into May whilst for the Spoo from March into June. ‘Tis a busy week for the Econ Baro (plus Wednesday’s FOMC Policy Statement); 16 metrics come due, those for today including March’s NY State Empire Index and that for NAHB Housing, plus February’s Retail Sales and January’s Business Inventories.

The Gold Update: No. 800 – (15 March 2025) – “Beware the Ides of March — ‘Tis Gold Update No. 800!”

Long-time (really long-time) readers of The Gold Update know that our microphones are just about everywhere as was the case in Rome’s Curia Pompeia (a little Latin lingo there) on this day in 44 B.C. Let’s roll the tape:

- Soothsayer: “Hail Caesar!”

- Julius Caesar: “Whaddya got, Soothie…”

- Soothsayer: “We who embrace Caesar, whose name is magnificent, whose presence is ever-accessible, who makes our world wonderful, we turn our hearts to thee, oh Caesar…”

- Julius Caesar: “Oh just get on with it, Soothie…”

- Soothsayer: “Oh great Caesar! Beware the Ides of March! For on this very day 2,068 years hence shall come the 800th consecutive Saturday edition of The Gold Update!”

- Julius Caesar: “Soothie… Get out!”

Following which of course out came the long knives and the rest — as ’tis said — is “histoire”.

Welcome to the 800th Gold Update, our having missed nary a Saturday throughout. ‘Tis again a “milestone” for us, and we shan’t forget those who’ve substantively got us here, most notably the Mighty Moriarty of 321Gold, along with Goldseiten, Gold-Eagle, Kitco, Investing.com, TalkMarkets, GoldSeek and YOU: the most savvy Gold readers ’round the world. Our truly heartfelt thanks to everyone.

Moreover, welcome to Golden Goal Two, such “milestone” level of 3000 by the April futures contract having been reached this past Thursday evening @ 20:49 GMT with spot Gold then following yesterday (Friday) morning @ 10:10 GMT. A doubly-beautiful thAng!

Further, a hardened aspect of The Gold Update these many years is that when we’re way wrong, we so say! In this case, we’ve of late been anticipating Gold reaching lower price levels, certainly so from the week ending 28 February wherein Gold high-to-low fell -130 points from 2974 to 2844. Instead, 3000 was just tapped.

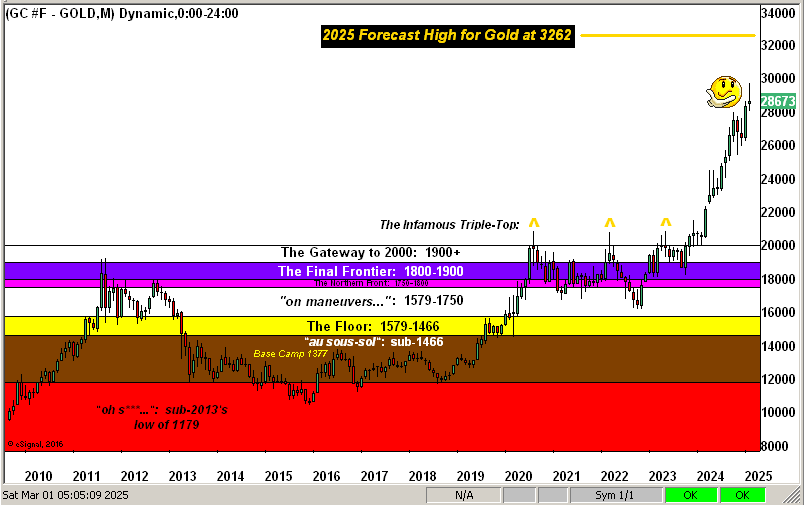

Indeed, whilst our Golden Goal Three for the year is still a projected a high of 3262, we’ve this reminder (from 04 January) as to Gold’s potential downside : “…applying the ‘expected yearly trading range’ method, the year’s low approximates…2507…” And should that eventuate, our sense remains it comes prior to 3262 ![]() “Goo goo g’ joob”

“Goo goo g’ joob”![]() –[Lennon, ’67].

–[Lennon, ’67].

But should we remain wrong (i.e. Gold not materially decline en route), ‘twould be great, for 3262 shall then appear in hindsight as having been a modest mandate.

Either way, Gold settled yesterday at 2994 in reaching a new All-Time High of 3017, the Monday-Friday net gain both by points (+76) and percentage (+2.6%) being the best of the year’s 11 weeks-to-date, within which (as aforenoted) only one has been down.

“Which begs the question mmb, is that an 11-week record? Congrats on 800 by the way…”

Thanks dear Squire: we couldn’t have made it this far without you. As for similar 11-week periods with but one (or even none) as down, on a mutually-exclusive basis ’tis happened century-to-date on seven other occasions, the prior case being within the grips of COVID from the weeks ending 29 May 2020 through 07 August 2020. Gold for that 11-week stint posted a net gain of +18.0%. This time ’round ’tis +13.5%. Regardless, as to “The Now”, all looks great in GoldLand:

Thus there we are for No. 800. It being a “milestone” for us in tandem with Golden Goal Two of price having achieved the 3000 “milestone”, let’s go to the stack. Therein note: nothing is listed in the 2800s. So swift has been Gold’s recent rise, that after having settled a total of 59 days in the 2600s and then 30 days in the 2700s, there’ve been but 11 settles in the 2800s, (just in case you’re scoring at home). Indeed, a word to the wise is sufficient. (What that means for you WestPalmBeachers down there is don’t be surprised should selling ensue). Here’s the stack:

The Gold Stack

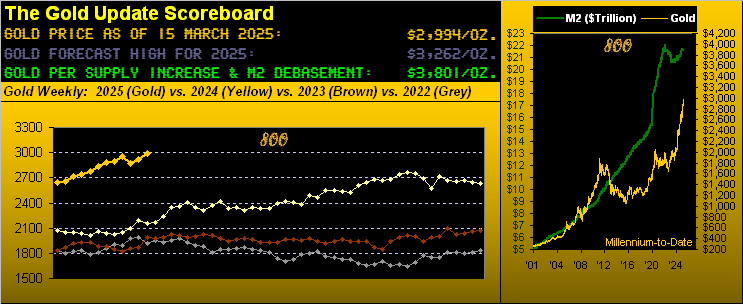

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3801

Gold’s All-Time Intra-Day High: 3017 (14 March 2025)

2025’s High: 3017 (14 March 2025)

10-Session directional range: up to 3017 (from 2870) = +147 points or +5.1%

Gold’s All-Time Closing High: 3001 (13 March 2025)

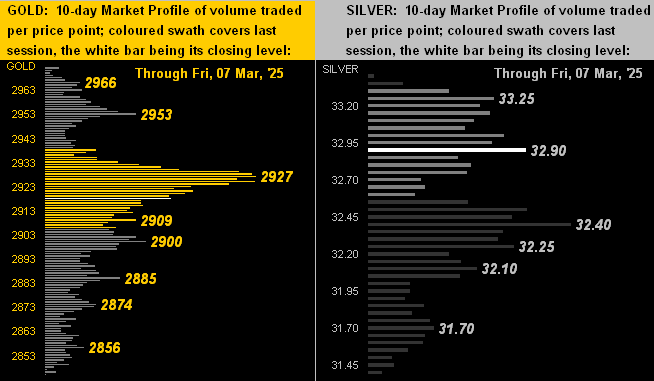

Trading Resistance: 2996

Gold Currently: 2994, (expected daily trading range [“EDTR”]: 43 points)

10-Session “volume-weighted” average price magnet: 2930

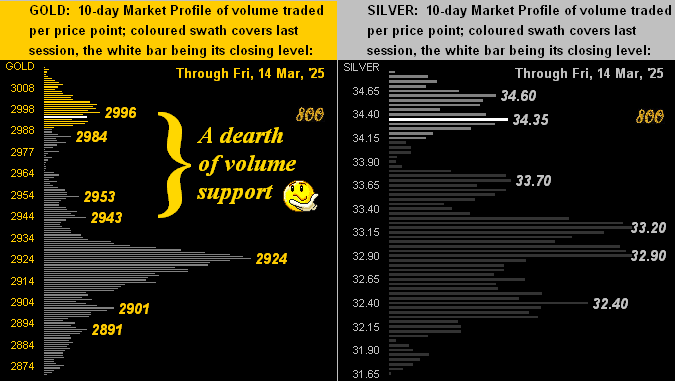

Trading Support: per the Profile, nothing substantive until 2924

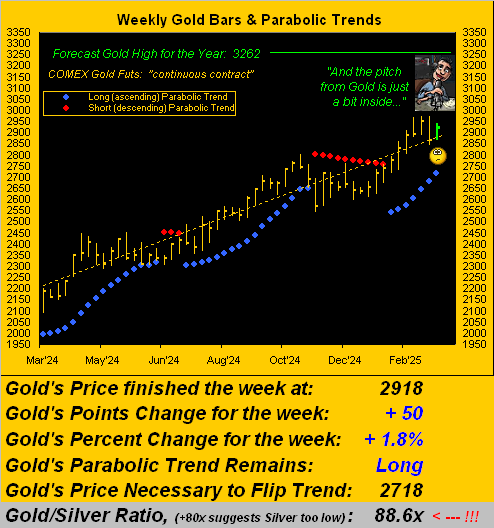

The Weekly Parabolic Price to flip Short: 2760

2025’s Low: 2625 (06 January)

The 300-Day Moving Average: 2479 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

To close it out, we again (as is on occasion a Gold Update tradition) grin over further “FinMedia Freakout!”. Our FinMedia friends pride themselves on their technical stock market expertise of which they know not just one, but two measures. They are called “The 200-day Moving Average” and “The 10% Correction”.

In this case, ’tis the latter which came to the fore across this past Thursday’s FinMedia spectrum as a result of the S&P 500 having reached down -10% from its recent all-time high of 6148, (the Index today at 5639). Rife was the air with panicky hysteria! From one FinMedia page to the next, the leading heading was nearly identical: “S&P 500 Enters Correction”. (Note: here at deMeadville, the correction commenced three weeks ago upon the S&P futures crossing below their own smooth valuation line as featured daily at the website, hint hint, wink wink, nudge nudge).

The good news is, by the time the FinMedia typically figures this out, ’tis oft a fabulous buy signal. Indeed prior to yesterday’s +117-point S&P rally, we internally texted it ought be bought. Boom! Following which came this hilarious rationale courtesy of CNBC: “Stocks bounced after a lack of new headlines out of the White House related to tariffs, easing concerns around escalating tensions for the time being.” (We’re curious as to how may hours may be the “time being”). The Ides of March, indeed. On verra…

That stated, we still view the S&P as treacherously overvalued en route to a down year. But counter to that remains the question: “Where then is COVID’s $7T ‘relief fund’ that all ended up in the stock market gonna go?”

“Which again begs the obvious question, right mmb?”

Better yet, Squire, as a statement: How about into Gold!

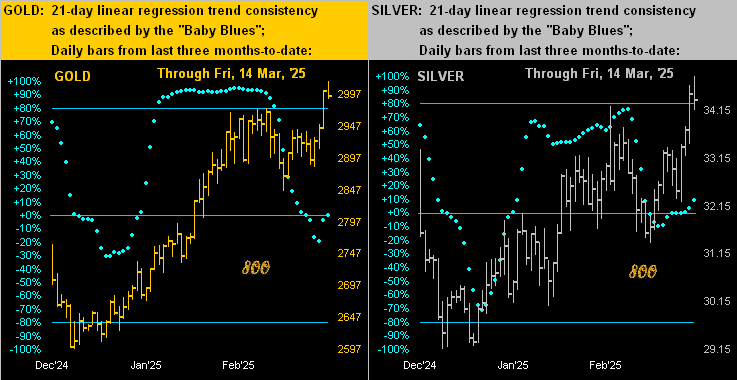

14 March 2025 – 08:32 Central Euro Time

April Gold topped 3000 last evening; spot (currently at a 12-point discount to the futures) has not quite yet made the trip; we’ve expected more of a price pullback which still can materialize; more on it all it tomorrow’s 800th consecutive Saturday edition of The Gold Update. At present, both the Euro and Swiss Franc are below today’s Neutral Zones; the other six BEGOS Markets are within same, and volatility is light. Cac volume in the EuroCurrencies is rolling from March into that for June; come Monday shall be the same for the Spoo. The FinMedia are all aghast that the S&P 500 has just “has entered a correction”, meaning we expect it to now rebound; by deMeadville’s Market Values, the “correction” began three weeks ago (21 February). The Econ Baro wraps its week with March’s UofM Sentiment Survey.

13 March 2025 – 08:44 Central Euro Time

Both the Euro and Silver are at present below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is mostly light. Looking at Market Rhythms for pure swing consistency, leading our 10-test basis is the Bond’s 2hr Parabolics, whilst on a 24-test basis are both the non-BEGOS Yen’s daily Parabolics and the Euro’s daily MACD. Oil looks poised to move above its Market Magnet: check the website post-close for confirmation thereto, as ‘twould suggest higher price levels near-term after being well down year-to-date; as noted yesterday, Oil is now -4.20 points below its smooth valuation line (see Market Values). Today’s incoming metrics for the Econ Baro include February’s PPI.

12 March 2025 – 08:43 Central Euro Time

The only BEGOS Market at present outside (below) today’s Neutral Zone is the Euro; session volatility is light in the context that EDTRs (see Market Ranges) are substantively up from year-end; notably that for the Spoo — which was 83 points as of 31 December — is for today 116 points, its highest reading since last 07 August. Looking at Market Values for the five primary BEGOS components, we’ve (in real-time) the Bond as as nearly +3 points “high” above its smooth valuation line, the Euro +0.0522 points “high”, Gold +54 points “high”, Oil -5.89 points “low” and the -476 points “low”, the S&P 500 itself now entering a 12th consecutive trading day as “textbook oversold”. The Econ Baro awaits February’s retail inflation, the CPI’s pace by consensus expected to have slowed a pip or two, albeit still above the Fed’s desired annualized rate; too, late in the session (purportedly) comes the month’s Treasury Budget.

11 March 2025 – 08:38 Central Euro Time

The Euro, Gold and Silver are at present above their respective Neutral Zones for today; none of the other five BEGOS Markets are below same, and session volatility is moderate. The S&P’s -2.7% decline yesterday was its worst since the -2.9% fall last 18 December, (prior to which was -3.0% last 05 August); obviously the leading aspects of our deMeadville analytics have been well ahead of the selling, technically by the Spoo’s linreg having already rotated to negative (see Market Trends) and fundamentally of course by the ongoing excessive overvaluation of the S&P given lack of earnings substance; by the Spoo’s Market Profile, overhead volume resistance spans the 5748-5797 zone. All that said, the S&P is now 10 consecutive trading days “textbook oversold”. Again, ’tis a quiet day for the Econ Baro ahead of February’s retail inflation (Wednesday) and wholesale inflation (Thursday).

10 March 2025 – 08:45 Central Euro Time

At present we’ve the Swiss Franc and Silver above today’s Neutral Zones; below same is the Spoo, and BEGOS Markets’ volatility is pushing toward moderate. The Gold Update cites the yellow metal having traced its first “inside” week year-to-date: our near-term bias remains for lower levels, and in real-time Gold’s linreg has rotated to negative (see Market Trends), the “Baby Blues” of trend consistency now below their 0% axis; by Market Profiles, Gold’s key line-in-the-sand is the volume-dominant 2927 level; and by Market Values, price in real-time is +66 points “high” above its smooth valuation line. The Econ Baro is quiet both today and tomorrow ahead of February inflation data later in the week. Too, the Spoo, Euro and Swiss Franc are due to see their cac volumes roll from March into June come week’s-end.

The Gold Update: No. 799 – (08 March 2025) – “Gold Goes Inside; Stocks Maintain Slide”

Whilst we’ve still our near-term negative bent for the price of Gold, nonetheless let’s reprise this from last week’s missive: “…one thing to watch is a stirring of geo-political jitters which as you regular readers know can quickly send Gold higher — but generally just briefly — before returning down from whence it came…”

And from the prior Friday’s White House brawl to yesterday morning’s RUS/UKR missile-drone attack, such geo-political jitters — in tandem with tariff tantrums — have kept Gold aloft, price settling the week at 2918 for a net five-day gain of +1.8% (+50 points).

Yet, ’twas a so-called “inside week” for the yellow metal, meaning Gold printed both a higher-low but lower-high than in the week prior. ‘Tis depicted below in the left hand panel wherein the outermost green and red horizontal lines are the prior week’s range and the innermost two this past week’s range, the diagonal slants showing the difference. Still, in spite of it all, Gold’s “Baby Blues” of trend consistency continued to fall, paired here with the S&P’s folderol and Silver’s attempting a grip on the ball:

“But mmb, that’s more than just S&P folderol ’cause it’s down -6% from its high!”

We’ve on occasion been queried if Squire is paid for such “teeing-up” comments. (Rather, for the privilege of his presence on this page, he pays us).

But to the point, yes, the S&P 500 (now 5770) has lost -6% of its value from the all-time high (6147) of just 13 trading days ago (19 February). Yet from our purview ’tis “nuthin’ but noise” given the mighty Index today is +765% above its FinCrisis low of 667 (06 March 2009) as well as +163% over the COVID low of 2192 (23 March 2020). Thus for you WestPalmBeachers down there, the S&P’s -6% pullback is a statistical irrelevancy. And as our regular readers know all too well, relevancy shall have returned upon the S&P’s price/earnings ratio (the “live” reading now 41.0x) having reverted to its reasonable mean in the low 20s, (which always has occurred — either up or down — since the S&P 500’s inception 68 years ago in March 1957) And in turn, the otherwise ongoing Investing Age of Stoopid shall have been eradicated. (Nevertheless, we’ve more on the FinMedia “Panic!” toward today’s wrap).

As to Gold’s ten trading weeks year-to-date, this past one (the rightmost green bar) is the first to be characterized as “inside”. Again, the inference as Gold continues to work off its extreme overbought condition is price having benefitted from geo-political and tariff trepidation; hence this past week’s buoyancy:

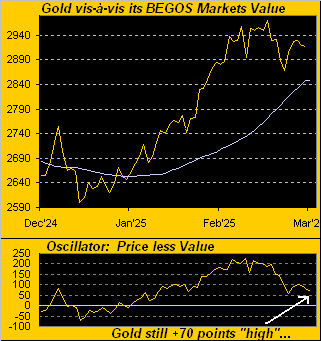

To be sure, Gold’s blue-dotted weekly parabolic remains safely Long. However, by our BEGOS Markets Values measure (in placing a near-term value on Gold per its movements relative to those of the four other primary BEGOS components, i.e. the Bond, Euro, Oil and S&P 500), price is still some +70 points “high” above its smooth grey valuation line; and of course, the two inevitibly shall eventually meet. Here they are from three months ago-to-date:

And again as you well know, we fully expect Golden Goal Two of “milestone” 3000 to trade this year, and further our forecast high for Golden Goal Three of 3262. Yet as the “Not in a Straight Line Dept.” reminds us, we see the route thereto traveling through the 2703-2641 zone, just in case you’re scoring at home.

‘Course, how lovely ‘twould be to be wrong and instead see Gold proceed from here at 2918 right up the road to the opening Scoreboard’s Dollar debasement value of 3798. Highly unlikely anytime soon, although in responding at a gathering this past week to the query “Is Gold now going to 10,000?” we said “No, and likely somewhat lower near-term, yet 4,000 perhaps is possible in two years or so…”

But obviously the bogeyman in the room is inflation — which most broadly is a Gold positive — but intermediately a threat to price should the Federal Open Market Committee resort to raising rates. The good news there, however, is both retail and wholesale inflation by consensii are expected to have somewhat slowed their February paces from those for January. Next Wednesday (the Consumer Price Index) and Thursday (the Producer Price Index) shall tell the tale.

Indeed let’s segue to the Economic Barometer which took a bit of a boffing during the week. Of the 15 incoming metrics, only five improved period-over-period. Most impressive were January’s Factory Orders which increased from December, that month’s decrease being favourably revised, and which beat consensus. But the stinker was the backup in January’s Wholesale Inventories, which accumulated over those for December, that month’s depletion revised to a slower pace, and were a bit more bloated than consensus. Too came the not so rare dichotomy of February’s Payrolls taking a rather severe hit per ADP, but by the Bureau of Labor Statistics actually increased. “What’s your source?” Here’s the Baro:

Toward closing, in light of the S&P 500 (which year-to-date is now down -1.9%, “OMG!”) having just recorded its weakest week (-3.1%) of the ten thus far this year, as we earlier teased, let’s check in with a few of Friday’s “FinMedia Freakout” finales:

Bloomy: “Wall Street’s Big Selloff Puts Pressure on America’s Rich Households” Lovin’ this one, for how many times have we written: “Marked-to-market everyone’s a millionaire; marked-to-reality nobody’s worth squat”;

DJNw: “Most Americans can’t afford life anymore…” So is DJNw’s assumption here the alternative? That’s a bummer.

CNBS: “The oversold stocks due for a technical bounce after a brutal week.” Truly ’tis dumbing down of the word “brutal”; we’ve haven’t had “brutal” since March 2020; and from 2008 into 2009, we regularly ate “brutal” for breakfast. So what leads to “brutal”? The aforenoted “live” S&P P/E of 41.0x.

“So then is the S&P about to crash, mmb?”

Obviously no one knows, Squire. What will eventuate over time is the reversion of the S&P’s P/E to a level of normalcy, as earlier cited in the low 20s via: 1) a doubling in earnings without the stock market rising, or 2) a 40%-50% stock market “correction”, or 3) a![]() “Combination of the Two”

“Combination of the Two”![]() –[Big Brother and the Holding Company, ’68]

–[Big Brother and the Holding Company, ’68]

Either way, we wrap with a wry note: per this penning, there remain two full weeks of winter. Yet for some reason of absurdity, StateSide folks early tomorrow move their clocks to summer hours. What that means for The Gold Update is — by adhering to its time-honoured traditional uploading each Saturday at 11:00 PacCoastTime — ’twill be an hour earlier here EuroSide at 19:00 for our next three editions (15, 22 and 29 March) until we then nudge our clocks forward come 30 March.

And specific to next week’s piece, beware the Ides of March, for it brings our 800th consecutive Saturday edition of The Gold Update…

He had Gold … do you? Currency then … Currency NOW!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

07 March 2025 – 08:40 Central Euro Time

StateSide ’tis February’s Payrolls day for the Econ Baro (and late in the session January’s Consumer Credit). At present we’ve the Bond, Euro, Swiss Franc and Oil all above their respective Neutral Zones for today; volatility for the BEGOS Markets is light. The S&P 500 remains “textbook oversold” such that a so-called “dead cat bounce” may be warranted; however the Index’s broader technical picture is facing a negative crossover on the monthly MACD that seemingly can confirm into April; given the unsustainably high “live” P/E of 40.4x, the S&P ought deservingly suffer rough sledding at least over the near-to-medium term, especially with the short-term U.S. Treasuries yielding better than triple that of the S&P (4.197% vs. 1.343%). ‘Tis to worthy to note that from the S&P’s March 2009 low, the Index has increased by as much as 822%: thus this 7% pullback is essentially noise; indeed were it not for COVID and the monetary creation thereto, the S&P today (5739) would instead be ’round 3000.

06 March 2025 – 08:44 Central Euro Time

Presently we’ve the Bond below its Neutral Zone for today, whilst Oil is above same; the BEGOS Markets’ volatility for this time has calmed to mostly light. Amongst the five primary BEGOS components, we’ve now a positive correlation between the Euro and Gold, which makes sense give the Dollar’s demise notably this week. Copper’s +4.9% net gain yesterday was the largest since 04 November 2022: at Market Trends, Copper’s rally was sufficient to stall the otherwise falling “Baby Blues” of trend consistency. Meanwhile, that measure for the Spoo continues to drop, albeit the S&P 500 itself is now seven days “textbook oversold”; still, the “live” P/E of the S&P (futs-adj’d) is a horribly high 43.1x. Today’s incoming metrics for the Econ Baro include January’s Trade Deficit and Wholesale Inventories, plus the revisions to Q4’s Productivity and Unit Labor Costs.

05 March 2025 – 08:38 Central Euro Time

The Euro, Silver and Copper are all at present above today’s Neutral Zones; the other five BEGOS Markets are within same, and session volatility is moderate-to-robust, Copper notably having traced 170% of its EDTR (see Market Ranges). As has oft been the case of late, we’ve no notable correlations amongst the five primary BEGOS components. In looking at Market Rhythms for pure swing consistency, our 10-test basis cites the Swiss Franc’s 1hr Parabolics as best, whilst on a 24-test basis we show both the non-BEGOS Yen’s daily Parabolics and the Euro’s daily MACD. The Dollar Index has thus far traded today down to its lowest level (105.280) since 11 November, Gold getting a bit of a bid in the balance, albeit to the extent ’tis geo-politically driven, we look for Gold to resume working lower (as detailed in the current edition of The Gold Update). The Econ Baro awaits February’s ADP Employment data and ISM(Svc) Index, plus January’s Factory Orders. Then late in the session brings the Fed’s Tan Tome.

04 March 2025 – 08:41 Central Euro Time

Both the Bond and Swiss Franc are at present above today’s Neutral Zones, whilst below same are Copper and Oil; session volatility for the BEGOS Market’s is moderate, (which you may be noting is the case ’round this time more frequently of late). Yesterday’s whirl back down in the S&P 500 ought not be too much of an eyeopener given the Spoo’s 21-day linreg trend having last week rotated from positive to negative, as presently is the stance as well for both Silver and of course Oil over recent weeks; by Market Trends, those for the other five BEGOS components are positive; however Gold’s “Baby Blues” of trend consistency are in freefall as are those for Copper. Too for the S&P per our Moneyflow page, all three time bases (weekly, monthly, quarterly) point to still lower levels ahead for the Index. Nothing is due today for the Econ Baro with then 13 incoming metrics remaining from tomorrow through the week’s balance.

03 March 2025 – 08:29 Central Euro Time

At present the Bond is below its Neutral Zone for today, whilst above same is the Euro; the BEGOS Markets’ volatility is mostly moderate. The Gold Update cites the anticipated fall having commenced for the yellow metal; as written: “…should the present selling become more substantive … ‘twould be reasonable to find price reach down into the 2703-2641 zone…” By Market Values, Gold — after having been better than +200 points “high” above its some valuation line — is now +56 points “high”. Notably too by that same metric, the Bond remains nearly +4 points “high”, the Euro basically in line, Oil -4.55 points “low” and the Spoo -104 points “low”. Despite the S&P 500’s +1.6% Friday rally, the Index is actually mildly “textbook oversold”; more meaningfully however, the overall weak level of earnings doesn’t support the “live” P/E of 44.0x. Q4 Earnings Season is complete with 69% of the S&P’s constituents bettering their bottom lines from Q4 a year ago, an above-average showing over 66% for the past eight years. The Econ Baro begins its week of 15 incoming metrics with February’s ISM(Mfg) Index and January’s Construction Spending.

The Gold Update: No. 798 – (01 March 2025) – “Thank Goodness Gold Finally Falls”

‘Course contra to our wary stance — courtesy of the FinMedia — emerged the “Suddenly Everybody’s a Gold Expert Dept.” proclaiming the price of 3000 being imminent. And thus it did not happen, oft normal in such market-amateur hysterias.

Rightly instead, Gold as anticipated whirled ’round down to record its third worst week in better than a year, this time dropping -2.8% (-82 points) in settling yesterday at 2867. Or to put it to music, we cue the Swiss rock band Gotthard from their ’07 song “The Call”: ![]() “The higher they fly, the harder they fall…”

“The higher they fly, the harder they fall…”![]()

“And, mmb, that really applies now to the stock market, eh?”

Frighteningly so, Squire. Indeed to quote George Kennedy in “The Eiger Sanction” (Universal, ’75): “They won’t even know it’s coming until it hits.” Or as a valued charter reader of The Gold Update has on occasion queried: “Does it really matter which snowflake causes the avalanche?”

Then this past Thursday (per our daily Prescient Commentary) came Gold’s “Baby Blues” of trend consistency at long last breaking down below their +80% axis (as we’ll later see), which is key in having generated this signal in the end-of-day work spree:

“The obvious question then is, mmb?”

Squire, “How low is low?” Thus here we go: should the present selling become more substantive from the current 2867 level, ‘twould be reasonable to find price reach down into the 2703-2641 zone. To be sure: we still expect Golden Goal Two of “milestone” 3000 to eventually trade, directly or indirectly en route to Golden Goal Three of 3262 as our forecast high for this year. But as we’ve herein reminded since New Year (Gold then 2639), the road to 3262 can quite fairly pass through the lower 2500s. Is that to where this down run is heading? Nobody knows. But ’tis better to get the year’s low place before the high.

And as we been emphasizing, a wayward wrench dropped into the Gold works is inflation. Recall our title from two missives ago included the phrase “Fed’s Next Hike”. Apparently “hike” is not an allowable utterance at large. Rather, press musings oscillate between “cut” and “pause”, with a lean of late toward the latter. This results from their not implementing math. Most notably came yesterday’s “Fed-favoured” inflation report for January’s Personal Consumption Expenditures. The headline number — rather than easing — remained steady at +0.3% whilst the core number’s pace increased from +0.2% to +0.3%. Here thus is our inflation summary for January:

As for yesterday’s S&P 500 big post-White House brawl rally, we eye it as a “dead cat bounce” given the significant deterioration of late in the Index’s Moneyflow regressed into S&P points. By the website’s S&P Moneyflow page, the Index per this leading indicator “ought be” some 180-to-230 points lower than currently ’tis (5955). Still, a tip of the cap to just concluded Q4 Earnings Season: therein, 454 S&P 500 constituents reported, 69% of them bettering their bottom lines from a year ago, which across the past 31 reporting quarters has averaged 66%. But as we point out ad nauseam, the overall level of earnings remains terribly weak given the price of the Index, the “live” price/earnings ratio of the S&P now 43.3x. So stay suspect when it comes to stocks.

Not suspect a wit (per the “SELL” in the table earlier displayed) is the inevitable cascade in Gold’s “Baby Blues”, the red-encircled dot below confirming such signal. So as is our month-end wont, here we go ’round the horn for all eight BEGOS components across the past 21 trading days (one month). And you know the jingle: ![]() “Follow the blues, instead of the news, else lose yer shoes”

“Follow the blues, instead of the news, else lose yer shoes”![]() :

:

So thus far for 2025 we’ve two months down (both net-net up for Gold) and ten to go. As noted, in the year’s balance remain Golden Goal Two of “milestone” 3000 and our projected Golden Goal Three of 3262 for the high. Yet ahead of such ascent we’ve this current descent, for which as stated we are thankful given major markets are not unidirectional. However, one thing to watch is a stirring of geo-political jitters which as you regular readers know can quickly send Gold higher — but generally just briefly — before returning down from whence it came. Either way, in the words of The Gold Update’s first ever reader away back in 2009 (JGS): “We’ll watch it together.”

So be a cool cat and stay with your Gold!

28 February 2025 – 08:42 Central Euro Time

Gold’s “Baby Blues” (see Market Trends) confirmed falling below their key +80% axis, indicative of still lower prices; more tomorrow in the 798th consecutive Saturday edition of The Gold Update. Along with the yellow metal at present, Copper, Oil and the Swiss Franc are all below today’s Neutral Zones; above same is the Bond, and BEGOS Markets’ volatility is firmly moderate. The Moneyflow of the S&P 500 continues to be weaker than the down move in the Index itself: yesterday’s change in the S&P was -1.6%, however the Money suggested a change of -3.1%: as this is a leading indicator, we look for further selling in the S&P; mind our S&P Moneyflow page. ‘Tis the final day of Q4 Earnings Season. And the Econ Baro wraps its week, indeed the month, with February’s Chi PMI plus January’s Personal Income/Spending and “Fed-favoured” Core PCE.

27 February 2025 – 08:45 Central Euro Time

Both the Swiss Franc and Gold are below today’s Neutral Zones; the other six BEGOS Markets are within same, and volatility is again moderate, although like yesterday ’round this time, Oil has traced but 18% of its EDTR (see Market Ranges). At Market Trends, Gold’s “Baby Blues” of trend consistency are provisionally (in real-time) dropping below their key +80% axis, indicative (upon confirmation) of lower prices near-term: recent missives of The Gold Update have been anticipative of a run down; looking at Market Values in real-time, Gold is +107 points “high” above its smooth valuation line. By that metric for the other four primary BEGOS components: the Bond shows as nearly +4 points “high”, the Euro as essentially in line, Oil as -6.25 points “low” and the Spoo now as -76 points “low”. The week’s selling in the S&P 500 has actually pushed it down into “textbook oversold” territory, however the Index remains dangerously high by its “live” (futs-adj’d) P/E of 44.6x. Included in today’s incoming metrics for the Econ Baro are January’s Durable Orders and Pending Home Sales, plus the first revision to Q4 GDP.

26 February 2025 – 08:40 Central Euro Time

The Bond and the EuroCurrencies are at present below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility is moderate, save for Oil which has traced just 15% of its EDTR (see Market Ranges). For the S&P 500, similar to that from Monday, on Tuesday whilst the Index fell -0.5%, the Moneyflow was instead suggestive of a -1.6% fall, again indicative of further selling still to come (see our S&P Moneyflow page). The Spoo’s 21-day linreg trend confirmed rotating to negative, the “Baby Blues” of trend consistency now having moved below their 0% axis (see Market Trends); should the selling turn more substantive, we’d look in due course for the S&P 5400s. The Bond’s cac volume is rolling from March into June, whilst that for Silver from March into May. And the Econ Baro awaits January’s New Home Sales.

25 February 2025 – 08:35 Central Euro Time

The Bond is above its Neutral Zone for today, whilst below same are Gold and Copper; session volatility for the BEGOS Markets is light. As anticipated, in real-time the Spoo’s 21-day linreg trend line has rotated to negative (see Market Trends) as has been that for Oil for the past few weeks; such trend for the other six BEGOS components is positive, albeit with weakening “Baby Blues” (which depict trend consistency) in decline for the Bond and all three elements of the Metals Triumvirate. The MoneyFlow of the S&P 500 was notably more negative yesterday (-1.2%) than that of the Index itself (-0.5%), suggestive of lower price levels near-term. The Econ Baro looks to February’s Consumer Confidence.

24 February 2025 – 08:41 Central Euro Time

Into the new week we’ve presently both the Euro and Spoo above today’s Neutral Zones; none of the other BEGOS Markets are below same, and volatility is mostly moderate. The Gold Update (as was the case a week ago) gives a near-term bearish bias strictly by technicals and the deMeadville proprietary measures (see Gold under BEGOS Markets): an affective metric this week shall be Friday’s release of PCE inflation data; either way, Gold completed an eighth consecutive up week for just the fifth time (mutually-exclusive basis) this century and currently priced at 2954 is -46 points below “Golden Goal Two” of “milestone 3000”. Nothing is due today for the Econ Baro. And, barring laggards, this is the final week of Q4 Earnings Season: with 402 S&P 500 constituents thus far having reported, 69% have improved their bottom lines from Q4 of 2023, a somewhat better-than-average improvement pace; problematic remains the extreme 45.2x P/E ratio.

The Gold Update: No. 797 – (22 February 2025) – “Gold Higher Every Week Year-to-Date”

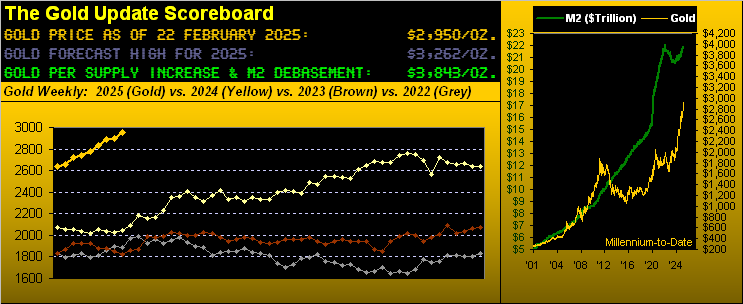

Speaking of scoring, to wrap, the U.S. Treasury (as you’ve no doubt read) presently “scores” the United States Bullion Depository supply of Gold at $42/oz. Therein said facility — just on the outskirts of Fort Knox, Kentucky — is “officially” (in round numbers) some 147,300,000 ounces of Gold according to “AI” (“Assembled Inaccuracy”), for an accounting value of $6,174,000,000. That is how much the U.S. Federal Government spends about every 10 hours. (Do the math if you must, starting with the annual spend of $6,740,000,000,000). Makes ya feel kinda small, what? However: marked-to-market at $2950/oz. puts the value — were it all liquidated at that price — to a supply total of $433,650,000,000 which essentially would run the federal government for one month. That’s it.

Au contraire Auric. Even if near-term the yellow metal gets sold, you can buy a lot of mint juleps with an ounce of Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

21 February 2025 – 08:35 Central Euro Time

Copper is the sole BEGOS Market at present outside (below) its Neutral range for today; however, session volatility is pushing toward moderate. Gold indeed made another marginal All-Time High yesterday in reaching 2973 (from the prior 2968); as you well know, the yellow metal — whilst still significantly undervalued vis-à-vis Dollar debasement — is extremely near-term overbought: more in tomorrow’s 797th consecutive Saturday edition of The Gold Update. The Spoo’s EDTR (see Market Ranges) has been narrowing since a recent peak at 93 points on 07 January: through yesterday, ’tis now 64 points; again, we’re minding the Spoo’s 21-day linreg trend (see Market Trends) for its rotating from positive to negative. The Econ Baro wraps its week with metrics which include January’s Existing Home Sales.

20 February 2025 – 08:31 Central Euro Time

The Swiss Franc, Gold and Silver are all at present above their respective Neutral Zones for today; none of the other BEGOS Markets are below same, and volatility is light, (save for the non-BEGOS Yen which has traced 103% of its EDTR, which for the BEGOS components can be seen at Market Ranges). Correlations amongst the five primary BEGOS components have been messy of late with no notably directional pairings therein. Gold appears poised to set another All-Time High (above 2968) as the day unfolds: the high thus far this session is 2967. The S&P 500 is entering its 21st consecutive trading day as “textbook overbought”; the Spoo’s “Baby Blues” look to slip into negative territory within the next few sessions as the linreg trend rotates to negative, (barring a firm rally). And amongst the metrics due for the Econ Baro are February’s Philly Fed Index and January’s Leading (i.e. “lagging” given the Baro) Indicators.

19 February 2025 – 08:33 Central Euro Time

At present, only Oil is outside (above) today’s Neutral Zone; session volatility for the BEGOS Markets is quite light. Looking at Market Rhythms for pure swing consistency, on a 10-test basis the best currently are the Bond’s daily Moneyflow, Copper’s 30mn Price Oscillator as well as the red metal’s 2hr Parabolics; on a 24-test basis our leaders are (as oft has been the case) the non-BEGOS Yen’s daily Price Oscillator and daily Parabolics, plus the Euro’s 4hr MACD. The flow into Gold is being maintained, price (2950) in real-time +203 points above its smooth valuation line; today marks the 22nd consecutive trading session for Gold with its “Baby Blues” (see Market Trends) above their key +80%, a stretch which for any BEGOS Market is remarkable. The Econ Baro looks to January’s Housing Starts/Permits; and late in the session come the Minutes from the FOMC’s 28/29 meeting.

18 February 2025 – 08:48 Central Euro Time

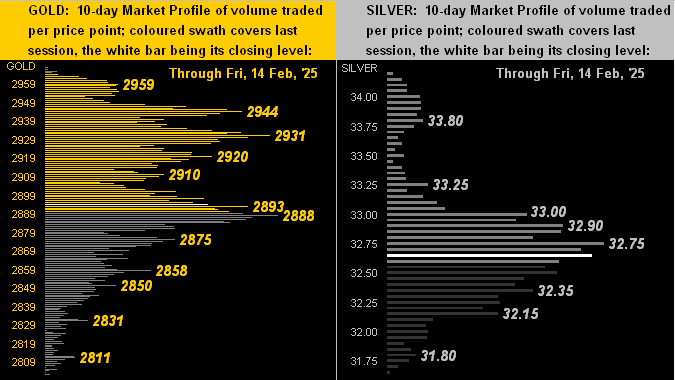

Into the session’s second day, as expected the BEGOS Markets have increased their range traveled: at present below their Neutral Zones are the Bond, Euro, Swiss Franc and Copper, whilst above same are Gold, Silver, Oil and the Spoo, with overall volatility firmly moderate, leaning toward robust as the day develops. Were the S&P 500 to open at this instant, ‘twould be at an all-time high of 6140 (vs. the actual-to-date of 6128). Going ’round the Market Values horn for the five primary BEGOS components (in real-time), we show both the Bond and Euro as nearly on their smooth valuation lines, Gold as +185 points “high” above same, Oil -4.35 points “low” and the Spoo as +94 points “high”. With Gold at 2925, the volume-dominant overhead Market Profile resistors are 2931 and 2944. The Econ Baro awaits February’s NY Empire State and NAHB Housing Indices.

17 February 2025 – 08:42 Central Euro Time

The BEGOS Markets begin the week with a two-day session (for Tuesday settlement); at present, we’ve the Bond below today’s Neutral Zone, whilst above same is Gold; session volatility already is pushing toward moderate and likely by this time tomorrow shall be mostly robust. The Gold Update graphically depicts last week’s price spike to the new All-Time High of 2968; still, we are cautious of Gold’s near-term extensive stance, seven consecutive up weeks now recorded; price is “textbook overbought” for the last 25 trading days, and (in real-time) ’tis +171 points above it smooth valuation line (see Market Values). Too, the inflation scare has us once again musing of the Fed potentially having to revert to raising rates. To this point in Q4 Earnings Season, 361 S&P 500 constituents have reported, of which 70% have bettered their bottom lines from Q4 of 2024: again, that is an above-average rate of improvement, albeit the Index itself remains catastrophically high with the “live” (futs-adj’d) P/E at this instant 47.8x.

The Gold Update: No. 796 – (15 February 2025) – “Gold’s Price Spike; Fed’s Next Hike”

So if you are thinking that we are thinking “down” is Gold’s watchword for this ensuing week, yes we agree, albeit as aforementioned, price of late is being headline-driven. Still as we turn to the stack, Gold year-to-date is well in the black:

The Gold Stack

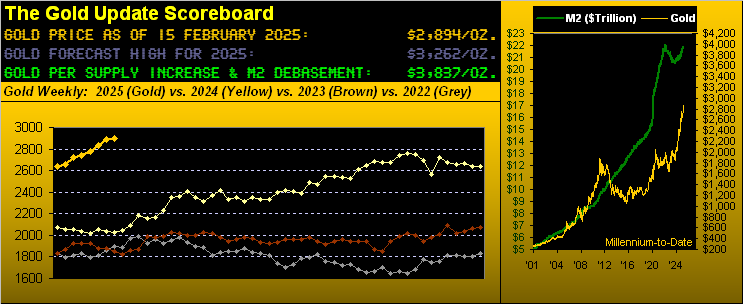

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3837

Gold’s All-Time Intra-Day High: 2968 (11 February 2025)

2025’s High: 2968 (11 February)

10-Session directional range: up to 2968 (from 2802) = +166 points or +5.9%

Gold’s All-Time Closing High: 2957 (13 February 2025)

Trading Resistance: notable overhead Profile nodes 2931 and 2944

10-Session “volume-weighted” average price magnet: 2903

Gold Currently: 2894, (expected daily trading range [“EDTR”]: 34 points)

Trading Support: most notably 2888, then 2875

2025’s Low: 2625 (06 January)

The Weekly Parabolic Price to flip Short: 2607

The 300-Day Moving Average: 2424 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Next week brings just a moderate dose of data for the Econ Baro, notable of which come Thursday (20 February) is the Conference Board’s Leading Indicators for January. Again for regular readers, you know our penchant for referring to such metric as “lagging” given the Baro has already told the tale. Thus the consensus for a flat January — or maybe +0.1% at best — makes sense.

Just ensure your Gold and Silver portfolio shares are many percent!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

14 February 2025 – 08:25 Central Euro Time

We’ve both Silver and Copper at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is mostly light, save for Silver which already has traced 110% of its EDTR (see Market ranges). Barring January being an outlier, the pace of inflation is increasing away for the Fed’s +2.0% preference; more tomorrow in the 796th consecutive Saturday edition of The Gold Update; to that end, Gold thus far today has traded up to 2064, just 4 points shy of its 2068 All-Time High achieved this past Tuesday; as a caution, Gold in real-time is +226 points “high” above its smooth valuation line (see Market Values). Too in real-time, Oil’s “Baby Blues” have provisionally moved above their -80%; as previously noted, confirmation of that condition typical brings higher prices near-term. And ’tis a busy day to end the week for the Econ Baro, scheduled metrics being January’s Retail Sales, Ex/Im Prices and IndProd/CapUtil, plus December’s Business Inventories.

13 February 2025 – 08:25 Central Euro Time

The Euro, Swiss Franc, Gold and Copper are all at present above today’s Neutral Zones; none of the other BEGOS Markets are below same, and volatility is mostly moderate. The Bond’s “Baby Blues” (see Market Trends) confirmed settling below their +80% axis: price already has moved lower into structural support of the 113s; were that to crack, a re-test of January’s lows in the 110s would be in order, especially should inflation be re-accelerating. By that same study, Oil’s “Baby Blues” are mildly curling back upward (-81% in real-time): a settle above -80% would suggest higher price levels; too, Oil’s cac volume is rolling from March into April. And the Econ Baro awaits January’s wholesale inflation data via January’s PPI.

12 February 2025 – 08:35 Central Euro Time

At present, all eight BEGOS Markets are within their respective Neutral Zones for today, and session volatility is light with January’s retail inflation metrics in the balance. Going ’round the Market Rhythms horn for pure swing consistency, currently the leaders (on a 10-test basis) are the Bond’s daily Moneyflow, the Euro’s 30mn Parabolics, Copper’s 15mn Price Oscillator, and the non-BEGOS Yen’s daily Parabolics; too, (on a 24-test basis) is again the Yen’s daily Parabolics as well as its daily Price Oscillator, plus the Euro’s 4hr MACD. And at Market Trends, despite the Spoo’s being in a 21-day linreg uptrend, its “Baby Blues” of the trend consistency are dropping for the fourth consecutive session. As noted, the Econ Baro awaits January’s CPI, plus (purportedly) late in the session the Treasury’s Budget. And per Humphrey-Hawkins, FedChair Powell, having testified yesterday before The Senate, concludes today with The House.

11 February 2025 – 08:47 Central Euro Time

Both Silver and Copper are at present below today’s Neutral Zones; the six other BEGOS Markets are within same, and session volatility is light-to-moderate. The S&P 500 is now “textbook overbought” through the past 14 consecutive trading days: there were significantly longer overbought stints during 2024, but ’tis something of which to be aware, especially given the “live” (futs-adj’d) P/E now at 48.8x and a yield of 1.243% less than a third of that for the 3mo US T-Bill of 4.228% annualized. At Market Trends we’re minding the Bond’s “Baby Blues” of trend consistency which are just starting to roll over to the downside with inflation data due both tomorrow and Thursday. And at Market Values the most extreme deviation is Gold’s being (in real-time) +216 points “high” above its smooth valuation line, pricing reaching another All-Time High earlier today at 2968. Again, ’tis a quiet session for the Econ Baro.

10 February 2025 – 08:34 Central Euro Time

The week starts finding at present the Swiss Franc below today’s Neutral Zone, whilst above same are both Gold and Silver; BEGOS Markets’ volatility is moderate. The Gold Update muses the 3000 level as within reasonable distance by month’s end, however cautions that price has risen for six consecutive weeks (which historically is a bit of an outlier); still, the weekly parabolic trend is Long and we maintain our forecast high for this year at 3262; more immediately, Gold (in real-time) is +200 points “high” above its smooth valuation line (see Market Values); too, price is quite stretched above its 300-day moving average, (nearly +20%). Q4 Earnings Season continues to run at an above average pace for S&P 500 constituents bettering their bottom lines from Q4 a year ago: 71% of the 286 reports thus far have so done; ‘course it remains very problematic that the overall level of S&P 500 earnings is too low to support the extremely high Index itself, (the “live” futs-adj’d P/E at this instant 48.4x). ‘Tis a back-loaded week for the Econ Baro with 13 metrics due beginning on Wednesday.