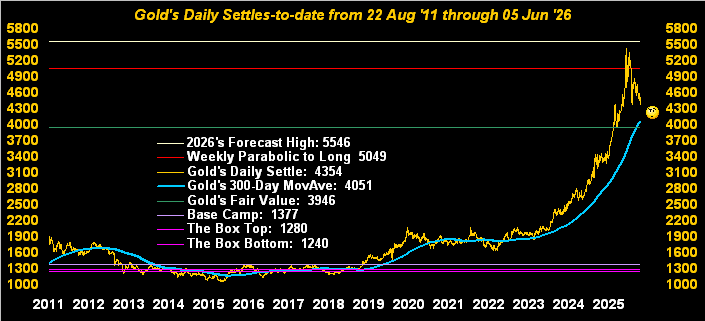

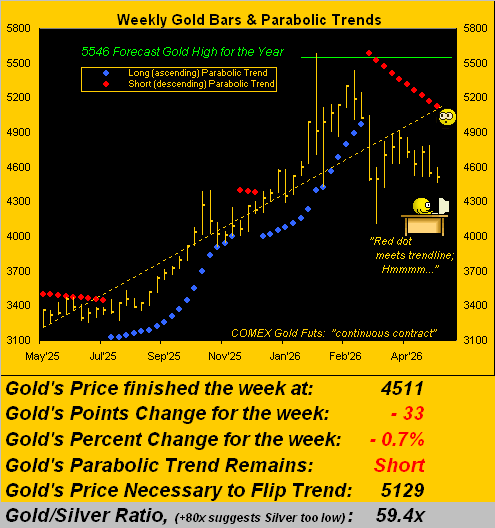

Gold is at present below its Neutral Zone for today; the balance of the BEGOS Markets are within same, and session volatility is light-to-moderate. After trading to the year’s low (4046) yesterday, Gold intra-day recovered nearly +200 points; either way, is Gold returning to Fair Value ’round 3948? More in tomorrow’s 865th consecutive Saturday edition of The Gold Update. Our best Market Rhythms for pure swing consistency are currently dominated by both Copper and Gold: on a 10-test basis, the Top Three rankings are Copper’s 2hr Parabolics, Gold’s daily Moneyflow and Copper’s 2hr MACD; for the 24-test basis they are Copper’s 30mn Price Oscillator and again the 2hr MACD, plus Gold’s 1hr MACD. For the Euro, Swiss Franc and non-BEGOS Yen, cac volume is rolling from June into that for September. And the Econ Baro concludes its week with June’s UofM Sentiment Survey.

Mark

Mark

11 June 2026 – 08:43 Central Euro Time

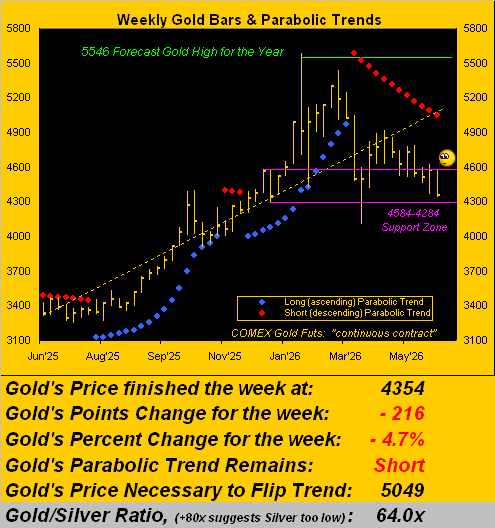

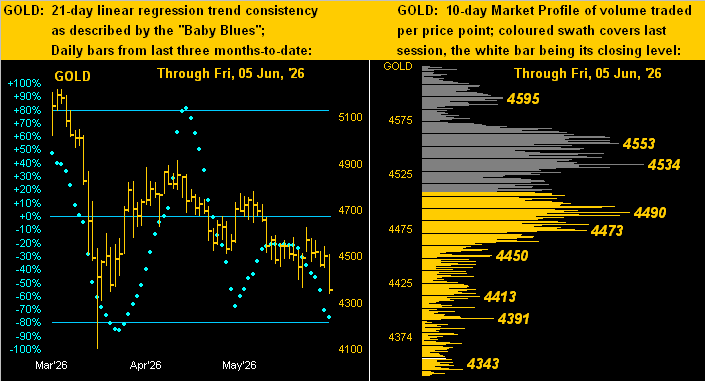

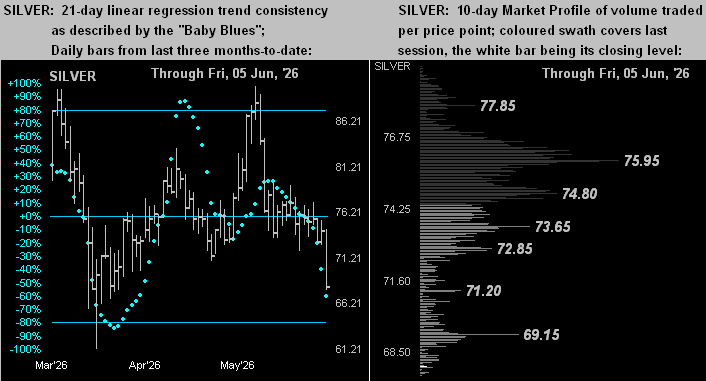

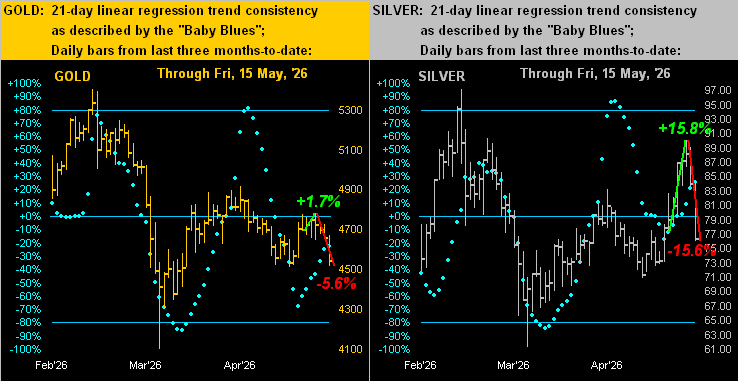

We’ve fresh Gold lows for the year, the yellow metal having today reached down to 4046, albeit ’tis since bounced to now 4107, indeed back inside of today’s Neutral Zone; below same is Oil whilst above same is the Spoo, and session volatility for the BEGOS Markets is moderate. Gold’s best Market Rhythm for pure swing consistency has been the daily Moneyflow which flipped to Short effective 28 April’s opening at 4698; too, by Market Trends, Gold’s “Baby Blues” of linreg consistency dropped below their key +80% axis back on 22 April, price having settled that session at 4758. And per its Market Profile, Gold’s “nearby” volume-dominant resistors are 4193, 4289, 4318 and 4352. today’s EDTR (see Market Ranges) being 115 points. Econ Baro incoming metrics for today include May’s PPI, (the month’s “Fed-favoured” PCE not coming due until 25 June during the week following the FOMC’s next Policy Statement of 17 June).

10 June 2026 – 08:39 Central Euro Time

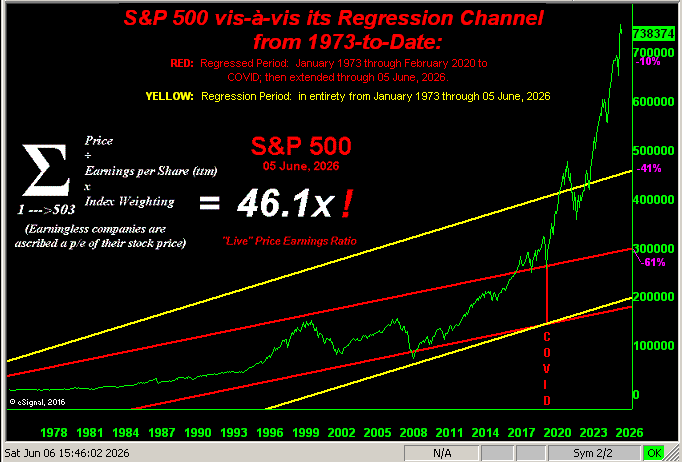

Gold, Copper, Oil and the Spoo are all presently below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility again is pushing toward moderate. By Market Values, the Bond yesterday settled above its smooth valuation line for the first time since 02 March, albeit as yields have been a bit pressured, price itself has not spent too many days above valuation going back a year or so-to-date. Indeed in going ’round the Market Values horn (in real-time) for the five primary BEGOS components, the Bond shows as +0^14 points “high”, the Euro as -0.003 points “low”, Gold as -357 points “low”, Oil as -9.97 points “low” and the Spoo as +114 points “high”; by Market Trends, the Spoo’s 21-day linreg trend looks to rotate to negative by week’s-end. The S&P 500 after having been technically “textbook overbought” through 42 consecutive trading days finally unwound that condition yesterday; ‘course, fundamentally the “live” (futs-adj’d) P/E of 46.2x remains stratospheric. The May inflation parade beings today as the Econ Baro looks to the CPI, plus late in the session comes the month’s Treasury Budget.

09 June 2026 – 08:35 Central Euro Time

At present we’ve the Euro, Swiss Franc, Copper and Spoo all above their respective Neutral Zones for today; below same is Oil, and BEGOS Markets’ volatility is pushing toward moderate. In concert with the Spoo’s “Baby Blues” now in full cascade (see Market Trends), the S&P 500 (following Friday’s -2.6% fall) yesterday attempted a “relief rally”, at one point having recovered +1.1%, to then settle but +0.3%; our sense remains a fairly near-term return for the S&P down to at least the 6800s, especially as other entities eventually perceive the current rotation of trend toward negative; the Spoo’s best Market Rhythm for pure swing consistency has been its 30mn MACD, and by Market Values (in real-time), the Spoo is +176 points above its smooth valuation line. Today’s Econ Baro awaits May’s Existing Home Sales, plus April’s Trade Deficit and Wholesale Inventories.

08 June 2026 – 08:43 Central Euro Time

The Bond, Gold and Silver are below today’s Neutral Zones, whereas Oil and the Spoo are above same; session volatility for the BEGOS Markets is moderate. The Gold Update cites price’s ongoing negative stance, Gold at this instant (4321) actually now down -0.3% year-to-date. And even as the S&P 500 is poised (via the Spoo) to open higher on the heels of Friday’s -2.6% decline — the biggest one-day drop thus far in 2026 — the Spoo’s “Baby Blues” (see Market Trends) are now in full cascade such that we can see an S&P high-to-low correction of at least -10% down into the 6800s as detailed in The Gold Update; too, despite Friday’s demise, the S&P is entering a 42nd consecutive trading day of being “textbook overbought”. Ten incoming metrics are due this week for the Econ Baro, albeit none are on the slate for today.

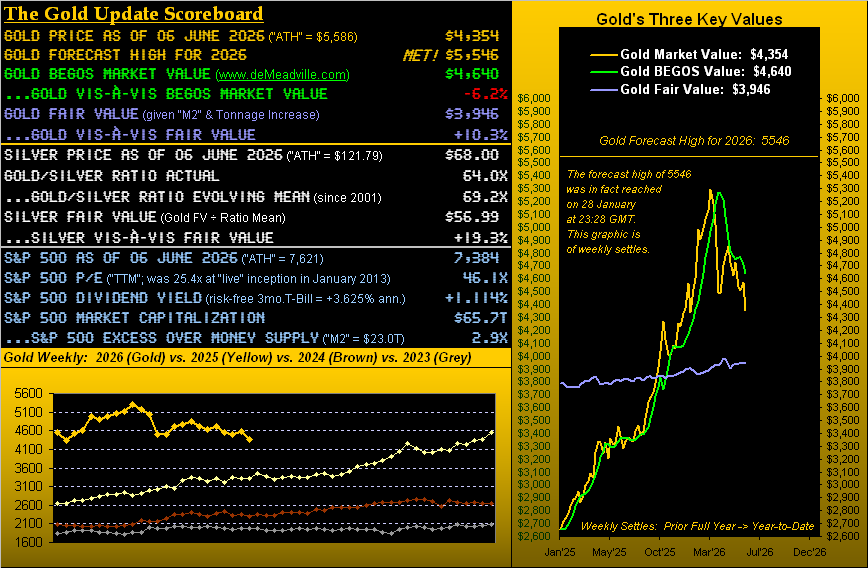

The Gold Update: No. 864 – (06 June 2026) – “Gold’s Still-Negative Track; S&P Poised to Crack”

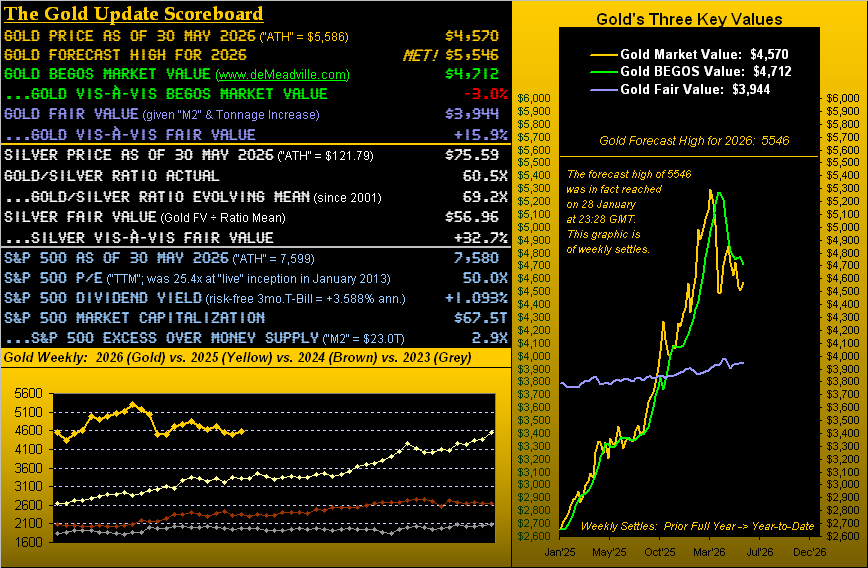

Wrapping it for Gold, clearly the yellow metal has been riding on its net-negative track, even as price by the opening Scoreboard is +10.3% above Fair Value (3946), yet -6.2% below its BEGOS* Market Value (4640) to which typically it can more swiftly ascend as ’tis a “faster” valuation measure.

*BEGOS = Bond / Euro / Gold / Oil / S&P 500

As for the suddenly struggling (albeit long overdue) S&P, we’ll leave you with this:

05 June 2026 – 08:36 Central Euro Time

Let’s start with the Spoo: yesterday we wrote its “Baby Blues” (see Market Trends) of linreg consistency “provisionally” had moved below their key +80% axis; however, come settle, they did not “confirm” as such; regardless, today they are at present again provisionally below -80%, price itself beneath its Neutral Zone for today, as is the case for all three elements of the Metals Triumvirate. The balance of the BEGOS Markets are within today’s Neutral Zones, and session volatility is light-to-moderate. In looking to Market Rhythms for pure swing consistency, on a 10-test basis our top three are Copper’s 1hr MACD, Gold’s daily Moneyflow and Oil’s 30mn EMA; on a 24-test basis Copper owns the top three positions by its 30mn Price Oscillator, 2hr MACD and 2hr Parabolics; Copper’s 21-day linreg still is positively sloped, however the “Baby Blues” are falling such that the trend can rotate to negative during next week. The Econ Baro wraps its week with May’s Payrolls data, plus late in the session comes April’s Consumer Credit.

04 June 2026 – 08:39 Central Euro Time

Both the Swiss Franc and Gold are at present above today’s Neutral Zones; below same are Copper and Oil, and session volatility for the BEGOS Markets is pushing toward moderate. In real-time, the Spoo’s “Baby Blues” which depict linreg consistency are finally breaking down, now provisionally below the key +80% axis; should this be confirmed by session’s end, we’d expect at least initially a drop from here (7544) toward the mid-7400s — which percentage-wise is not that substantive a pullback — but by pricing structure, 7300 appears plausible as does 7279 given the extreme overvaluation of the S&P 500 both technically and obviously fundamentally; as usual, mind the “Baby Blues” on the Market Trends page. Gold, albeit up today, is still in a “mild” downtrend: of technical note, Gold’s weekly Price Oscillator looks to go negative at some point during next week. For the Econ Baro today (along with the usual Thursday Initial Jobless Claims) we’ve the revision to Q1’s Productivity and Unit Labor Costs.

03 June 2026 – 07:36 Central Euro Time

As noted yesterday, just a momentary comment today: we’ve weakness in the the Bond, Swiss Franc and Gold, and strength in Oil. Another record high close yesterday for the S&P 500. The Econ Baro awaits ADP Employment data, Factory Orders and the ISM(Svc) Index. Addendum at 16:58 CET: we’ve returned to our post; the Econ Baro data today was improved for all three reports; later in the session comes the Fed’s “Tan Tome”; and with the exception of Oil, we’ve weakness across the board today for the seven other BEGOS Markets, albeit the Spoo’s “Baby Blues” of linreg consistency (see Market Trends) are still buoyant above the key +80% axis; however their remaining there — we sense — is short-lived.

02 June 2026 – 08:49 Central Euro Time

Currently we’ve the Bond, EuroCurrencies and Metals Triumvirate all above their respective Neutral Zones for today; below same are Oil and the Spoo, and BEGOS Markets’ volatility is mostly moderate. ‘Twas another record-setting day yesterday for the S&P 500, the intra-day high being 7618 and settle at 7600: the Index is now 37 consecutive trading days “textbook overbought” and “extremely so”; by Market Values, the Spoo is (in real-time) +391 points above its smooth valuation line; by Market Rhythms, the Spoo’s best study for pure swing consistency is its 12hr Moneyflow (10-test basis); or if targeting a fixed number of Spoo points, the daily EMA has gained a minimum of 52 points (Long or Short) through its last 10 swings. Nothing is on tap today for the Econ Baro. Note to readers: we are going “in motion” over the next 36 hours or so; tonight’s Tue-Wed work will be run at a minimum level and tomorrow’s commentary may be off-timed and quite brief or later updated; we plan that through the Wed-Thu night work all shall be back to normal.

01 June 2026 – 08:50 Central Euro Time

The new week finds the Bond, Swiss Franc and Gold all at present below today’s Neutral Zones; above same are Copper, Oil and the Spoo, and session volatility for the BEGOS Markets is moving toward moderate. The Gold Update cites the gyrating ways of Gold these days whilst still within a general downtrend since the January All-Time High (5586); too, the weekly Parabolic Short trend mains in place, now entering its 12th week. Were the S&P 500 to open at the instant, ‘twould be at a record high of 7604 give the Spoo still on the upside move this morning.; the Spoo’s “Baby Blues” of linreg consistency (see Market Trends) have yet to break below their key +80% axis. 13 incoming metrics are on the Econ Baro’s docket for this week, beginning today with May’s ISM(Mfg) Index and Construction Spending for April.

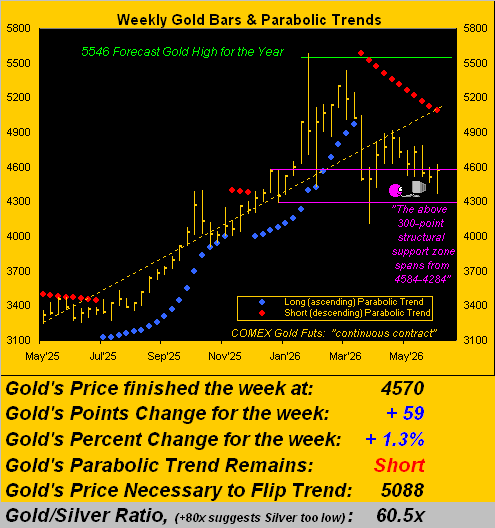

The Gold Update: No. 863 – (30 May 2026) – “Golden Gyration; Irksome Inflation”

Gyrating Gold abounds! Through the completion of May’s 20 trading days, Gold (per its August contract) has chronologically gone up to 4708, down to 4546, up to 4810, down to 4681, up to 4769, down to 4488, up to 4616, down to 4396, price nonetheless getting the month-end bid in settling up yesterday (Friday) at 4570. Gold’s gyrating high-to-low run for the month was -8.8% … but the net change was a comparably wee -2.1%, (Gold having closed the month of April at 4669).

Either way, that’s a ![]() “Whole Lotta Shakin’ Goin’ On”

“Whole Lotta Shakin’ Goin’ On”![]() –[Jerry Lee Lewis, ’57] only to result in

–[Jerry Lee Lewis, ’57] only to result in ![]() “Goin’ Nowhere”

“Goin’ Nowhere”![]() –[Chris Isaak, ’95].

–[Chris Isaak, ’95].

However, there’s been this one anti-conventional wisdom constant throughout. On those days wherein ’twas inferred the Middle-East “war shall continue”, Gold would go down; on the alternate days wherein ’twas said a “peace deal was close”, Gold would go up. (And we’ve herein documented ad nauseam how Gold — after initially spiking — then directionally defies geo-political conventional wisdom).

‘Course, on those “war shall continue” days, Oil and the Dollar would get the bid to the detriment of Gold, but vice-versa if “a peace deal was close”. And as noted, such assessment continues to revolve 180° from one day to the next as if ’twere a modern-day rewrite of Leo Tolstoy’s “War and Peace”, –[circa 1865].

“Or even Shakespeare’s ‘Much Ado About Nothing’, huh mmb?”

Well, we wouldn’t go so far as to say war is “nothing”, Squire, but The Bard’s title –[circa 1598] is apropos of Gold’s gyrational travel throughout May, although price’s regression trend has therein been negative, (as surprisingly too has been that for Oil, even as its peaks and troughs have been pointedly opposed to those for Gold).

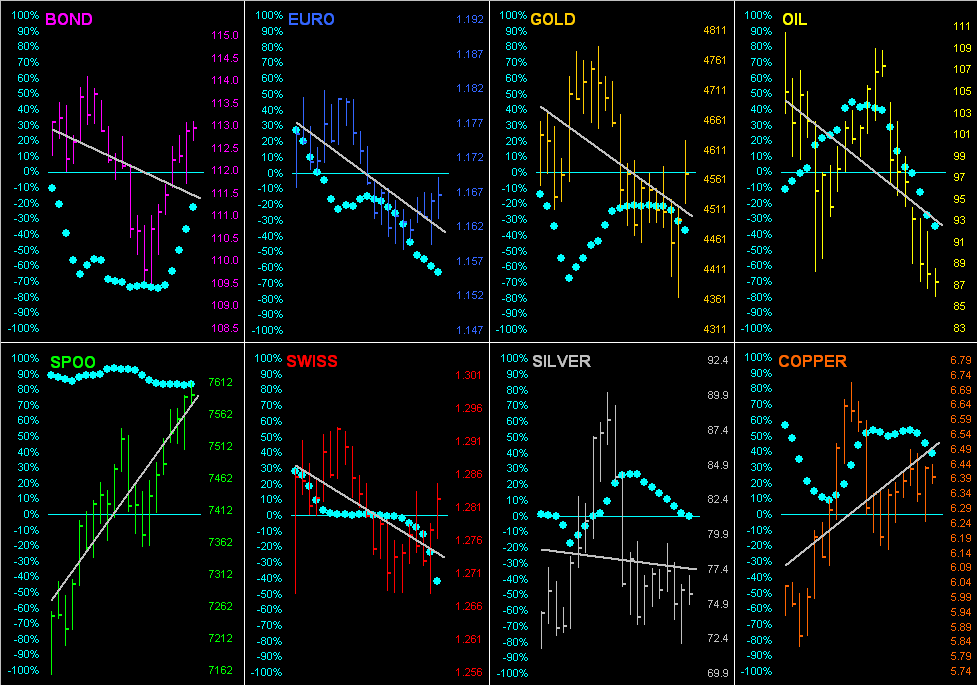

So, it being month-end, let’s go ’round the horn for all eight BEGOS Markets across their last 21 trading days (one month), featuring their respective grey diagonal trendlines and “Baby Blues” which are the dots that depict the day-to-day consistency of trend. Note the S&P 500 (“SPOO”) sporting the steepest uptrend of the set:

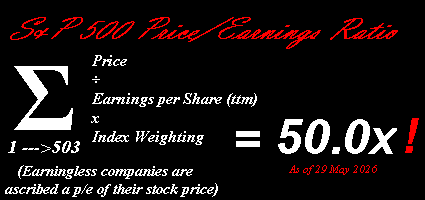

But into feeding “AI” (“Assembled Inaccuracy”) that precise formula, this time the response (and ’tis always different) is that it “…cannot be computed without a private premium database feed…”, in lieu then offering the Wall Street Journal’s calculation of 25.7x. (Clearly, they’ve no idea what’s coming). Again cue Kansas Joe & Memphis Minnie: ![]() “When the Levee Breaks”

“When the Levee Breaks”![]() –[’29], (yes really, the “crash” year).

–[’29], (yes really, the “crash” year).

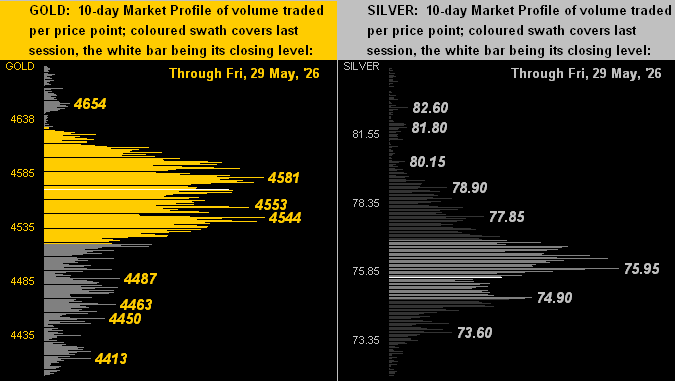

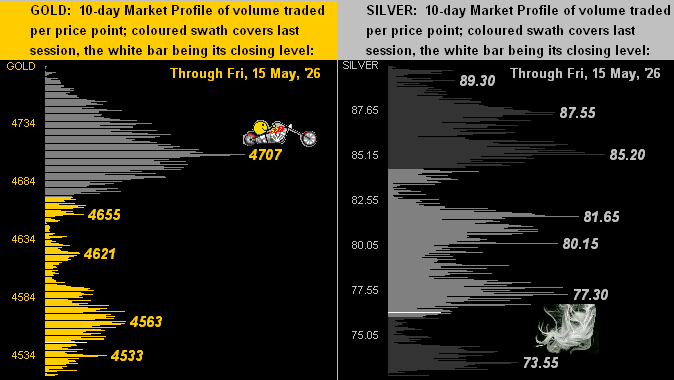

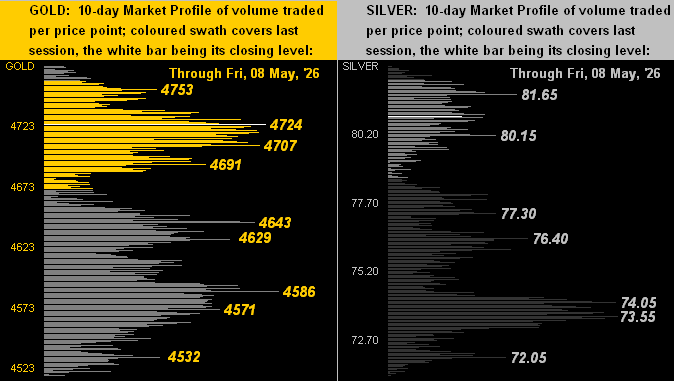

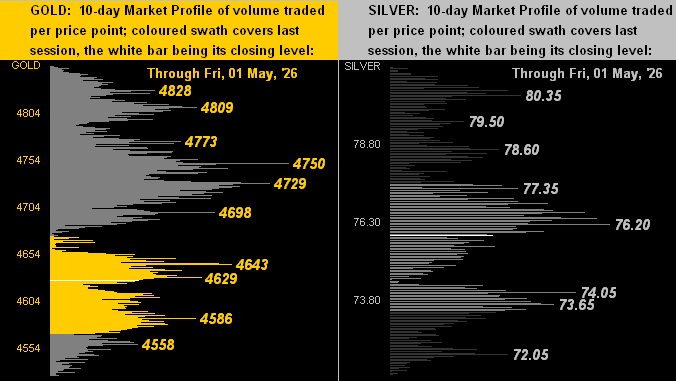

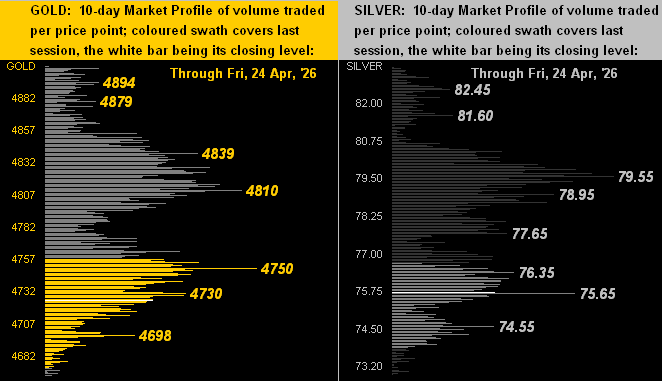

Coming here are the 10-day Market Profiles for Gold on the left and for Silver on the right. Recall a week ago the large pricing Profile gaps for both precious metals, each having since fallen beneath those respective zones. Today, both the yellow and white metals are trading within their most volume-dominant price areas of the past two weeks:

Thus we’ve Golden gyrations and irksome inflation. Might better guidance be obtained from next week’s batch of thirteen incoming Econ Baro metrics, which include a purported slowing in StateSide Payrolls for May? And what about that S&P 500 price/earnings ratio now at a full 50.0x? The Index is now 36 consecutive trading days “textbook overbought”, indeed “extremely” so per Friday’s record high (7599). Regardless…

Hang on to your Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

29 May 2026 – 08:37 Central Euro Time

Oil is presently the only BEGOS Market outside (below) today’s Neutral Zone; volatility for the session is light. Yesterday’s “core” PCE for April was sufficiently “Fed-friendly” that the FOMC likely sit on their hands come the 17 June Policy Statement, even as other inflation measures support a FedFunds rate increase: more tomorrow in the 863rd consecutive Saturday edition of the Gold Update. Looking in real-time at the five primary BEGOS components’ Market Values, we’ve: the Bond just -0^23 points “low” beneath its smooth valuation line, the Euro -0.012 points “low”, Gold -163 points “low”, Oil -11.19 points “low, and the Spoo +411 points “high”. The “live” (futs-adj’d) P/E of the S&P is 49.6x and the yield 1.091% vs. the annualized 3mo T-Bill’s 3.590%. The Econ Baro concludes its week with May’s Chi PMI.

28 May 2026 – 08:47 Central Euro Time

Oil is the only BEGOS Market at present above its Neutral Zone for today; below same are the Bond, Euro, Gold, Silver and the Spoo; session volatility is moderate-to-robust, Gold notably having already traded 107% of its EDTR. At Market Trends, the “Baby Blues” of linreg consistency are in decline for every BEGOS component except for the Bond; those for the Spoo barely are falling, yet remain above the key +80% axis, (their actual level in real-time is +82% after having been as high as +93% last week). The S&P 500 established a marginal record closing high yesterday (7520), albeit the intra-day high was not a record. A bevy of incoming metrics arrive today for the Econ Baro, including the first revision to Q1’s GDP, plus April’s Durable Orders, New Home Sales, Personal Income/Spending and the “Fed-Favoured” PCE inflation gauge.

27 May 2026 – 08:43 Central Euro Time

The Bond is the only BEGOS Market at present above its Neutral Zone for today; below same are Gold, Silver and Oil, and session volatility is light. Yesterday, the S&P 500 made both record intra-day (7539) and closing (7519) highs: the Index is now “textbook overbought” through the last 33 consecutive trading days, and the “live” (futs-adj’d) P/E at this instant is 49.1x. The Spoo’s “Baby Blues” of linreg “consistency” have barely been treading water these last several days just above +80%, which we continue to mind for a breakdown toward lower price levels; the Spoo’s best Market Rhythm for pure swing consistency has been (on a 10-test basis) its 2hr Price Oscillator and (on a 24-test basis) its 2hr Parabolics. Cac volume for Gold is rolling from June into that for August with +33 points of fresh premium, whilst that for the Bond is rolling from June into September at a -0^16 points discount. Nothing is due today for the Econ Baro ahead of tomorrow’s “Fed-Favoured” PCE inflation gauge for April.

26 May 2026 – 08:41 Central Euro Time

The two-day session for the BEGOS Markets continues, the Spoo still poised to pull the S&P 500 up to a record high were it to open at this instant, albeit not as robustly so as we saw 24 hours ago; the Spoo is now some -30 points off its intrasession high of 7570. The Metals Triumvirate has all its elements back inside today’s Neutral Zones, while still above same are the Bond, Euro and Spoo; Oil -5.2% remains beneath its Neutral Zone. Overall session volatility still is moderate for the two days combined. The Bond and Oil continue being the best two correlated (negative) of the five primary BEGOS components, although there is firm positive correlation between the Euro and Gold. 10 incoming metrics are due for the Econ Baro as the week unfolds, beginning today with Consumer Confidence for May.

25 May 2026 – 08:49 Central Euro Time

The Spoo has reached an all-time high this morning at 7565, spurred (’tis said) by a potential two-month ceasefire in the USA/IRN war. StateSide (Memorial Day) and EuroSide (Pentecost) physical bourses are closed; however were the S&P 500 to open at this instant, ‘twould so do at a record high 7543. The BEGOS Markets are all trading for Tuesday settlement, six of the eight at present above their Neutral Zones for the session, the two exceptions being Copper (within) and Oil (below), the latter being the largest mover thus far -5.7% at 91.47; volatility is moderate. The Gold Update graphically depicts both precious metals as being in year-to-date linear regression downtrends even as record highs were established back in late January. Q1 Earnings Season has concluded with 80% of S&P reporting constituents having bettered their bottom lines from Q1 a year ago; ex-COVID recovery, this Q1 was the best quarter for year-over-year percentage of improved constituents since Q3 of 2018. There are holiday trading halts for the Bond and Spoo at 17:00 GMT, and for the Metals and Oil at 18:30 GMT; the Currencies go the distance to 21:00 GMT.

The Gold Update: No. 862 – (23 May 2026) – “Precious Metals Prices Perspectives”

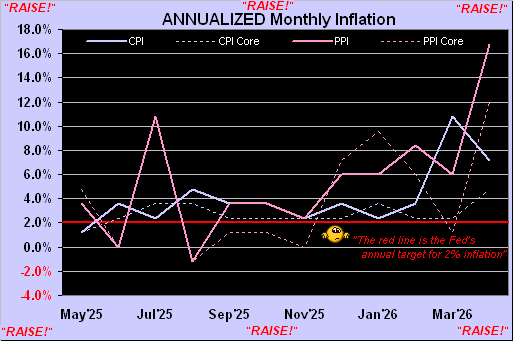

To close, regular readers well-know that because we duly track inflation, we’ve suggested for a couple of years now that the Federal Reserve’s Open Market Committee really should raise their Bank’s Funds rate. Yet finally, some in the trading world also are starting to realize same. Welcome aboard, to wit this phrase reported yesterday, (hat-tip Bloomy): “Bond traders are fully pricing in an interest-rate hike by the [behind the curve] Federal Reserve this year.” And within next week’s mix of incoming Econ Baro metrics is the “Fed-favoured” inflation gauge of Personal Consumption Expenditures for April: annualizing its consensus for both the “headline” and “core” numbers continues to state inflation as well above the Fed’s +2% target. So just how shall the FOMC’s 17 June Policy Statement read?

Stay perspectively tuned, and (in the spirit of aforementioned 2004-2006) your Gold holdings unpruned!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

22 May 2026 – 08:42 Central Euro Time

Both Copper and the Spoo are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility into “Getaway Friday” is quite light. As this week has unfolded, the S&P 500’s daily Parabolics and MACD have taken on negative readings; too, the Spoo’s “Baby Blues” (see Market Trends) for linreg consistency have in real-time dropped another notch to +83%, their key line-in-the-sand being +80%. Going ’round the horn for the five primary BEGOS components’ Market Values in real-time: we see the Bond -3^21 points “low” vis-à-vis its smooth valuation line, the Euro -0.023 points “low”, Gold -240 points “low”, Oil in line with its Market Value, and the Spoo +351 points “high”. For the Econ Baro we’ve the revision to May’s UoM Sentiment Survey, plus April’s Leading (i.e. “lagging”) Indicators. And ’tis the final day of Q1 Earnings Season. Tomorrow comes the 862nd consecutive Saturday edition of The Gold Update. Monday brings limited trading hours for the BEGOS Markets given Memorial Day StateSide and Pentecost on this side of The Pond.

21 May 2026 – 08:48 Central Euro Time

Copper is at present the sole BEGOS Market outside (below) its Neutral Zone for today; session volatility is again mostly light. Copper at 6.2835 is trading below its most volume-dominant Market Profile price (6.3050) through which it fell yesterday; too by Market Trends, Copper’s linreg remains positive as ’tis been since 13 April, but is now lacking puff; (as previously noted, that for the Spoo too remains positive, but the upside consistency is becoming less so); Copper’s best Market Rhythm for pure swing consistency on both the 10-test and 24-test bases has been the 30mn Price Oscillator: indeed per the last 16 swings, price by that Rhythm (with the benefit of hindsight) as achieved intra-trade profit of at least 0.048 points ($1,200/cac) 13 times. The Econ Baro looks to metrics including May’s Philly Fed Index and April’s Housing Starts/Permits.

20 May 2026 – 08:36 Central Euro Time

Silver is at present above its Neutral Zone for today, whilst below same is Oil; volatility for the BEGOS Markets is mostly light. The Spoo yesterday settled below its Market Magnet (7416), suggestive of still lower prices near-term; as noted, we’re minding the Spoo’s “Baby Blues” of linreg consistency (see Market Trends) for the Blues to break below the key +80% which now looks to occur as soon as tomorrow, following which price ought further fall; the Blues have not produced a signal for the Spoo since the Long suggestion back on 02 April, price opening that day at 6619. Amongst the five primary BEGOS components, our best correlation remains negative between the Bond and Oil. Nothing is due today for the Econ Baro. And late in the session comes the FOMC Minutes from its 28/29 April meeting.

19 May 2026 – 08:41 Central Euro Time

The Bond, Euro, Swiss Franc, Silver and Copper are all presently below their respective Neutral Zones for today; the other three BEGOS Markets are within same, and volatility is light-to-moderate. At Market Trends, we’re minding the Spoo’s “Baby Blues” of linreg consistency: whilst they remain well-above the key +80% axis, they are nonetheless in the early signs of decline, barring the Spoo racing back up towards its all-time high (7540 v.s current 7409); by Market Rhythms the Spoo’s best for pure swing consistency on a 10-test basis has been the 15mn Price Oscillator, whereas on a 24-test basis ’tis been the 2hr Price Oscillator; and by its Market Profile, the Spoo’s most volume-dominant price of the past fortnight is 7421, which is about the midpoint of today’s trading range thus far. The sole incoming metric today for the Econ Baro is April’s Pending Home Sales.

18 May 2026 – 08:36 Central Euro Time

Presently, the Bond, Copper and Spoo are below today’s Neutral Zones, whilst above same is Oil; BEGOS Markets’ volatility is moderate. The Gold Update sees price’s downtrend as remaining in force, be it by the near-term 21-linreg trend (see Market Trends) or the broader-term weekly Parabolics, the prior week’s rally thus having been one of “relief”. The Spoo appears en route to recording a second consecutive down day, which across the prior 33 trading days (from 31 March) has only twice occurred; the S&P 500 itself of course remains technically overbought through the last 27 trading days as well as fundamentally overvalued, indeed vastly so via the “live” futs-adj’d P/E at this instant of 47.9x. Due for the Econ Baro is the NAHB Housing Index for May. And this is the final week of Q1 Earnings Season.

The Gold Update: No. 861 – (16 May 2026) – “Gold’s Recent Trend Not Much of a Friend”

And as is the rule (albeit 2004-2006 was an exception), higher rates make the Dollar more attractive at the conventional-wisdom expense of Gold, (which simplified for you WestPalmBeachers down there means Gold goes down when rates go up). ‘Course, we all know that “Big Oil” et alia are getting the blame; yet inflation was already on the move pre-war, and moreover by the above graphic — assuming that neither do you eat nor drive — the “core” rates themselves are way above the Fed’s targeted +2% shelves. ![]() “Oh Well”

“Oh Well”![]() –[Fleetwood Mac, ’69].

–[Fleetwood Mac, ’69].

Too, we’ve the Economic Barometer, for which nine of last week’s 15 incoming metrics improved period-over-period, notably therein Industrial Production for April at +0.7%, its month-over-month swing (from -0.3% in March) the best since that for August 2024. But March’s Business Inventories backed up quite a bit for a second consecutive month. Is the moving of product slowing given inflation is growing? (Do we dare again utter the “s” word?) Perhaps not just yet as the Baro is still uptrending:

Here’s how it all stands for Gold in the stack.

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 5586 (29 January 2026)

2026’s High: 5586 (29 January)

Gold’s All-Time Closing High: 5411 (28 January 2026)

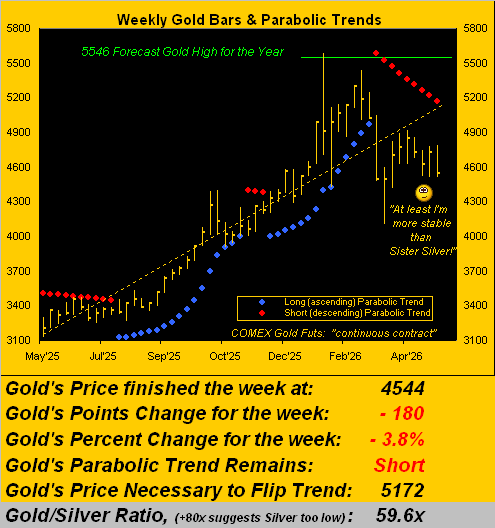

The Weekly Parabolic Price to flip Long: 5172

10-Session directional range: up to 4983 (from 4510) = +273 points or +6.1%

Gold’s BEGOS Market Value (from our opening “Scoreboard”): 4769

10-Session “volume-weighted” average price magnet: 4667

Trading Resistance: Market Profile notables: 4563 / 4621 / 4655 / 4707

Gold Currently: 4544, (expected daily trading range [“EDTR”]: 107 points)

Trading Support: per the Market Profile: 4533

2026’s Low: 4100 (23 March)

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 4017

The 300-Day Moving Average: 3980 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Of non-geopolitical interest in the ensuing week is the Wednesday release of the FOMC’s 28/29 April Meeting Minutes. A bit more hawkish than usual perhaps? We’ll see who’s been really paying attention to the math. And Friday brings for April the Conference Board’s Leading (i.e. “lagging”) Indicators, which have not mustered a positive reading since last July, even as the Econ Baro has essentially risen throughout. ‘Course, ’tis said The Board can go a bit “woke” in its assessments…

Go with the Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

15 May 2026 – 08:44 Central Euro Time

The Dollar’s firm week has it up to its highest level (99.110) since 01 April; thus ’tis no surprise to see the BEGOS Markets (save for Oil) working lower: at present, the Bond, EuroCurrencies, Metals Triumvirate and Spoo are all below today’s Neutral Zones; Oil is above same, and its cac volume is rolling from June into that for July at a -4.20 points discount. Gold’s 21-day linreg remains negative (see Market Trends) and the weekly parabolic Short trend looks to complete its ninth week as we’ll see in tomorrow’s 861st consecutive Saturday edition of The Gold Update. The S&P 500 closed above 7500 yesterday for the first time, the intra-day high (7517) finding the “live” P/E at 49.9x; the yield on the Index is 1.066% vs. 3.588% annualized on the “risk-free” U.S. three-month T-Bill. The Econ Baro finishes its week with May’s NY State Empire Index and April’s IndProd/CapUtil. And there remains one week still to run in Q1 Earnings Season.

14 May 2026 – 08:46 Central Euro Time

Inflation is running sufficiently “hot” such that under just-appointed FedHead Warsh the FOMC “ought” raise rates per its next Policy Statement (17 June); on verra… At present, we’ve Copper as the sole BEGOS Market outside (below) its Neutral Zone for today, and session volatility is again light. The Spoo yesterday moved well-above volume-dominant Market Profile resistance at 7421: its current 7488 price is (in real-time) +516 points above its BEGOS Market Value, such equating the P/E of the S&P 500 to 49.5x, the Index itself yesterday completing a 25th consecutive session as “textbook overbought” whilst posting a record high at 7460. Our best correlation amongst the five primary BEGOS Markets is negative between the Bond and Oil. For the Econ Baro we await metrics including April’s Retail Sales and Ex/Im Prices, plus March’s Business Inventories.

13 May 2026 – 08:37 Central Euro Time

Presently, both the Euro and Oil are below their respective Neutral Zones for today, whist the Spoo is above same; BEGOS Markets’ volatility is light. Over the past couple of years we’ve in The Gold Update said that the Fed need raise rates: that may soon come to pass given the continued ramping up of inflation; (the next FOMC Policy Statement is due 17 June). Looking at Market Rhythms for pure swing consistency, our top three (10-test basis) have been Gold’s daily Moneyflow, the non-BEGOS Yen’s 30mn Moneyflow and the Bond’s 1hr MACD; too (on a 24-test basis) they are the Euro’s 30mn Moneyflow, Oil’s 2hr MACD and Silver’s 30mn Parabolics. Silver has been firmly breaking out to the upside, indeed +25% across just the past 11 trading days low-to-high inclusive. And the Econ Baro awaits wholesale inflation for April via the PPI.

12 May 2026 – 08:36 Central Euro Time

Seven of the eight BEGOS Markets are at present in the red, six of which are below today’s Neutral Zones; the lower Bond is within same and Oil is the sole up component at 99.45 and above its Neutral Zone; session volatility is again mostly moderate. The Bond (112^23) yesterday failed to hold Market Profile volume-dominant support at 113^06, and price moved beneath the Market Magnet; by Market Rhythms for pure swing consistency, the Bond’s best on a 10-test basis has been its 1hr MACD and on a 24-test basis the 15mn Price Oscillator. For the Precious Metals, at Market Trends Gold’s 21-day linreg still is negative, however that for Silver has rotated to positive, even as price is lower thus far today. April’s CPI and Treasury Budget come due for the Econ Baro.

11 May 2026 – 08:43 Central Euro Time

The Bond, Euro, Swiss Franc and Gold all are at present below today’s Neutral Zones; above same are Copper and Oil, and BEGOS Markets’ volatility is mostly moderate. The Gold Update queries if last week’s rally was one of “relief” given the 21-day linregs for both Gold and Silver remain negative, but less so as the “Baby Blues” of trend consistency are rising (see Market Trends); cited too is our long-ongoing concern of the S&P 500’s extreme overvaluation; by the Spoo’s BEGOS Market Value in real-time, ’tis +532 points above the smooth valuation line and the S&P’s “live” (futs-adj’d) P/E is 48.1x. That stated, substantive money has been getting thrown into the S&P: per our MoneyFlow page, all three time gauges (weekly, monthly and quarterly) suggest the S&P can continue higher still by a few hundred points, (barring this being a “blow-off top”). ‘Tis a busy week for the Econ Baro with 15 incoming metrics scheduled, beginning today with April’s Existing Home Sales.

The Gold Update: No. 860 – (09 May 2026) – “Gold: Relief Rally or Downtrend Finale? (and S&P Wary)”

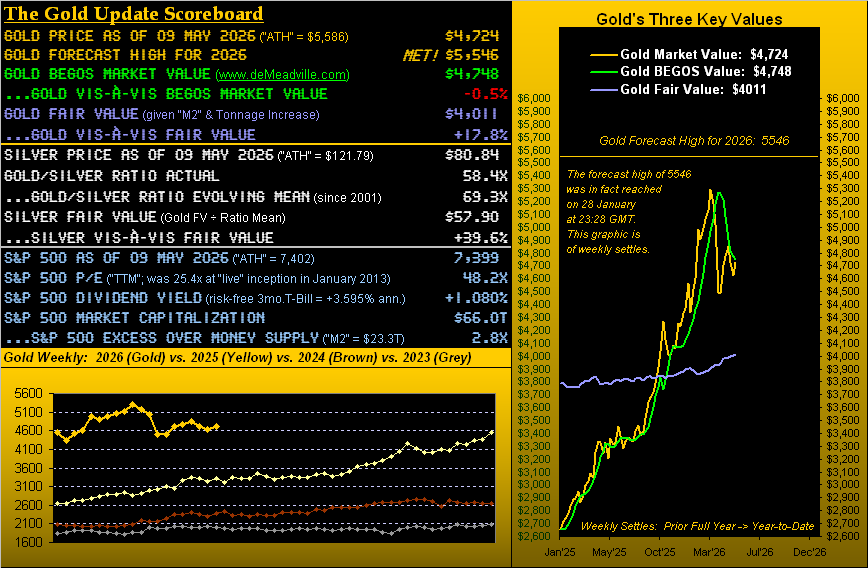

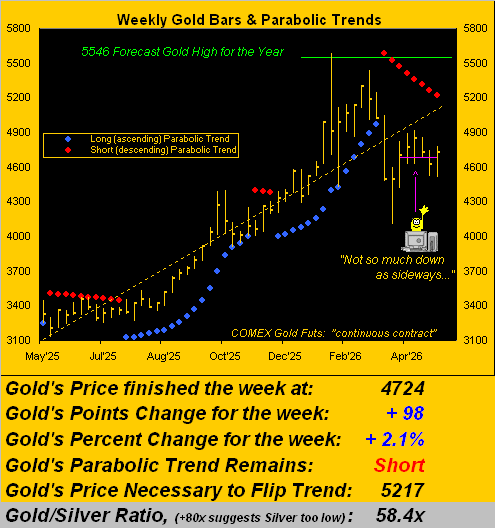

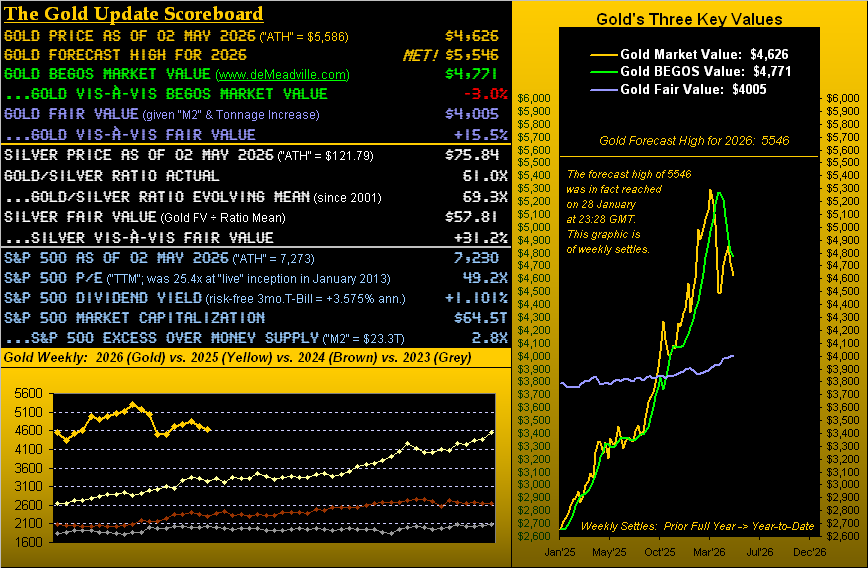

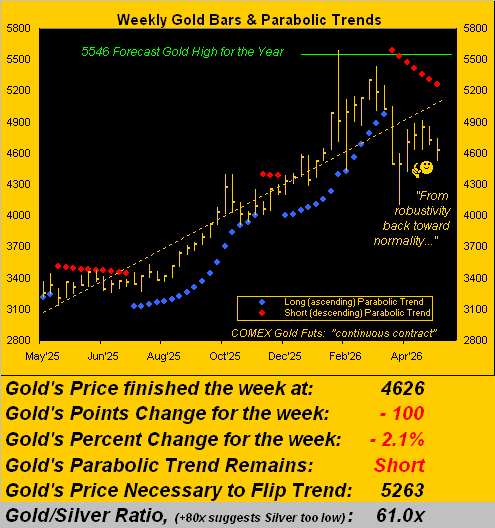

The lower Gold levels we’d anticipated two weeks ago (price having dropped from our 25 April penning at 4725 by as much as -4.6% to 4510 this past Monday) clearly panned out. Since that low, Gold has recovered all of such loss and then some, climbing on Thursday to as high as 4775 in settling the week yesterday (Friday) at 4724. And by the above Scoreboard, the combination of Gold recovering contra to its declining BEGOS Market Value* (now 4748) puts those two levels relatively near one another. As we oft quip: “Means reversion is a beautiful thAng”. However (as also therein depicted), given Gold’s Fair Value (now 4011), price remains notably overvalued by +17.8%.

*Gold’s value based on its movement relative to those of BEGOS: Bond, Euro, Gold, Oil, S&P 500

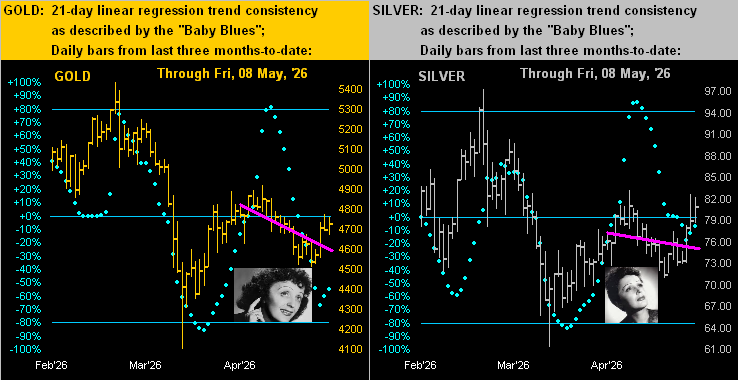

Still, per our title’s query: is Gold in just a relief rally, or did the recent downtrend reach its finale? Let’s have a look. Et voilà, our latest view, along with that for Silver too, their respective pink 21-day linear regression trends still negatively skewed. Cue Edith Piaf from ’45: ![]() “La Vie en Rose”

“La Vie en Rose”![]()

‘Course (save for those WestPalmBeachers down there), market participants know ’tis the tendency of technicals to lag price. And those trendlines for Gold and Silver are losing their downside consistency because the baby blue dots — at least for the past three trading days — are on the rise. As these “Baby Blues” tend to lead price, we may see such trends rotate from negative to positive over the next week or two, (the blue dots then having crossed back above their respective 0% axes).

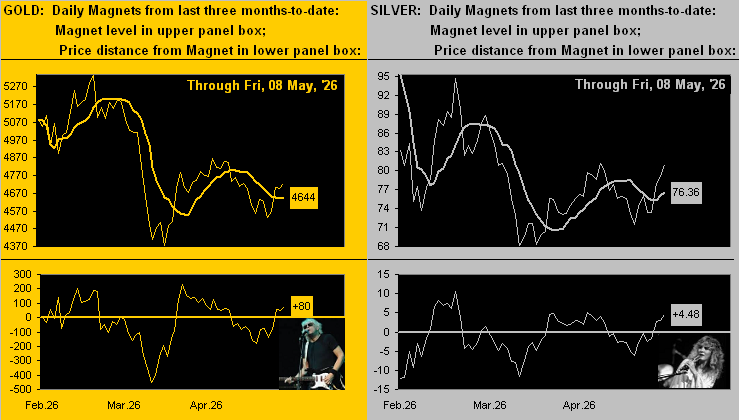

But wait, there’s more: let’s go to the Market Magnets for both precious metals. Note the steely upside crossovers of price above Magnet. As described on the website: “…being ‘attracted’ to and crossing the Magnet, we expect price to continue in the same direction. But when the price gets too far away from the Magnet, we anticipate price to be re-attracted to the Magnet…” Cue Walter Egan with Stevie Nicks from ’78: ![]() “Magnet and Steel”

“Magnet and Steel”![]()

Sideways notwithstanding, for Gold in the ensuing week to flip its parabolic trend from Short to Long, price need rise +493 points such as to eclipse the noted 5217 level. As of now, the expected weekly trading range is “only” 335 points, (last’s week’s actual range being “just” 265 points), and the daily 107 points. Thus barring the long-bankrupt U.S. Treasury actually acknowleding bankruptcy (or some other momentous market-moving event), Gold’s Short trend likely has more than a week before reaching its end, even should price continue to ascend.

Meanwhile: shall there ever be an end to the meteoric rise in the S&P 500? Our wariness is beyond extreme. ‘Round here, the high-level finance folks with whom we’re humbly honoured to engage all ‘know’ that “The Crash!” is coming. (‘Tis been re-hashed time and again now for some three years). Regardless, recall in our 18 April missive that for the S&P’s practically non-existent dividend yield to match that of the annualized three-month U.S. T-Bill, the Index need decline -64%. (That won’t be on CNBS). And perhaps such demise is near, for as a fine friend the other day said: “It’s different now.” That thus stated, we’ve repetitively learned that ’tis never different.

To be sure, the S&P’s Q1 Earnings Season has exhibited excellent year-over-year growth; but as we’ve regularly underscored, the actual level of earnings remains too poor to maintain price, especially given more than triple the yield in the “risk-free” T-Bill.

So, here’s the quintessential question to pose for equities chasers in this Investing Age of Stoopid. The price of an investment into which you want to pile on along with all the lemmings is $48.20. Your trusty stockbroker tells you that if you buy today at that price, one year from now your value will be — including dividend yield — $49.72. Gonna buy it? Of course not. A +3.15% gain is boring! No. You want stocks that triple several times a year, ’cause that’s what everybody else has.

“Well, what exactly is that $48.20 stock, mmb?”

‘Tis not a stock, Squire. Rather, ’tis proportionally the “price” and “return” of the S&P 500 today. The price/earnings ratio settled this past week at 48.20x. That means you are willing to pay $48.20 for something that in a year shall earn $1.00, putting the price (per retained earnings) at $49.20. Add in the amazing yield of 1.080% for another 52¢ and there’s your all-in value a year hence of $49.72 … just in case you’re scoring at home.

Looking to gain even less? By the same proportional math for some specific S&P constituents, buying Tesla (TSLA) equates to paying $358 for something that earns $1. CoStar Group (CSGP)? $536 to gain $1. Or ![]() “How much is that doggie in the window?”

“How much is that doggie in the window?”![]() –[Patti Page, ’53] Datadog (DDOG) $647 to earn $1. Then of course, one can do a full face-plant with CrowdStrike Holdings (CRDW) by paying an actual $528 for something that earns nothing. Have a great day. The Economic Barometer continues to have its share of them…

–[Patti Page, ’53] Datadog (DDOG) $647 to earn $1. Then of course, one can do a full face-plant with CrowdStrike Holdings (CRDW) by paying an actual $528 for something that earns nothing. Have a great day. The Economic Barometer continues to have its share of them…

We’ll wrap it here with this updated image from “A Picture is Worth a Thousand Words Dept.”, or in this case, perhaps just one word: “YIKES!”

Here’s a better word: “GOLD!”

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

08 May 2026 – 08:48 Central Euro Time

The EuroCurrencises, Metals Triumvirate and Spoo are all presently above today’s Neutral Zones; below same is Oil, and session volatility for the BEGOS Markets runs from mild for the Bond to robust for Copper, the latter having thus far traced 169% of its EDTR (see Market Ranges). Copper’s best Market Rhythm for pure swing consistency is (on a 10-test basis) the 30mn Moneyflow and (on a 24-test basis) the daily MACD; too, the daily MACD in swinging has reached at least 0.10 targeted (in hindsight) points across the last 10 swings in-a-row. Gold (4740) has moved well-up from its Monday low of 4510: more on the precious metals in tomorrow’s 860th consecutive Saturday edition of The Gold Update. Today the Econ Baro awaits April’s Payrolls data, May’s UoM Sentiment Survey, and March’s Wholesale Inventories.

07 May 2026 – 08:46 Central Euro Time

Record highs continue for the S&P 500, yesterday achieving 7369: the futs-adj’d “live” P/E at this moment is 46.7x and the yield is down to 1.076%. Presently, both Gold and Silver are above today’s Neutral Zones; otherwise, the rest of the BEGOS Markets are within same, and volatility is light. By Market Trends, we’ve positive 21-day linregs for the Swiss Franc, Copper, Oil and the Spoo; thus they are negative for the Bond, Euro, Gold and Silver. Oil yesterday settled below its Market Magnet for the first time since 20 April as well as below its smooth valuation line for the first time since 27 April, both suggestive of still lower prices near-term; Oil’s best Market Rhythm for pure swing consistency is its 30mn Moneyflow. The Econ Baro’s incoming metrics include March’s Consumer Credit and Construction Spending, plus the latter’s (delayed) for February, and the initial read of Q1’s Productivity and Unit Labor Costs.

06 May 2026 – 08:43 Central Euro Time

‘Tis a moderate-to-robust volatile start to Wednesday with seven of the eight BEGOS Markets at present above their day’s respective Neutral Zones, the sole component below being Oil. Gold is up better than +100 points, however by Market Trends the “Baby Blues” of linreg consistency are still falling, as are those for Silver; since The Gold Update’s (25 April) anticipation for lower Gold prices, the yellow metal has dropped by as much as -4.6%, notwithstanding this second session of “relief rally”; currently 4677, Gold’s most volume-dominant overhead resistor is 4725 (see Market Profiles). The S&P 500 continues to make record highs (7273) even as the Index is now 19 consecutive trading days “textbook overbought”: by Market Values in real-time, the Spoo is +505 points “high” above its smooth valuation line. For the Econ Baro we’ve April’s ADP Employment data.

05 May 2026 – 10:11 Central Euro Time

A bit tardy this morning given an internet “slowdown”. For the moment, we’ve all three elements of the Metals Triumvirate above today’s Neutral Zones, as is the Spoo. The other BEGOS Markets are within same, and volatility is light-to-moderate. The precious metals’ recovery thus far today is not enough to stem the “Baby Blues” of linreg consistency from further falling in real-time, (see Market Trends). As to our best Market Rhythms for pure swing consistency, the 10-test leaders have been Gold’s daily Moneyflow, the Euro’s 30mn Moneyflow and Copper’s 8hr Moneyflow; for the 24-test basis they are Silver’s 15mn for both its Moneyflow and MACD, plus the Bond’s 1hr Moneyflow. The Econ Baro awaits April’s ISM(Svc) Index, March’s Trade Deficit and New Home Sales, plus the latter (delayed) for February.

04 May 2026 – 08:35 Central Euro Time

The Bond, Gold and Oil are all at present below today’s Neutral Zones; above same are the Euro and Spoo, and session volatility for the BEGOS Markets is mostly moderate. The Gold Update takes a mildly cautious stance on the precious metals, both of which though Friday are up +6.8% year-to-date, having of course been substantially higher in late January; at Market Trends, Gold’s “Baby Blues” of linreg consistency continue to drop, whereas those for Silver are momentarily hesitant; by Market Values, Gold is (in real-time) -158 points below its smooth valuation line; too by the deMeadville EMAs, the 21-day has crossed beneath the 89-day, plus the daily Parabolics, MACD, Price Oscillator and Moneyflow are all negatively positioned. The Spoo for the moment would elicit a higher open later today for the S&P 500. And ’tis a busy week for the Econ Baro beginning with March’s Factory Orders.

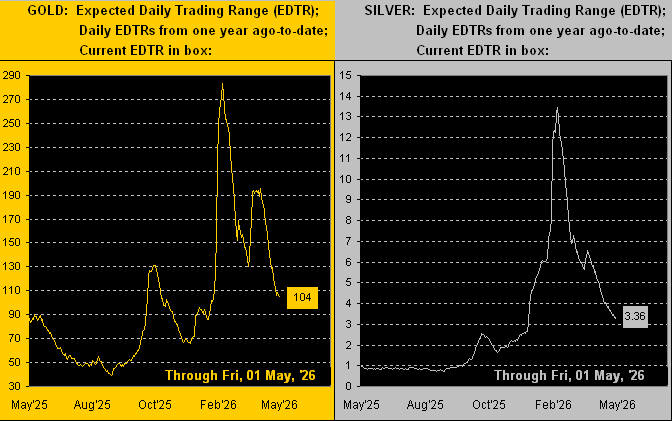

The Gold Update: No. 859 – (02 May 2026) – “Gold’s Year-to-Date Gain Nearly Gone”

As thereon depicted in the two boxes, Gold’s EDTR going into Monday is now 104 points, only 37% of the expectation for 283 points back its peak on 09 February, and that for Silver is now 3.36 points, just 25% of the 13.46 sought for that same date. As to achieving/exceeding the EDTRs, across the past 28 trading days, Gold has only so done six times and Silver seven. Also notable is a reduction in trading activity: Gold’s average daily contract volume in April was but a scant 65% of that for March, and for Silver ’twas 76%. Cue Pink Floyd’s: ![]() “The Narrow Way”

“The Narrow Way”![]() –[’69].

–[’69].

Thus in further review, Gold has given back most of what had been a substantive gain by 29 January of 5586 (+28.9%) to now a vastly reduced +6.8%, albeit having since nicely recovered from March’s 4100 low. To wit, this day-to-day graphic of Gold’s percentage ride since the 4332 (black line) close in 2025, the “lower highs” of both 02 March and 17 April giving at least technical cause for concern:

However, we do not take fundamental pause. Yes, Gold is currently +15.5% above the Gold Scoreboard’s Fair Value of 4005, and could well revisit that level. But hardly shall we allow debasing currency us dishevel!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

01 May 2026 – 08:44 Central Euro Time

The Bond, Swiss Franc, Gold and Copper all at present are below their respective Neutral Zones for today; above same is Oil, and BEGOS Markets’ volatility is light. As anticipated, Silver’s linreg (see Market Trends) has joined Gold in rotating from positive to negative; more on the metals’ expectedly down week in tomorrow’s 859th consecutive Saturday edition of The Gold Update. Going ’round the the Market Values horn in real-time for the five primary BEGOS components: we’ve the Bond -2^16 points “low” beneath its smooth valuation line, the Euro -.005 points “low”, Gold -166 points “low”, Oil +7.09 points “high” and the Spoo +475 points “high”, the S&P itself now 16 trading days “textbook overbought”. Were StateSide equities to open at this instant, they’d be a bit higher, and we expect there’ll be much near-term FinMedia babble regaining “Dow 50k”, (as it first briefly had in February), barring it all going wrong. The Econ Baro completes its busy week with April’s ISM(Mfg) Index.

30 April 2026 – 08:41 Central Euro Time

Following three straight days of decline, both precious metals are presently above today’s Neutral Zones, as is Oil; the balance of the BEGOS Markets are within same, and session volatility is moderate. By Market Trends as suggested yesterday, Gold’s linreg has (in real-time) rotated to negative, whilst that for Silver looks to so do by tomorrow despite both metals being up today. Looking at Market Rhythms for pure swing consistency, our Top Three by the 10-test basis are Gold’s daily Moneyflow, Copper’s 8hr Parabolics, and again Gold’s 30mn MACD, whereas per a 24-test basis we’ve Copper’s 30mn Parabolics, the Swiss Franc’s 1hr MACD, and the Spoo’s 1hr Parabolics. Nine metrics come due today for the Econ Baro, including April’s Chi PMI, March’s Personal Income/Spending,“Fed-Favoured” PCE data and Leading Indicators, plus the first peek at Q1 GDP and the Employment Cost Index.

29 April 2026 – 08:44 Central Euro Time

Presently, the Euro is below its Neutral Zone for today, whilst above same are both Copper and Oil; BEGOS Markets’ volatility is light. As we’d already seen for Silver, Gold too yesterday traded down into the “Golden Ratio” retracement zone as noted in The Gold Update: Gold’s low thus far in the week is 4568 whilst that for Silver is 71.93; ‘twould appear by week’s end, both precious metals linregs shall have rotated from positive to negative (see Market Trends); as well, Copper’s “Baby Blues” of trend consistency confirmed dropping below the +80% axis, indicative of lower prices near-term. The S&P 500 is now 14 consecutive trading sessions as “textbook overbought”; and the Spoo by its Market Value is (in real-time) +427 points above its smooth valuation line. There are varying sources for today’s incoming Econ Baro metrics: to be sure, we’ll get March’s Durable Orders, and maybe a combination of February and March data for Housing Starts/Permits, plus perhaps same for New Home Sales, albeit they also are scheduled for next week … on verra… Then at 18:00 GMT comes the FOMC’s “no change” Policy Statement.

28 April 2026 – 08:45 Central Euro Time

The Euro, Swiss Franc, and all three elements of the Metals Triumvirate are presently below their respective Neutral Zones for today; above same is Oil, and session volatility for the BEGOS Markets is moderate, noting therein that Silver already has traced 101% of today’s EDTR (see Market Ranges). Too, Silver’s cac volume is rolling from May into that for July. At Market Trends, the “Baby Blues” of regression trend consistency continue to fall for the precious metals; indeed Silver has today reached down into the “Golden Ratio” retracement range as cited in the current edition of The Gold Update; as well, both Gold and Silver are now trading below the bottom of their 10-day Market Profiles. The S&P 500 has again recorded closing (7174) and intra-day (7179) highs, and is now 13 consecutive trading days “textbook overbought”; the “live” (futs-adj’d) P/E is 48.8x. The Econ Baro awaits Consumer Confidence for April.

27 April 2026 – 08:40 Central Euro Time

Early on we’ve the Bond at present below its Neutral Zone for today, whilst above same is Oil; volatility for the BEGOS Markets is light-to-moderate. The Gold Update points to last week’s decline in the “Baby Blues” of regression trend consistency for both precious metals such that lower price levels are likely in the near-term offing. The S&P 500 concluded Friday at an all-time closing high of 7165, the intra-day high having been a record 7169; by the Spoo, today’s S&P opening ought be mildly lower; per the Spoo’s 10-day Market Profile, price (currently 7188) has its most volume-dominant Profile support at 7162. Copper’s cac volume is rolling from May into that for July. And whilst nothing is due today for the Econ Baro, ’tis a busy week with 14 scheduled metrics, plus the “no change” FOMC Policy Statement on Wednesday.

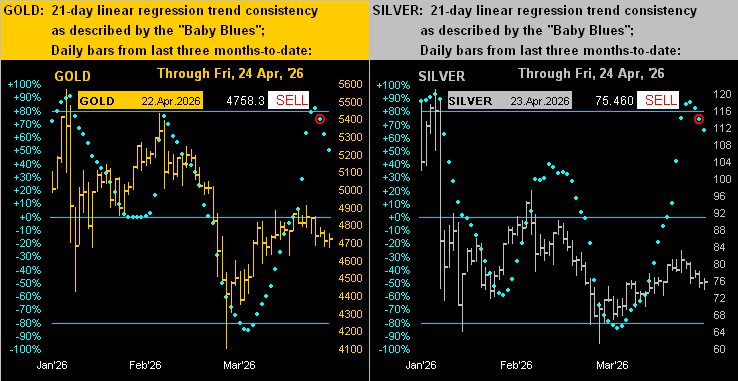

The Gold Update: No. 858 – (25 April 2026) – “Likely Lower Levels for the Precious Metals”

“Ahh, the breaking down of the ‘Baby Blues’, right mmb?”

Exactly so, Squire. The baby blue dots of 21-day linear regression trend consistency have been a favoured leading indicator of deMeadville for many years. (As a valued reader wrote to us better than a decade ago: “Let me not forget to tip my hat to the Baby Blues – they have made my trading far more successful and less stressful!”)

And specific to the above case for both Gold on the left and for Silver on the right, their respective “Baby Blues” have fallen through the key +80% axis per the red-encircled dots, the rule there being likely lower levels near-term.

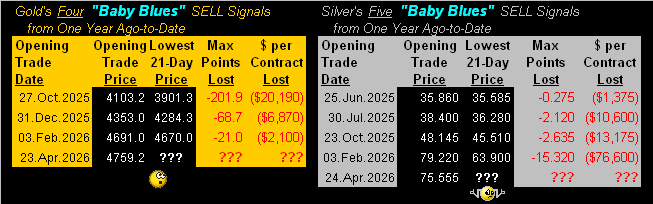

To wit, the fine team from our “There’s No Holy Grail Dept.” assembled this table of “Baby Blues” sell signals for both Gold (four) and Silver (five) from a year ago-to-date, even as we hasten to state that “Shorting Gold is a bad idea.” The maximum points and monetary losses/contract within the ensuing 21 trading days (one month) are therein compiled, the two new fresh signals with “???”:

Thus, as an appropriate musical ditty: ![]() “Where Do We Go From Here?”

“Where Do We Go From Here?”![]() –[Chicago, ’70]

–[Chicago, ’70]

‘Course, ’tis unknown as to how low the precious metals shall go, if at all. And by price structure, we don’t see anything helpfully tangible. So we went instead to ol’ Leonardo “Fibonacci” Bonacci to find some reasonable expectation for the downside. And here’s what “The Fibster” found:

- For Gold (June contract): it settled yesterday (Friday) at 4725. The dominant recent low was 4129 (22 March) and dominant high 4918 (17 April). Thus the Golden Ratio retracement range spans from 4616 (-38.2%) down to 4430 (-61.8%).

- For Silver (May contract): it settled yesterday (Friday) at 75.69. The dominant recent low was 61.21 (likewise on 22 March) and dominant high 83.25 (likewise on 17 April). Thus the Golden Ratio retracement range spans from 74.21 (-38.2%) down to 69.63 (-61.8%).

All that, just in case you’re scoring at home. Preferably however, Gold and Silver simply resume higher. Yet, ad nauseam we repeat: “Follow the Blues instead of the news, else lose yer shoes.”

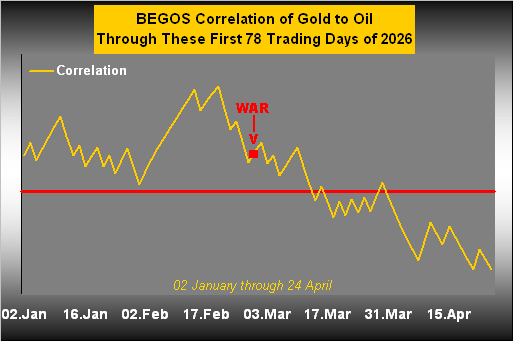

Either way, to be sure, Gold and “Big Oil” have been in a war phase of negative correlation. Restrain the transit of Oil and the price rises. In turn, the demand for Dollars with which to purchase Oil also rises. And whilst we’ve on occasion demonstrated over the years that “Gold plays no currency favourites”, in these warring times, the knee-jerk reaction is to sell Gold given the oxymoronic condition known as “Dollar strength”, which on balance (albeit not very consistently) been the case since the USA/IRN war commenced on 28 February. Indeed in the past week alone, the Buck made “higher daily highs” each of Monday through Thursday, although the “war-high” Dollar Index level of 100.500 remains above the current 98.340 level.

But the point is: rising Oil has led to declining Gold as we look at their BEGOS Markets (Bond / Euro / Gold / Oil / S&P 500) correlation through these first 78 trading days of 2026. Note the red square marking the war’s commencement, (Gold then 5296 vs. 4725 today, i.e. -10.8%). Beneath the red axis indicates negative correlation:

Toward closing, on a nightly basis for the website we run 405 Market Rhythm studies across all of the BEGOS Markets. And whilst nothing works in perpetuity for any market study, that which has been best for Gold through its last 10 swings is the four-hour Price Oscillator, (which is a “canned” study supplied by high-level data providers). In running this particular study through the deMeadville number-crunching, we found it to have reached an “in hindsight“ profit objective of at least 56 points 10-times in-a-row, (from 05 February-to-date with an average duration per swing of five calendar days). At $100/point/contract, here’s that “in hindsight“ profit picture:

Again we emphasize the above results are “in hindsight“.

“Yeah, but still, mmb, ten times back-to-back is amazing!”

Squire, this is where — again — cash management is of critical concern. You may recall the French Revolution survivor Pierre-Simon, Marquis de Laplace. Per his infamous “Rule of Succession”, in this case for something having occurred ten consecutive times, the probability of an eleventh like occurrence is mathematically 91.67%. HOWEVER (emphasized), in the reality of trading, the actual probability is 50.00%. Period. Do try not to get carried away.

But should precious metals near-term slip away, ‘tis good to still have Gold along the way!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

24 April 2026 – 08:40 Central Euro Time

Into week’s end we’ve at present Gold, Silver and Oil below today’s Neutral Zones; the other five BEGOS Markets are within same, and volatility for the session is light. Following (per yesterday’s comment) Gold having confirmed on Wednesday the “Baby Blues” of linreg consistency having moved below their key +80% axis, price since has dropped to as low as 4672; too, Silver’s “Baby Blues” yesterday confirmed moving below their +80% axis; more of course in tomorrow’s 858th consecutive Saturday edition of The Gold Update. The S&P 500 made a marginal record intraday high yesterday to (precisely) 7147.78, (the prior such high being on 17 April at 7147.52); the Index is now 11 consecutive days “textbook overbought”. The Econ Baro concludes its quiet week with the revision to April’s UofM Sentiment Survey.

23 April 2026 – 08:48 Central Euro Time

The Bond, Gold, Silver, Copper and the Spoo are all presently below today’s Neutral Zones; only Oil is above same, and BEGOS Markets’ volatility is mostly moderate, noting that Copper already has traced 103% of today’s EDTR (see Market ranges). By Market Trends, ironically Oil is the sole BEGOS component in negative linreg, as today at 94.23 price is well-down from 117.63 peak of three weeks ago. Thus Gold’s linreg is positive, however, its “Baby Blues” of trend consistency confirmed settling below the key +80% level yesterday such that still lower prices “ought be” in the near-term offing. Currently 4733, the mid-4600s would seem a reasonable destination, below which there is trading congestion through 4600-4400 zone; for pure swing consistency, Gold’s best Market Rhythms have been the daily Moneyflow (10-test basis) and the 15mn Moneyflow (24-test basis). For the Econ Baro we’ve just the usual Initial Jobless Claims from the prior week.

22 April 2026 – 08:42 Central Euro Time

All three elements of the Metals Triumvirate are at present above their respective Neutral Zones for today, whilst below same is Oil; volatility for the BEGOS Markets is mostly light, the largest EDTR tracing to this point being Oil at 49% (see Market Ranges). Oil’s best Market Rhythm for pure swing consistency on a 10-test basis is the 1hr MACD, whilst on a 24-test basis ’tis the 15mn Parabolics; Oil’s 21-day linreg trend is slightly becoming more negative as the “Baby Blues” of trend consistency have fallen below the 0% axis (see Market Trends); and by its Market Profile, Oil (currently 88.77) is trading below its most volume-dominant price for the past fortnight of 89.70. Nothing is due today for the Econ Baro. And Q1 Earnings season for the S&P 500 continues to run at an above-average pace: with 53 constituents thus far having reported, 44 (83%) have improved their quarterly year-over-year bottom lines; at issue, however, remains the dangerously high (futs-adj’d) P/E of 48.2x.

21 April 2026 – 08:44 Central Euro Time

Presently we’ve both precious metals below today’s Neutral Zones; otherwise, the balance of the BEGOS Markets are within same, and volatility is light. From an intra-day standpoint since the past week or two, the markets can best be characterized as “messy”. Regardless, let’s go ’round the horn (in real-time) for the Market Values of the five primary BEGOS components: the Bond is just -0^10 points “low” beneath its smooth valuation line, the Euro 0.013 points “high”, Gold -63 points “low”, Oil -6.16 points “low” (having reverted all the way back to its BEGOS valuation after having been some +34 points “high” at the beginning of April), and the Spoo +457 points “high”, the S&P 500 having completed a fifth consecutive session as extremely “textbook overbought”; too, by our MoneyFlow page (quarterly basis), the S&P “ought be” -597 points lower than ’tis. The Econ Baro looks to March’s Retail Sales and Pending Home Sales, plus Business Inventories for February.

20 April 2026 – 08:46 Central Euro Time

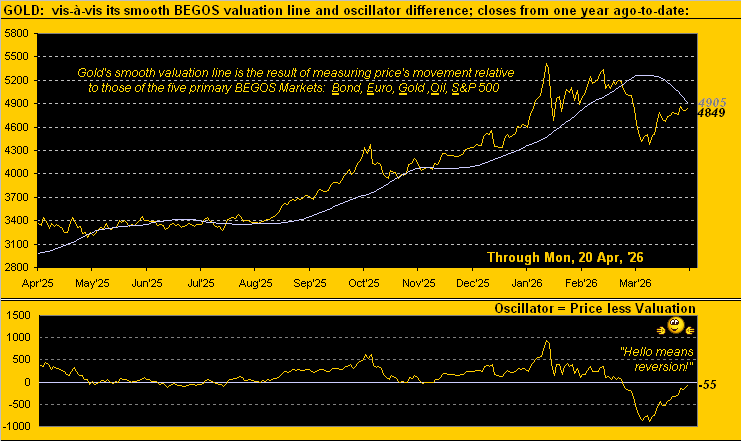

With events in the Middle East taking a negative turn, the BEGOS Markets today featured various “gap” openings, notably Oil which settled Friday at 85.57 opened up at 88.15, Gold from 4849 down to open at 4812 and the Spoo from 7164 down to open at 7103. At present, the Bond, Gold, Silver and Spoo are below today’s Neutral Zones, whilst Oil is above same, and session volatility is mostly moderate. The Gold Update points to price having nearly reverted back up to its BEGOS Market Value, whereas the S&P 500 having set a record high on Friday remains vastly overvalued by earnings (fundamental) as well as extremely “textbook overbought” (technical). Nothing is due today for the Econ Baro with a very light load in the week’s balance of just six incoming metrics. However, Q1 Earnings Seasons really starts to ramp up as its third week gets underway.

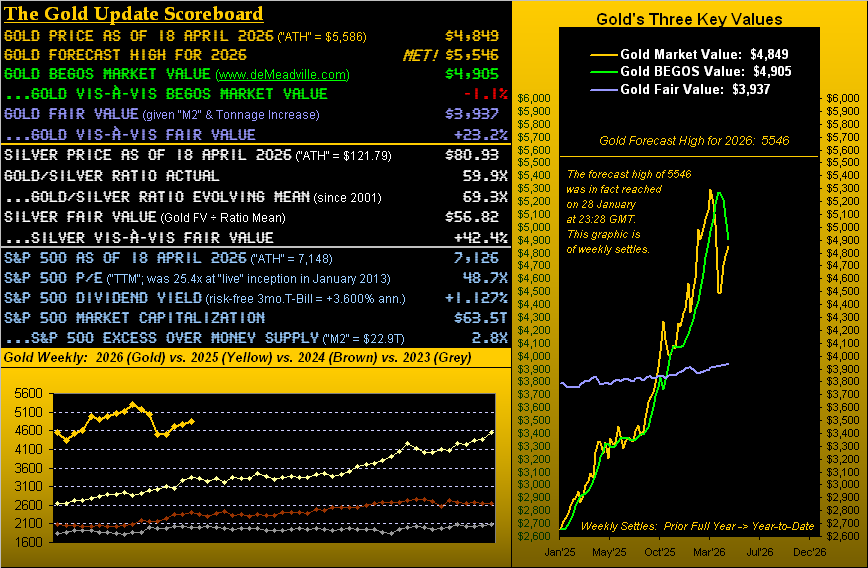

The Gold Update: No. 857 – (18 April 2026) – “Gold’s Means Reversion; S&P’s Record Excursion”

Moreover, in each trading day’s Prescient Commentary we cite the stance of the BEGOS Markets relative to their “Neutral Zones”: be a market higher or lower, if its price is within that day’s Neutral Zone, we deem the day as essentially “unchanged”. And across Gold’s past 10 trading days, five have concluded within the Neutral Zone.

“It’s kinda like that Chris Isaac song, right mmb?”

Squire is referring to the ’95 tune about the girl with dirty blonde hair wearing a taupe miniskirt whilst standing with her overnight case in the Greyhound bus station: ![]() “Goin’ Nowhere”

“Goin’ Nowhere”![]() .

.

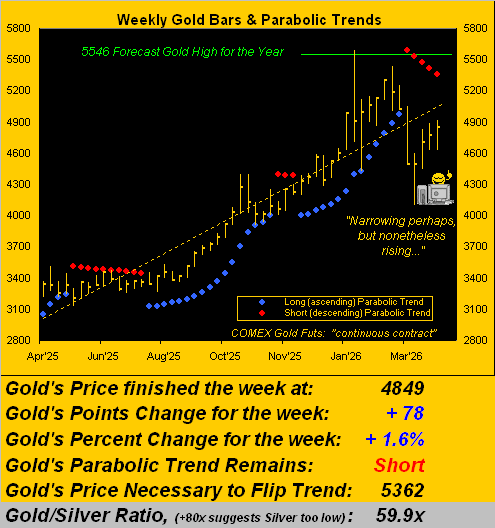

Not that Gold’s hasn’t gone anywhere. Price year-to-date has spanned from 5586 (our forecast high 5546) down to 4100 (our forecast low 4136), a range of -1486 points (-26.6%). ‘Course, with 179 trading days remaining in 2026, ’tis far too soon to “take credit” that we “nailed it”. But range has been nonetheless narrowing. Both of the past two weeks have recorded notably narrower trading ranges (262 and 292 points chronologically) than those of the three prior (571, 501 and 413 chronologically). So to Gold’s weekly bars we go, the red-dotted parabolic Short trend having completed its fifth week, such stance having commenced back on 16 March when priced opened at 5010:

Now we just made reference to the S&P 500, the mighty Index overvalued, overbought and overhyped beyond belief.

“Well, mmb, they say the war is winding down…”

Squire, it puts us in mind of the old saying “There’s been a sudden breakout of peace”, albeit so called “cease fires” carry a rather temporary tone. And now we’ve just learned the Straits of Hormuz have again been “closed”.

Regardless, ’twas but seven missives ago on 28 February that we penned “… in setting this morning to write our 850th consecutive Saturday missive, we’ve just learned of the commencement of USA/ISR attacks on IRN…” The S&P then was 6879, Oil 67.29 and Gold 5296. Today, Gold is -8% lower at 4849, Oil +27% higher at 85.57 (and at one point was +75% higher at 117.63) and the S&P now +4% higher at the record closing high of 7126. Were not higher energy prices to wreak havoc on corporate earnings?

To be sure, only the single war month of March is included in this Q1 Earnings Season, which whilst still quite young for the S&P 500 has thus far been excellent: 30 constituents have reported, of which 25 — that’s 83% — have bettered their bottom lines over Q1 of a year ago. Going as far back as 2017, the average quarterly year-over-year improvement is 66%. ![]() “Happy Days Are Here Again”

“Happy Days Are Here Again” ![]() –[Ager/Yellen, ’29]. However, problematic as we’ve time and again mentioned is that the nominal level of earnings need really to double toward supporting the stratospherically high level of the S&P; the median increase thus in Q1 earnings Season far is “only” +20% — which actually is great — but ’tis not the +100% “requisite” to get earnings in line with price.

–[Ager/Yellen, ’29]. However, problematic as we’ve time and again mentioned is that the nominal level of earnings need really to double toward supporting the stratospherically high level of the S&P; the median increase thus in Q1 earnings Season far is “only” +20% — which actually is great — but ’tis not the +100% “requisite” to get earnings in line with price.

Yet, so happy are the S&Pers that they’ve driven up the Index to now being (by our technical cocktail of Relative Strength, Stochastics and John Bollinger’s Bands) extremely “textbook overbought”, the price/earnings ratio a laughable 48.7x, with a pitifully puny yield of 1.127%, whereas noted in the opening Gold Scoreboard, the three-month annualized U.S. T-Bill yield is 3.600%. Again, that’s more than triple the S&P’s dividend return and you shan’t lose your money … at least not until the U.S. Treasury defaults and/or the Buck gets nixed as the world ‘s reserve currency. For you WestPalmBeachers down there, that is why you want to own Gold.

Meanwhile, to the suddenly sagging Econ Baro we go, ignored ‘natch by an S&P all aglow, the high P/Es list pulled from the website you know:

Toward our wrap, here’s the stack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 5586 (29 January 2026)

2026’s High: 5586 (29 January)

Gold’s All-Time Closing High: 5411 (28 January 2026)

The Weekly Parabolic Price to flip Long: 5362

10-Session directional range: up to 4908 (from 4628) = +280 points or +6.1%

Gold’s BEGOS Market Value (from our opening “Scoreboard”): 4905

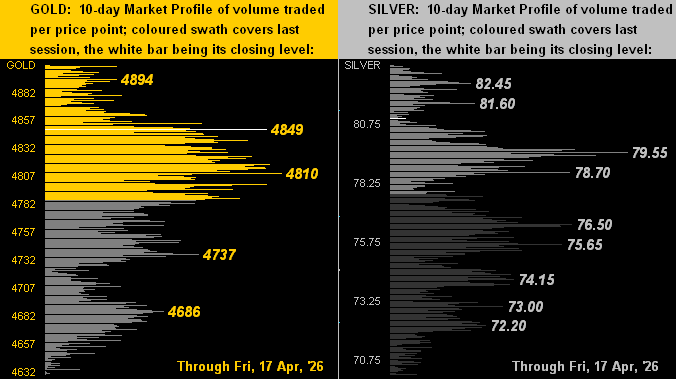

Trading Resistance: vis-à-vis the Market Profile, 4880 – 4910

Gold Currently: 4849, (expected daily trading range [“EDTR”]: 135 points)

Trading Support: vis-à-vis the Market Profile, the lower 4800s

10-Session “volume-weighted” average price magnet: 4785

2026’s Low: 4100 (23 March)

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3937

The 300-Day Moving Average: 3863 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

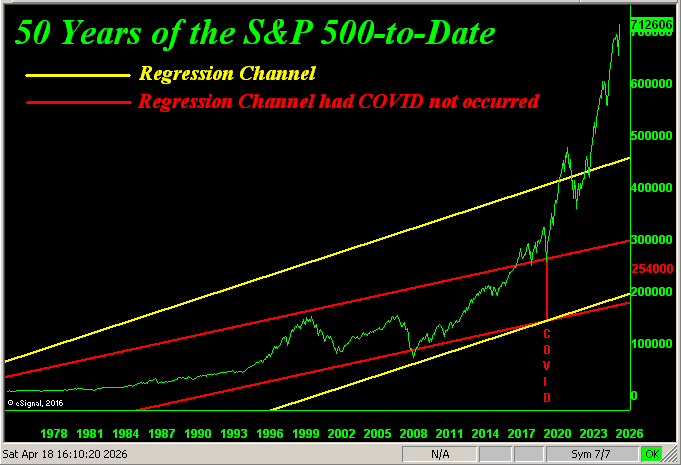

So as Gold gathers itself via means reversion, the S&P 500 has made a record high excursion. But is it really that impressive? After all, year-to-date Gold is now +11.9%, whereas the S&P is comparably +4.1%. Still, truth be told, both markets are fundamentally overvalued, Gold per its Fair Value and the S&P by its high (understatement) P/E. Gold indeed reverted well back down toward Fair Value when price plummeted to 4100 just this past 23 March, (Fair Value then 3890). But what about for the S&P? How far would price have to fall to bring the present dividend yield of 1.127% up to match the aforementioned T-Bill’s 3.600%? We put the question to “AI” (“Assembled Inaccuracy”), which responded thus:

- “Based on recent market data as of mid-April 2026, the S&P 500 would need to fall approximately 4,586 points to increase the dividend yield from 1.127% to 3.600%.”

Naturally, we followed-up with the math to find ‘twould be an S&P 500 “correction” of -64% to 2540 — right in the heart as below marked of the extrapolated “had COVID not occurred” red regression channel … just in case you’re scoring at home:

Query: How are those Gold n’ Silver holdings workin’ out for ya?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

17 April 2026 – 08:43 Central Euro Time

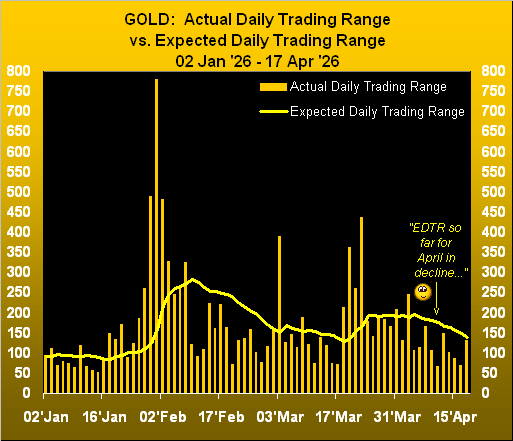

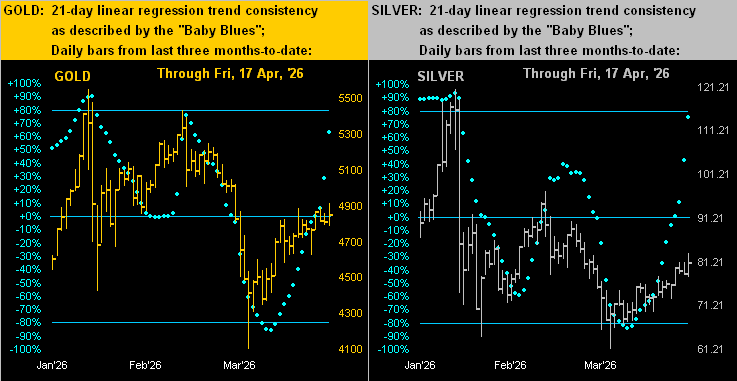

Presently, all eight BEGOS Markets are within their respective Neutral Zones for today, and session volatility is very light. The Bond (currently 113^20) yesterday moved under Market Profile support (114^06 now resistance) and price slid below the Market Magnet (114^01); nonetheless, by its Market Trend, the Bond’s linreg is positive and improving upside consistency given the rising “Baby Blues”. Gold again has been recording a comparatively narrow week; the yellow metal’s EDTR (see Market Ranges) has compressed from 196 points two weeks ago to now 140 points; further insight per tomorrow’s 857th consecutive Saturday Edition of The Gold Update. Nothing is due for the Econ Baro until next Tuesday. And Q1 Earnings Season for the S&P 500 is off to a well above-average start: of the 26 constituents having thus far reported, 22 (85%) have bettered their quarterly year-over-year bottom lines; problematic is that the nominal level of earnings is too low to support an S&P here at 7041, given the “live” (futs-adj’d) P/E of 47.8x.

16 April 2026 – 08:44 Central Euro Time

The S&P settled above 7000 yesterday at a record closing high of 7023, (intra-day 7026); the “live” (futs-adj’d) P/E is now 47.6x and the yield 1.126%, (that for the 3mo T-Bill annualized is 3.612%). At present for the BEGOS Markets, both Silver and Copper are above today’s Neutral Zones, the balance of the bunch being within same; session volatility is again light. By Market Values, the Spoo (in real-time) is +327 points above its smooth valuation line; the MoneyFlow for the S&P has notably improved so far this week; however by our broadest measure (63 days, i.e. one quarter), the Flow finds the Index +607 points too high. Cac volume for Oil has rolled from May into that for June with priced discounted by -2.80 points. And the Econ Baro completes its early week with metrics including April’s Philly Fed Index and March’s IndProd/CapUtil.