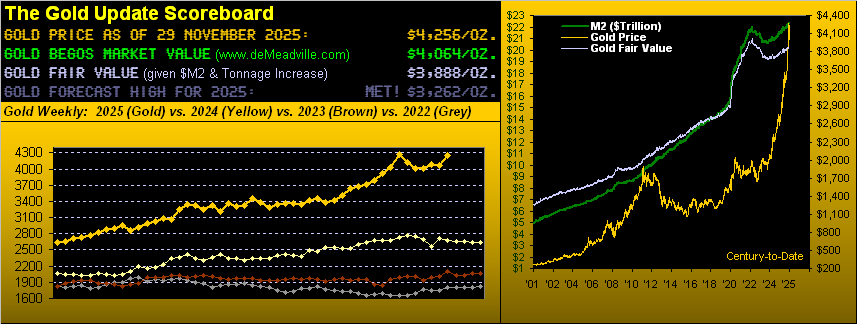

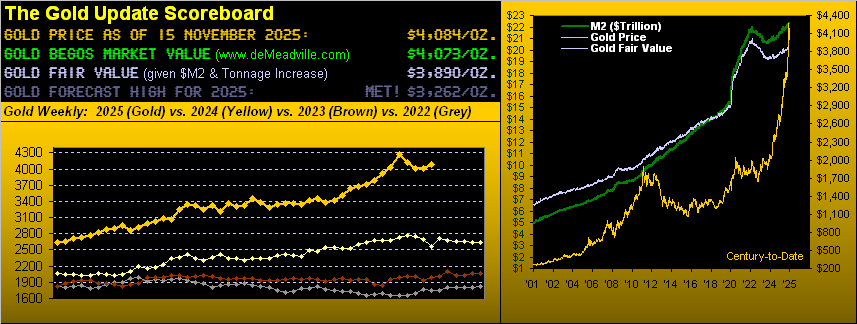

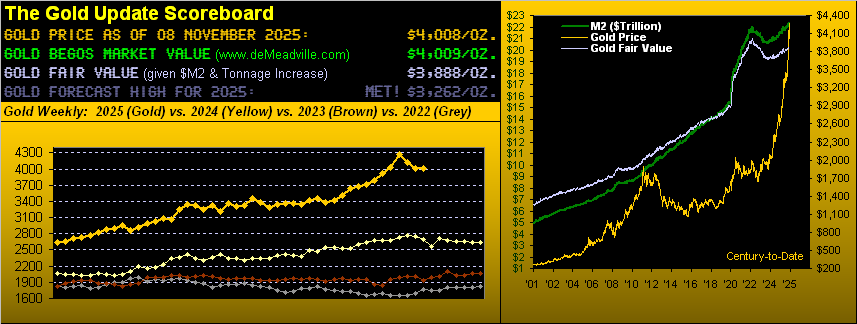

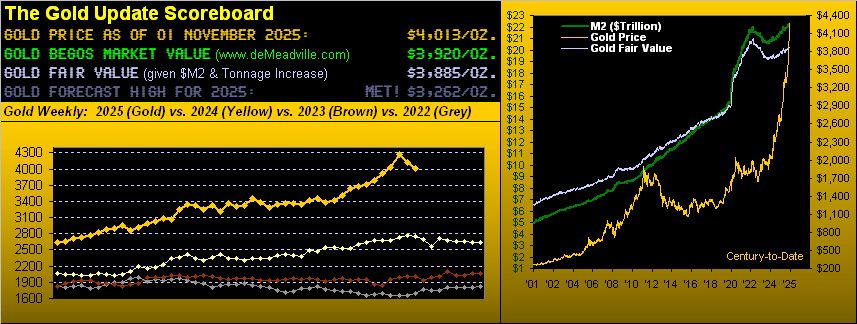

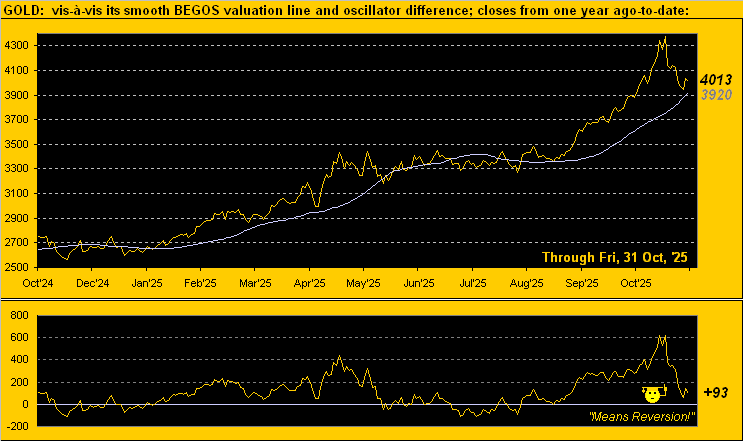

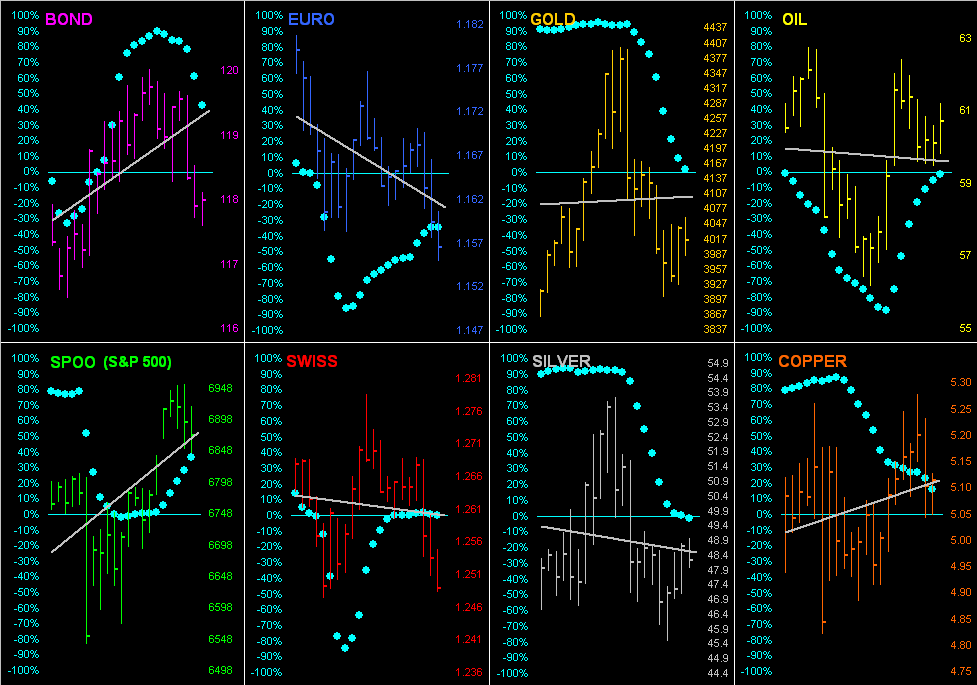

Gold yesterday by its “continuous contract” reached another All-Time High at 4410; (the “front month” currently is February, which itself had reached 4433 on 20 October but with a lot of forward “premium” at that time when ’twas not yet the “front month”). Either way, more on having achieved 4410 in tomorrow’s 840th consecutive Saturday edition of The Gold Update. For the present, with session volatility for the BEGOS Markets moving toward moderate, we’ve the Bond and Swiss Franc below today’s Neutral Zones, whilst above same are Silver and Copper. Of note, Copper’s “Baby Blues” for linreg consistency (see Market Trends) yesterday dropped below their key+80% axis indicative of lower prices near-term; Copper’s best Market Rhythm of late is its daily MACD. The Econ Baro looks to December’s revision to the UofM Sentiment Survey and November’s Existing Home Sales; due too are that month’s Personal Income/Spending and “fed-favoured” Core PCE Index: instead however may come the still unreported data for October, given the “shutdown”.

Mark

Mark

18 December 2025 – 08:40 Central Euro Time

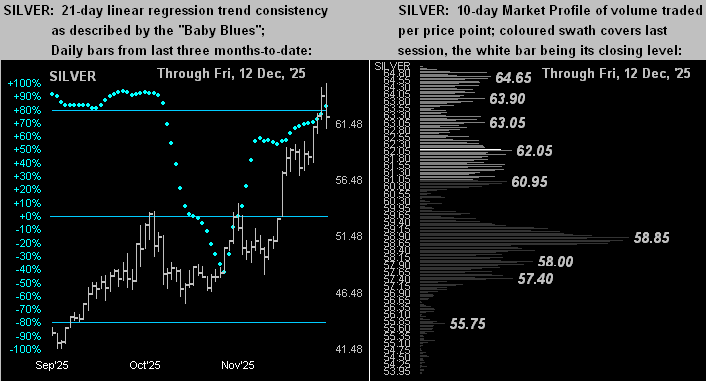

Another record high for Silver yesterday in trading up to 67.18 at which level year-to-date the white metal was up +129%; Silver currently is 66.61 and at present inside her Neutral Zone for today, as are all the BEGOS Markets, save for Oil’s being below same; session volatility is light. The NASDAQ 100 finished yesterday on a “Hobson Close” in settling on the low of the session, which by market lore is indicative of an up opening; indeed the Spoo is presently positioned for an opening S&P 500 gain of +22 points, placing the “live” futs-adj’d P/E at 54.2x. Too, the Spoo yesterday settled having crossed below its BEGOS Market Value, typically indicative of still lower prices near-term; the Spoo’s linreg trend remains up, but ’tis weakening (see Market Trends). Amongst the metrics expected today for the Econ Baro are December’s Philly Fed Index and November’s CPI; the Conference Board’s Leading (i.e. “lagging”) Indicators are “scheduled” but are not likely to be reported as the wake of the “shutdown” keeps the full view of the economy somewhat in question.

17 December 2025 – 08:40 Central Euro Time

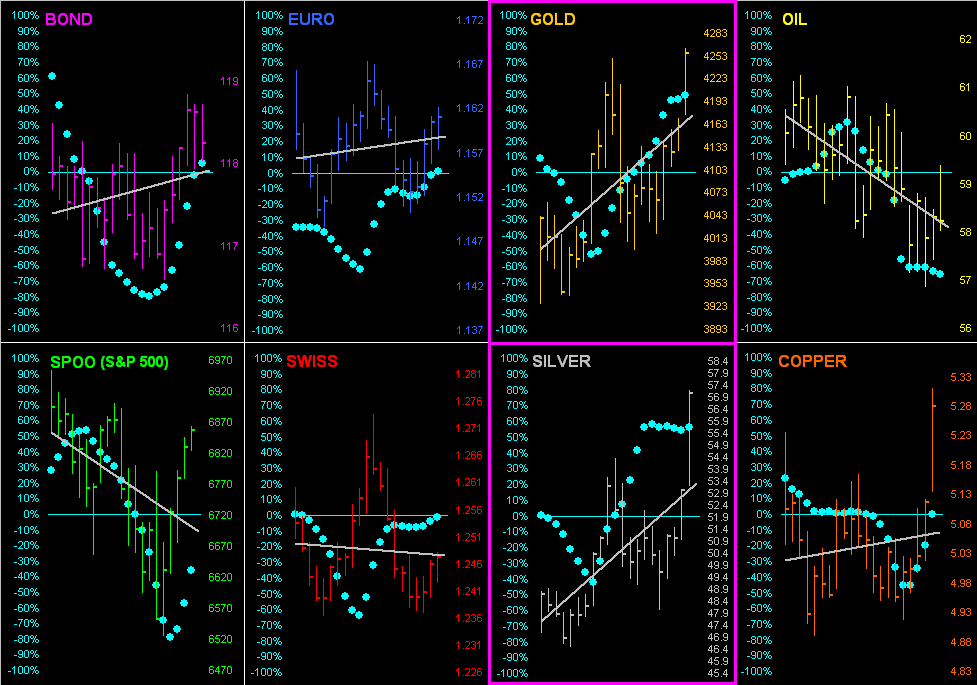

We’ve record highs for Silver this morning, up to as much as 66.65; and even as the Dollar Index is up a firm +0.5%, all three elements of the Metals Triumvirate are at present above their respective Neutral Zones for today, as is Oil; below same are the Bond, Euro and Swiss Franc, and session volatility for the BEGOS Markets is moderate-to-robust, Silver having thus far traced 119% of its EDTR (see Market Ranges). Looking at Market Values for the five primary BEGOS components: the Bond is -2^08 points “low” vis-à-vis its smooth valuation line, the Euro +0.013 points “high”, Gold +250 points “high”, Oil -3.72 points “low” and the Spoo +62 points “high”. Incoming data for the Econ Baro remains sporadic as “scheduled” reports in arrears are not necessarily being released; there are three metrics “due” for today (including November’s Retail Sales and October’s Business Inventories), but already they are indicated as likely not to arrive; either way, data that is being released has continued to move the Baro lower month-to-date.

16 December 2025 – 08:49 Central Euro Time

Presently we’ve the Metals Triumvirate and Spoo all below today’s Neutral Zones; the other BEGOS Markets are within same, and volatility thus far again is moderate. Save for Silver and Copper, EDTRs (see Market Ranges) of late have been narrowing. And by Market Trends, save for the Bond and Oil, the six other BEGOS components are in 21-day linreg uptrends. The Spoo’s moving from its December cac into that for March has added +59 points of premium to price; the March Spoo yesterday meekly moved up through significant Market Profile resistance before being swiftly sold back down; currently 6839, such resistance is 6908 up to 6926; the Spoo’s EDTR is 78 points. There are 11 metrics “scheduled” today for the Econ Baro, some in arrears and some timely; they notably include: November’s Payrolls data (to fold in as able some of that for October which was not reported), IndProd/CapUtil, October’s Retail Sales, plus September’s Housing Starts/Permits and Business Inventories.

15 December 2025 – 08:37 Central Euro Time

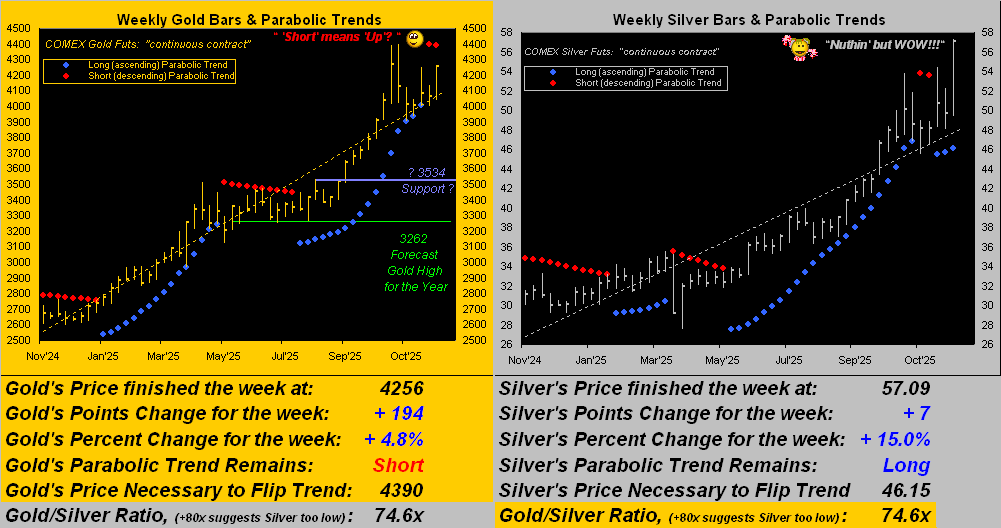

The final full trading week of the year begins, finding at present the Bond and Metals Triumvirate above their respective Neutral Zones for today; none of the other BEGOS Markets are below same, and session volatility is moderate. The Gold Update celebrates Silver having surpassed 60, and the yellow metal’s weekly parabolic trend having flipped from yet another “short-lived” Short stint (just 3 weeks) to Long; presently 4377, Gold is only -21 points below its record 4398 high; by their Market Profiles, Gold’s most volume-dominant support is 4237 and for Silver (currently 63.43) ’tis 58.85. Oil’s cac volume is moving from January into that for February, and that for the Spoo from December into March. Purportedly “scheduled” this week for the Econ Baro are 26 metrics, some delayed, some current: for today we await December’s NY State Empire Index and the NAHB Housing Index.

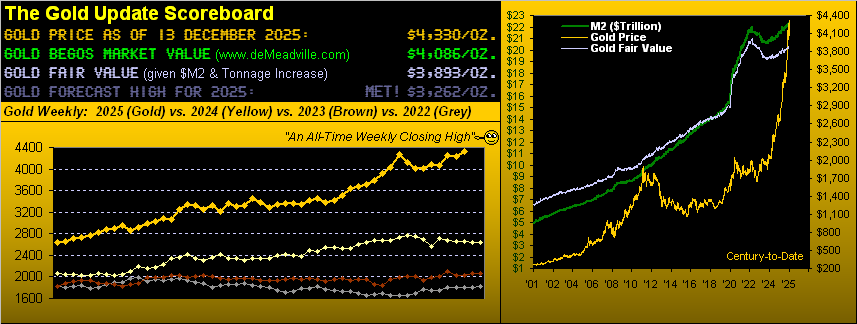

The Gold Update: No. 839 – (13 December 2025) – “Gold Beams Back To Long; Silver Screams So Strong!”

Indeed, Sweet Sister Silver, few took notice of you until just recent weeks. And yet, what an incredible year you’ve had! Like Gold, your settle yesterday at 62.09 is an All-Time Weekly Closing High, which per the above table places you +112% year-to-date, let alone your having also en route achieved an All-Time Intraday High to 65.09, at which price you momentarily were +122% in 2025.

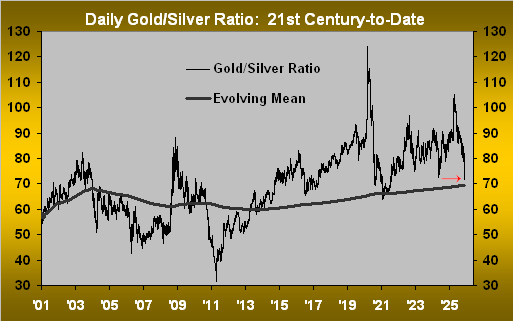

Moreover: as herein a week ago graphically portrayed would be inevitable, the Gold/Silver ratio fully reverted to its evolving mean (69.4x century-to-date), penetrating it to 66.7x during Thursday; (it settled the week at 69.7x).

And for the “johnny-come-lately” FinMedia came the usual “having just figured it out” hype. “Oh Silver is going to 100!” they say; “Oh Silver is gonna hit 200!!” they say; “Oh Silver will get to 300!!!” they say. (Yes, we’ve seen all three prognosticative “reports”).

But we “say” let’s instead do the math, ok? For what reasonably is Silver’s Fair Value today?

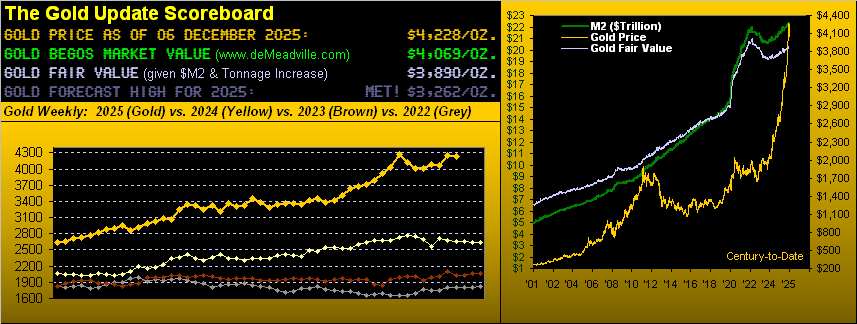

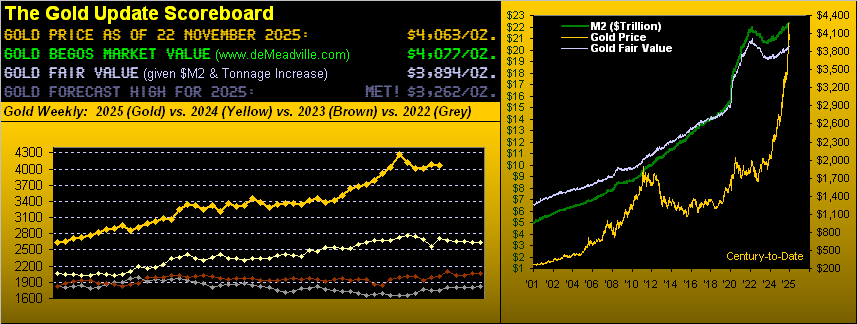

Again, ’tis a simple calculation as we’ve previously presented. Per the opening Gold Scoreboard, the Fair Value for the yellow metal is presently 3893. Divide that by the mean of the Gold/Silver ratio (69.4x) et voilà the Fair Value of the white metal is now 56.08. Thus currently priced at 62.09, we may “say” that Silver is +11% overvalued. Too, by her “textbook technicals” (our cocktail of Relative Strength, Stochastics and John Bollinger’s Bands), Silver is now 22 consecutive trading days “overbought”; (by comparison, Gold and Copper both are 11 days “overbought”) … all that just in case you’re scoring at home.

But: at least Silver finally has achieved an area of rational market valuation. “Brava Brava, Sista Silva!!”

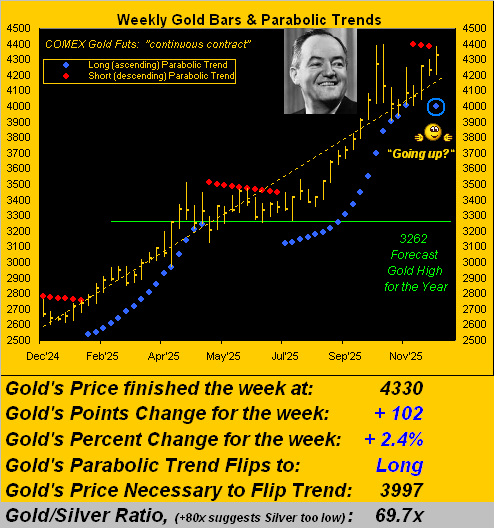

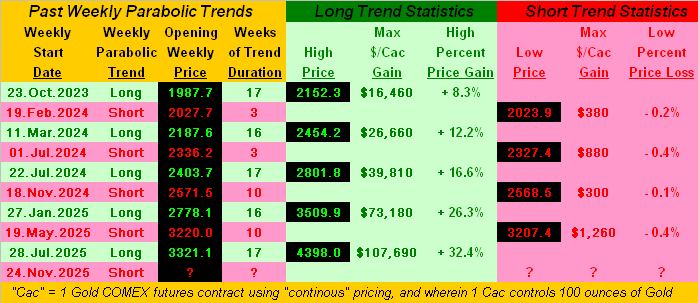

As for good old precious Gold, on its way to making this fresh All-Time Weekly Closing High, the weekly parabolic Short trend again met a “short-lived” end. Since February 2024, there have been five such parabolic Short trends of 3, 3, 10, 10 & 3 weeks; but those Long have been 17, 16, 17, 16 & 17 weeks. Indeed, the similarity of the Long trends’ durations is striking: ![]() “Uh oh, it’s magic”

“Uh oh, it’s magic”![]() –[The Cars, ’84]. And now a new one has begun, (technically come Monday’s open),

–[The Cars, ’84]. And now a new one has begun, (technically come Monday’s open),

However, ’tis actually not magic; rather ’tis math that makes the next graphic’s newly-encircled blue dot appear. And today priced at 4330, Gold in 2025 is +64%, with the All-Time Intraday High from 20 October still in place at 4398. As for the just “failed” Short trend of only three red-dotted weeks, it opened on Monday 24 November at 4069 and was snuffed out yesterday at 4330. (Reminder: “Shorting Gold is a bad idea”). Rather, we’re “pleased as punch” indeed, HHH:

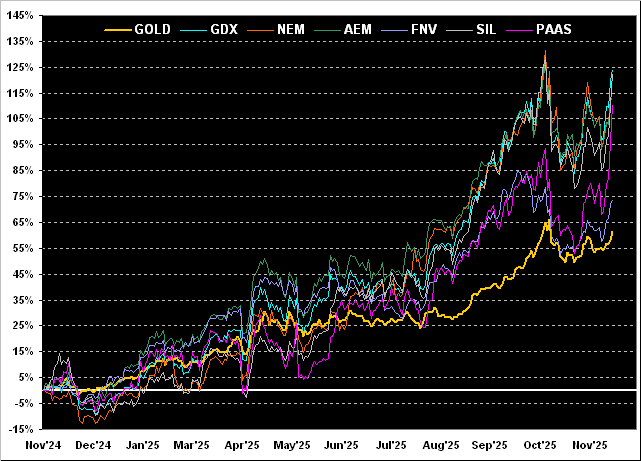

Thus year-to-date for the precious metals ’tis been great, albeit arguably quite extended given both Gold and Silver presently +11% above Fair Value. In fact by rounding out the Metals Triumvirate, Copper also is having a fine year +33%, its sixth-best this century. That, too, has brought some bounce to Sister Silver from her industrial metal aspect, although we can also credit Copper as being money, certainly so from the Bronze Age (2000 BC).

Regardless, per our title, Gold has beamed back to Long with Silver screaming so strong! Which reminds us that upon blending in your Osterizer precious Gold with industrial Copper and pressing “puree”, you of course get Silver! (Metallurgists, please hold your email):

Either way, collect all three today!!!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

12 December 2025 – 08:39 Central Euro Time

Presently, all eight BEGOS Markets are within today’s Neutral Zones, and session volatility is light. Silver yesterday traded up to a record high of 64.72, however by Fair Value, the white metal has become quite overvalued: more on that in tomorrow’s 839th consecutive Saturday edition of The Gold Update. Amongst the five primary BEGOS components, we’ve currently no notable correlations. The Dollar Index yesterday traded down to its lowest level (98.135) since 24 October. The S&P 500 yesterday reached its highest level (6903) since the all-time high of 6920 on 29 October. Volume for the currencies (Euro, Swiss Franc and the non-BEGOS Yen) is moving from their respective December cacs into those for March. And nothing is scheduled today for the Econ Baro, albeit some four dozen metrics remain missing per the six-week Oct-Nov StateSide “shutdown”.

11 December 2025 – 08:41 Central Euro Time

The Bond is presently above its Neutral Zone for today, whilst below same are Copper, Oil and the Spoo; session volatility for the BEGOS Markets is firmly moderate. As anticipated, the FOMC voted with dissent to nonetheless cut the FedFunds rate -25 bps to the 3.50%-3.75% target range: the S&P 500 responded in moving to its highest level (6901) since 29 October (wherein the all-time high of 6920 still stands); however, overnight selling has pushed the Spoo (6840) lower towards its BEGOS Market Value (6801), the futs-adj’d “live” P/E at 57.7x. Silver has recorded another record high this morning at 63.25, however has since slipped back into today’s Neutral Zone. And incoming metrics “scheduled” in arrears today for the Econ Baro are both September’s Trade Deficit and Wholesale Inventories.

10 December 2025 – 08:42 Central Euro Time

Silver yesterday topped 60.00 for the first time and thus far today has traded to as high as 62.14, the Gold/Silver ratio having fully reverted to its century-to-date evolving mean of 69.4x, the ratio currently 68.3x; the white metal is at present above its Neutral Zone for today, as is Copper; the rest of the BEGOS Markets are within same, and session volatility is light. Silver’s best Market Rhythm is currently (if seeking a targeted outcome of 0.52 points) is the 12hr MACD, or on a pure swing basis the 6hr MACD; of note, Gold these last couple of weeks continues not to confirm Silver’s rally. What is “scheduled” for the Econ Baro versus that which is actually released of late is patchy at best: expected for today is November’s Treasury Budget, plus in arrears, Q3’s Employment Cost Index. Then come 19:00, look for the FOMC (not unanimously) to lower the FedFunds rate by -0.25% to the 3.50-3.75% target range.

09 December 2025 – 08:37 Central Euro Time

Only Copper is at present outside (below) its Neutral Zone for today; moreover, it already has traced 106% of its EDTR (see Market Ranges); otherwise, BEGOS Market’s volatility is mostly light. By Market Rhythms, Copper’s best is its daily MACD. Too, ’tis unusual to see one market dominating our Top Three Rhythms for pure swing consistency, but on a 10-test basis, ’tis the Euro’s 15mn Parabolics, 1hr EMA, and 6hr MACD. Yesterday’s S&P 500’s MoneyFlow (+0.2%) was firmer than the Index itself (-0.3%); the Spoo’s trading range is narrowing: the EDTR just back on 25 November was 119 points; today ’tis 83 points. “Scheduled” today for the Econ Baro are the Q3 revisions to Productivity and Unit Labor Costs, the preliminary readings for which were not reported given the “shutdown”.

08 December 2025 – 08:42 Central Euro Time

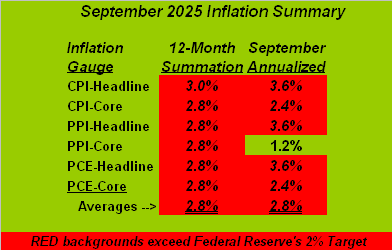

Presently, the Euro is the only BEGOS Market outside (above) its Neutral Zone for today; session volatility is light-to-moderate. The Gold Update points to Silver having nearly reached the milestone of 60.00 (59.90 on Friday); too, we calculated a Fair Value for Silver at 56.05. Also therein, September’s inflation summary table is indicative of paces running above the Fed’s desired 2% target range such that they ought not cut the Funds rate come Wednesday, but likely shall so do given a weakening jobs market at least by ADP data; (recall the BLS was shutdown for six weeks). As the Spoo meanders higher this morning, the S&P 500 looks to start its week with a “live” P/E of 58.2x. For the five primary BEGOS components per their Market Values (in real-time): the Bond is -2^10 points below its smooth valuation line, the Euro basically in sync nears its line, Gold +168 points above same, Oil in sync, and the Spoo +88 points over its line. Nothing is scheduled today for the Econ Baro.

The Gold Update: No. 838 – (06 December 2025) – “Gold Sinks Slightly as Silver Skirts Sixty”

And yes, Virginia, in that display the price/earnings ratio of the S&P 500 truly is now an “off the edge of the bell curve” 58.0x, the mighty Index having settled yesterday at 6870, a mere -50 points below its all-time intraday high of 6920 (29 October). ‘Tis too bad earnings are not sufficient enough to keep pace with price, (let alone an “M2” money supply of $22.4T that is vastly unsupportive of the S&P’s $60.8T market capitalization). Reprise: ![]() “When the levee breaks…”

“When the levee breaks…”![]() –[McCoy/Minnie ’29; Led Zeppelin ’71].

–[McCoy/Minnie ’29; Led Zeppelin ’71].

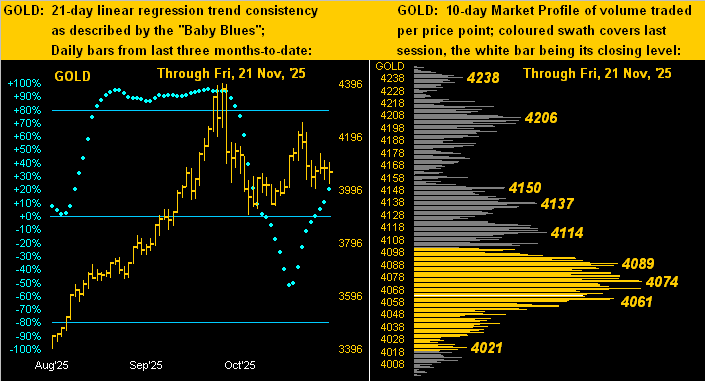

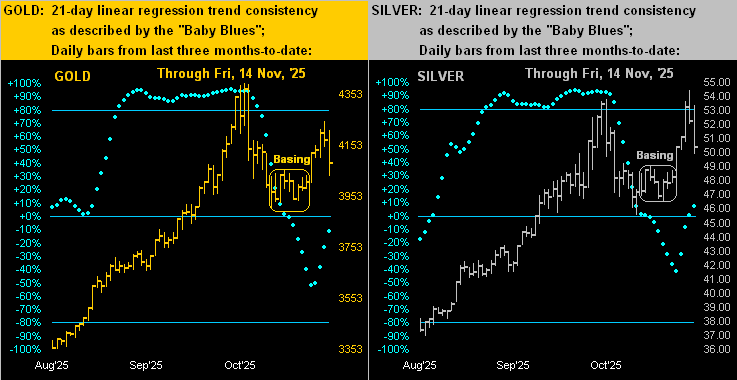

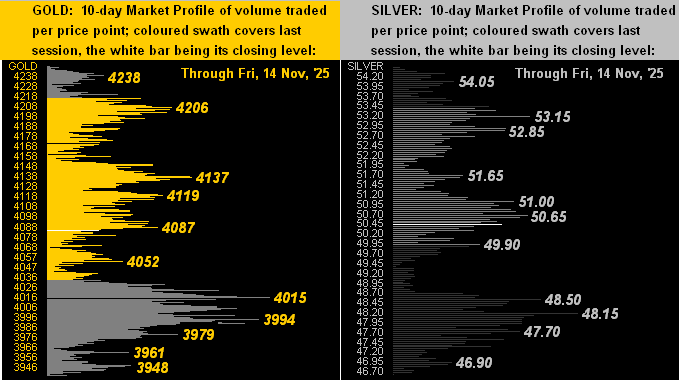

However, hovering of late as if a zeppelin unto itself has been Gold. But as we turn to the two-panel display of Gold’s daily bars from three months ago-to-date on the left and 10-day Market Profile on the right, one senses some descent. Note therein the “Baby Blues” of regression trend consistency having ticked lower for the past two days. Too, price has slipped below its most volume-dominant Profile support level of 4237. Not that this absolutely turns the tide, but it does remind us that hardly do markets move in a straight line:

To wrap, per our title, Gold sank slightly (-0.7% net for the week) as Silver skirted sixty (+3.0% net for the week). And now Sister Silver sits at 58.80, a mere 1.20 points from 60.00, with an expected daily trading range of now 2.24 points. By such yardstick, Silver can grab 60.00 come Monday. But then there’s Wednesday and the aforementioned FOMC Policy Statement on the Funds Rate. A cut almost surely shall see Silver eclipse 60.00. But what if the Committee instead abstains?

To wit: as longtime readers of The Gold Update know, our microphones are just about everywhere, including last week at the Eccles Building in D.C. wherein a small contingent of Silver traders came down on the bus from the COMEX in N.Y. to plead Powell for another rate cut. Squire even arranged for an inconspicuous MINOX camera to capture the moment:

But should such plea fail a cut by which to abide — and prices thus decide to slide — keep Gold and Silver for the ride!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

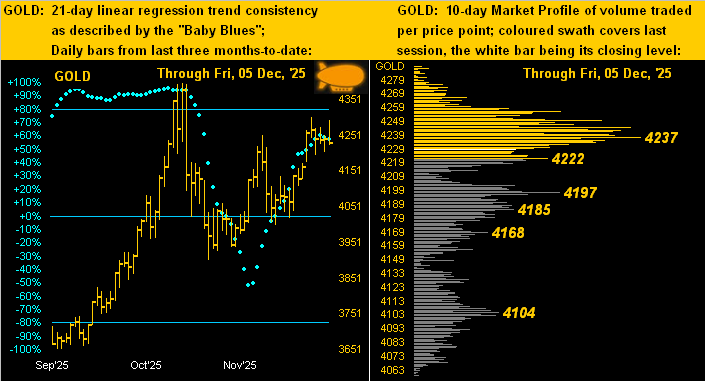

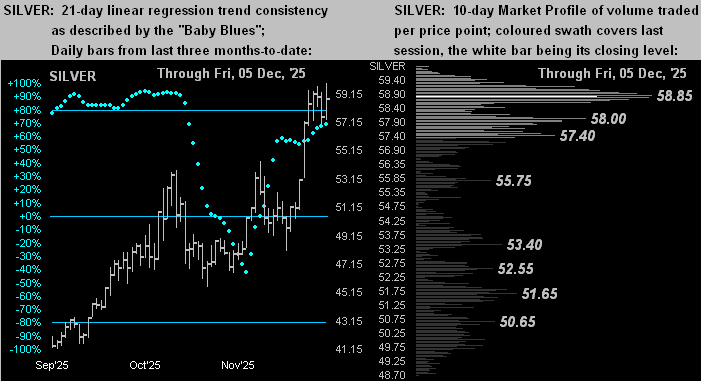

05 December 2025 – 08:41 Central Euro Time

The EuroCurrencies and Metals Triumvirate are all above today’s Neutral Zones; none of the other BEGOS Markets are below same, and session volatility is on balance moderate, Copper however having already traced 130% of its EDTR (see Market Ranges). The Spoo has thus far traded up to 6884, its highest level since 13 November; too, the Spoo’s “Baby Blues” of linreg consistency (see Market Trends) have inched back above their 0% axis, the trend having rotated from negative to positive despite the “textbook overbought” condition of the S&P 500 itself; the Spoo settled last evening an excessive 126 points above its Market Magnet; currently 6882, the Spoo’s most volume-dominant supporter is 6863. Gold is completing its third week of the parabolic Short trend, the past two weeks of which have been up; more on that in tomorrow’s 838th consecutive Saturday edition of The Gold Update. And scheduled for the Econ Baro are December’s UofM Sentiment Survey, October’s Consumer Credit, plus purportedly in arrears, September’s Personal Income/Spending and “Fed-favoured” Core PCE.

04 December 2025 – 08:41 Central Euro Time

The Bond, Swiss Franc and Silver are all presently below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and volatility to this point of the session is light-to-moderate. Silver’s daily bars have the appearance of a near-term top being put in place despite yesterday’s all-time high of 59.66, (price now 57.99); Silver’s best swing Market Rhythm if seeking a profit target (0.84 points) is the 6hr Moneyflow, whereas on a pure swing basis ’tis the 4hr Parabolics. Meanwhile the S&P 500 has worked its way up technically to a moderately “textbook overbought” condition; more importantly, the fundamental reality of the “live” (futs-adj’d) P/E of now 58.7x is essentially off the end of the Bell Curve. Metrics scheduled today for the Econ Baro include October’s Trade Deficit and September’s Factory Orders.

03 December 2025 – 08:33 Central Euro Time

Presently above today’s Neutral Zones are the Euro, Swiss Franc, Copper and Oil, whilst below same is Silver; session volatility for the BEGOS Markets is pushing toward moderate. Yesterday for the Swiss Franc, price settled above the most volume-dominant Market Profile resistor, as well as pierced above its Market Magnet. Currently topping our Market Rhythms for pure swing consistency are (on a 10-test basis) the Swiss Franc’s 8hr MACD and for Silver both its 2hr MACD and 4hr Parabolics, plus (on a 24-test basis) the Euro’s 4hr MACD, Silver’s 2hr Parabolics, and the non-BEGOS Yen’s 4hr MACD. The Econ Baro looks to November’s ADP Employment data ISM(Svc) Index, and perhaps in “shutdown” arrears September’s Ex/Im Prices and IndProd/CapUtil.

02 December 2025 – 08:44 Central Euro Time

Silver, after achieving another all-time high yesterday at 59.44 — then year-to-date +103% — is at present below today’s Neutral Zone; the balance of the BEGOS Markets are within same, and session volatility is light. The S&P 500’s mid-November correction of some -350 points and subsequent return back up was enough to unwind any textbook technical overbought/oversold conditions; however, the “live” (futs-adj’d) P/E of 56.1x remains our biggest overvaluation (understatement) concern. Specific to the Spoo by Market Trends, its linreg had rotated from positive to negative effective 17 November, but as the “Baby Blues” of trend consistency are recovering, such trend looks to rotate back to positive in a day or two, barring substantive selling; for consistent swing trading, the Spoo’s best Market Rhythm of late has been the 30mn Price Oscillator. Nothing is scheduled today for the Econ Baro.

01 December 2025 – 08:34 Central Euro Time

Both the Bond and Spoo are at present below today’s Neutral Zones, whilst above same is Oil; session volatility for the BEGOS Markets is firmly moderate as December commences. The Gold Update celebrates Silver’s remarkable year, through Friday +94.9%, and even more so this morning, having hit another all-time high at 58.61. Silver’s best Market Rhythm for pure swing consistency has been the 2hr MACD, or for targeted profit (0.84 points/cac) the 6hr Moneyflow; and Silver’s EDTR (see Market Ranges) is 2.13 points/day. Meanwhile Gold at 4275 is -123 points below its record high level of 4398 (20 October). For the Econ Baro we’ve November’s ISM(Mfg) Index plus (purportedly) September’s Construction Spending, one of 49 “missing” metrics from the StateSide “shutdown”.

The Gold Update: No. 837 – (29 November 2025) – “Gold’s New Short Trend Shoved Aside; Silver’s Rise to All-Time Highs”

“So can we play your tune, mmb?” Spin it, Squire:

![]() “Follow the Blues instead of the news, else lose yer shoes”

“Follow the Blues instead of the news, else lose yer shoes”![]()

(Squire has this closet DJ thing going on of late).

Now to peek at the Economic Barometer and accompanying S&P 500 (red line). And you know the old expression that when government is out of the way, (i.e. “gridlock is good”), the economy is less suffocated. However: even though nearly three weeks have passed since the StateSide “shutdown” was resolved, there actually is an increase in missing metrics as bureaus are strained to “catch-up”. In fact, since 01 October, there’ve been 98 scheduled Econ Baro metrics, of which half (49) are now missing; a week ago ’twas 46. All that said, such absence of data has evolved into a rising Baro such that we penned in yesterday’s Prescient Commentary “…the Econ Baro has returned to its highest level since last February, which if detected by the FOMC may see rates held steady rather than cut come the 10 December Policy Statement….”:

Sadly of course per the graphic, earnings remain unsupportive of the S&P’s catastrophically high price level. (But then again, that’s archaic old-school piffle; today nobody cares).

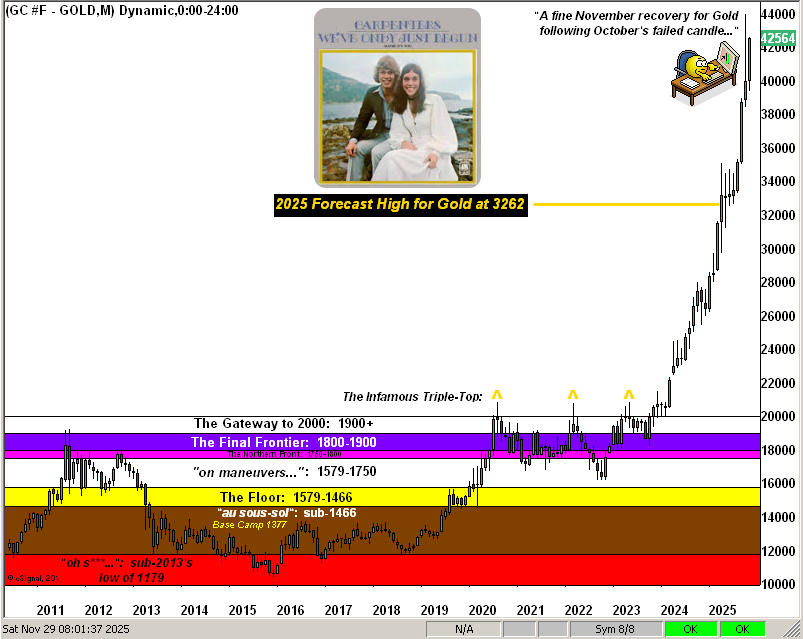

Toward this week’s wrap we’ve the Gold Structure by the month across the past 16 years. Concern over the last month’s “failed” October candle was short-lived, albeit let us be cognizant that we’ve only just begun a weekly parabolic Short trend, (which with bullish persistance, too, shall fail of its own accord).

“Here ya go mmb, Carpenters 1970…” ![]() “We’ve only just begun…”

“We’ve only just begun…”![]()

Indeed, “DJ” Squire. Aren’t you instead supposed to be on avalanche control this time of year?

“Yeah mmb, during next month up in the Haute-Tarentaise.”

You might mind the S&P as well, Squire, as when it goes over the cliff, ’tis gonna be scary! Meanwhile, here’s the happy Gold Structure:

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

28 November 2025 – 08:28 Central Euro Time

Subject to the CME data outage from 02:45 GMT (03:45 CET): Silver is teasing another all-time high; by the March cac ‘twould be 55.06, the current price being 54.64; more tomorrow in the 837th consecutive Saturday edition of The Gold Update. The two-day session continues for the BEGOS Markets, currently finding both the Bond and Euro below their Neutral Zones whilst above same are Gold and Silver; session volatility (inclusive of yesterday) is now moderate. For the five primary BEGOS components per their Market Values in real-time: the Bond is +0^17 points “high” above its smooth valuation line, the Euro essentially on same, Gold is +157 points “high”, Oil -0.66 points “low” and the Spoo +60 points “high”. Albeit there remain many missing metrics due to the recent StateSide “shutdown”, the Econ Baro has returned to its highest level since last February, which if detected by the FOMC may see rates held steady rather than cut come the 10 December Policy Statement.

27 November 2025 – 08:47 Central Euro Time

‘Tis a BEGOS Market’s two-day session for Friday settlement, with trading halts later today and early closures tomorrow. At present, we’ve Silver above its Neutral Zone and having traded as high as 54.43 as it nears its all-time high (basis March) of 55.06; below today’s Neutral Zone is Copper, and overall session volatility thus far is light. Looking at correlations within the five primary BEGOS components, our best currently is positive between Gold and Oil, both having been mildly down since late October, albeit by Market Trends (on a slightly shorter timeframe), Gold’s linreg is positively-sloped whereas that for Oil is negative. The Econ Baro is recording “delayed data” as it becomes available, however overall, many metrics remaining missing, and as the BLS stated last week, some reports simply shan’t ever be assembled; regardless, the tilt of the Baro for most of November has been up. A very Happy Thanksgiving to you StateSiders over there!

26 November 2025 – 08:39 Central Euro Time

Both the Swiss Franc and Silver are presently above their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and session volatility is light-to-moderate. By Market Rhythms for pure swing consistency, our Top Three on a 10-test basis are the Euro’s 4hr MACD, Silver’s 4hr Parabolics, and Gold’s 12hr Moneyflow; for the 24-test basis they are the Euro’s 15mn Parabolics, Silver’s 1hr MACD, and Copper’s daily Parabolics. Although yesterday’s S&P 500 change was +0.9%, its MoneyFlow regressed into S&P points was -0.5%: mind the MoneyFlow page. Due to the recent StateSide “shutdown”, there is conflict amongst reporting entities as to which Econ Metrics actually shall come through: likely for today we’ll at least receive November’s Chi PMI (an earlier date than usual given tomorrow’s holiday), plus purportedly from back in September both Durable Orders and New Home Sales.

25 November 2025 – 08:39 Central Euro Time

Copper is at present above today’s Neutral Zone, whilst below same is Oil; BEGOS Markets’ volatility is again light. Gold nicely commenced its new weekly parabolic Short trend by — as surmised in The Gold Update — firmly rising yesterday, (albeit that doesn’t preclude there not being lower levels in the offing); too, Gold’s cac volume today is rolling from December into that for February, inclusive of +37 points of fresh premium; rolling as well today is Silver’s cac volume from December into that for March, (and to follow today/tomorrow is same for the Bond). At Market Trends, six of eight linregs are negative, the only two positives being those for Gold and Silver. Scheduled for the Econ Baro are November’s Consumer Confidence, October’s Pending Home Sales, and in playing “catch-up”, September’s PPI and Retail Sales.

24 November 2025 – 08:40 Central Euro Time

Presently, all eight BEGOS Markets are within today’s Neutral Zones, and session volatility is light. The Gold Update cites price’s weekly parabolic trend as having confirmed the anticipated flip from Long-to-Short, but in the context that Short trends within the past two years have had negligible negativity, and thus in hindsight have been buying opportunities. Q3 Earnings Season is complete with 71% of S&P 500 reporting constituents improving their quarterly year-over-year bottom lines, which favourably compares with typical improvement of 66%; still, the overall level of earnings is far too low to maintain the “live” (futs-adj’d) P/E of the S&P of 51.8x at this instant. Copper’s cac volume is rolling from December into that for March. And whilst no fresh metrics are scheduled for the Econ Baro, there may be some “catch-up” data on IndProd/CapUtil for September, which of course we’ll duly incorporate.

The Gold Update: No. 836 – (22 November 2025) – “Gold’s Key Weekly Trend Flips Short”

As for Gold, we’ll watch how the new Short trend unfolds. If such history from the past two years holds, for buyers ’tis a time to be bold! Nonetheless, in any event, hang on to your Gold!

Oh Squire, you shouldn’t have… Rather, go fetch the rain-chilled Taittinger!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

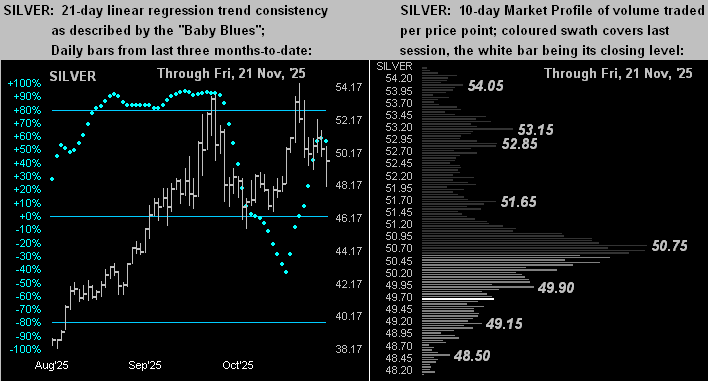

21 November 2025 – 08:34 Central Euro Time

We’ve presently the Euro, Swiss Franc and Spoo above their respective Neutral Zones for today, whilst below same are Gold, Silver and Oil; session volatility for the BEGOS Markets is again moderate. Amongst the five primary BEGOS Markets, the best correlation currently is negative between the Bond and the Spoo. The latter thus far today has traded to its lowest level (6539) since 08 September, the selling rather anticipated given the ongoing — indeed leading — plunge of the Spoo’s “Baby Blues” (see Market Trends). Yesterday saw a “data dump” from the Dept. of Labor for some seven Initial Jobless Claim reports as the Econ Baro continues to bring in metrics missing from the recent StateSide government “shutdown”; scheduled for today is November’s revised UofM Sentiment Survey. Tomorrow brings the 836th consecutive Saturday edition of The Gold Update. And we’ve reached the final day of Q3 Earnings Season, for which the S&P 500 year-over-year has been well above its average improvement, but remains well below the foundation needed to support the hyper-high levels of the S&P.

20 November 2025 – 08:38 Central Euro Time

The Euro is at present below its Neutral Zone for today, whilst above same is the Spoo; session volatility for the BEGOS Markets is moderate. Going ’round the Market Values’ horn for the five primary BEGOS components, we’ve (in real-time) the Bond as -1^08 points “low” vis-à-vis its smooth valuation line, the Euro as -0.009 points “low”, Gold as just -15 points “low”, Oil as only -0.37 points “low” and the Spoo as a scant -11 points low; however with respect to the latter, the “live” (futs-adj’d) P/E of the S&P 500 is 54.3x and the yield 1.171% vs. 3.772% annualized for the 3-month U.S. T-Bill. As to the Econ Baro, the BLS has announced there shan’t be a Payrolls report for October; however, that for September is to be released today, as is November’s Philly Fed Index, plus October’s Existing Home sales and Leading (i.e. “lagging”) Indicators.

19 November 2025 – 08:45 Central Euro Time

At present, Silver is the sole BEGOS Market outside (above) its Neutral Zone for today; session volatility is light. Looking at the Top Three Market Rhythms for pure swing constancy, we’ve (on a 10-test basis) Gold’s 12hr Moneyflow, Silver’s 30mn Price Oscillator and the Swiss Franc’s 1hr Price Oscillator; too, (on a 24-test basis) we’ve Gold’s 4hr Moneyflow, the Bond’s 15mn MACD, and the Swiss Franc’s 30mn Moneyflow. At Market Trends, the Spoo’s “Baby Blues” of linreg consistency are accelerating their drop, as also is the case for both Copper and Oil. The Econ Baro is sensitive to missing metrics finally coming to the fore, albeit rather sporadically; scheduled for today are October’s Housing Starts/Permits and August’s overdue Trade Deficit.

18 November 2025 – 08:50 Central Euro Time

Gold — as we’ve been anticipating — has provisionally flipped its 17-week parabolic Long trend to Short; confirmation arrives at Friday’s settle, (barring price first making a record high above 4398); currently price is 3997 and presently below its Neutral Zone for today, as too are Silver and the Spoo; above same is the Bond, and BEGOS Markets’ volatility is moderate. As noted yesterday, the Spoo’s linreg (see Market Trends) in real-time has rotated from positive to negative, suggestive of still lower S&P 500 levels; the Spoo’s best Market Rhythm for pure swing consistency through yesterday is the 1hr Moneyflow; mind too the separately-calculated MoneyFlow for the Index itself on our S&P page. Due today for the Econ Baro are November’s NAHB Housing Index, along with October’s Ex/Im Prices and IndProd/CapUtil, (for which there is as yet no September data).

17 November 2025 – 08:43 Central Euro Time

Silver and the Spoo are presently above today’s Neutral Zones, whilst below same is Oil; session volatility for the BEGOS Markets is moving toward moderate. The Gold Update points to Friday’s precious metals’ price slides as potentially leading to piercing Gold’s weekly parabolic Long trend as this week unfolds: the low thus far today is 4051 and the parabolic flip price for the week is 4004; Gold’s EDTR (see Market Ranges) is 103 points. At Market Trends, the Spoo’s “Baby Blues” of linreg consistency are (in real-time) down to their 0% axis as the trend rotates from positive toward negative, barring price getting a firm rally in these next few days. Due for the Econ Baro is the NY State Empire Index for November; 54 metrics remain missing from the government “shutdown” and — even having ended — its spillover effect of ongoing unreported data. And this is the final week of Q3 Earnings Season.

The Gold Update: No. 835 – (15 November 2025) – “Gold Flies, Silver Highs … Both Into End-of-Week Demise”

And per the above graphic, is the S&P 500 (“live” price/earnings ratio 54.4x) wisely waving the white flag? Our preference is instead the Gold flag as we go to the Stack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 4392 (20 October 2025)

2025’s High: 4392 (20 October 2025)

Gold’s All-Time Closing High: 4374 (20 October 2025)

10-Session directional range: up to 4248 (from 3938) = +310 points or +7.9%

Trading Resistance: Profile notables 4087 / 4119 / 4137 / 4206 / 4238

Gold Currently: 4084, (expected daily trading range [“EDTR”]: 103 points)

10-Session “volume-weighted” average price magnet: 4079

Trading Support: Profile notables 4052 / 4015 / 3994 / 3979 / 3961 / 3948

The Weekly Parabolic Price to flip Short: 4004

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3890

The 300-Day Moving Average: 3168 and rising

2025’s Low: 2625 (06 January)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

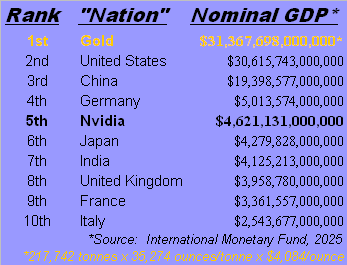

Let’s wind it up here with a brief revisit of Nvidia about which we mused in last 12 July’s missive. At today’s writing, NVDA again is at the top of the S&P pops, sporting a spritely market capitalization of $4.6T, which would make it the fourth-largest nation by nominal Gross Domestic Product in the world! However, (for those of you scoring at home), that compares to its present balance sheet net worth of “only” $100B.

Now: imagine you are buying in the States a new house, the median value for which in August was $413,500. Query: would you instead pay $19,108,377 for that house? Obviously no. Yet if NVDA today was that house, that’s how much you’d pay for it, (were you a wealthy, albeit daft, WestPalmBeacher down there).

“But, mmb, the price of NVDA is discounting its future earnings.”

Squire, a word to the wise is sufficient: the future is now.

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

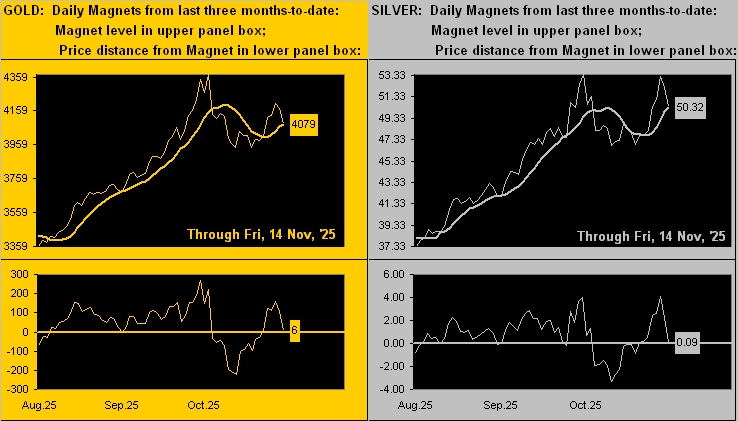

14 November 2025 – 08:45 Central Euro Time

The Spoo is presently below its Neutral Zone for today, whilst above same is Oil; cac volume for Oil is rolling from December into that for January; session volatility for the BEGOS Markets is moderate, with Oil exceptionally having already traced 128% of its EDTR (see Market Ranges). Yesterday, both the Bond and Spoo respectively fell below their most volume-dominant Market Profile support levels and crossed beneath their Market Magnets. Too yesterday, Silver traded to an all-time high at 54.42 and the Gold/Silver ratio looks to finish the week below 80x for the first weekly settle under that level since 12 July ’24: more on all that in tomorrow’s 835th consecutive Saturday Edition of The Gold Update. Due but not necessarily arriving today for the Econ Baro are October’s PPI, Retail sales, and September’s Business Inventories.

13 November 2025 – 08:36 Central Euro Time

Similar to this past Monday, Gold — and especially Silver — recorded very firm trading sessions yesterday: so robust was Silver (+4.2%) that the Gold/Silver ratio was driven down to 78.9x, the lowest reading in better than a year (since 22 Oct ’24). However in a 180° turnabout, Oil — after having seen both its Market Value and Market Magnet measures turn bullish on Tuesday — whirled ‘right back down below both indicators, the -4.2% drop ranking sixth-worst year-to-date. Presently, the Bond is below its Neutral Zone for today, whilst above same are Gold, Silver, Copper and the Spoo; BEGOS Markets’ volatility is pushing toward moderate. StateSide, the government “shutdown” has concluded with 45 metrics missing for the Econ Baro, to the extent they eventually are updated; due as well for today are October’s CPI, Treasury Budget and the prior week’s Initial Jobless Claims, should bureaus be up and running in time to report these items.

12 November 2025 – 08:34 Central Euro Time

Copper and the Spoo are at present above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility is thus far is mostly light. Looking at Market Rhythms for pure swing consistency, our Top Three on a 10-test basis are the non-BEGOS Yen’s 4hr MACD, the Swiss Franc’s 15mn Moneyflow and Silver’s 6hr Price Oscillator; on a 24-test basis the leaders are Gold’s 4hr Moneyflow, The Euro’s 30mn Moneyflow and Oil’s 4hr Parabolics. Oil yesterday confirmed moves above its smooth valuation line (see Market Values) and Market Magnet; by Market Profiles, Oil’s notable volume-dominant supports are 60.60 and 60.10, however there is resistance at 61.00. ‘Tis again a day without scheduled metrics due for the Econ Baro, (irrespective of the StateSide government “shutdown” which may be finally resolved fairly quickly).

11 November 2025 – 08:43 Central Euro Time

Presently, all eight BEGOS Markets are within their respective Neutral Zones for today, and session volatility is light. Yesterday’s firm up moves for the precious metals from their basing processes were sufficient to now find their “Baby Blues” of linreg consistency (see Market Trends) having turned higher in real-time, albeit the actual linreg trends remain negative; nonetheless, on a points basis, yesterday was Gold’s second-best net gain (+116) for the year-to-date and for Silver (+2.18) third-best; by percentage, the day ranked sixth-best for Gold (+2.9%), and again third-best for Silver (+4.5%); by their Market Profiles, Gold (currently 4136) finds its nearest notable volume-dominant support at 4087, whilst for Silver (currently 50.50) ’tis 49.90. Yesterday’s +1.5% gain for the S&P 500 was further supported by a 2.1% gain in its MoneyFlow as regressed into S&P points; however, the “live” (futs-adj’d) P/E is a treacherous 57.7x. Again, nothing for the Econ Baro is scheduled for today.

10 November 2025 – 08:44 Central Euro Time

Indications are the StateSide government “shutdown” may be resolved this week; that noted, no regularly scheduled metrics are due for the Econ Baro until Thursday; and since the start of the “shutdown” 45 metrics remain missing. For the BEGOS Markets at this instant, the Bond is below its Neutral Zone for today, whilst above same are the three elements of the Metals Triumvirate, Oil and the Spoo, and session volatility is moderate. Even as by Market Trends the “Baby Blues” of linreg consistency continue to fall for both Gold and Silver, The Gold Update points to the precious metals as having been basing, and both are well up today. There are two weeks still to run in Q3 Earnings Season, and although year-over-year improvement on balance is running at an above-average pace with a median bottom-line increase of +9.4%, earnings essentially need to double to get the P/E of the S&P 500 ( the “live” reading 56.3x) down to a far more realistic valuation.

The Gold Update: No. 834 – (08 November 2025) – “Gold (Yes Really) Records a Third Consecutive Down Week”

Irrespective of how “long” continues this parabolic Long trend, Gold’s “other” blue dots — indeed those “Baby Blues” that depict the consistency of trend — are in full plummet as next displayed at lower left for price’s daily bars from three months ago-to-date. And you regular readers well know the tune: ![]() “Follow the Blues instead of the news, else lose yer shoes”

“Follow the Blues instead of the news, else lose yer shoes”![]() –[mmb, circa 2000 A.D.] But as leerily leading are the Blues, price again is basing more than further falling, having already come well off the 4398 All-Time High. As well by the 10-day Market Profile at lower right, Gold looks nicely nested in that “fat” volume-dominant trading zone spanning as braced from 4022 down to 3990:

–[mmb, circa 2000 A.D.] But as leerily leading are the Blues, price again is basing more than further falling, having already come well off the 4398 All-Time High. As well by the 10-day Market Profile at lower right, Gold looks nicely nested in that “fat” volume-dominant trading zone spanning as braced from 4022 down to 3990:

As for Q3 Earnings Season (with still two weeks to run), year-over-year results have increased at an above-average pace: 71% of the 428 reporting S&P 500 constituents have improved their respective bottom lines from Q3 a year ago; typically ’tis only around 66%. That’s the Good News.

Now for the Bad News: the median earnings per share gain (encompassing 420 constituents with positive earnings from both a year ago and now) is +9.4%; such improvement instead ought be ’round +100% just to get the price/earnings ratio back down to some reasonable valuation and the yield (1.172%) more competitive with three-month U.S. annualized dough (3.757%). For as shown in the above graphic, such p/e is presently 55.9x, (the formula provided for proof). “AI” (“Assembled Inaccuracy”) begs to differ with 29.3x; but as we’ve stated before, if actually fed that formula, “AI” replies ’tis incapable of obtaining the answer.

Thus be it the “Look Ma! No Earnings!” crash or the “Look Ma! No Money!” crash, we — as do many others with whom we communicate — await the inevitable S&P “Dash for Cash!” crash. After all, given the S&P’s current market capitalization of $59.5T supported by a liquid money supply (“M2” basis) of “only” $22.4T, ’twill be a heckova train wreck … perhaps further derailed by Gold?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

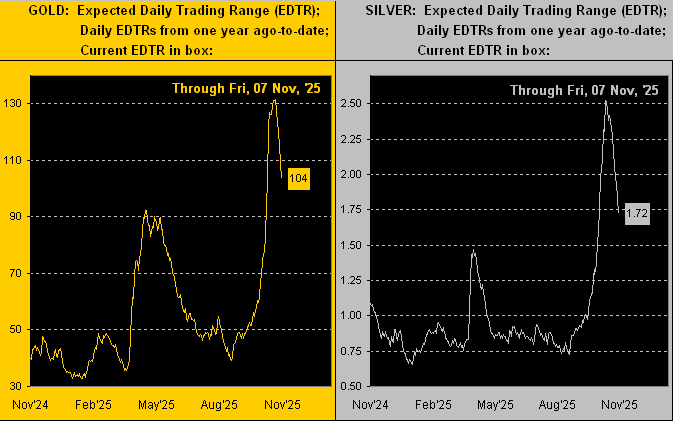

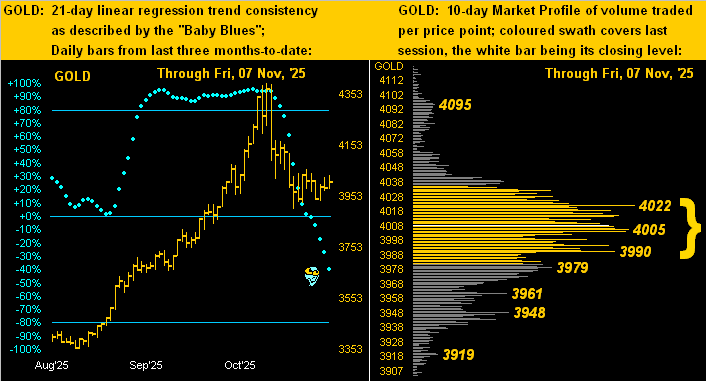

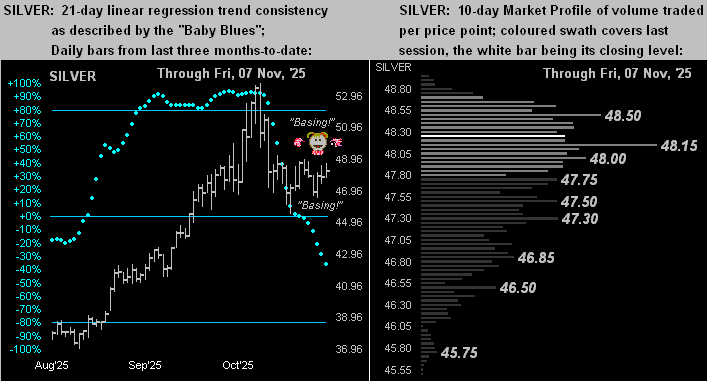

07 November 2025 – 08:53 Central Euro Time

At present we’ve the Bond, Euro and Swiss Franc below their respective Neutral Zones for today; above same are Gold, Silver and Oil, and session volatility for the BEGOS Markets is moving toward moderate. Gold, currently 4013, is net “unch” for this week: ’tis the line in the sand to avoid a third straight down week; more of ‘course, in tomorrow’s 834th consecutive Saturday edition of The Gold Update. At Market Trends, save for Copper and Oil, the “Baby Blues of linreg consistency are falling for the sixth other BEGOS components. For all eight markets, their best pure swing Market Rhythms are as follows: Bond 30mn Moneyflow, Euro and Swiss Franc their 4hr MACDs, Gold 4hr Price Oscillator, Silver 6hr Price Oscillator, Copper 2hr Parabolics, Oil 2hr Price Oscillator, and Spoo 15mn MACD. The StateSide government “shutdown” shall preclude today’s release of October Payrolls data; but awaiting the Econ Baro is the UofM Sentiment Survey for October, plus late in the session September’s Consumer Credit.

06 November 2025 – 08:34 Central Euro Time

The Euro plus the three element of the Metals Triumvirate are presently above today’s Neutral Zones; the balance of the BEGOS Markets are within same, and volatility is light. By Market Trends, linregs are positive for Copper, Oil and the Spoo, and negative for the Bond, Euro, Swiss Franc, Gold and Silver. That noted, yesterday Gold crossed back above its Market Value and Silver back above its Market Magnet; the yellow metal’s best Market Rhythm for pure swing consistency currently is the 4hr Price Oscillator, whilst for the white metal ’tis the 15mn Moneyflow. And the Bond yesterday moved below its most volume-dominant Market Profile support (117^14, price now 116^17). As the StateSide “shutdown” continues, the following metrics due today for the Econ Baro shall go missing: Q3’s Productivity and Unit Labor Costs, September’s Wholesale Inventories, and the prior week’s Initial Jobless Claims.

05 November 2025 – 08:39 Central Euro Time

Both Gold and Silver are at present above today’s Neutral Zones, whilst below same is the Spoo; session volatility for the BEGOS Markets is moderate. Whilst higher today, the precious metals’ “Baby Blues” of linreg consistency continue to cascade (see Market Trends). Notably by Market Values, Gold finally has fully reverted to its smooth valuation line after having been above it for 53 consecutive trading days (since 20 August); by its Market Profile, Gold’s most volume-dominant zone of overhead resistance spans from 3990-to-4039; similarly for Silver ’tis from 47.75-to-48.60. The Dollar Index at this instant is precisely 100.000 after basically having been below that level for the past three months. And the Econ Baro does receive two non-government metrics today: October’s ADP Employment and the ISM(Svc) Index, (the StateSide shutdown continuing following a 14th-failed Senate vote last evening).

04 November 2025 – 08:48 Central Euro Time

The Bond is currently above its Neutral Zone for today, whilst below same are Silver, Copper, Oil and the Spoo; BEGOS Markets’ volatility is firmly moderate. By Market Trends, Gold’s 21-day linreg has rotated to negative; with 3975 thus far today’s low, again, should 3901 be penetrated by week’s end, the weekly parabolic Long trend shall flip to Short. The Spoo today has closed its up gap from the opening back on 27 October; too, the daily MACD is approaching a negative crossover, and the daily Moneyflow study has dropped below the key mid-point level of 50. Today’s Econ Baro metrics that shan’t be received (give the StateSide “shutdown”) are September’s Trade Deficit and Factory Orders.

03 November 2025 – 08:32 Central Euro Time

‘Tis a fairly quiet start to November for the BEGOS Markets; presently the Bond is below today’s Neutral Zone, whilst above same is Oil; session volatility is light. The Gold Update confirms our expectations for price having had a second consecutive down week; however year-to-date, there’ve yet to be three negative weeks in-a-row; Gold’s “expect weekly trading range” (172 points) brings the weekly parabolic Long trend into jeopardy should 3901 (last week’s low) be tested as ’tis “within range”. Looking at Market Values for the five primary BEGOS components, in real-time we’ve the Bond as not quite a full point “low” below its smooth valuation line, the Euro -0.025 points “low”, Gold +89 points “high”, Oil -1.04 points “low” and the Spoo +126 points “high”. Given the ongoing StateSide “shutdown”, for the second consecutive month there shan’t be the otherwise due Construction Spending for September, making for a 35th missing Econ Baro metric; however October’s ISM(Mfg) shall be reported.

The Gold Update: No. 833 – (01 November 2025) – “Gold Furthers Fall as Called”

To wrap this week, regular readers of The Gold Update know we (as just done) “rib” those “WestPalmBeachers down there”, the claim-to-fame of south Florida’s brightest bulbs being “Hanging Chad” back in 2000 during “W vs. Algore”.

Technically, Florida is one of 50 states comprising the federal union of the U.S. Fundamentally however, Florida is more of a foreign country unto itself. Its pencil-thin panhandle barely clings to the southernmost coastline of Alabama and Georgia. The distance from Miami to Havana, Cuba is just 70% the distance to Jacksonville. And ’tis written the State’s average elevation is 100 feet (30m). Florida is FLAT, man. (In ’64, we visited an auntie there, and given the lack of depth perception, once was enough).

But to the point (hat-tip A.C.): assuming ratification by the state’s legislature, eight months from this day on 01 July 2026, Florida shall officially acknowledge both Gold and Silver as legal tender in coin form, and without sales tax on purchases thereof. To quote Grace Slick with The Jefferson Airplane at Woodstock back in ’69: “It’s the new dawn!”

So for Florida, with Gold and Silver, let fiat be gone!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

31 October 2025 – 08:47 Central Euro Time

All eight BEGOS Markets are currently within their respective Neutral Zones for today; session volatility is light. It remains the case amongst the five primary BEGOS components that’ve we’ve no notable correlations therein. Tomorrow’s 833rd consecutive Saturday edition of The Gold Update shall cite price’s return back down into the 3000s (as anticipated), albeit ’tis presently 4031 and By Market Values still +110 points “high” above the smooth valuation line; similarly, the Spoo is +156 points above same. Silver had a firm day yesterday in climbing back up through 47.75-48.15 resistance zone (see Market Profiles). We await October’s Chi PMI for the Econ Baro; however, today’s missing reports due to the StateSide “shutdown” are Q3’s Employment Cost Index plus September’s Personal Income/Spending and “Fed-favoured” Core PCE Index.

30 October 2025 – 08:45 Central Euro Time

Presently, Gold is above its Neutral Zone for today, whilst below same is Oil; BEGOS Market’s volatility is firmly moderate. Unsurprisingly, the FOMC with little data upon which to decide nonetheless reduced the FedFunds interest rate 25bps to a 3.75%-4.00% target range. Despite yesterday’s “unch” session, the S&P 500 is (yet again) extremely “textbook overbought”, buoyed almost solely by NVDA and to an extent AAPL; breadth yesterday was poor (25%/75%); the Spoo by Market Values shows (in real-time) as +180 points “high” above its smooth valuation line. For the Econ Baro today, given the ongoing StateSide government “shutdown”, the Bureau of Economic Analysis shan’t be furnishing the first peek at Q3 GDP, nor the Bureau of Labor Statistics the prior week’s Initial Jobless Claims. Q3 Earnings Season has reached the midway mark: for the S&P 500, 72% have bettered their bottom lines from a year ago, an above-average pace; of course, the overall level of S&P earnings remains far too low to maintain the current Index levels, especially with a risk-full yield of just 1.126% vs. a risk-less 3.730% on a 3mo. T-Bill.

29 October 2025 – 08:42 Central Euro Time

Both EuroCurrencies are at present below today’s Neutral Zones, as is Oil, whilst above same are the Metals Triumvirate and Spoo, session volatility for the BEGOS Markets is moderate. Gold yesterday traded down to as low as 3901, which as posted on “X” (@deMeadvillePro) was down through the first of three potential “fib” levels, followed then by 3857 and 3729; both precious metals today, however, are higher, even as their “Baby Blues” (see Market Trends) continue to drop. Our best Market Rhythms for pure swing consistency are currently (on a 10-test basis) Silver’s 30mn Moneyflow, Oil’s 4hr MACD and Gold’s 30mn Parabolics, plus (on a 24-test basis) the non-BEGOS Yen’s 2hr Moneyflow, Silver’s 15mn Moneyflow, and Gold’s 60mn Parabolics. For the Econ Baro we await September’s Pending Home Sales. And late in the session comes the FOMC’s Policy Statement for a -0.25% FedFunds interest rate cut.

28 October 2025 – 08:41 Central Euro Time

All three elements of the Metals Triumvirate, plus Oil, are at present below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility is mostly moderate. As anticipated in The Gold Update, Gold and Silver continue to correct, the “Baby Blues” of linreg consistency (see Market Trends) furthering their falls in real-time; indeed we may see Silver’s trend having rotated from positive to negative by tomorrow or Thursday; mind as well the widened Market Ranges for both precious metals (Gold’s EDTR for today is 129 points whilst that for Silver is 2.42 points). The P/E of the S&P 500 has further skyrocketed to in excess of 60x due in large part to INTC’s “ttm” earnings now but $0.01: the P/E of INTC is now 2,822.5x (see S&P 500, Valuations and Rankings). Despite the StateSide “shutdown”, the Econ Baro will take in some actually data today: October’s Consumer Confidence.

27 October 2025 – 08:42 Central Euro Time

(Note: Europe is now on winter hours). The week gets underway presently finding the Bond, Swiss Franc and Gold below today’s Neutral Zones, whilst above same are Copper and the Spoo; BEGOS Markets’ volatility is moving toward moderate. The Gold Update sees further near-term downside for price as the “Baby Blues” of linreg consistency (see Market Trends) accelerate lower; indeed Gold today has moved below a shelf of support (see Market Profiles) spanning from 4132-4123, (price now 4083); and in real-time Gold is +250 points above its smooth valuation line (see Market Values). Were the S&P 500 to open at this instant (+0.9%), its P/E would be 50.9x. The week’s highlight comes Wednesday via the Policy Statement from the FOMC. And due today (but unlikely to be reported given the “shutdown”) are Durable Orders for September.

The Gold Update: No. 832 – (25 October 2025) – “Gold Meme’d Gets Bean’d!”

Meanwhile, the Economic Barometer remains unfulfilled: 39 metrics are to have been received since the start of the StateSide government “shutdown” effective 01 October. But with 26 thus far missing, just 13 have been received — including a surprise on Friday: September’s Consumer Price Index was issued; (more on that in the wrap). Otherwise, amongst all 13 of the incoming metrics, just five improved period-over-period. Lookin’ a bit rickety, our Baro, as we ever-anticipate for stocks ![]() “Stormy Weather”

“Stormy Weather”![]() –[Arlen/Koehler, ’33]. And yes, Virginia, if you actually perform the math (a science apparently unemployed by the modern-day money manager), the price/earnings ratio of the S&P 500 settled yesterday at 50.5x, (which for you WestPalmBeachers down there means portfolio theory is a thing of the past):

–[Arlen/Koehler, ’33]. And yes, Virginia, if you actually perform the math (a science apparently unemployed by the modern-day money manager), the price/earnings ratio of the S&P 500 settled yesterday at 50.5x, (which for you WestPalmBeachers down there means portfolio theory is a thing of the past):

So as teased, we wrap with yesterday’s surprise release of the CPI, (both the headline and core readings a bit hot for the Fed’s liking). But our immediate response was: “Did the ‘shutdown’ just end?” Quickly we checked … but … no. Yet, after all, the CPI like so many Econ Baro metrics is released by a federal government agency, in this case the Bureau of Labor Statistics, which did not first report the scheduled Producer Price Index.

But then we found out what happened with respect to the CPI: in order for the Social Security Administration (which is not fully “shutdown”) to keep benefit check payouts in pace with inflation, “They gotta have that CPI, baby!” We thus give a tip of the cap to whoever he/she/it was that snuck into the otherwise shuttered BLS — perhaps heroically in the wee hours on personal time — to gather, crunch, arrange and release the data. ‘Tis most appreciated and deserving of a year-end bonus.

As to a potentially negative near-term course for Gold, appreciate what ’tis, indeed add to your load!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

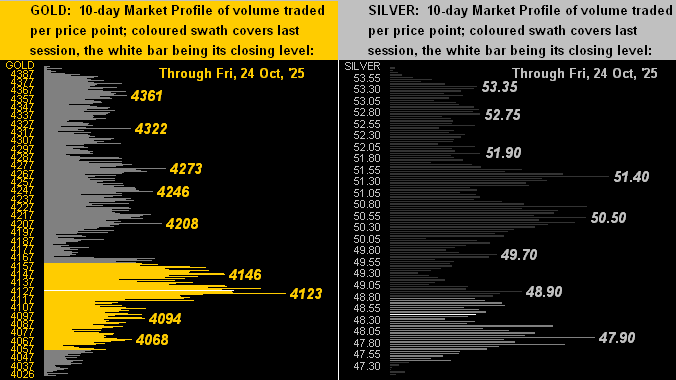

24 October 2025 – 08:24 Central Euro Time

The Euro, Swiss Franc, Gold and Silver are all below today’s Neutral Zones; above same are Copper and the Spoo, and session volatility for the BEGOS Markets is light. Gold’s “Baby Blues”(see Market Trends) of linreg consistency have provisionally dropped below their key +80% axis such as (upon day’s-end confirmation) to then expect lower prices near-term; vis-à-vis its smooth valuation line (see Market Values), Gold in real-time shows as +289 points “high”; more on the yellow metal in tomorrow’s 832nd consecutive Saturday edition of The Gold Update. Oil’s “Baby Blues” yesterday confirmed crossing above their -80% axis: given price in real-time is about -2 points below its own valuation line, near-term we’d expect Oil to visit the mid-63s from the current mid-61s. Due (but likely not arriving) today for the Econ Baro are September’s CPI (<– update, yes CPI reported) and New Home Sales; however, the non-governmental UofM Sentiment Survey for October ought make the trip.

23 October 2025 – 08:49 Central Euro Time

The Bond, Euro and Swiss Franc are at present below their respective Neutral Zones for today, whilst above same is Oil; session volatility for the BEGOS Markets is moving toward moderate. At Market Trends, Gold’s “Baby Blues” of linreg consistency are dropping, but have yet to move below their key +80% (as did Silver’s so confirm yesterday); thus far today, both precious metals are stabilizing to this point; however by Market Values, Gold in real-time is +335 points above its smooth valuation line; further of note today for Gold, it has been trading either side of its most volume-dominant price of the past fortnight which by the Market Profile is 4123. Given the scattered nature of late amongst the five primary BEGOS components, we find no reasonable correlation — neither positive nor negative — therein. The Econ Baro awaits September’s Existing Home Sales; but with yet another Senate vote such that the StateSide government remains closed, this shall be the fourth consecutive week of missing Initial Jobless Claims.