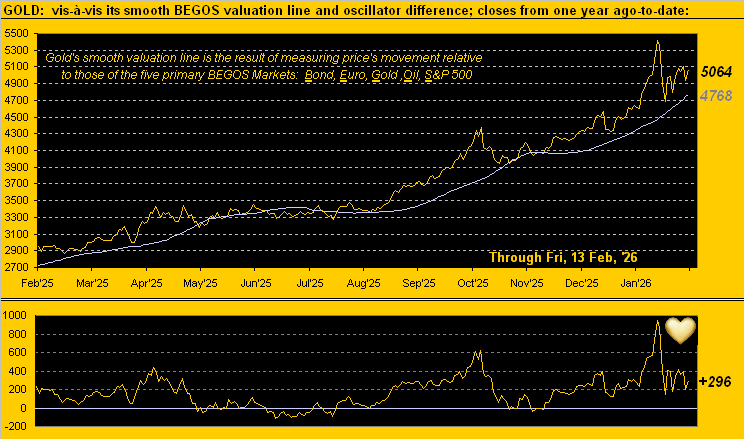

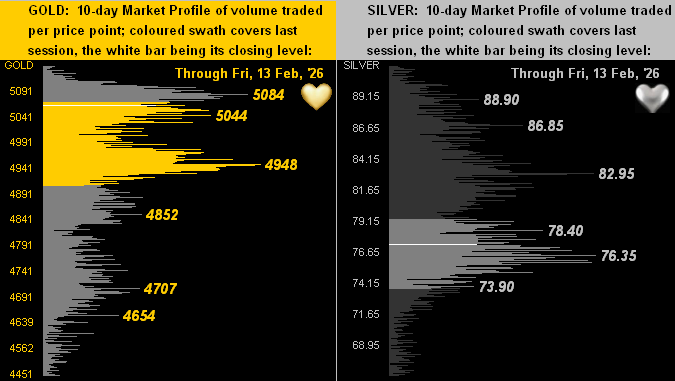

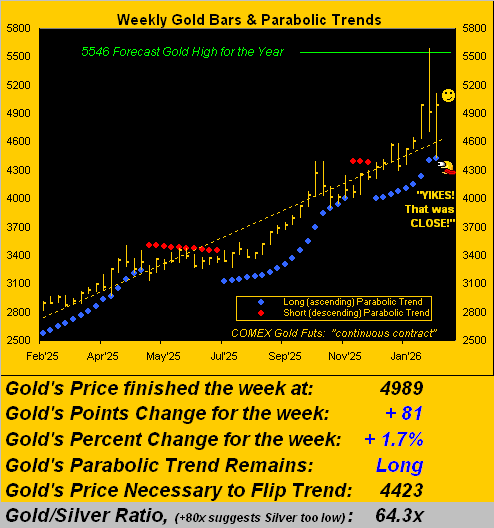

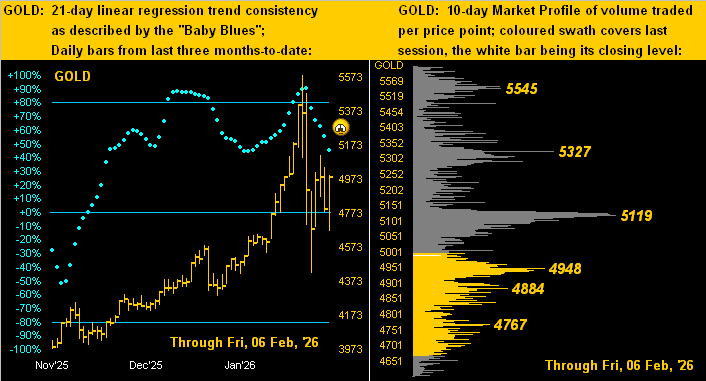

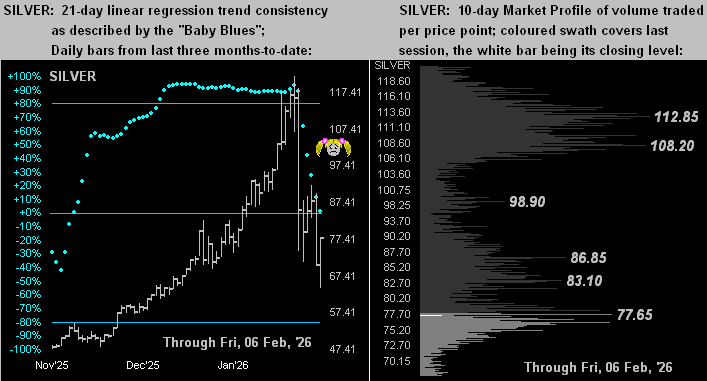

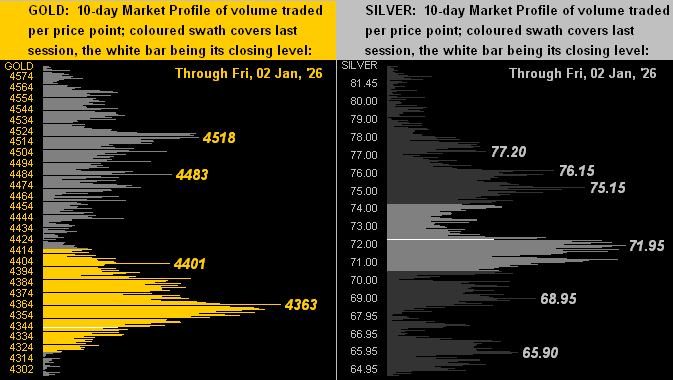

The BEGOS Markets’ two-day session continues with volatility naturally having widened from light at this time yesterday to now moderate. Above the session’s Neutral Zones are the Bond and Oil, whilst below same are the two EuroCurrencies, the three elements of the Metals Triumvirate, and the Spoo. Gold high-to-low through the combined session has declined by as much as -199 points; by Market Values, Gold (in real-time) is +131 points above its smooth valuation line after having been +418 points a week ago; too by its Market Profile, Gold has slipped below its most volume-dominant support level of 4948; ’tis the like case for Silver having eclipsed down through 76.35. Oil’s cac volume is rolling from March into that for April. The week’s parade of 18 scheduled Econ Baro metrics begins today with February’s NY State Empire and NAHB Housing Indices.

Mark

Mark

16 February 2026 – 08:42 Central Euro Time

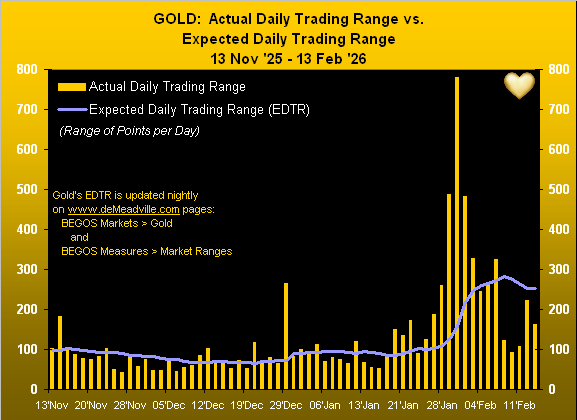

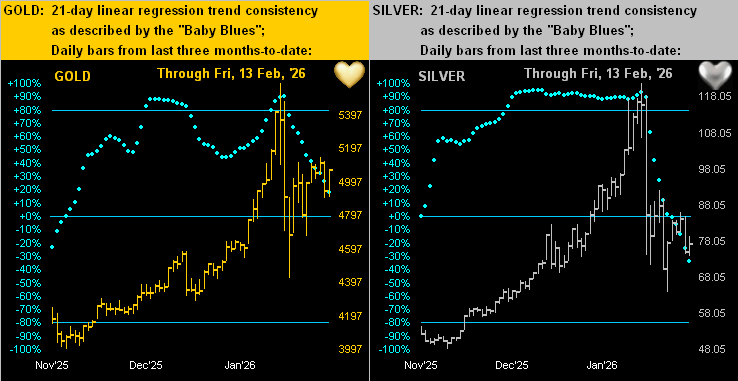

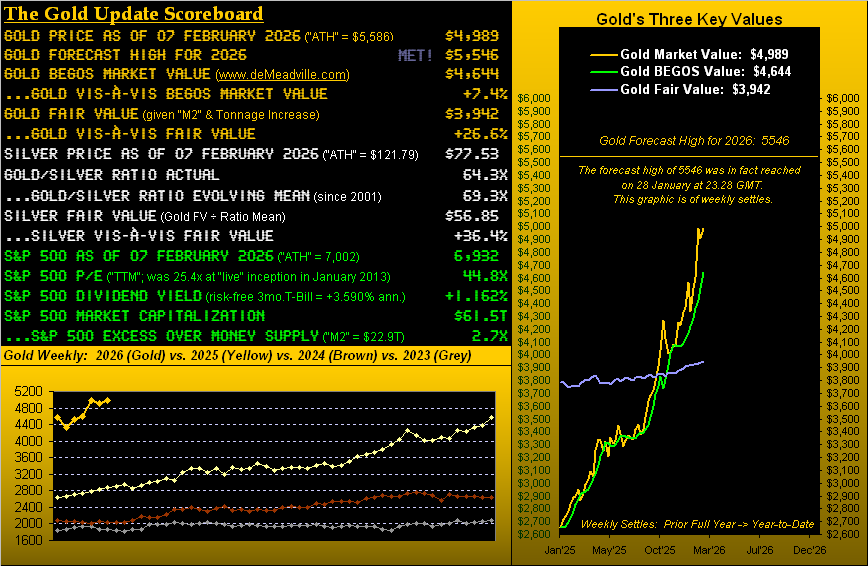

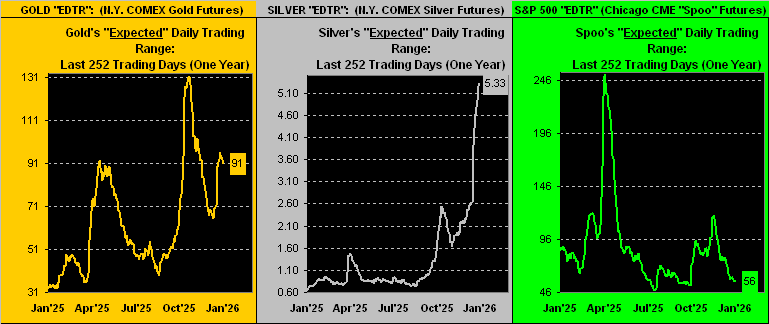

Given the StateSide holiday, ’tis a two-day session for the BEGOS Markets with settlement tomorrow (Tuesday). Presently, we’ve but one BEGOS component outside (below) its Neutral Zone for the session, that being Gold -0.9% (5017); overall volatility thus far expectedly is quite light. The Gold Update cites (as we’d anticipated a week prior) a compressing of the yellow metal’s trading range; Gold’s EDTR (see Market Ranges) for today is 248 points, but doubtless the actual range shan’t be that vast, (barring something geo-politically untoward); too, given the ongoing drop by Gold’s “Baby Blues” (see Market Trends), the 21-day regression trend may confirm having rotated to negative by week’s end. Nothing is due today for the Econ Baro with a heavy balance of 18 metrics scheduled through the week. And with two weeks to run in Q4 Earnings Season, we still expect reports from some 100 S&P 500 constituents: thus far, 71% have bettered their like Q4 of a year ago, which continues to be an above-average pace; however, the “live” P/E (futs-adj’d) at present 46.2x is a significant downside warning sign.

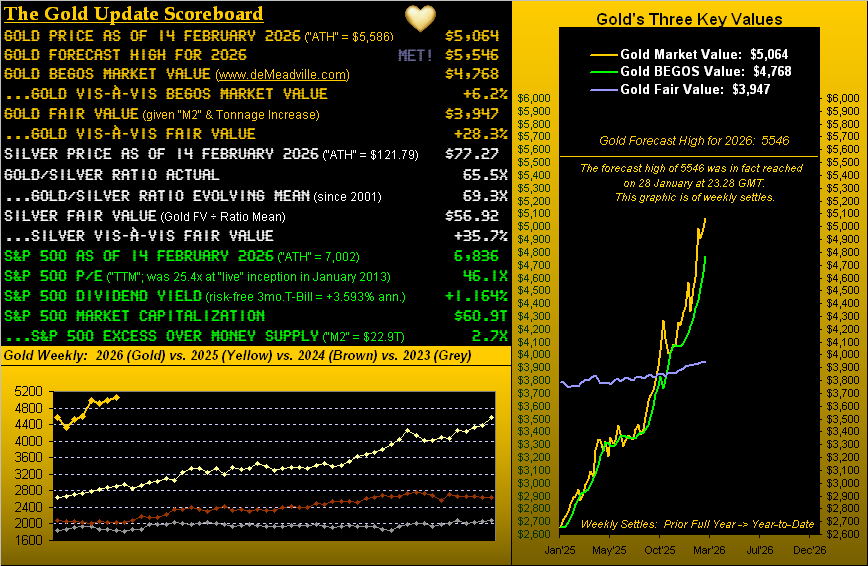

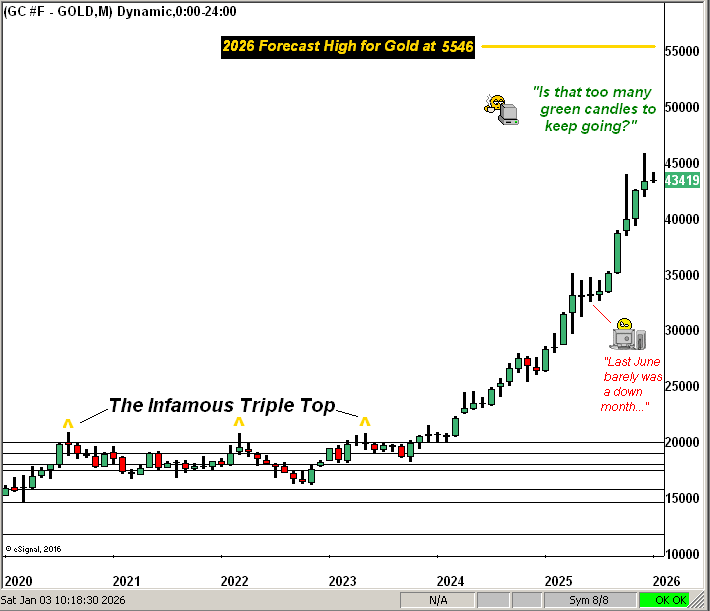

The Gold Update: No. 848 – (14 February 2026) – “Gold’s Range Compresses as the Uptrend Regresses”

And so, to the stack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 5586 (29 January 2026)

2026’s High: 5586 (29 January)

Gold’s All-Time Closing High: 5411 (28 January 2026)

10-Session directional range: up to 5140 (from 4428) = +712 points or +16.1%

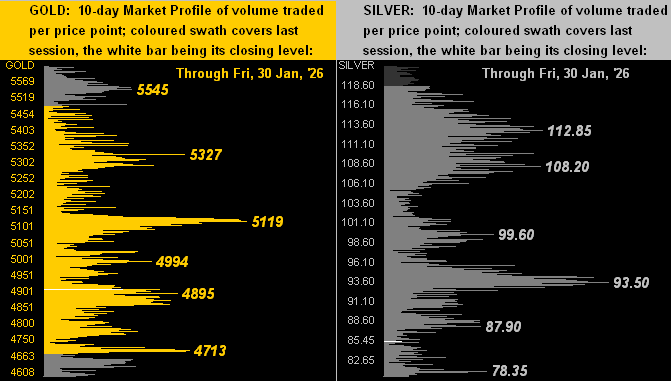

Trading Resistance: notable by the Market Profile, 5084

Gold Currently: 5064, (expected daily trading range [“EDTR”]: 248 points)

Trading Support: notable by the Market Profile, 5044 / 4948 / 4852 / 4707 / 4654

10-Session “volume-weighted” average price magnet: 4921

The Weekly Parabolic Price to flip Short: 4563

2026’s Low: 4319 (02 January)

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3947

The 300-Day Moving Average: 3549 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

To close, a most highly-valued reader of The Gold Update just enlightened us as to equity margins being on the up move. Without our doing the actual math, margin debt today purportedly exceeds the $1T level, last year alone having increased some 36%.

“Wow, mmb, that’s more than double what the S&P did last year…”

‘Tis so, Squire, the S&P 500’s net gain in 2025 being +16.4%. Is it any wonder that (again per the opening Scoreboard) today’s S&P market capitalization of $60.9T is 2.7x the liquid money supply? Sell your stock and get cash from your broker? Or just an I.O.U.?

But wait, there’s more: how are how those precious metals’ margin requirements working out for ya? Three years ago on Valentine’s Day in 2023, the price of Gold was 1864 and the COMEX margin required to trade one futures contract was $7,000. Today at 5064, Gold is +172% higher than ’twas then … but the margin today at $46,000 is an increase of +557%! And as for Silver (deep breath): she settled Valentine’s Day 2023 at 21.85 with required contract margin of $8,000. Now Silver at 77.27 is +254% higher … but her requisite margin per contract at $76,000 is a +850% increase! Nuthin’ like a li’l volatility to keep one on one’s liquidity toes, eh?

Still, we close with this happy news. For even as price compression may weigh, with trend regression in play, everyday with Gold is Valentine’s Day!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

13 February 2026 – 08:34 Central Euro Time

Presently we’ve the EuroCurrencies below their respective Neutral Zones for today, whilst above same are the precious metals; BEGOS Markets’ volatility remains light into this hour of the session. Gold, after having on Wednesday moved up through its Market Magnet, was unable to sustain upside furtherance, falling back down through same yesterday, as did both Oil and the Spoo; and all three elements of the Metals Triumvirate yesterday failed to hold their most volume-dominant support levels (see Market Profiles). Also, EDTRs (see Market Ranges) — whilst still vast — have begun to narrow a bit; more on the metals in tomorrow’s 848th consecutive Saturday edition of The Gold Update. And although we’re still a week away from the “Fed-favoured” PCE for December, today the Econ Baro receives the CPI for January. As for Q4 Earnings Season, with two weeks yet to run, some 100 S&P 500 constituents are still to report. Monday is a StateSide holiday for physical bourses.

12 February 2026 – 08:41 Central Euro Time

At this moment, all eight BEGOS Markets are within their respective Neutral Zones for today, and session volatility to this point continues to be light. Gold yesterday settled above its Market Magnet, suggestive of some upside follow-through near-term term, even as per The Gold Update price remains significantly overvalued; ’tis just mildly lower so far today. As to the Spoo, it crossed yesterday below its most volume-dominant Market Profile support level of 6968, even as price this morning is mildly higher. At Market Trends, the “Baby Blues” of trend consistency are falling for the Euro, Swiss Franc, Gold and Silver: “Follow the Blues instead of the news, else lose yer shoes.” And the Econ Baro awaits January’s Existing Home Sales along with the usual Initial Jobless Claims from the prior week.

11 February 2026 – 08:42 Central Euro Time

The Euro, Swiss Franc, Silver and Copper are all at present above today’s Neutral Zones; the rest of the BEGOS Markets are within same, and session volatility again is light. For the precious metals by Market Trends, the “Baby Blues” of trend consistency continue to fall for both Silver and Gold; but the trends currently are directionally opposed, that for the white metal being negative, yet still positive for Gold, (basis 21-day linear regression); volume-dominant Market Profile support for Silver is 77.65 whilst for Gold ’tis 4948. The ongoing above-average Q4 Earnings Season for the S&P 500 has served to bring its “live” (ttm) P/E down from the 50s into the 40s, (still a far cry above Jerome Cohen’s 11x-15x for a bull market); too, the S&P remains practically yieldless at 1.143% vs. the essentially riskless 3mo T-Bill’s annualized 3.590%, i.e. more than triple the return of the all-to-risk S&P. The Econ Baro looks to slightly-delayed January data for Payrolls, plus that month’s Treasury Budget.

10 February 2026 – 08:40 Central Euro Time

At present we’ve the Bond above its Neutral Zone for today, whilst below same are both Silver and Copper; session volatility for the BEGOS Markets is light with a bevy of incoming EconData due through the balance of the week. With respect to both the noted white and red metals, their respective Market Trends are rotating to negative as too already have done those for the Bond and Spoo; the uptrenders thus remain the two EuroCurrencies, Oil and Gold, the latter’s “Baby Blues” of trend consistency continuing to fall as the uptrend weakens. Gold’s major Market Profile volume-dominant prices are: 5327, 5098 and 4948. Too for the Spoo, its most dominant is 6968. “Scheduled” metrics today for the Econ Baro are December’s Retail Sales and Ex/Im Prices, Q4’s Employment Cost Index, and in “shutdown” arrears, November’s Business Inventories.

09 February 2026 – 08:44 Central Euro Time

The week starts finding at present both the Bond and Oil below today’s Neutral Zones, whilst above same are the Euro, Swiss Franc and Silver; BEGOS Markets’ volatility is light-to-moderate. The Gold Update focuses on the yellow metal having reached what historically (save for the FinCrisis) by percentage is peak volatility; too, both Gold and Silver remain well-overvalued vis-à-vis their respective Fair Value. Going ’round the horn in real-time for the Market Values of the five primary BEGOS components: we’ve the Bond -3^06 points “low” per its smooth valuation line, the Euro -0.018 points “low”, Gold +365 points “high”, Oil +2.68 points “high”, and the Spoo -170 points “low” even as the “live” P/E of the S&P (futs-adj’d) remains what we deem as dangerously stretched at 45.8x. Three voluminous weeks of Q4 Earnings Season remains, wherein thus far, year-over-year improvement is above average; but again, prices on balance are very strained to the upside (see S&P 500 > Valuations and Rankings). And ’tis a busy week for the Econ Baro: although nothing is due today, the balance of the following four days seeks 16 incoming metrics.

The Gold Update: No. 847 – (07 February 2026) – “Gold Reaching Peak Volatility”

Gold by its daily trading range (intraday low to intraday high, or vice-versa) is establishing point swings ![]() “like ya never done seen”

“like ya never done seen”![]() –[mmb, ’18]. Gold’s daily range through these first 25 trading days of 2026 has averaged 197 points per session, the current “expected daily trading range” (for Monday) being 283 points, an historical maximum. That is wider than Gold’s entire trading range from the start of the 21st century on 02 January 2001 (opening price 273) for nearly five years until 12 December 2005 (settle price 532).

–[mmb, ’18]. Gold’s daily range through these first 25 trading days of 2026 has averaged 197 points per session, the current “expected daily trading range” (for Monday) being 283 points, an historical maximum. That is wider than Gold’s entire trading range from the start of the 21st century on 02 January 2001 (opening price 273) for nearly five years until 12 December 2005 (settle price 532).

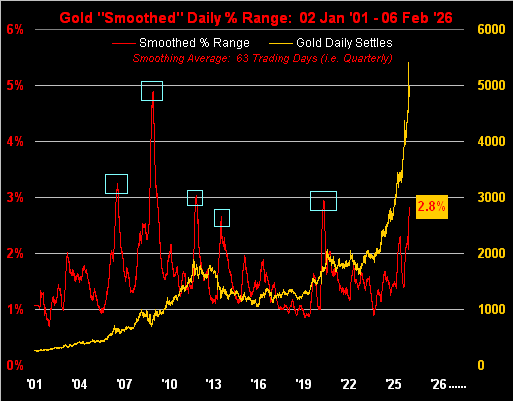

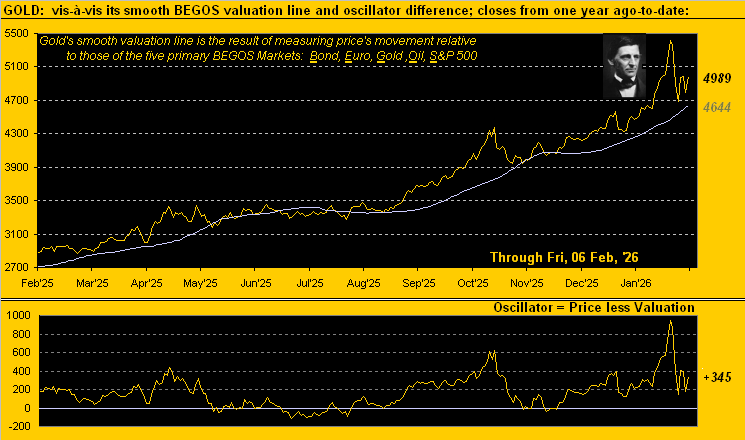

However: in turning to the reality of percentage swings, Gold’s actually been here before, having yet again arrived at what (at least historically) has been ’round peak volatility. Year-to-date, Gold’s average daily percentage range is 4.2%, including one day of 10.9% and another of 16.6%; (the year’s daily median thus far is 2.6%). All that said, towards subjectively selecting what is peak volatility, we’ve the following graphic spanning Gold’s 6,314 trading days thus far this century. In order to smooth out the daily percentage gyrations of price distance traveled, the red line is a 63-day (one quarter) moving average of range. Note the boxes at the extremes of range (save for the FinCrisis) having peaked just either side of 3%, the current value as of yesterday (Friday) per the label at 2.8%, even as the week’s final session sported an intraday gain of +7.0%, with price (the Gold line) settling at 4989:

So from six Econ Baro metrics last week, we have 16 scheduled through next week. To be sure, ever since the past autumn’s U.S. government “macro-shutdown”, the stream of incoming data has been nothing short of screwy-louie (technical term). For example, as regards inflation: next Friday brings (per the Bureau of Labor Statistics) January’s Consumer Price Index … but ’tis not ’til the Friday thereafter we receive (per the Bureau of Economic Analysis) December’s Personal Consumption Expenditures. Are we therefore going backward? Ought we commandeer H. G. Well’s time machine –[Taylor, Mimieux, MGM, ’60]?

Indeed we thus could go forward to assess the state of Gold’s volatility (among other things). But that would take out all the fun. Besides, we’ve oft quoted the late, great Richard Russell: “There’s never a bad time to buy Gold.” Yet, ’tis also been said the day to sell your Gold is the day everybody wants it. As overvalued as both Gold and Silver presently are, that “day” remains a long way into the future. So mind and preserve your precious metals!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

06 February 2026 – 08:39 Central Euro Time

Presently above today’s Neutral Zones are the Swiss Franc, Gold, Silver, Copper and Oil; the other three BEGOS Markets (Bond, Euro and Spoo) are within same, and volatility for the session is moderate. Per yesterday’s comment on the weakening S&P 500 MoneyFlow, such leading indicator has further declined relative to the change in the Index itself (see S&P 500 > MoneyFlow). Silver from its record high of 121.785 just a week ago has since fallen into today by as much as -47.5% in reverting toward Fair Value, whereas Gold from 5586 has reverted just -16.4%: more on valuation of the precious metals in tomorrow’s 847th consecutive Saturday edition of The Gold Update. Given the fall in the Spoo last evening post-RTH, it need rise some +33 points for the S&P not to open negatively come 14:30 GMT. The Econ Baro looks to UofM’s initial February Sentiment Survey; then late in the session to close out the week comes December’s Consumer Credit; (again as previously noted, January’s Payrolls data has been delayed until next Wednesday).

05 February 2026 – 08:34 Central Euro Time

As to which we herein alluded last Friday, the MoneyFlow of the S&P 500 continues to deteriorate: by all three of our period measures, the S&P “ought be” several hundred points lower than currently ’tis; as this is a directionally leading indicator, do mind the MoneyFlow page; too by Market Trends, that for the Spoo has rotated to negative. At present, we’ve Silver, Copper and Oil below their respective Neutral Zones for today; the other BEGOS Markets are within same, and session volatility is mostly moderate, duly noting therein that Silver has already traced 134% of its EDTR (see Market Ranges); 4hr Silver (as mentioned in last Saturday’s Gold Update) continues to be a timely Market Rhythm for the white metal, notably by both Parabolics and Price Oscillator. ‘Tis a fairly quiet day for the Econ Baro with just last week’s Initial Jobless Claims coming due. And the Payrolls data for January has been rescheduled from tomorrow until next Wednesday.

04 February 2026 – 08:30 Central Euro Time

Gold has regained (for now) the 5000 handle; price at present is above its Neutral Zone for today, as are both Silver and the Spoo; the rest of the BEGOS Markets are within same, and volatility to this point is again light-to-moderate in the context that — with the exception of the Bond — EDTRs have been expanding (see Market Ranges). Silver (89.17) is up into structural resistance (86.13 to 93.56): should she stall in this range, mind that by Market Trends, the “Baby Blues” of trend consistency are falling for both precious metals as their uptrends continue to weaken. Of note yesterday, Copper settled above both its most volume dominant resistance level (see Market Profiles) and too above its Market Magnet, whereas the Spoo settled beneath dominant support and the Magnet. For the Econ Baro today we’ve January’s ADP Employment data and the ISM(Svc) Index.

03 February 2026 – 08:38 Central Euro Time

The two EuroCurrencies and the Metals Triumvirate all are at present above today’s Neutral Zones; Oil is below same, and session volatility for the BEGOS Markets is light-to-moderate. Yesterday had the “Baby Blues” of regression trend consistency (see Market Trends) for both Gold and Silver settle beneath their respective +80% axes, meaning both metals’ trends remain up, but are weakening such that bounces as we’re seeing today don’t necessarily preclude still lower prices near-term. By Market Profiles, the most volume-dominant overhead resistor for Gold is 5119 and for Silver 93.50. And by its Market Value, Gold in real-time (4937) is +371 points “high” above its smooth valuation line. Nothing is due today for the Econ Baro. For Q4 Earnings Season, 160 S&P 500 constituents have thus far reported with 115 (72%) having improved their bottom lines from Q4 year ago, which is an above-average pace. However, the “live” (futs-adj’d) P/E remains extremely high at 47.9x with the yield a lowly 1.132%; that for the 3mo T-Bill annualized is 3.578%.

02 February 2026 – 08:42 Central Euro Time

Precious metals’ selling continues as Gold and Silver work lower toward being less overvalued; both are at present below today’s Neutral Zones as are Copper, Oil and the Spoo; the Bond is above same, and BEGOS Market’s volatility is robust, save for the EuroCurrencies. The Gold Update appears to have precisely called the year’s high at 5546 (price then only reaching a bit further to 5586), albeit we’ve tempered than by duly noting there still are 11 months in 2026’s balance; either way including today, Gold has fallen more than -1,000 points since last Thursday’s record high and Silver some -40%. The good news is Gold — which by its BEGOS Market Value was nearly +1,000 points — “high” has since cut that to now (in real-time) just +48 points “high”, although price is still more than +15% above Fair Value (3938). For the Econ Baro we’ve 10 metrics due this week, beginning today with January’s ISM(Mfg) Index.

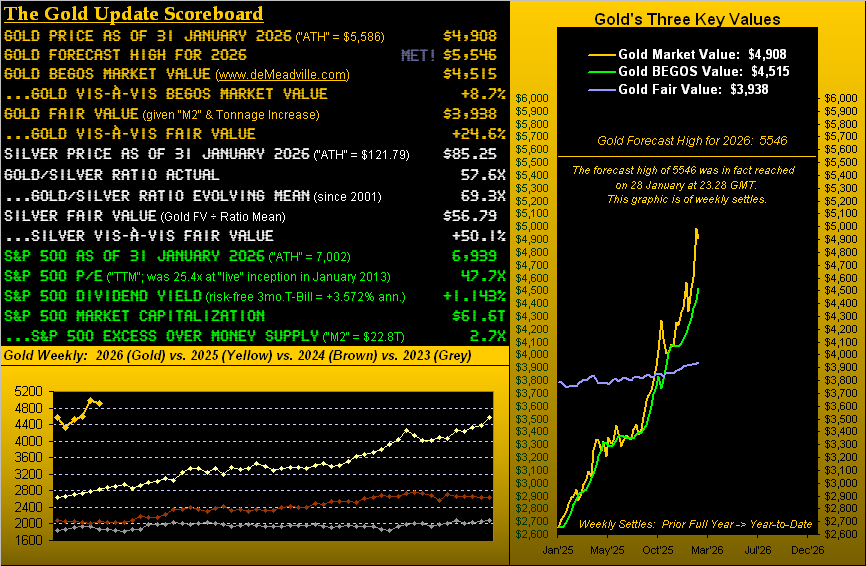

The Gold Update: No. 846 – (31 January 2026) – “Metals’ Mania Maxed!”

Note in the Baro the reference to inflation. Friday {finally} brought wholesale inflation data for December via the Producer Price Index. Both the “headline” and “core” readings came in at five-month highs, respectively annualized at +6.0% and +7.2%, (the 12-month summations being a less daunting +2.6% in each instance). And directly from the first paragraph of the FOMC’s Policy Statement: “Inflation remains somewhat elevated”, that release being two days prior to the PPI report. Fundamentally, that can be construed as a Gold-negative, should the Fed have to reverse rate gears and raise ’em. Either way, in muted response to the FOMC, the net change in the S&P from Wednesday through Friday was just a wee -0.6%. But by our indicatively leading MoneyFlow page, the change “ought have been” -3.1%. As folks later figure that out, a lower S&P near-term is likely. Too, the “live” price/earnings ratio of the S&P remains a “lofty” (kind understatement) 47.7x.

To close, we go to the “Now What? Dept.” Per our title, has the metals’ mania maxed? As stated, the selling into week’s-end was record-setting. Yet certainly so across the past five months had been the buying. And ’tis said that “What goes up must come down” … or at least not ridiculously stray from valuation. So as to near-term direction, mind near-term trends for protection. For the moment (as these always are evolving), our best pure swing Market Rhythm for Gold is its 30-minute MoneyFlow, and for Silver her four-hour Price Oscillator. (Do try not to get carried away).

And specific to geo-politically influenced metals’ mania, not only have we in other missives proven (in nauseatingly numerical detail) that such rallies are relatively short-lived with price returning down from whence it came (and then some), but also that regressing a Gold price to geo-politics is absurdly abstract. For at the end of the day, it simply comes down to how much dough (or lack thereof) is there to go ’round, and thus, how much need be printed to make everyone sound. Per the opening Scoreboard, that S&P 500 market capitalization-to-liquid money supply ratio of 2.7x is worrisome. Is your broker liquid?

Now as we prepare to publish, we are learning of disturbing geo-political events this weekend from Gaza to Iran. So should the metals be maxed or otherwise: aren’t you glad you hold Gold?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

30 January 2026 – 08:35 Central Euro Time

No further record highs for the metals today: notably Gold, after yesterday achieving our forecast high for this year of 5546 — moved higher still to 5627 — only to then succumbed a full -500 points within the balance of the session. Have the metals maxed? More of course in tomorrow’s 846th consecutive Saturday edition of The Gold Update. For the moment, all eight BEGOS Markets are below their respective Neutral Zones for today, (meaning the Dollar is getting the bid); session volatility is robust with solid losses across the metals’ board (at present Gold -3.8%, Silver -6.5% and Copper -4.4%). The “:”live” (futs-adj’d) P/E of the S&P is 45.3x; the monetary outflow yesterday was far worse than the essentially “unch” day for the Index (see our MoneyFlow page). And the Econ Baro wraps the week with January’s Chi PMI and December’s PPI.

29 January 2026 – 08:49 Central Euro Time

GOLD 5546 Achieved! With still these two trading days remaining in the new year’s first month, Gold this morning achieved our targeted forecast high for all of 2026, and then some, price reaching thus far up to 5627; Silver too has topped 120. Indeed at present, all three elements of the Metals Triumvirate are above today’s Neutral Zones, as are the two EuroCurrencies and Oil; the Bond is below same, and session volatility for the BEGOS Markets is moderate-to-robust, Copper alone having traced 250% of its EDTR (see Market Ranges) in hitting an all-time high of 6.385. As for Gold in real-time, at 5581 ’tis +1051 points above its smooth valuation line (see Market Values), a century-to-date record be it by points or percentage (+25%). Today’s Econ Baro metrics include in “shutdown” arrears November’s Trade Deficit, Wholesale Inventories and (purportedly) Factory Orders, plus Q3’s Revised Productivity and Unit Labor Costs.

28 January 2026 – 08:47 Central Euro Time

Gold’s cac volume is rolling from February into that for April with an additional +39 points of premium, and — with or without — a fresh All-Time High has been reached thus far today at 5318 (April) or 5279 (February). Presently for the BEGOS Markets we’ve the Bond, Gold, Silver and the Spoo above their respective Neutral Zones for today, whilst below same are the two EuroCurrencies; session volatility is moderate-to-robust, Gold having traced 115% of its EDTR. Gold by Market Values is +803 points above its smooth valuation line; and dominant Market Profile support for the yellow metal (basis April) is 5121. Of note the current 5312 price is -234 points (-4.2%) below our forecast high for this year of 5546. The Spoo is positioned such that the S&P 500 (were it to open at this instant) would trade above 7000 for the first time. And much ado shall be FinMedia-made about “The Dow” approaching the 50,000 milestone. Nothing is due today for the Econ Baro. And we look for no change in the FedFunds rate come the FOMC’s Policy Statement at 19:00 GMT.

27 January 2026 – 08:46 Central Euro Time

Silver’s late-in-the-session drop yesterday of -12% prompted us to query on “X” (@deMeadvillePro) as to if the high was in place. However this morning, Silver is back above its Neutral Zone for today as are Gold, Copper and the Spoo; Oil is below same, and BEGOS Markets’ volatility is moderate, save for Silver which already has traced 141% of its EDT (see Market Ranges). Silver’s high yesterday was 117.70 whereas present price is 112.44 (+8.3% on the session). For the S&P 500, earnings improvements have driven the P/E down to 47.3x — still a dangerously high ratio — but at least well off it having been above 64x in the prior week. Thus far in Q4 Earnings Season, 52 constituents have reported of which 38 (73%) have bettered their bottom lines from Q4 a year ago, which is an above average pace. For the Econ Baro today we’ve the January read of Consumer Confidence.

26 January 2026 – 08:41 Central Euro Time

Gold, having settled Friday at 4983, gapped higher to begin the week in opening at 5013 and since has traded to as high as 5108; Silver has reached 109.32. The Gold Update underscores the overvaluation fundamentally and technically for the precious metals, whilst nonetheless maintaining our Gold target for this year of 5546. Presently, the Bond, Euro, Swiss Franc, Gold and Silver all are above today’s Neutral Zones; within same are Copper, Oil and the Spoo; session volatility for the BEGOS Markets is moderate-to-robust. Going ’round the Market Values horn for the five primary BEGOS components in real-time: the Bond is -1^17 points below its smooth valuation line, the Euro -0.005 points below same, Gold +653 points above, Oil +2.83 points above, and the Spoo -71 points below valuation. In “shutdown” arrears for the Econ Baro we’ve November’s Durable Orders.

The Gold Update: No. 845 – (24 January 2026) – “Silver Taps 100 Whilst Gold Scrabbles for 5000”

Silver yesterday (Friday) at 15:10 GMT saw the current front month contract (March) achieve 100.00 for the very first time, en route to trading as high as 103.53 before settling the week at 103.26. Hearty congratulations to Sweet Sister Silver!

Gold however was unable to keep pace in the day’s milestone race, reaching “only” up to another All-Time High at 4991, rather than (as yet) eclipsing 5000 in closing at 4983.

Thus, on marches the metals’ mania mayhem with Gold year-to-date up now a net +15% and Silver +46%. (For you stock jocks, the S&P 500 thus far is +1%; have a great day).

Wonderful as ’tis in maintaining our 5546 forecast Gold high for 2026, we’ve this prudent cash management reminder from the “Metals Meltdown Dept.” … just in case you’re scoring at home:

- Back at Gold’s 06 September 2011 record high of 1923, price by December four years hence had “corrected” -46%;

- Back at Silver’s 25 April 2011 record high of 49.80, price by December four years hence had “corrected” -73%.

“But mmb, you’ve already said that’s not gonna happen again, right?”

No one “knows” with certainty Squire, however we very much doubt it. To be sure, we’re in the third massive metals “spike” since 1980, (recall then by 1982 Gold having succumbed -66% and Silver -88%). Means reversion does happen.

The big difference between (yes we have to reprise it) ![]() “Now and Then”

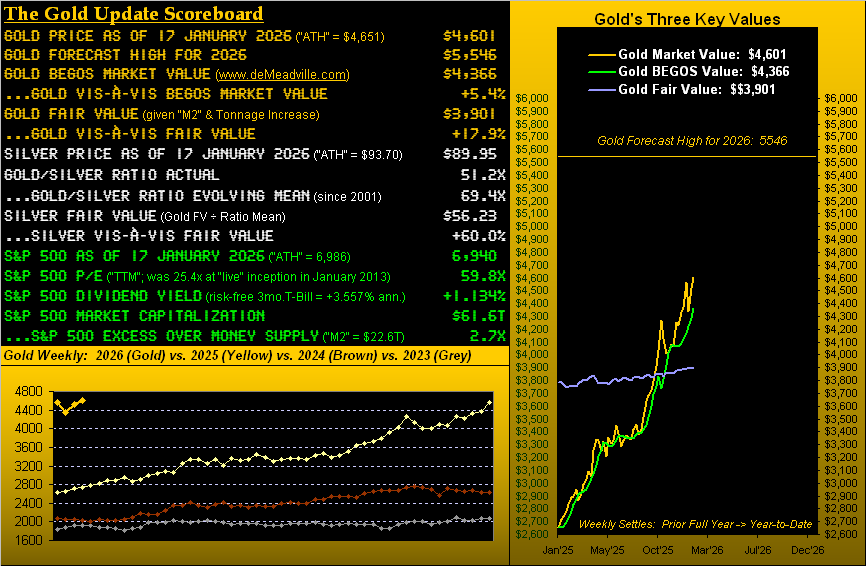

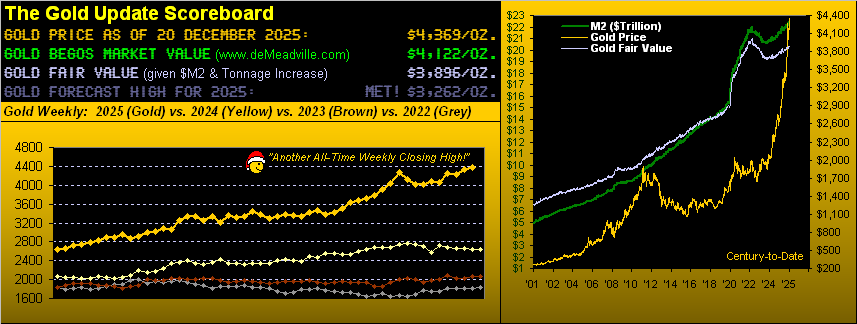

“Now and Then”![]() –[BeaTles, ’23] is back then the precious metals couldn’t get a seat in the theatre, let alone a back stage pass; now Gold and Silver are on centerstage aglow in all the lights. Too, as we described in last year’s final missive: the perception of Gold has morphed from a yield-less, irrelevant relic to meme-like stock proportions, and seriously is becoming more widely recognized as a foundational mitigant to debt-driven Dollar debasement and geopolitical jitters, overvaluation be damned. To wit per the above opening Gold Scoreboard:

–[BeaTles, ’23] is back then the precious metals couldn’t get a seat in the theatre, let alone a back stage pass; now Gold and Silver are on centerstage aglow in all the lights. Too, as we described in last year’s final missive: the perception of Gold has morphed from a yield-less, irrelevant relic to meme-like stock proportions, and seriously is becoming more widely recognized as a foundational mitigant to debt-driven Dollar debasement and geopolitical jitters, overvaluation be damned. To wit per the above opening Gold Scoreboard:

Gold at present is +12.7% above its BEGOS Market Value (4421 by price’s movement relative to those of the five primary BEGOS Markets being the Bond, Euro, Gold, Oil and S&P 500) and further ’tis +27.6% above Fair Value (3905 by price’s 45-year regression to the debasing Dollar via “M2”, countered by the increase in the supply of Gold).

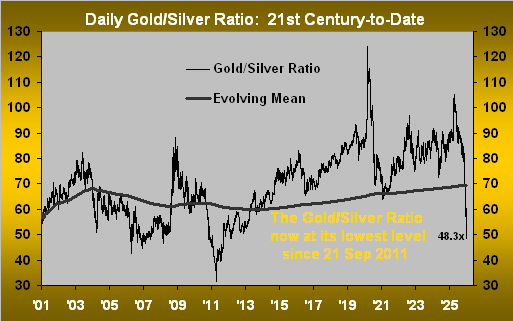

As for Silver, she is +83.4% above her Fair Value (56.30 given that for Gold divided by the evolving mean of the Gold/Silver ratio). And such ratio now at 48.3x is a 14-year low as shown below by the day across the past 25 years:

Note therein the reference to the “live” price/earnings ratio of the S&P 500 now at 59.1x. If you’ve forgotten the math, we’ve not forgotten it for you:

And yes, that p/e of 59.1x remains stratospherically excessive even as Q4 Earnings Season thus far has been very positive for the S&P: of the 46 constituents having reported, 74% have bettered their bottom lines from Q4 a year ago. But the overall high level of price — and thus practically no yield — inevitably is problematic given the yield in Treasuries remains more than triple that of S&P, and without risk of capital loss, (’tis assumed anyway…gulp…) But we get it: “Debt ain’t sexy.” So, cue Fleetwood Mac from ’76: ![]() “You can go your own way…”

“You can go your own way…”![]()

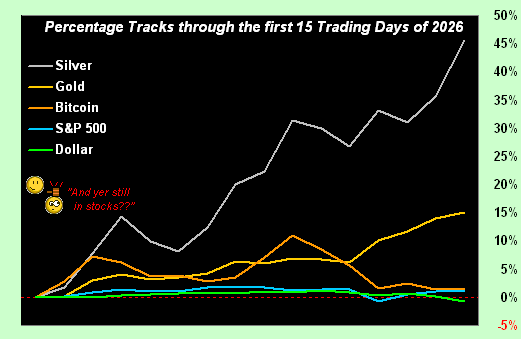

Into the new week, ’tis time for Gold 5000, (again barring “The Sell”). Gold has begun 2026 with a bang, indeed its best opening 15 trading days by percentage gain of any year so far this century, (which for you WestPalmBeachers down there is since 01 January 2001). And certainly the same (understatement) can be said for Silver, her having thus far gone nuclear! Regardless of what can be deemed as too far too quickly — especially with respect to overvaluation — we close with this graphic of the early year-to-date percentage tracks for each of Silver (+46%), Gold (+15%), Bitcoin (+1%), S&P 500 (+1%) and the Dollar Index (-1%):

‘Course with “only” 236 trading days remaining in 2026, what possibly could go wrong? For Gold and Silver the trend is Long!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

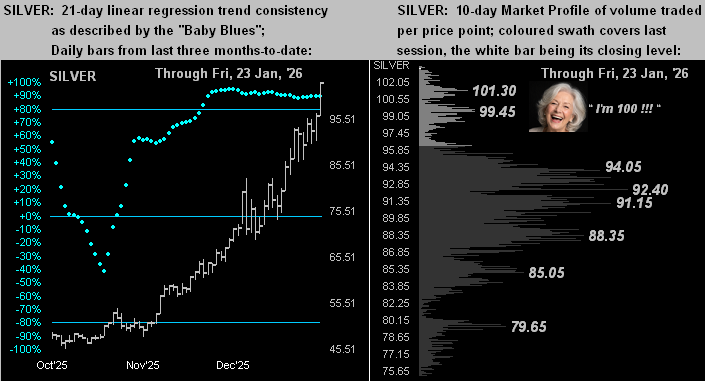

23 January 2026 – 08:45 Central Euro Time

Presently we’ve the Euro and Swiss Franc below their respective Neutral Zones for today, whilst above same are Gold, Silver and the Spoo; BEGOS Market’s volatility is again light-to-moderate. Milestones on tap: Gold 5000 (record high this morning 4970) and Silver 100 (record high this morning 99.40). The S&P 500’s “live” P/E (futs-adj’d) is 64.4x. Tomorrow’s 845th consecutive edition of The Gold Update (milestones made or not) shall nonetheless continue to celebrate the amazing run of the precious metals, albeit we’ll again caution valuation as having become quite upside extreme, (although certainly not as much as is the S&P). Too, we’ll make mention of December inflation as some metrics (CPI) in “shutdown” arrears have finally been reported. The Econ Baro concludes the week with the revised look at the UofM Sentiment Survey. And with some 10% of S&P constituents having thus far reported earnings for Q4, some 76% of those have bettered their bottom line of Q4 a year ago; but by the aforementioned P/E, the overall level of earnings remains tellingly weak relative to the price of the Index.

22 January 2026 – 08:34 Central Euro Time

Silver is the sole BEGOS Market at present outside (above) its Neutral Zone for today; session volatility has slowed a bit from recent days, thus far looking light-to-moderate. Looking at Market Rhythms for pure swing consistency, our Top Three through yesterday are — on a 10-test basis — Gold’s 12hr Parabolics, the Swiss Franc’s 4hr Price Oscillator, and Silver’s 4hr Parabolics; on a 24-test basis ’tis the Swiss Franc across the board by the 2hr Price Oscillator, 4hr Moneyflow and 4hr MACD. The P/E of the S&P 500 settled last evening at a whopping 63.7x; the yield is 1.156%; (the 3mo T-Bill annualized is 3.588%). The Econ Baro looks in “shutdown” arrears to Personal Income/Spending along with the attendant “Fed-favoured” PCE data; too, in arrears, shall be what is being termed a “revision” to Q3 GDP and its Chain Deflator.

21 January 2026 – 08:43 Central Euro Time

Gold records yet another All-Time High this morning at 4891 and is above its Neutral Zone for today as are both the Bond and Spoo; the Swiss Franc is below same, and session volatility for the BEGOS Markets is mostly moderate, Gold being the exception with a 142% tracing of its EDTR (see Market Ranges). Yesterday, both Gold and Silver, along with the Euro and Swiss Franc, moved and settled above their most volume-dominant Market Profile levels. Gold in real-time at 4845 is +446 points “high” above its smooth valuation like (see Market Values), of note, Silver at present is just mildly lower today at 94.45, whereas Gold is +1.7%. Scheduled for the Econ Baro are December’s Housing Starts/Permits, plus purportedly in “shutdown” arrears Construction Spending for both September and October.

20 January 2026 – 08:40 Central Euro Time

The BEGOS Markets’ two-day session continues with further record highs for both Gold (4727) and for Silver (94.75); both at present are above their Neutral Zones for this session, as too are Copper, the Euro and Swiss Franc; below same are the Bond and Spoo, and volatility (it being a double-day) is mostly robust, although Silver (despite its new high), Copper and Oil have traced no more than 70% of their EDTRs (see Market Ranges). Looking at Market Values (in real-time) for the five primary BEGOS components: the Bond is -2^15 points “low” vis-à-vis its smooth valuation line, the Euro -0.016 points “low”, Gold +342 points “high”, Oil +1.14 points “high” and the Spoo -76 points “low” having in this session crossed beneath its valuation line that portends still lower prices near-term. The Dollar Index — which had a firm start to the year — has given back more than that which was gained. Again, there is no Econ Data due until tomorrow. And mind our Earnings Season page as Q4 reporting picks up its pace this week.

19 January 2026 – 08:46 Central Euro Time

Given the StateSide holiday, ’tis a two-day session (for Tuesday settlement) for the BEGOS Markets. Therein at present we’ve both the Bond and Spoo below the session’s Neutral Zones, whilst above same are the Euro, Swiss Franc, Gold and Silver; volatility is moderate-to-robust, the two EuroCurrencies both having already exceeded 100% of today’s EDTR tracings (see Market Ranges). The Gold Update in maintaining our 5546 price forecast for this year nonetheless continues to cite the current overvaluation of Gold and Silver in this “Metals’ Mania Mayhem!”, noting that intra-week selling increased over that prior, even as prices further rose, and indeed are into higher record territory today (Gold thus far to 4698 and Silver to 94.37). The S&P 500 remains beyond any imaginable level of overvaluation, the futs-adj’d “live” P/E at this moment 59.2x. The reporting pace of Q4 earnings increases as the week unfolds. And nothing is scheduled for the Econ Baro until Wednesday.

The Gold Update: No. 844 – (17 January 2026) – “Metals’ Mania Mayhem!”

With all that in your metals’ pack, here’s the stack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 4651 (14 January 2026)

2026’s High: 4651 (14 January 2026)

10-Session directional range: up to 4651 (from 4356) = +295 points or +6.8%

Gold’s All-Time Closing High: 4634 (14 January 2026)

Trading Resistance: 4603 / 4621 / 4643

Gold Currently: 4601, (expected daily trading range [“EDTR”]: 86 points)

10-Session “volume-weighted” average price magnet: 4548

Trading Support: 4496 / 4471 / 4459

2026’s Low: 4319 (02 January)

The Weekly Parabolic Price to flip Short: 4154

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3901

The 300-Day Moving Average: 3401 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

To wrap, in the midst of this metals’ mania mayhem, we ought not be put off by some degree of price retrenchment, especially with 5546 for our forecast high as the year goes by.

“And here’s a surprise, mmb! Copper’s sister Coppélia just sent us this!”

Now Squire, do behave out there. And indeed, folks, stay with your Gold and Silver!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

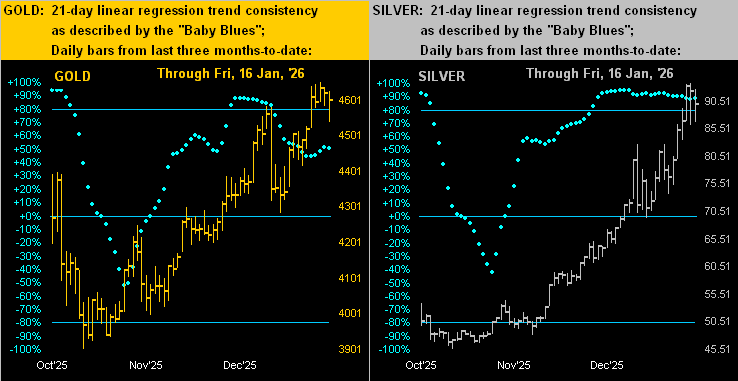

16 January 2026 – 08:45 Central Euro Time

Both Silver and Copper are below their respective Neutral Zones for today, whilst above same is the Spoo, (“live” fut’s-adj’d S&P 500 P/E now 60.7x); BEGOS Markets’ session volatility ranges from light (Bond and Euro EDTR tracings of 26%) to robust (Copper’s 102%); EDTRs are updated daily on the Market Range page. Gold has dipped below its most volume-dominant Market Profiles support of 4621, price currently 4612; however the precious metals remain extremely high vis-à-via their Fair Value as we’ll depict in tomorrow’s 844th consecutive Saturday edition of The Gold Update; obviously too, given lack of earnings support, the S&P remains overvalued by a massive margin; the riskless 3mo T-Bill yield (3.565%) is 3.1x that of the S&P’s dividend yield (1.131%). The Econ Baro wraps its busy week of 20 incoming metrics with January’s NAHB Housing Index and December’s IndProd/CapUtil.

15 January 2026 – 08:43 Central Euro Time

The “live” P/E of the S&P 500 settled yesterday at 60.2x. Meanwhile, we’ve presently the EuroCurrencies, Metals Triumvirate and Oil all below today’s Neutral Zones; within same are the Bond and Spoo, and session volatility for the BEGOS Markets is moderate-to-robust, with both Silver and Copper already having traced in excess of 100% of their respective EDTRs for today (see Market Ranges). All-time high metals’ readings recorded yesterday were: Gold 4651, Silver 93.56, and Copper 6.154. Through the first nine trading days of 2026, the Dollar Index has recorded a net daily gain six times. Our S&P leading MoneyFlow continues to thin with a bit of a negative bent, (see S&P 500: MoneyFlow). And the Econ Baro awaits January’s Philly Fed and NY State Empire Indices, plus in “shutdown arrears”, November’s Ex/Im Prices.

14 January 2026 – 08:38 Central Euro Time

Record highs continue for Gold, Silver (91.37!), Copper and the Spoo/S&P 500. Per last evening’s post on “X” (@deMeadvillePro) the S&P settled yesterday with a “live” P/E of 59.9x. This morning, all three elements of the Metals Triumvirate are at present above today’s Neutral Zones; the rest of the BEGOS Markets are within same, and session volatility is pushing toward moderate. Gold (4643) is in real-time +312 points above its smooth valuation line (see Market Values); Market Profile support is 4621, followed by 4603; (the most volume-dominant support is still 4459); and by its Market Trend, Gold’s “Baby Blues” of linreg trend consistency have ceased their recent fall. The Econ Baro looks to in “shutdown” arrears November’s Retail Sales, PPI, and purportedly October’s Business Inventories, plus Q3’s Current Account. And late in the session comes the Fed’s “Tan Tome”.

13 January 2026 – 08:46 Central Euro Time

On the heels of record highs yesterday for Gold, Silver and the S&P 500, we’ve at present both the Bond and Gold below today’s Neutral Zones; the balance of the BEGOS Markets are within same, and session volatility is light-to-moderate, except for the non-BEGOS Yen which has traced 118% of its EDTR (see Market Ranges for those of the BEGOS Markets). By Market Trends, all are linreg positive, save for the two EuroCurrencies. Looking at Market Profiles, volume-dominant supports are as follows: Bond 115^16, Gold 4459, Silver 75.90, Copper 5.8650, Oil 58.00, and the Spoo 6953; volume-dominant resistance for the Euro is 1.172 and for the Swiss Franc 1.271. Oil’s cac volume is rolling from February into that for March. And for the Econ Baro we’ve December’s CPI and Treasury Budget, plus purportedly in “shutdown” arrears, September’s New Home Sales.

12 January 2026 – 08:39 Central Euro Time

The BEGOS Markets finally appear to be waking up to the new year. The Gold Update cites sovereign invasions, currency concerns, and now we read of Chairman Powell facing an investigative issue. At present, both the Bond and Spoo are below today’s Neutral Zones, whilst the two EuroCurrencies and Metals Triumvirate are above same; only Oil at the moment is inside its Neutral Zone; session volatility is mostly robust. Too, The Gold Update points to the yellow metal’s year-to-date growth pace as sufficiently steep such that our forecast high for this year — 5546 — could be reached as swiftly as by February’s end, albeit this highly is unlikely as markets do not move in a straight line. ‘Tis a very busy week for the Econ Baro, although nothing for today is scheduled. And Q4 Earnings — which has had quite a weak start with just 43% of 23 reporting companies having beaten their Q4s of a year ago — looks later in the week to the major financial entities.

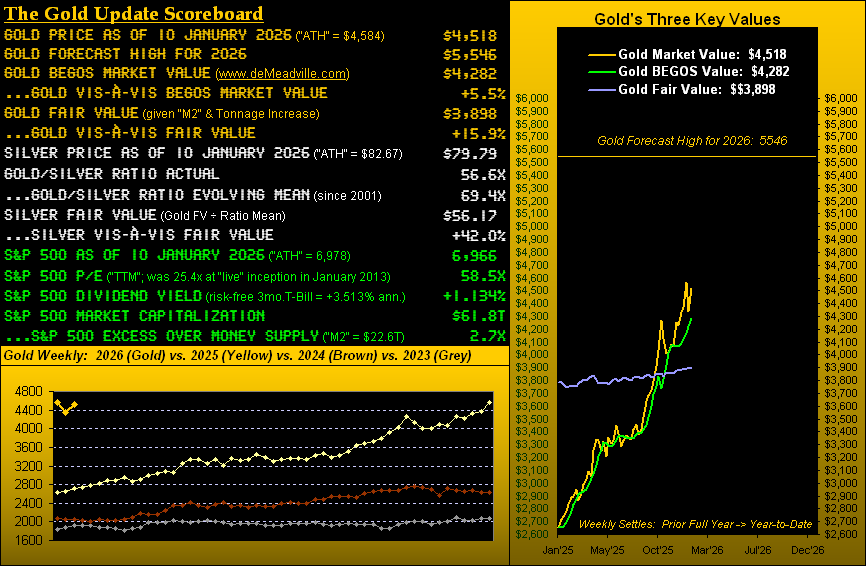

The Gold Update: No. 843 – (10 January 2026) – “Six Days into ’26, Gold and Silver Net Upticks”

Six trading days into 2026 find Gold having already netted a year-to-date gain of +4.3% and Silver +12.4%. Or … just in case you’re scoring at home … to go deeper inside the data for the 138 hours so far traded, 81(59%) have been up for Gold and 75 (54%) have been up for Silver.

Moreover, from the “‘Tis Too Early to Extrapolate Dept.”, Gold at its current year-to-date regressed growth pace would achieve our 5546 forecast high for 2026 come 27 February. Too early, indeed, perhaps too much detail. Yet it punctuates just how positive are the precious metals’ internals thus far into the young year.

“And like you say, mmb, markets don’t move in a straight line…”

‘Tis axiomatic, Squire, given markets’ means reversion is natural phenomenon ![]() “do-doo-de-do-doo”

“do-doo-de-do-doo”![]() –[Henson, ’69]. For as we’ve herein quipped over the years: “The markets are never wrong; but they can be vastly misvalued.”

–[Henson, ’69]. For as we’ve herein quipped over the years: “The markets are never wrong; but they can be vastly misvalued.”

And thereto, overvaluation is the present state of both the precious metals — and far more so — that of the S&P 500. As depicted in our above newly-enhanced Gold Scoreboard, whereas Gold settled this past week yesterday (Friday) at 4518, ’tis +5.5% above its BEGOS Market Value* of 4282, and further, +15.9% above Fair Value of 3898. Too, Silver’s settle at 79.79 is +42.0% above her Fair Value of 56.17. So clearly there will be price retrenchment for both the yellow and white metals as the year unfolds, albeit within the broader context of Gold getting to 5546.

(*Valuing Gold by its price movement relative to those of the five primary BEGOS Markets: Bond, Euro, Gold, Oil, S&P 500).

As to the S&P 500, today’s market capitalization of $61.8T is 2.7x the supportive StateSide liquid money supply (“M2”) of $22.6T. And as we wrote in last Thursday morning’s Prescient Commentary, the S&P: “…settled [Wednesday] with a “live” P/E of 57.2x, more than double from its inception 13 years ago [meaning] earnings have since grown at less than half the rate of the S&P itself…” Then yesterday, the S&P recorded yet another record high (6978), boosting such price/earnings ratio to now 58.5x per the Scoreboard .

Again we reprise Jerome B. Cohen: “…in bull markets the average [P/E] level would be about 15 to 18 times earnings…” What that means for you WestPalmBeachers down there is by buying the S&P as a whole unit today, you’d pay $58.50 for something that earns $1.00 (an implied yield of 1.709%, the actual dividend yield by the Scoreboard being 1.134%), all whilst facing a “means reversion” capital risk of worse than -50% upon it all going wrong.

‘Course for Gold, ’tis all going well, (and by present valuation too well, but hardly shall we complain). For the 52 weekly settles from one year ago-to-date, Gold is trending higher at a rate of +1.1% per week. At such pace, price a year from now would be dubiously 7843. Comparably, by century-to-date, there’s been but one other mutually-exclusive similar pace: from mid-May 2005 to mid-May 2006, (price recording a +69% run from 421 to 712). History — as is its wont — has thus repeated as we go to Gold’s weekly bars since this a date year ago, the blue-dotted parabolic Long trend now five weeks in duration:

Supportive indeed for the precious metals are the aforementioned concerns over the world becoming a bit more wobbly. Regardless, anticipated trimming of recently netted gains “ought” not be too much of a concern. As to technically monitoring it all, we’ve this from our Market Rhythms’ analyses, with the corollary that ’tis — whilst current — measured via hindsight per each study’s last ten swing signals, (even as “shorting Gold is a bad idea”):

- Gold: for pure swing consistency, its best study of late has been the Parabolics on the 12hr time frame, else if targeting a profit per swing, the daily MACD;

- Silver: for pure swing consistency, her best study of late has been the Parabolics on the 30mn time frame, else if targeting a profit per swing, the 2hr MACD.

And, as always, remember: just because a technical study has profitably panned-out ten times in-a-row, ever-shifting market dynamics can bring such streak to an abrupt halt time and again.

“Yer sure givin’ it all away today, mmb…”

Just our way of humbly sharing with our valued readers what we’re seeing, Squire. Here’s to Gold and Silver!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

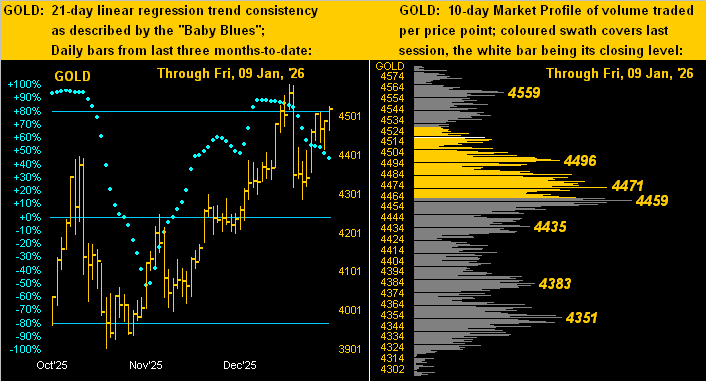

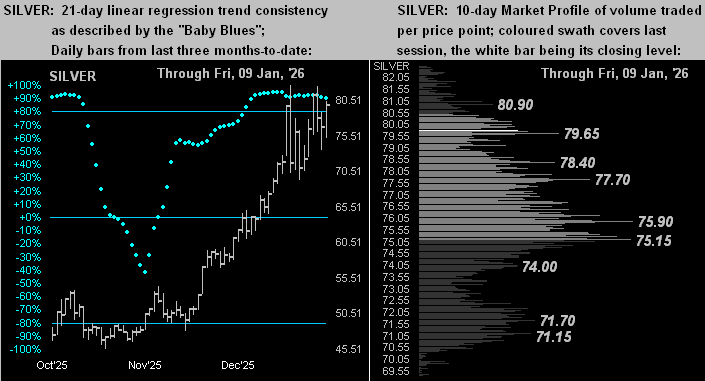

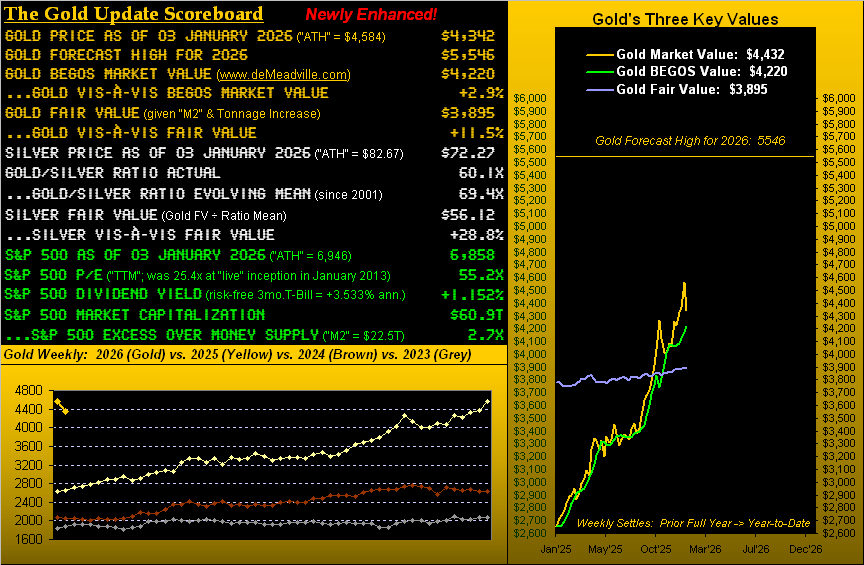

09 January 2026 – 08:36 Central Euro Time

Toward rounding out the first full trading week of 2026 , we’ve at present the Euro, Swiss Franc and Spoo below their respective Neutral Zones for today, whilst Copper is above same; BEGOS Markets’ volatility is moving toward moderate. Save for the Metals Triumvirate, EDTRs (see Market Ranges) are near or even below where they were at this time a year ago. The 30mn MACD for both Oil and the Spoo has been their best Market Rhythm on pure swing basis. By their Market Profiles, Oil finds volume-dominant support at 58.00 and the Spoo at 6953. At Market Trends, the Euro’s linreg (in real-time) has rotated from positive to negative, the Dollar Index continuing to get the currency bid thus far into the new year. The Econ Baro looks to January’s UofM Sentiment Survey, December’s Payrolls data, and in “shutdown” arrears, Housing Starts/Permits for perhaps both September and October. And tomorrow brings the 843rd consecutive Saturday edition of The Gold Update.

08 January 2026 – 08:36 Central Euro Time

The Spoo as a “continuous contract” topped 7000 yesterday for the first time; intraday, the S&P 500 made an all-time high (6966) and settled with a “live” P/E of 57.2x, more than double from its inception 13 years ago: that means earnings have since grown at less than half the rate of the S&P itself. At present, we’ve Gold, Silver and the Spoo all below their respective Neutral Zones for today; the balance of the BEGOS Markets are within same, and session volatility is mostly moderate. The Euro yesterday settled below its smooth valuation line (see Market Values) for the first time since 25 November, a portent of still lower prices near-term; at Market Trends, the Euro’s “Baby Blues” of trend consistency are accelerating lower as, too, are those for the Swiss Franc, and to an extent for Gold. The Econ Baro looks to some catch-up metrics today from the “shutdown”: included are November’s Consumer Credit, October’s Trade Deficit and Wholesale Inventories, and Q3’s initial read of Productivity and Unit Labor Costs.

07 January 2026 – 08:41 Central Euro Time

The Bond is at present above its Neutral Zone for today, whilst below same are Oil and all three elements of the Metals Triumvirate; session volatility for the BEGOS Markets is mostly moderate, save for the Spoo which thus far has traced just a wee 18% of its EDTR (see Market Ranges). Oil is now the only BEGOS component in negative linreg, albeit as noted yesterday, the “Baby Blues” of trend consistency continue to ascend, even as price is lower today; broadly, Oil’s best Market Rhythm — in hindsight with a profit target of 2.70 points per swing — has been its daily EMA, having reached that target the last 10 of 10 times; (too as noted yesterday, Oil’s best Market Rhythm on a pure swing basis has been the 4hr Moneyflow). Scheduled today for the Econ Baro are December’s ADP Employment data and ISM(Svc) Index, along with (purportedly for November) Factory Orders and Business Inventories.

06 January 2026 – 08:41 Central Euro Time

At present, we’ve the Bond below its Neutral Zone for today, whilst above same are both Silver and Copper; BEGOS Markets’ volatility is moderate across-the-board. Oil yesterday settled above (and currently is on) Market Profile support at 58.00: on a pure swing basis, Oil’s best Market Rhythm has been the 4hr Moneyflow; and by its Market Trend, although Oil’s linreg remains negatively sloped, but its “Baby Blues” of trend consistency are rising for the sixth-consecutive session. The Spoo at 6955 is -39 points below is continuous contract all-time high of 6994 (26 December ‘2025): the futs-adj’d “live” P/E of the S&P 500 is 55.7x and the yield 1.138% vs. the “risk-free” 3mo T-Bill annualized yield of 3.515%. Nothing is scheduled for the Econ Baro today; and as noted, Q4 Earnings Season is underway.

05 January 2026 – 08:43 Central Euro Time

Not surprisingly, the precious metals are getting a geo-political boost, both Gold and Silver, as well as Copper, at present above today’s Neutral Zones; below same are the EuroCurrencies and Oil, whilst quietly within are the Bond and Spoo; session volatility for the BEGOS Markets spans from light for the Spoo to robust for Copper. The Gold Update has selected 5546 as the yellow metal’s forecast high for this year, even as price is currently overvalued both by its Fair and BEGOS Market Values. Going ’round the Market Values horn in real-time for the five primary BEGOS components: the Bond is -2^03 points “low” vis-à-vis its smooth valuation line, the Euro is essentially in sync with same, Gold is +200 points “high”, Oil -2.35 points “low” and the Spoo +60 points “high”. The Econ Baro looks to December’s ISM(Mfg) Index. And Q4 Earnings Season gets underway.

The Gold Update: No. 842 – (03 January 2026) – “We Forecast Gold’s High for ’26 at 5546”

However, that raises the question of a barrier to Gold 5546: for if the Fed were not to cut… on verra…

In summary, yes Gold is — for the present– overvalued (and certainly so is Silver … again see the opening Scoreboard). But hardly would we sell here. More prudently, should Gold as the months unfold break below Fair Value (currently 3895), ’tis an opportunity to buy “mohrrrr….”

Either way, we’ll wrap it here with this observation: if Gold is overvalued, then the S&P 500 is massively so. Per our final 2025 Prescient Commentary from last Wednesday morning, we wrote: “The S&P 500 — which a year ago closed with its ‘live’ P/E at 46.1x — now finds it at 55.1x.” As depicted earlier in the BEGOS Markets’ Standings, the S&P sported a +16.4% gain for 2025; in turn, its Price/Earnings ratio increased (finishing the year at 54.6x) by +18.4%. For you WestPalmBeachers down there, that means relative to share prices, earnings growth for the Index as a whole wasn’t there! “Whoopsie…”

“GOT GOLD???”

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

02 January 2026 – 08:41 Central Euro Time

Whereas the final trading day of 2025 saw all eight BEGOS Markets record a down day, this start to 2026 finds five of the eight to the upside: the Metals Triumvirate, Oil and Spoo all at present are above today’s Neutral Zones; below same are the Bond and Swiss Franc, (only the Euro is currently within its Neutral Zone); session volatility is moderate across the board. Tomorrow’s 842nd consecutive Saturday edition of The Gold Update — with its newly enhanced Scoreboard — shall also of course feature the final 2025 Standings of the BEGOS components, as well as our annual forecasted price for Gold’s high. As for “the now”, by Market Trends, Gold’s “Baby Blues” of linreg consistency continue to drop, as do those for the EuroCurrencies, and to a degree, for the Spoo, too. The Econ Baro awaits Construction Spending: because of the recent StateSide “shutdown”, there is source conflict as this being the report for October or November. On verra… Let the year commence.

31 December 2025 – 08:46 Central Euro Time

The final trading day of 2025 is a full session for the BEGOS Markets. At present, we’ve the Euro, Swiss Franc, Silver, Copper and Spoo all below their respective Neutral Zones for the session; the other BEGOS components (Bond, Gold and Oil) are within same, and volatility is mostly moderate-to-robust, the precious metals again to this hour already having traded in excess of 100% of their EDTRs (see Market Ranges); the EDTR for Gold is 90 points and for Silver ’tis 4.30 points; for pure swing trading, Gold’s best Market Rhythm is its 12hr Parabolics, whereas for Silver ’tis her 30mn Parabolics. As anticipated, Gold’s “Baby Blues” of linreg consistency (see Market Trends) have confirmed falling beneath the key +80% axis: structural support spans the 4200s, (which today already have been tapped per the session low thus far at 4283). The S&P 500 — which a year ago closed with its “live” P/E at 46.1x — now finds it at 55.1x. The Econ Baro (its 36 missing “shutdown” metrics notwithstanding) concludes the year with last week’s Initial Jobless Claims. Back Friday for the full session. A Safe and Happy New Year to All!

30 December 2025 – 08:36 Central Euro Time

Yesterday’s substantive selling in the precious metals found Gold’s intraday high-to-low drop of -5.8% ranking 19th-worst century-to-date, whilst that for Silver of -15.1% ranked 6th-worst. At present, both metals above above their Neutral Zones for today, as too are both Copper and Oil; the balance of the BEGOS Markets are within same, and session volatility is light-to-moderate, save for the two precious metals already having traced in excess of 100% of their EDTRs (see Market Ranges). Gold’s “Baby Blues” of linreg consistency (see Market Trends) have dropped (in real-time) below the key +80% axis, confirmation of which likely leads to lower prices near-term. Yesterday’s -0.3% fall in the S&P 500 was internally weaker, the MoneyFlow regressed into S&P points having been -0.7%. The Econ Baro looks to December’s Chi PMI. And the FOMC’s 09-10 December meeting Minutes shall be released late in the session.

29 December 2025 – 08:39 Central Euro Time

On the heels of the current edition of the Gold Update entitled “Yes, Gold REALLY Is Getting Ahead of Itself”, the precious metals are taking a bit of a pounding this morning: with all three elements of the Metals Triumvirate presently below today’s Neutral Zones, Silver — which began the session north of 80 in trading to a record high of 82.67, is now 75.52 , -5.2% having traded 266% of its EDTR (see Market Ranges), and Gold is 4491 with a 165% EDTR tracing. The Bond is at present above its Neutral Zone, and session volatility for the BEGOS Markets is mostly robust as skewed by the metals; notably quiet is the Spoo with just a 27% EDTR tracing. By Market Values (in real-time) for the five primary BEGOS components: the Bond is -1^27 points “low” vis-à-vis its smooth valuation line, the Euro +0.012 points “high”, Gold +314 points “high” in spite of today’s selling, Oil -2.20 points “low”, and the Spoo +135 points “high”. Due for the Econ Baro is November’s Pending Home Sales.

The Gold Update: No. 841 – (27 December 2025) – “Yes, Gold REALLY Is Getting Ahead of Itself”

Good grief, Squire, how did that WestPalmBeacher get in here?

“He didn’t, mmb, it’s just some kinda AI infiltration…”

Well, we simply must get on to our Amsteg security team. Honestly…

To Gold: With specific respect to this week’s title, our missive from back on 06 September, (the 14th anniversary of 2011’s All-Time Intraday Gold High at 1923), was queryingly entitled “Is Gold (Again) Getting Ahead of Itself?” The key word therein is “Again”. Because prior, we’d originally postulated about Gold having gotten ahead of itself away back on 01 October 2011 (Update No. 98), price having settled that Friday (30 September 2011) at 1627 and thus already -15% from the 1923 record high of just four weeks earlier.

But annoyingly, such postulation was far more prescient than that for which we planned: come 03 December 2015 — yes four years hence — Gold’s fallout from 1923 to 1045 completed an all-in correction of -45%.

“Oh no, mmb, yer not sayin’ this is gonna happen all over again … are you?”

Calme-toi, Squire. ‘Tis not gonna happen all over again, for there’s a big difference between ![]() “Now and Then”

“Now and Then”![]() –[BeaTles, ’23]:

–[BeaTles, ’23]:

- “Then”, during that massive decline, Gold was discarded as a yield-less, storagely-expensive, debasively-irrelevant relic. The 1045 bottom was -57% below its Fair Value that day of 2450.

- “Now”, having settled yesterday (Friday) at a record-high close of 4562, ’tis a +337% increase over the past 10 years, 2025 finding everyone having suddenly become a Gold expert, in turn morphing the precious metals into “meme” stocks as we’ve on occasion quipped since this past spring (seasonally and pricewise).

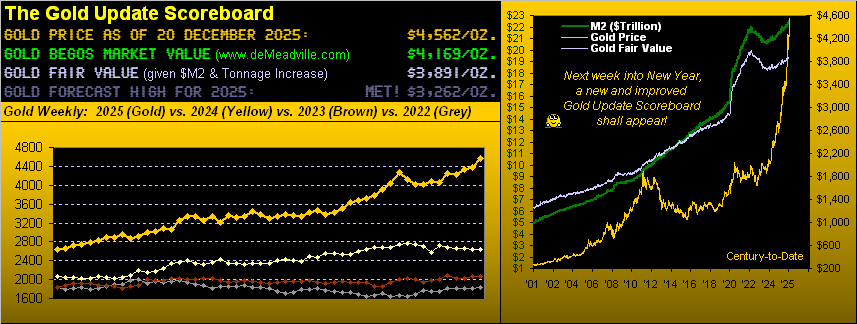

‘Tis been great for Gold, en route bringing Silver up to far more realistic pricing. But the recent overshoot of Fair Value is significant. By such metric, Gold at 4562 is now +17% above its 3891 Fair Value, whilst Silver at 79.68 is +42% above its 56.06 Fair Value. And you know, and we know, and given everybody from Bangor ME to Honolulu and right ’round the world instantly having become a Gold expert knows: the yellow metal since Nixon’s nixing of the Gold Standard (15 August 1971) has been priced sub-par relative to its Fair Value. But today, ’tis priced at that stated +17% premium. And “reversion to the mean” we ‘spect shall be seen.

Regardless of Gold’s mis-valuation, the market is never wrong: today’s 4562 level is the truth. Price’s primary driver these last 54 years is dollar debasement, offset to an extent by the increase in Gold’s supply.

Course, there is additional conventional wisdom to justify still-higher Gold: “Oh, the world is working toward war!”, they say; “Oh, the banks are going to fail!”, they say; “Oh, the fiats are finished!”, they say. And duly legitimate notions they all are. But at the end of the day, when such Gold-gyrating stimuli fall from the FinMedia fray, ’tis inevitably Dollar debasement that leads Gold’s upward way.

Thus — courtesy of the “Reverse Engineering Dept.” — we query:

“What ought be today’s level of the liquid U.S. Money Supply (“M2″) to justify 4562 Gold?”

M2 today is $22.5T and Gold’s Fair Value is 3891. So with a rough “back of the napkin” pencil scribbling — without regard for the ongoing increase in Gold’s tonnage — simple arithmetic proportion puts M2 up to $26.4T such as to be aligned with 4562 Gold today. For those of you scoring at home, that implies a +$3.9T M2 increase.

“And how long will that take, mmb?”

Squire, upon it all going wrong in the financial world, it could happen in a heartbeat. Regular readers of The Gold Update know of the “Look Ma! No Money!” crash wherein liquidation of the S&P 500’s current market capitalization of $61.5T would be readily supported by “only” $22.5T of M2. Your broker then remits to you an “I.O.U.”, stock trading ceases, and everyone “owed dough ” waits for the Federal Reserve to “print” and (in that vacuum) distribute the +$39T difference. Gold in turn would rapidly race up into the five figures.

That stated, following the Fed’s last series of rate hikes — which rightly rebased the Dollar in reducing M2 from $22.0T in April of 2022 to $20.6T come October 2023 — the money supply since has steadily returned to debasing, indeed at a regressed trending rate of +$15.7B per week.

Thus: at that pace from today’s M2 level of $22.5T to the $26.4T level supportive of Gold now at 4562 would take 250 weeks, i.e. some five years! But wait, it gets worse: account along the way for an increase in the Gold supply (typically some +2,770 tonnes per year) and empirically, it would take even longer for Gold to rightly be at today’s 4562. Yes, Gold REALLY has gotten ahead of itself; but far be it from us to stand in the way of the “bigger fish to fry” global financial stability concerns.

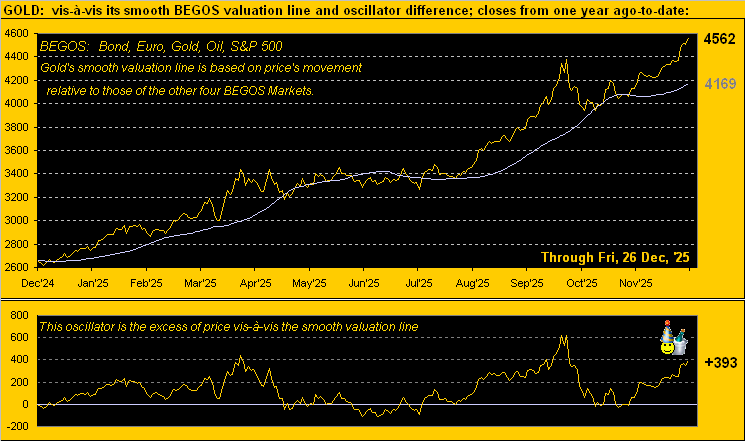

So relax: hardly are we bearish on Gold. We love what’s happening! But — the current “metals mania” aside — as we oft caution given Gold is a major liquid market, price shan’t ascend in a straight line, let alone move lower as such. And for the present being priced some +17% above Fair Value, Gold too is +9.4% (+393 points) above its BEGOS Market Value of now 4169:

And now into New Year we go, the record-high precious metals miraculously ![]() “Going to a Go-Go”

“Going to a Go-Go”![]() –[The Miracles, ’65]. As teased in the opening Gold Scoreboard, we’re revamping its look and expanding its summary of what we deem as critical “need-to-know” info on Gold, Silver, and too, the S&P 500: thus you’ll have a tidy summary at the top every Saturday. Indeed next Saturday shall be our month/quarter/year-end edition of The Gold Update (plus one trading day in January), including our Gold forecast high for 2026. So don’t give it a miss, as miracles do happen!

–[The Miracles, ’65]. As teased in the opening Gold Scoreboard, we’re revamping its look and expanding its summary of what we deem as critical “need-to-know” info on Gold, Silver, and too, the S&P 500: thus you’ll have a tidy summary at the top every Saturday. Indeed next Saturday shall be our month/quarter/year-end edition of The Gold Update (plus one trading day in January), including our Gold forecast high for 2026. So don’t give it a miss, as miracles do happen!

A Safe and Happy New Year to Everybody!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

26 December 2025 – 08:43 Central Euro Time

Today’s full session for the BEGOS Markets presently finds the Bond and Swiss Franc below their respective Neutral Zones, whilst above same are all three elements of the Metals Triumvirate, both Gold and Silver having again recorded new highs at 4562 and 75.50. Session volatility is moderate, noting therein that Silver has traced 105% of its EDTR (see Market ranges). Tomorrow’s 841st consecutive Saturday Edition shall give an estimate of how much the Money Supply (“M2”) need increase to catch up in matching these otherwise overvalued levels of the precious metals. Meanwhile, Gold by its BEGOS Market Value is (in real-time) +371 points above its smooth valuation line; the Spoo is currently +147 points above same. Nearby volume-dominant Market Profile support for Gold is 4518 whilst for the Spoo ’tis 6960. Nothing is due for the Econ Baro, (albeit 36 metrics remaining missing).

24 December 2025 – 08:33 Central Euro Time

We’ve furtherance of record highs this morning for the precious metals, Gold having tapped 4555 and Silver 72.75. At present above today’s Neutral Zones are both Silver and Copper; the balance of the BEGOS Markets are within same, and volatility for the abbreviated session is pushing toward moderate; (session closures range today from 18:00 GMT for stocks to 18:15 GMT and 18:45 GMT for the various BEGOS components). The S&P 500 yesterday settled at an all-time high (6910), albeit did not achieve its record intra-day high (6920 on 29 October); by Fair Value (+50 points) to the futures, the S&P at this instant would open lower by -6 points. And per Market Values, the Spoo in real-time is +134 points above its smooth valuation line; Gold is +364 points above same as price continues to break further above Fair Value (3896). Due for the Econ Baro are last week’s Initial Jobless Claims. Back on Friday for a full session, and thus a most Merry Christmas to one and all!

23 December 2025 – 08:33 Central Euro Time

Gold has cleared the 4500 handle in trading thus far to as high as 4531, whilst Silver has cleared its 70 handle in thus far reaching up to 70.16: whilst we welcome such lofty prices, a word to the wise is sufficient: Gold is at present +16% above Fair Value and Silver +24% above same. Too, the yellow metal is currently above today’s Neutral Zone, as are the Bond and Swiss Franc, a phenomena not unusual as we glide toward year-end. Session volatility for the BEGOS Markets is mostly moderate. Copper’s “Baby Blues” of linreg consistency (see Market Trends) continue to inch below the key +80%, albeit price has yet to respond in kind. They may be quite an array of data arriving today for the Econ Baro: problematic thereto is much conflict between our reporting sources as to what shall or shall not be issued, either timely or in arrears; we’ll have it all updated later in the session; also there is “talk” of another StateSide “shutdown” come late January.

22 December 2025 – 08:47 Central Euro Time

The current edition of The Gold Update entitled “Merry Metals!” is being well-vindicated this morning with record highs for both Gold (4453) and Silver (69.53); both are presently above today’s Neutral Zones as are Copper, Oil and the Spoo; below same is the Bond, and BEGOS Markets’ volatility is moderate, duly noting that Gold has traced 130% of its EDTR (see Market Ranges). Too, The Gold Update graphically summarizes the precious metals’ best pure swing Market Rhythms as currently Gold’s 12-hour Parabolics and Silver’s six-hour Moneyflow. The Spoo has regained the 6900s: currently 6910, the all-time high is 6975 (12 December); the futs-adj’d “live” P/E of the S&P 500 is 56.0x; the amount of money to move the S&P one point is the thinnest ’tis been since 15 October, (i.e. mind the froth). Nothing is scheduled today for the Econ Baro.

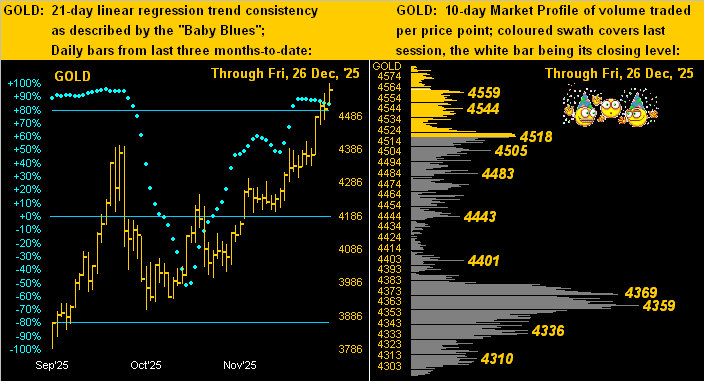

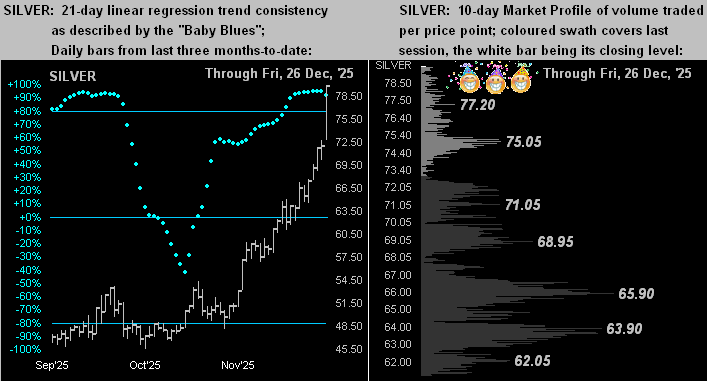

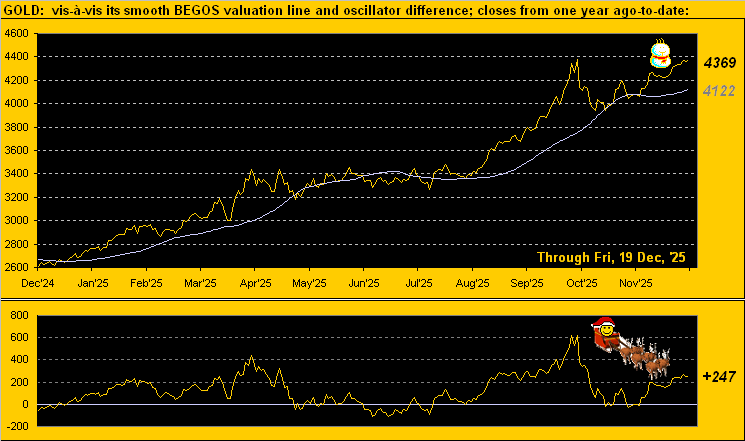

The Gold Update: No. 840 – (20 December 2025) – “Merry Metals!”

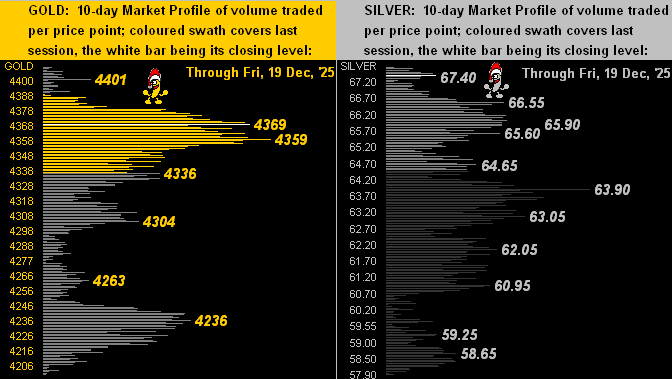

Next to our 10-day Market Profiles for Gold (below left) and for Silver (below right). With such an array of underlying support levels, ’tis truly a Santa Bananarama, which is ![]() “Really Saying Something … bop-bop shoobie do-wah”

“Really Saying Something … bop-bop shoobie do-wah”![]() –[’82]:

–[’82]:

Yet despite the Baro’s woes, the S&P 500 still seeks a Santa Claus rally, the Mighty Index now down just -14 points from November’s settle. We’ve recently pointed out that for the 24 completed Decembers thus far this century, 16 have been up, (which for you WestPalmBeachers down there means eight have been down).

Regardless, the FinMedia is “freaking out” (technical term). This past week brought two items of note from the children’s writing pool at the once highly-respected Barron’s. To wit:

—> (Tuesday) “Stock Markets Are Suffering Amid Bubble Fears” … “Suffering”? The S&P settled Tuesday a scant -1.5% below its all-time closing high. Now ’tis but -1.0%. But wait, it gets funnier:

—> (Friday) “The Stock Market Has a 10% Chance of a 30% Crash in 2026” … Since when did a 30% correction be deemed a “Crash”? More accurately, we’d opine — by employing the lost art of proper portfolio theory in concert with the S&P’s “live” price/earnings ratio of now 55.8x — that “The Stock Market Has a 100% Chance of a 50% Crash in 2026” … (write it down).

Rightly or wrongly either way, here’s the Gold Stack for Santa’s sleigh sack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 4410 (18 December 2025)

2025’s High: 4410 (18 December 2025)

10-Session directional range: up to 4410 (from 4199) = +211 points or +5.0%

Trading Resistance: Per the Profile 4410

Gold’s All-Time Closing High: 4374 (20 October 2025)

Gold Currently: 4369, (expected daily trading range [“EDTR”]: 66 points)

Trading Support: Profile notables 4369 / 4359 / 4336 / 4304 / 4263 / 4236

10-Session “volume-weighted” average price magnet: 4313

The Weekly Parabolic Price to flip Short: 4014

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3896

The 300-Day Moving Average: 3295 and rising

2025’s Low: 2625 (06 January)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Et voilà:

A Most Merry Metals’ Christmas to Everyone Everywhere!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

19 December 2025 – 08:43 Central Euro Time

Gold yesterday by its “continuous contract” reached another All-Time High at 4410; (the “front month” currently is February, which itself had reached 4433 on 20 October but with a lot of forward “premium” at that time when ’twas not yet the “front month”). Either way, more on having achieved 4410 in tomorrow’s 840th consecutive Saturday edition of The Gold Update. For the present, with session volatility for the BEGOS Markets moving toward moderate, we’ve the Bond and Swiss Franc below today’s Neutral Zones, whilst above same are Silver and Copper. Of note, Copper’s “Baby Blues” for linreg consistency (see Market Trends) yesterday dropped below their key+80% axis indicative of lower prices near-term; Copper’s best Market Rhythm of late is its daily MACD. The Econ Baro looks to December’s revision to the UofM Sentiment Survey and November’s Existing Home Sales; due too are that month’s Personal Income/Spending and “fed-favoured” Core PCE Index: instead however may come the still unreported data for October, given the “shutdown”.