And to be sure, there’s a lot on the mid-summer table to affect the price of Gold. Most imminently, next Wednesday (30 July) brings The Big Double-Whammy of StateSide Q2 Gross Domestic Product followed by the Federal Open Market Committee’s Policy Statement. Then two days hence brings 01 August and the introduction of more “Trump Tariffs!”

Too, there’s this from the “Oh By The Way Dept.” ‘Tis time for the U.S. Treasury to spritely come up with $7T to pay its noble holders of maturing Bills, Notes and Bonds. According to “AI” (“Assembled Inaccuracy”), as of this year’s Q1, operating cash amounted to about $406B, which combined with other monetary assets totaled a tad over $1T for 2024. Thus by your six-year-old’s first grade arithmetic, the Treasury is about -$6T short of its looming funding requirements.

So who or what is going to buy all this requisite new debt? Here’s a thought: remember that (as we herein mathematically constructed) “all” $7T of the COVID monetary “creation” essentially found its way into the S&P 500. So, why not have the Treasury thus promote a “group sell” of $7T in stocks with the proceeds moving into debt at its currently attractive rates? ‘Tis so easy, a WestPalmBeacher can do it.

“But mmb, that might crash the stock market…”

The stock market, Squire, is so overdue for a harrowing crash, be it driven fundamentally, technically and/or quantitatively, a “group sell” to save the U.S. Treasury would be the perfect crash catalyst.

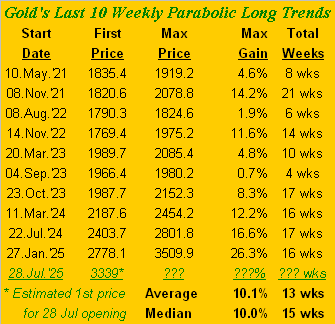

But with respect to Gold (and barring such selling of stocks), should the ensuing Treasury auctions be feeble, ‘twould fall to the Fed being forced to make that next BIG accounting entry to buy up the difference. And Gold, in turn, would go upside gonzo nuts (again, a technical term).

Speaking of stocks, we’ve run out of ways to indeed express (purposeful repeat) how we’ve run out of ways to describe the LooneyTunes overvaluation of the S&P 500. During recent years, we’ve herein detailed in-depth (using what is today an unknown science called “math”) sensible scenarios for the “Look Ma! No Earnings!” crash and the “Look Ma! No Money!” crash. Now let’s add to those the “That’s All, Folks!” crash, wherein upon it all going wrong, the market doesn’t so much crash as instead ’tis just closed, (rather akin to the “Look Ma! No Money!” crash). Then again the Fed can create the difference and ’tis more upside gonzo nuts for Gold.

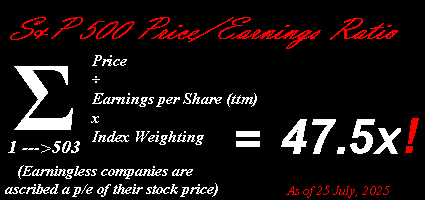

As to the current state of the S&P, ’tis now 23 consecutive trading days “textbook overbought”, as well as having arrived at our “extremely overbought” classification with a sub-par Q2 Earnings Season in process. Oh yes, we saw the CNBC[S] end-of-week headline last evening: “S&P 500 posts fifth straight record close this week, powered by solid earnings”. Hardly are earnings “solid”. To wit:

In this era of dumbing-down earnings estimates to dirt, ’tis super easy to beat ’em: so far for Q2, we’ve 149 S&P 500 constituents having reported, of which 79% have exceeded expectations! Why typically, only 76% so do! Sadly however, here’s where the “solid” earnings hocus-pocus loses focus. In an average Earnings Season, 66% of the constituents improve their bottom lines over the like quarter of a year earlier. To this point for Q2, such rate has slowed to 63%. ‘Course that shan’t be on CNBS, Bloomy nor FoxyB. But ’tis why the following multiple has gone beyond stoopid:

Again, don’t argue nor ask “AI“; just do the math. And per last week’s piece, yes, we still sense “The Sell” shall be ever-intense.

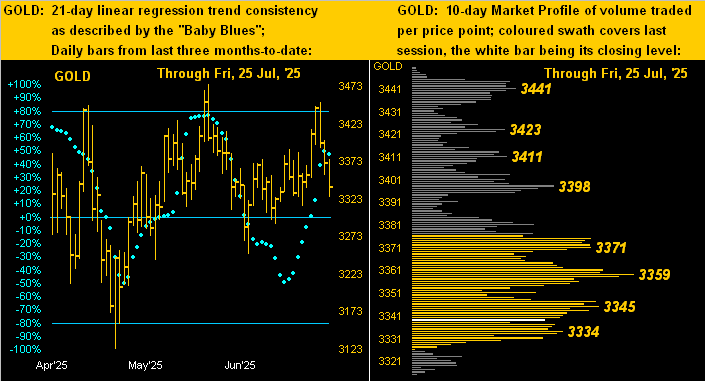

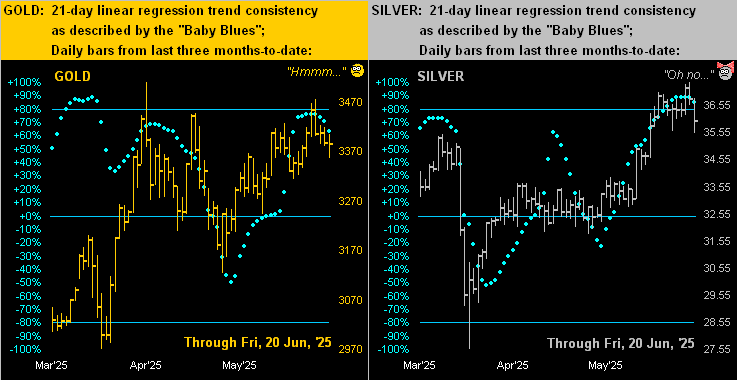

As to the math that makes up the Economic Barometer, as anticipated, ’twas well ahead of last Monday’s lagging indicator known as the Conference Board’s “Leading Indicators”. So severe had been June’s Econ Baro plunge, we knew the consensii for just -0.1% shrinkage in the June reading was too timid: rather, it came in (no surprise) at -0.3%. Too, the month’s Existing Home Sales slowed and Durable Orders shrank. But bailing the Baro out by just the wee-est of bits was growth in June’s New Home Sales, plus a reduction in the prior week’s Initial Jobless Claims. So below, we’ve the whole picture from one year ago-to-date. Duly therein note the insert of the S&P 500 futures chart for the past month (21 trading days): we made such a song-n’-dance a week ago about the baby blue dots of trend consistency being finally in decline … but they’ve suddenly lurched back up (per the three red dots). “Perfect timing ain’t easy…”: