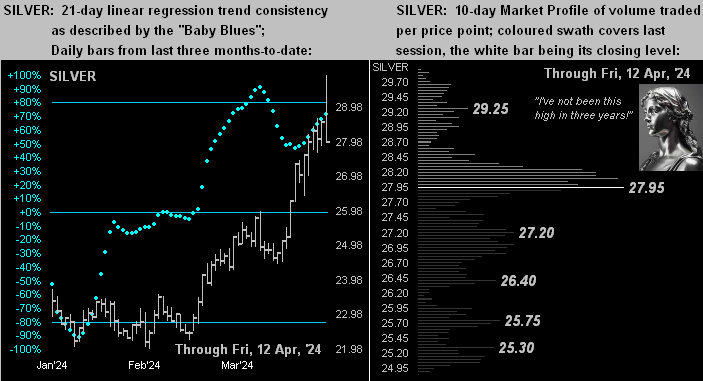

To sum it all up with further Gold highs intact, let’s wrap with the stack:

The Gold Stack

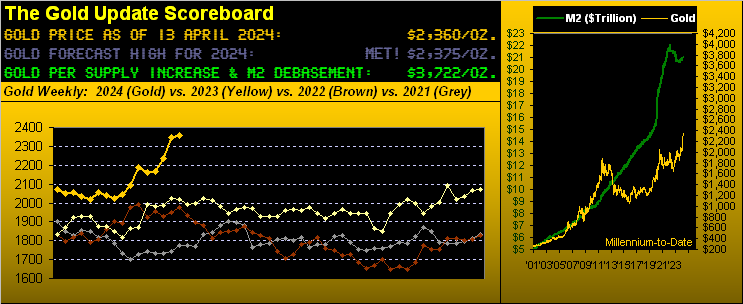

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3722

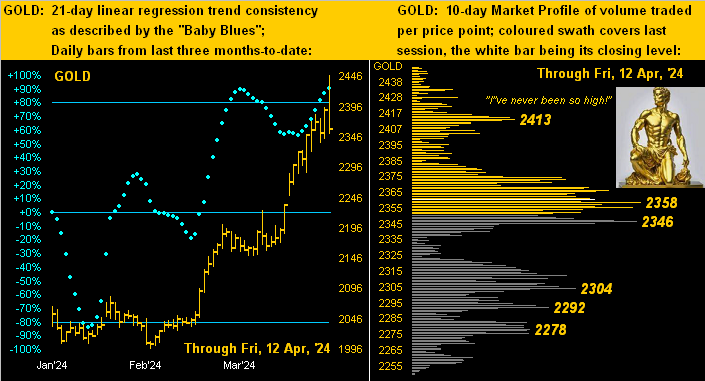

Gold’s All-Time Intra-Day High: 2449 (12 April 2024)

2024’s High: 2449 (12 April 2024)

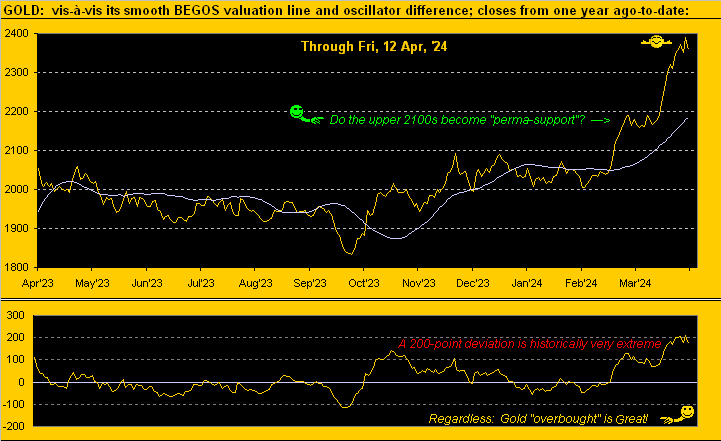

10-Session directional range: up to 2449 (from 2249) = +200 points or +8.9%

Trading Resistance (Profile selection): 2413

Gold’s All-Time Closing High: 2391 (11 April 2024)

Gold Currently: 2360, (expected daily trading range [“EDTR”]: 44 points)

Trading Support (Profile selections): 2358 / 2346 / 2304 / 2292 / 2278

10-Session “volume-weighted” average price magnet: 2340

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Weekly Parabolic Price to flip Short: 2023

The 300-Day Moving Average: 1996 and rising

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Next week brings 13 metrics into the Econ Baro, plus Q1 Earnings Season ramps up, notably featuring financial institutions. We indeed sported a wry smile yesterday over the FinMedia’s concern of Wells Fargo (WFC) having beaten earnings “estimates”, but the stock then falling “on the news”. Perhaps ’twas because the company actually made less money than a year earlier, (but we’re not supposed to point that out). Best to point to that which broadly makes money and secures your world of wealth: Gold!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro