“And now for something completely different” –[Monty Python, ’71]. Rarely do we bring up bits**t…

“Now, now, mmb…”

…yes, Squire, ok, “Bitcoin”. But it did take prime time billing this past week in anticipated –and in turn — approval of 11 exchange-traded funds now tradable (including from some high-level names such as Franklin Templeton, Blackrock, and Fidelity). And whereas with both Gold and the Casino 500 we’ve mathematical extremes vis-à-vis price and valuation (the former priced way too low and the latter way too high), with Bitcoin price is valuation given ’tis something based on nothing beyond a fixed supply. Reprise: “The market is never wrong”; ’tis where the traders have placed Bitcoin: thus ’tis priced right at valuation, pure and simple. Through transactional growth should Bitcoin gain further acceptance toward supplementing worthless fiat currencies, the price ought materially rise ![]() “as time goes by…”

“as time goes by…”![]() –[Herman Hupfeld ’31].

–[Herman Hupfeld ’31].

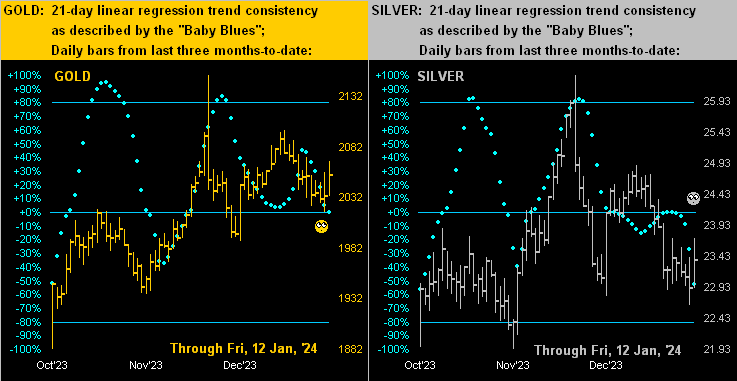

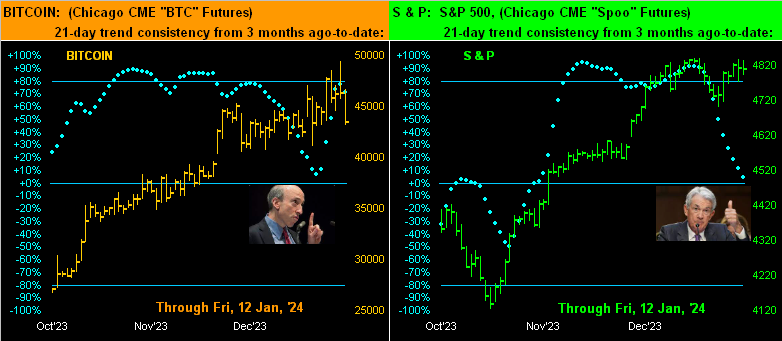

Either way, we decided to take a peek at “The Now” for Bitcoin. Since the SEC’s cautionary “Gensler Granting” of the ETFs this past Thursday, Wall Street treated Bitcoin as essentially it does “all things” anticipated: the rumour having been bought, the news then was sold. ‘Tis depicted here (at left) across the past three months-to-date, the rightmost two days evident of the peak (futs 49,435) and subsequent sell (futs now 43,425). The “Baby Blues” nicely captured the consistency of the recent run up before pipping down on Friday. For the present, the strength of the broader trend across the panel is encouraging, however there’s that unfilled gap from 04 December (39,640 to 40,325); still, because Bitcoin spot trades ’round the clock, such unfilled gap may be mere talk. But not so much mere talk are the S&P futures (at right), the “Baby Blues” therein extending their descent. “Got stock?” Sorry to hear that:

Thus there we are for this week as Gold bided its time whilst Bitcoin saw prime time … at least for a bit. Directionally near-term for Bitcoin, we’re clueless. Broadly for Gold we’ve no concerns. But for the Casino 500, we’re worried the whole roulette wheel could fly right off the spindle (given we do the earnings — or lack thereof — math). Regardless with respect to the latter, the children’s writing pool over at the once-mighty Barron’s ran this past week with “Why S&P 500 Pain Could Turn to Gains”. What pain? There’s been no S&P pain since the January-October “owie” back in 2022. Which in turn (save for the brief COVID crash and dash) pales in comparison to the last real pain from the 2007-2009 FinCrisis. But through generational turnover in today’s “stocks never go down” bubblesphere, this is to where we’ve arrived. And when the fear sets in that upon selling one’s stock, one might not actually receive the proceeds, the stock market rather than crashing might instead simply shutdown … just a passing thought.

GOT GOLD???

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro