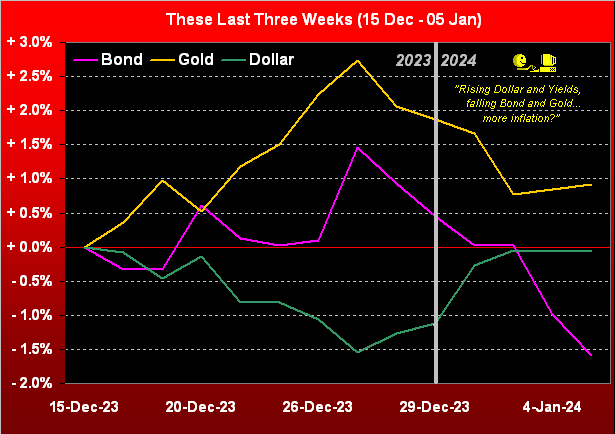

Hardly is renewed inflation a firm forecast. Yet curiously, the Buck and the Bond appear early on as inflation anticipative; and as is our wont to say: “…the market is never wrong…”

“But as you also always say, mmb, it can be really misvalued…”

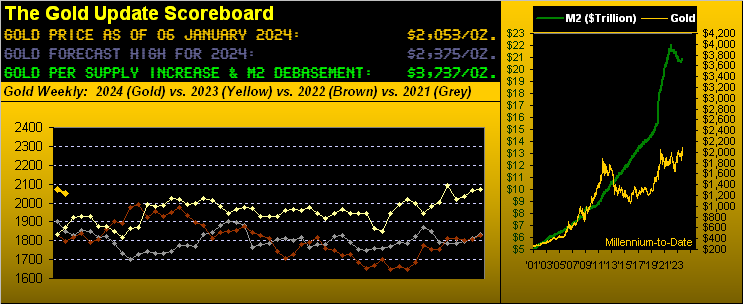

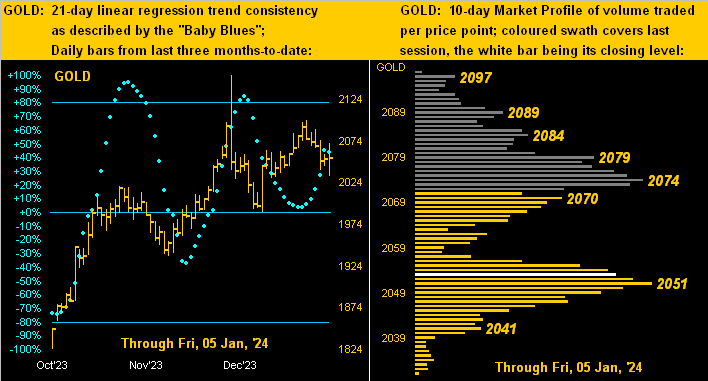

True enough, Squire, the two most glaring examples (per our honestly performed math) being the S&P 500 priced +76% above earnings valuation and Gold priced -45% below debasement valuation. As for ![]() “How long has this been going on…”

“How long has this been going on…”![]() –[Ace, ’74], the S&P’s valuation above mean and Gold’s valuation below same extend back a good dozen years. “…tick tick tick goes the means reversion clock…”

–[Ace, ’74], the S&P’s valuation above mean and Gold’s valuation below same extend back a good dozen years. “…tick tick tick goes the means reversion clock…”

But as to inflation anticipation: between now and the Fed’s end-of-January confab, StateSide there’re four key incoming data sets on inflation: the Consumer Price Index, Producer Price Index, Export/Import Prices, and the “Fed-favoured” Personal Consumption Expenditures Index. And on this side of the Pond as the year begins, we’re weathering an +8% increase in the cost of our morning café crème/croissant … ouch!

Why? Because “the club” (oh yes) says ’tis responding to price increases in what it now pays per kilo of coffee. So we decided to check: and ICE Coffee futures for March delivery have increased in the last few months by as much as +41% (10 October low to 19 December high). However, the good news for you caffeine heads out there is Dow Jones Newswires having run yesterday (Friday) with “Eurozone Inflation Rose Less Than Expected, Keeping Rate-Cut Talk on Track” in turn easing our inflative coffee cost concerns … whew!

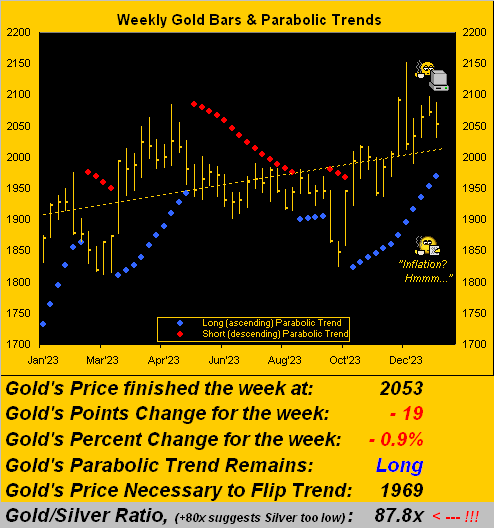

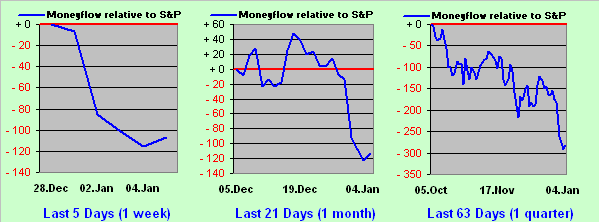

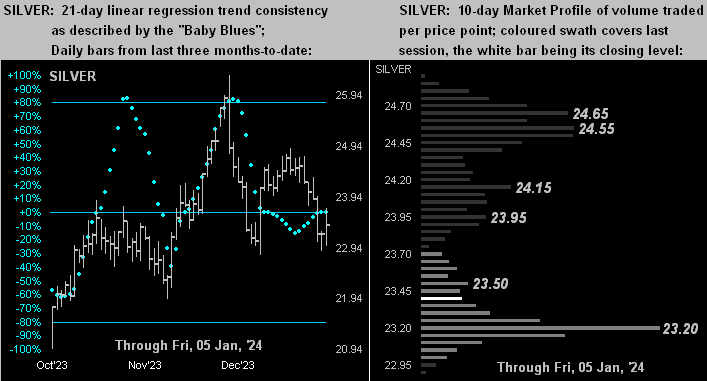

But as this is not “The Coffee Update”, let’s get on to Gold, which indeed has stumbled thus far into New Year, price having sported its first down week since that ending 08 December in settling yesterday at 2053, albeit a still comfy +84 points above the parabolic trend’s flip-to-Short level at 1969. And at the foot of this weekly bars graphic we’ve the Gold/Silver ratio now 87.8x, its highest end-of-week level since that ending last 10 March, (the century-to-date average but 67.9x):

We opened in musing on inflation: reporting thereto ranks significant in the first full trading week of 2024 with December’s CPI due Thursday (11 January) followed by the PPI on Friday (12 January). Shall such metrics renew the inflation scare? Or instead remain benign over which we’ve nothing to care? As a great friend and financial colleague remarked over this morning’s inflated coffee: “This is not going to be an easy year.” Indeed with valuations so out of whack, it may not be an easy several years. “Well, ya gotta buy the dip”, they say. Ok, you go first, Conway. We’ll hedge with Gold for the Long way!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro