Thus we’ve covered calamity following Gold’s record high — and to an ongoing extent — same for the above Econ Baro. But what about (as entitled) misfortune-to-be for the stock market? After all the FinMedia appears all-in for an S&P 500 record high (above 4819 vs. the current 4608 level). To wit, Dow Jones Newswires just reported “The VIX says stocks are ‘reliably in a bull market’ heading into 2024…” So clearly no one has done the math as to the stock market’s usual demise when the VIX is this low (12.35 at Friday’s settle). And yet by the website’s S&P 500 menu, we’ve still yet to see any true “fear” in the MoneyFlow, even as we tweeted so (@deMeadvillePro) this past Tuesday.

Further, we’ve herein on occasion enumerated a number of factors continuing to be present for it all to go wrong for stocks, notably the ongoing lack of earnings support. Yet as a long-time reader wrote in this past week: “It hasn’t been about EPS for a long time. It’s all about stock price.” And we comprehensively agree. That is because “It’s different this time” … just as ’tis always been different prior to every one of the stock market’s true crashes; (e.g. in our lifetime: 27 August 1987, 24 March 2000, 11 October 2007, and 19 February 2020, not to mention the myriad of other double-digit “corrections” therein). Imagine the 38 roulette slots (or 37 here in Europe) having their numbers replaced with S&P 500 constituent symbols. “Half on NVDA and half on AMZN!” … “Le jeux sont FAIT, Monsieur, rien ne va PLUS!” That’s where we are today.

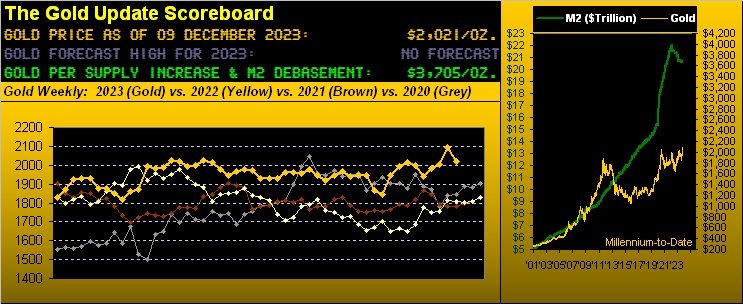

Not to belabour the point, but we have a question. What are companies such as Advanced Micro Devices (AMD, p/e 1,003.3x), Ceridian HCM (CDAY, p/e 2,593.4x), Ventas (VTR, p/e 3,593.8x) et alia even doing in the S&P 500? How about the Index’s 34 constituents not even making money? Reprise the late, great Vince Lombardi: “What the hell’s goin’ on out there?!?!?” (Friendly reminder: US liquid Money Supply [“M2”] now $20.7T; S&P 500 market capitalization now $40.2T; have a nice day).

Stark misfortune-to-be, indeed. By any historical yardstick, the is S&P is so significantly overstretched ’tis stunning that it hasn’t yet steeply succumbed. But until it does — and ’twill — as is our wont to say, the Investing Age of Stoopid merrily rolls on its way.

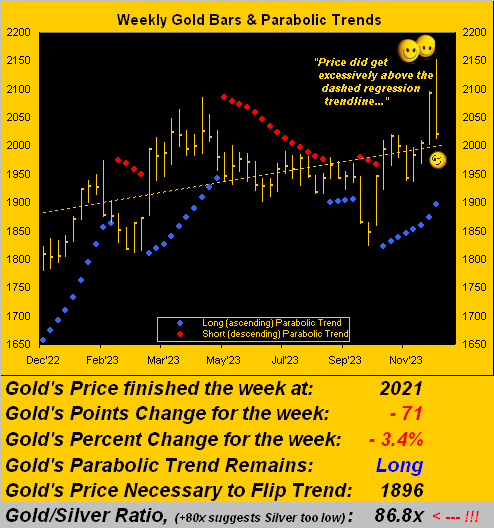

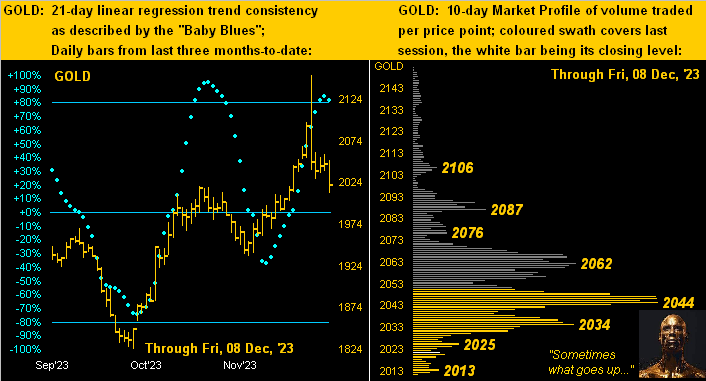

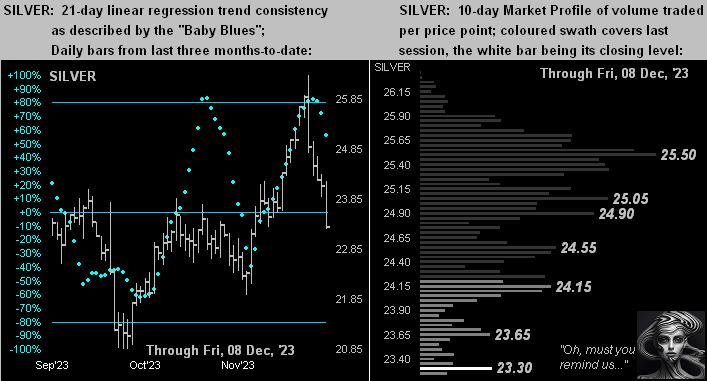

Meanwhile not so merrily rolling downward this past week were the precious metals. First to Gold’s two-panel graphic of the daily bars from three months ago-to-date on the left and 10-day Market Profile on the right. Earlier we mentioned Gold’s key 21-day linear regression trend as being up, which ’tis; however, its baby blue dots of trend “consistency” are just now kinking over to the downside, suggestive of still lower prices near term. Yet by pricing structure, we don’t see too much further damage beyond the present 2021 level down to 1975. But by the Profile for now, the mid-2040s clearly show as trading volume resistance: