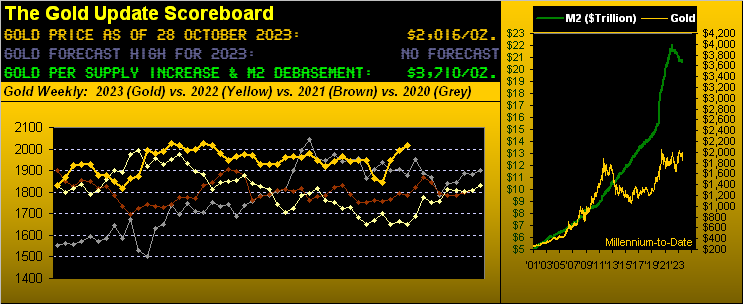

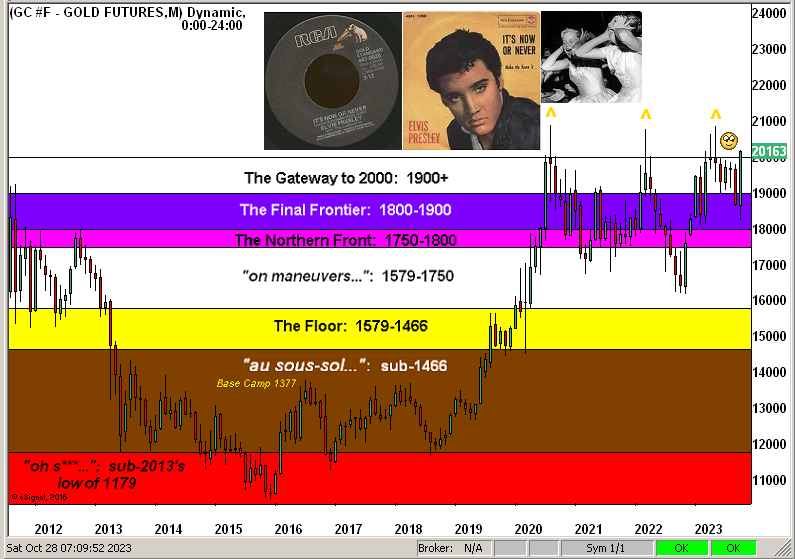

So with but two trading days remaining in October, here now is our stratified Gold Structure by the month across these past dozen years. As oft previously shown, now courtesy of the “Here We Go Again Dept.” we’ve Gold’s triple top which “is meant to be broken” as highlighted by the three Golden arrows. Moreover, we’ve anticipated on occasion throughout this year’s missives that Gold shall record a fresh All-Time High in 2023: obviously the momentum is there, barring a post-geo-political price retrenchment (as is the rule rather than the exception). Nonetheless, let’s cue Elvis from back in ’60 with ![]() “It’s now or never…”

“It’s now or never…”![]() :

:

Through these 10 months we’ve emphasized the importance of doing the math to get to the truth of such critical metrics as economic inputs, p/e calculations, and so forth. And whilst nothing light can be made of the horrific Mid-East mayhem, as this past week unfolded a mathematical “challenge” shall we say “came to light” over at the United States Department of State. Hat-tip ExecutiveGov which reported: “The Department of State has issued an advisory cautioning United States citizens against travel to more than 200 countries amid rising geopolitical tensions and conflict.” ‘Course, you can see where this is going, given (hat-tip Quora) stating: “Today, there are 197 countries in the world…“ The bottom line here being: if you’re in the States, you’re sorta stuck from going anywhere, nor beyond! Best therefore not to squirm; rather stay firm and stuck in Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro