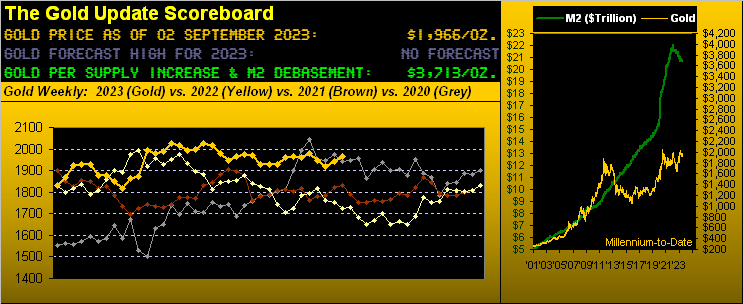

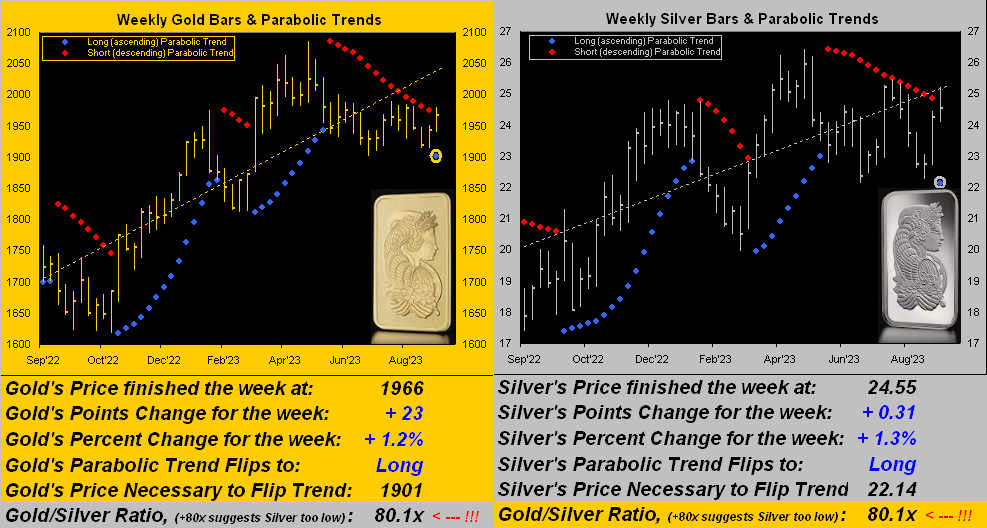

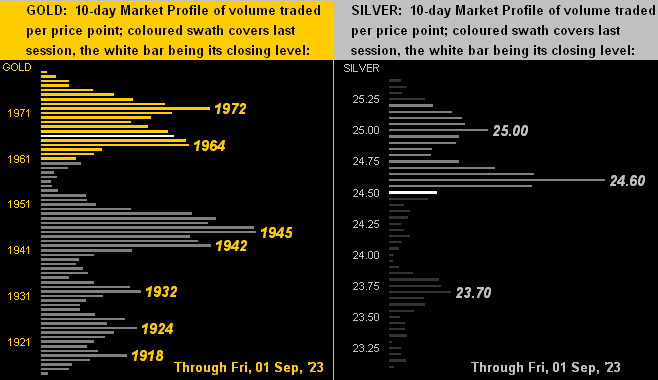

‘Course the key question from here is: “How high is high?” Notwithstanding last Spring’s structural resistance (for Gold in the 2000-2100 range and for Silver in her 25-27 range), let’s recall “average maximum” price follow-throughs. For Gold’s last 10 parabolic Long trends (dating back to September 2018), the average max upside upon Long trend confirmation is +11.1%: thus in that vacuum from today’s 1966 level, to reach such “perfect world” average would bring an All-Time Record High of 2184. Likewise for Sister Silver’s last 10 parabolic Long trends, (in her case dating back to December 2018), the average max upside (as anticipatively noted a week ago) is +19.6%. Such increase from today’s 24.55 price, would bring 29.36, a level not traded for Silver since 01 February 2021.

And for Silver, that’s still a far cry from her All-Time Record High of 49.82 on 25 April 2011, the Gold/Silver ratio on that day a mere 32.1x versus today’s 80.1x. The century-to-date average of that ratio is now 67.7x. Pricing Silver to that puts her at 29.04 … which is not far from the just-cited 29.39 potential upside follow-through per the new parabolic Long trend. ‘Tis one of those things that happily makes you go “Hmmm…”

“Hmmm…” (not necessarily happily) also applies to the state of the Economic Barometer. Hardly is it humming along, but neither is it sputtering to a stop. From this past week’s load of 16 incoming metrics, 8 showed period-over-period improvement, 7 were worse, and arguably the most important of all the data points — Core Personal Consumption Expenditures — again came in at +0.2% (an annualized rate of +2.4%) for the month of July. Such rate of this Federal Reserve-favoured inflation gauge means the Open Market Committee — some say — shan’t further raise their Banks’ Funds Rate for the balance of the year. On verra…

To look at the Econ Baro year-over-year, its net neutral state may argue that the Fed simply go to bed, i.e. “Everything’s great!” Dow Jones Newswires just went on record with August’s StateSide jobs report as “near perfect”. And as for equities, Bloomy concluded the week with “Stock Traders Get Back to Believing Everything is Just Perfect”. Perfection abounds. And why not? Oh to be sure, risk-free three-month U.S. “no debt ceiling dough” settled the week at an annualized rate of 5.268%, whereas the “all-to-risk” S&P 500’s yield is a paltry 1.507%. BUT: it doesn’t matter for neither do earnings, our “live” price/earnings ratio for the S&P finishing the week at 40.6x, not quite double the S&P’s 66-year lifetime median ’round 23x. (Best not to wreck everyone’s fun).

Regardless, here’s the Baro with the S&P 500 today at 4516, only -5.9% below its all-time closing high of 4797 from back on 03 January 2022: