Meanwhile, FedChair Powell inferred (depending on one’s source) this past week that at least (maybe) two more FedFunds rate hikes are in the cards for this year, and further that inflation may take years to tame. ![]() “Ain’t that a shame…”

“Ain’t that a shame…”![]() –[Fats Domino, ’55]. And the Fed-favoured inflation gauge of Core Personal Consumption Expenditures for May says ’tis so: it came it at +0.3%, which annualized is +3.6% — the 12-month summation now +4.3% — still more than twice the Fed’s target of +2.0%. As to the “elasticity” effect of FedHikes on the inflation rate, we’ll leave such to you brighter bulbs out there. But clearly there’s more pain to gain.

–[Fats Domino, ’55]. And the Fed-favoured inflation gauge of Core Personal Consumption Expenditures for May says ’tis so: it came it at +0.3%, which annualized is +3.6% — the 12-month summation now +4.3% — still more than twice the Fed’s target of +2.0%. As to the “elasticity” effect of FedHikes on the inflation rate, we’ll leave such to you brighter bulbs out there. But clearly there’s more pain to gain.

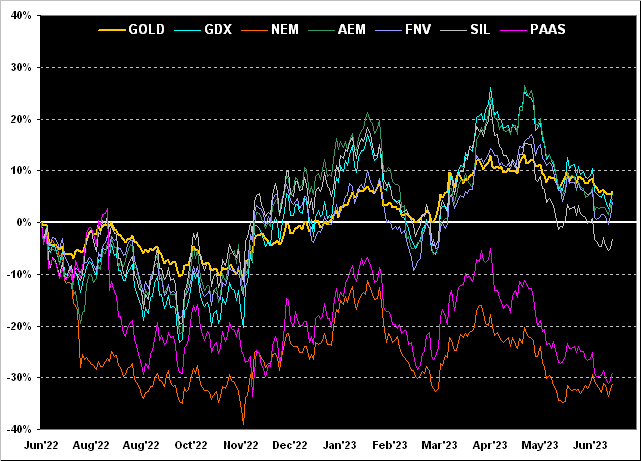

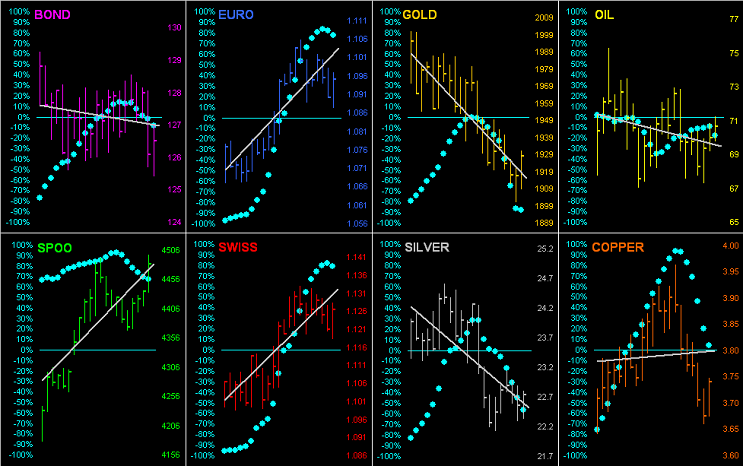

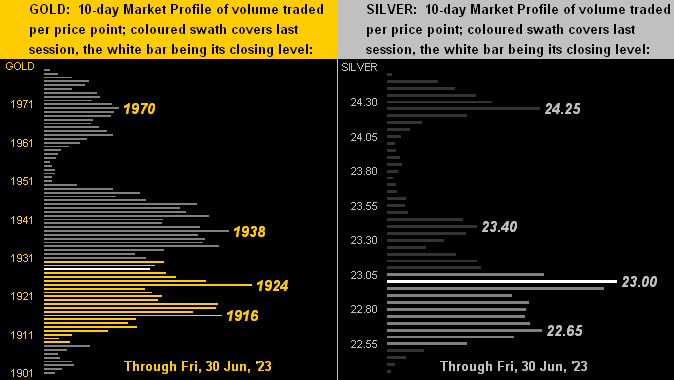

As to BEGOS Markets’ pain, let’s next go ’round the horn for all eight components across the past 21 trading days (one month) by their daily bars and baby blue dots of trend consistency. And as you can see, four of the grey trendlines are rising and four are falling; but in all eight cases, the “Baby Blues” are now in decline, certainly so those for Copper for which at the start of last week we so tweeted (@deMeadvillePro) in anticipating lower price levels. All of this of course is a harbinger of higher interest rates and thus the Dollar leading The Ugly Dog Contest:

To close, the more this stuff comes up, the more bemused we find ourselves. This time’ round over at an event hosted by the ever-regal Brookings Institution spoke one Graham Steele (Assistant Secretary of the Treasury for Financial Institutions), who stated “…Work on climate-related financial risk and the insurance sector is a top priority for the Biden-Harris Administration, the Treasury Department, and FIO…” (Indeed throughout the Secretary’s address the word “climate” was mentioned 38 times, thus the thrust of it all).

But the phrase “climate-related financial risk” really hit home with us with respect to the extreme undervaluation of Gold versus the extreme overvaluation of the S&P 500. This was discussed earlier today with a distinguished friend and colleague, who likened it to Publius Ovidius Naso’s character Icarus (8 A.D.) being the S&P as his bees-waxed featherings melted away upon approaching the sun, i.e. Gold:

So don’t find yourself head-over-heels when suddenly the S&P is “limit down”; rather, get some Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter: @deMeadvillePro