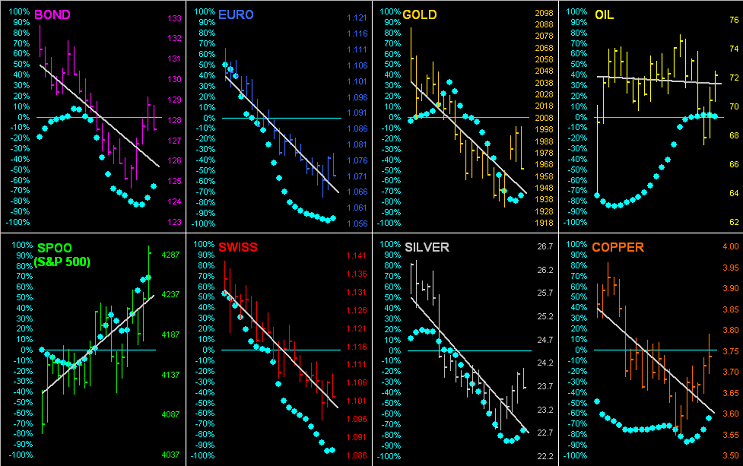

It essentially being month-end, let’s open up the BEGOS Markets’ gates as we go ’round the horn for all eight components by their daily bars from one month ago-to-date. As shown, save for the senseless S&P (Spoo), the balance of the diagonal trendlines are down given the firming Dollar![]() “phenomenon do-do-do-doooo…”

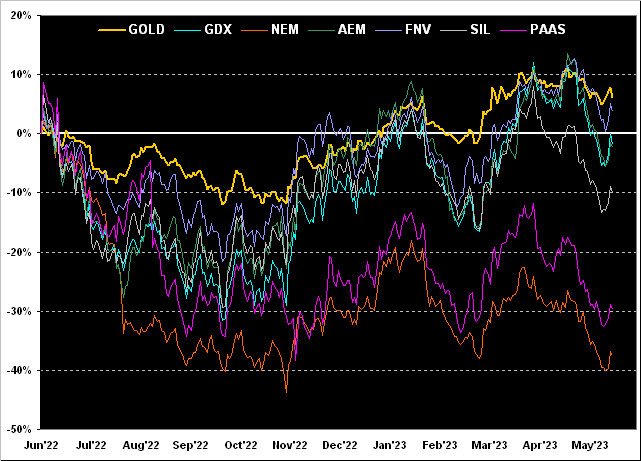

“phenomenon do-do-do-doooo…”![]() . And as you regular website viewers know, the baby blue dots represent the day-to-day consistency of each component’s grey trendline. So notably mind the “Baby Blues” for both Gold and Silver as they’re just starting to curl upward:

. And as you regular website viewers know, the baby blue dots represent the day-to-day consistency of each component’s grey trendline. So notably mind the “Baby Blues” for both Gold and Silver as they’re just starting to curl upward:

Which in turn leads us to this wrap.

We’ve oft referred to the current monetary climate as The Investing Age of Stoopid. So bizarre has it become that we are seeing headlines which a generation ago would have been regarded as completely irrational, (and obviously never would have made the front, if any, newspaper page). Nonetheless, the once quite useful WSJ just ran above Friday’s fold with “Robust Labor Market Poses Threat to Stocks’ Rally” –> What? Shouldn’t a robust labor market encourage a stocks’ rally? But then we forget. In this New Age of piling into earnings-less stocks, valuation has no bearing to price. Rather the Fed has become EVERYTHING, even as FinMedia guidance to the Fed’s “next move” is useless as it changes from week-to-week: “They’re gonna pivot; no wait, they’re gonna pause; no wait, they’re gonna raise, but only once and then they’re gonna pause…” Good grief: for the bazillionth time, this is why we do the math. (To which point, see last week’s missive as regards the Fed-favoured Core PCE inflation gauge). And by doing the math, we know that to expect.

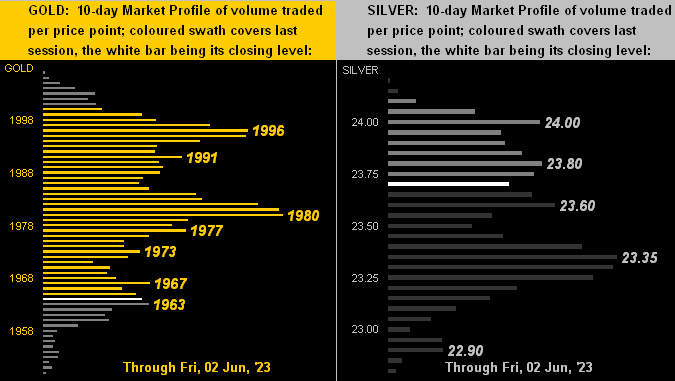

And most broadly, yes, Gold shall eventually go to the moon! So either get in, or get off the gantry!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter: @deMeadvillePro