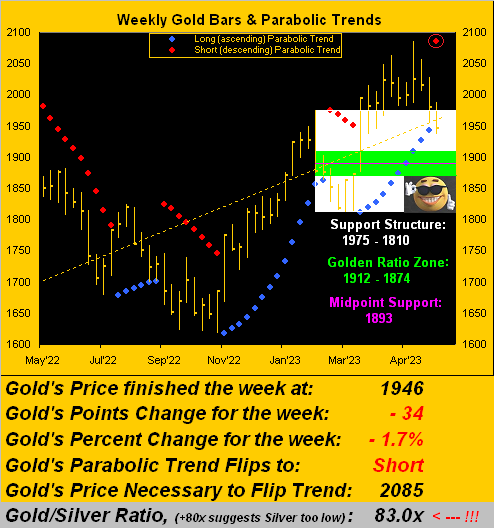

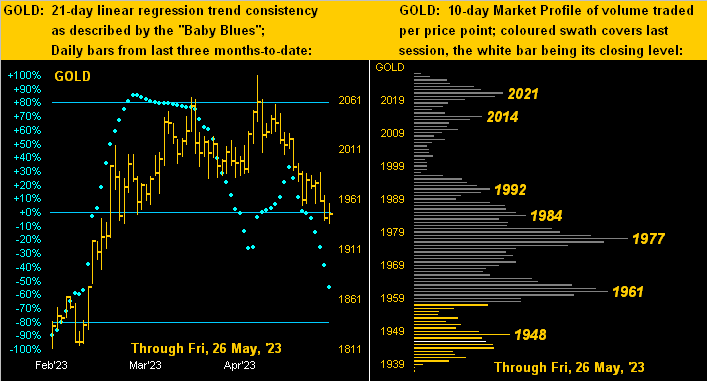

And thus the age old question again is asked: “How low doth Gold go?” Within the above graphic, the white area represents the most recently carved support structure for Gold, spanning from the 02 February high of 1975 down to the 28 February low of 1810. Therein, the green zone encompasses Golden Ratio support spanning from 1912 to 1874. That in turn is bisected by the purple midpoint support line at 1893 — a reasonable downside target — which is -53 points below Gold’s having settled out the week yesterday (Friday) at 1946.

More specific to the last 10 parabolic Short trends that extend back a full five years, be it by average, trimmed-mean, or median adversity, such vacuum suggests Gold reaching the 1852-1835 area. Whilst that still is inside the overall white support structure, our lean is that the 1893 purple line is the extent of adversity on this down run. On verra…

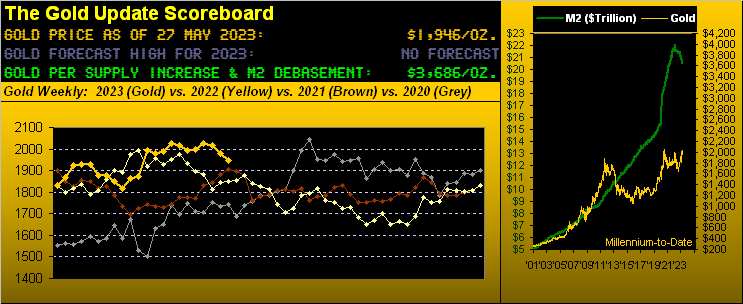

‘Course, that’s all technical. But as long as Gold continues to be kicked around as a commodity rather than as a currency, the technicals typically will out. Ultimately there remains the main fundamental: currency debasement. And by our opening Gold Scoreboard, we value Gold today at 3686, even accounting for the wee increase in the supply of Gold itself plus some shrinkage of late in the StateSide “M2” Money Supply.

“But mmb, Gold always rises to prior maximum debasement values, right?”

Exactly right there, Squire. Historically ’tis the case, however the lag time can be significant: the last such occurrence was per Gold’s still-standing All-Time High of 2089 on 07 August 2020, the debasement value for which was attained some eight years earlier during March 2012. Indeed as a charter reader of The Gold Update has quipped these many years: “Gold will make you old.” But ’twill also make you financially substantive.

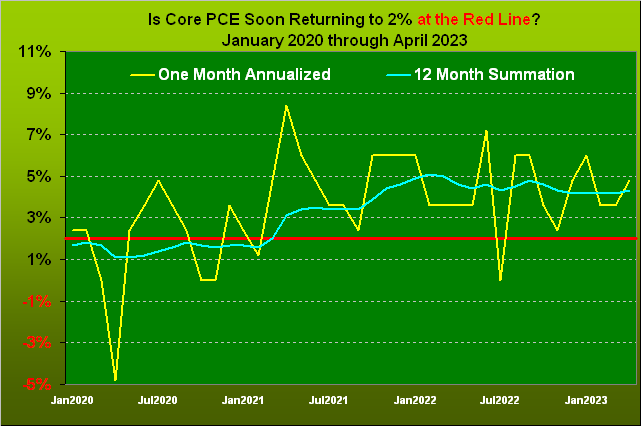

Speaking of substantive, such is the state of the Federal Reserve’s favoured inflation rate. As the Fed assumes that neither do you drive nor eat, it looks to push down Core Personal Consumption Expenditures to an annualized inflation pace of +2%. And the full-throat FinMedia buzz is that following another +0.25% FedFunds rate increase come the 14 June Open Market Committee’s Policy Statement, they shall then “pause”. Shall that produce enough “economic slowdown” to garner just +2% annualized Core PCE inflation? We don’t think so, per the following graphic: