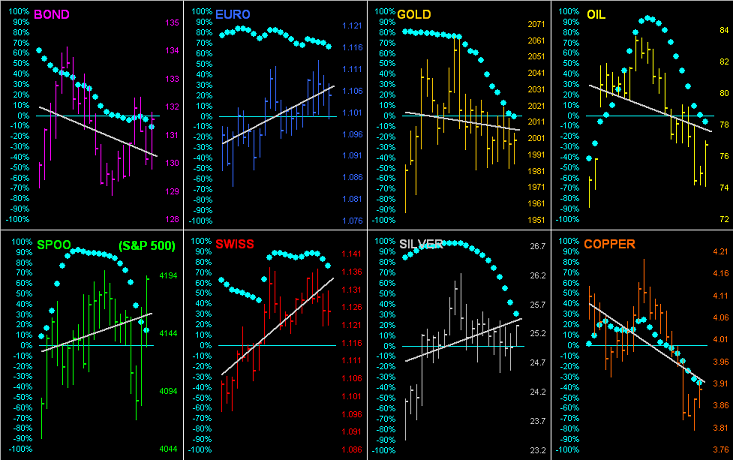

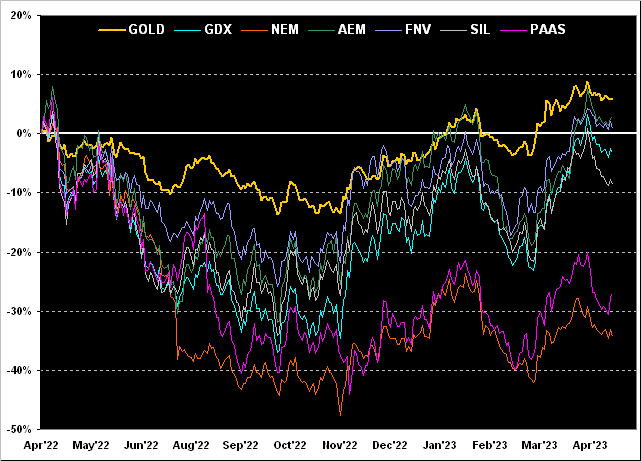

We’ve completed the year’s first trading quadrimestre (a little French lingo there). And just as we saw at March’s month-end, so too through April is Gold again sporting the highest year-to-date percentage BEGOS Markets vertex as the ![]() “The Leader of the Pack”

“The Leader of the Pack”![]() –[The Shangri-Las, ’64]:

–[The Shangri-Las, ’64]:

And contrary to conventional wisdom that Gold and the stock market are inversely correlated, barely off the pace is the S&P 500 in second place, with the reportedly “left for dead” U.S. 30-year Treasury Bond rounding out the podium.

Still, specific to the yellow metal through these last three missives inclusive, we continue to anticipate a new Gold All-Time High as nigh — albeit having fully expected en route some near-term retrenchment into the 1900s — which has been exactly the case thus far. (Note that per reader requests, recent editions of The Gold Update are now being archived on the website, such that you can look back to see what we’ve said).

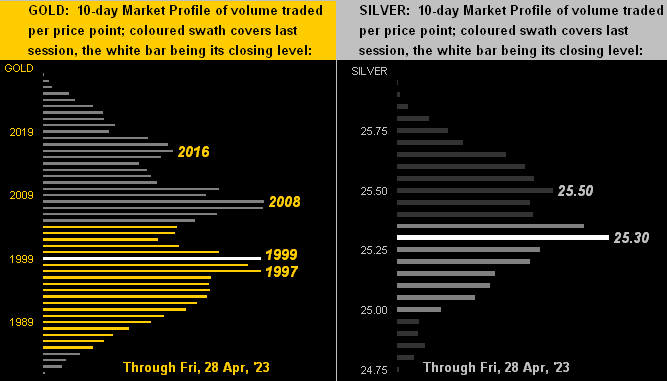

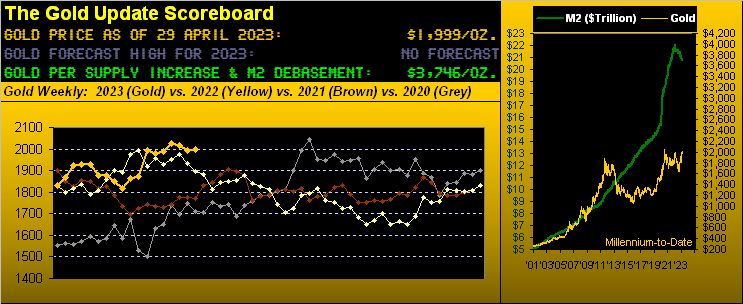

To be sure, in yesterday’s (Friday’s) settling of the week, (and month and quadrimestre) at ![]() “1999”

“1999” ![]() –[Prince, ’82], ’tis but a 90-point sprint to the present All-Time High (of 2089 back on 07 August 2020), which as herein detailed a week ago can happen in a heartbeat.

–[Prince, ’82], ’tis but a 90-point sprint to the present All-Time High (of 2089 back on 07 August 2020), which as herein detailed a week ago can happen in a heartbeat.

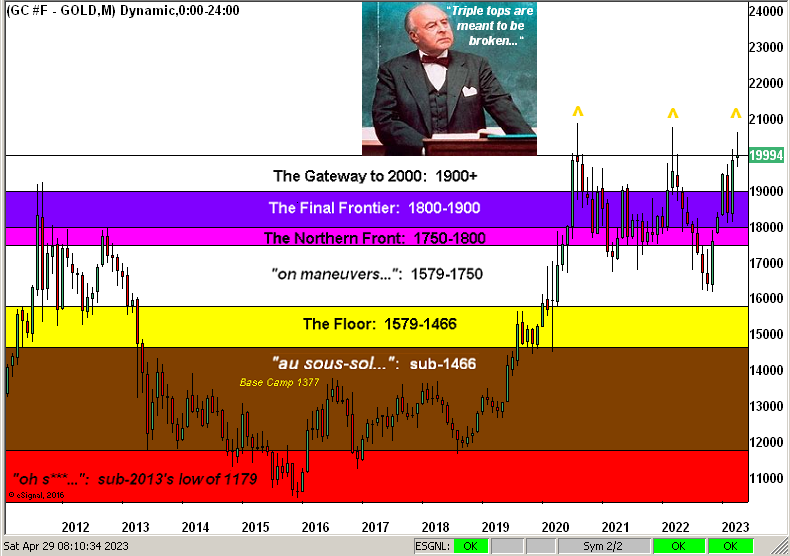

But in looking ahead toward Gold’s inevitably passing up through 2089, again we’re anticipating the mid-2100s come this July, given typical price gains during parabolic Long trends. The current one is represented by the rightmost ascending blue dots across Gold’s weekly bars from one year ago to date, (with the flip for the ensuing week still well out of range down there at 1890):

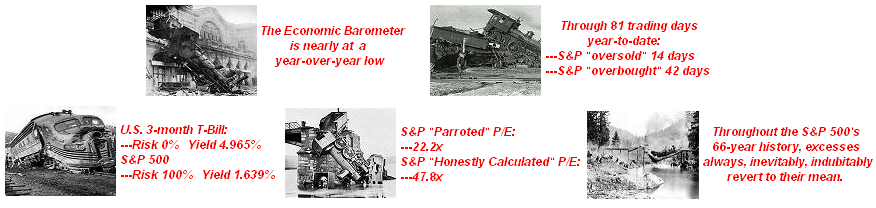

Talk about taking the wrong track … yet the stock market per our preferred measure of the S&P 500 (currently 4169) refuses to revert to rational valuation (sub-3000, at least). Indeed as Q1 Earnings Season continues to unfold, of the 249 constituents having reported, a full 40% have posted worse bottom lines than for Q1 of a year ago. Is it any wonder our “live” price/earnings ratio for the S&P remains in rarefied air at 47.8x up there? Recall Jerome Cohen’s writing that “…in bull markets the average level would be about 15 to 18 times earnings…” Still in today’s S&P there are 28 constituents with P/Es of 100x or greater … and hardly is this even a “bull market”. Let’s cue Dire Straits from back in ’85 with ![]() “Why Worry?”

“Why Worry?” ![]() After all, have a gander at the Economic Barometer:

After all, have a gander at the Economic Barometer: