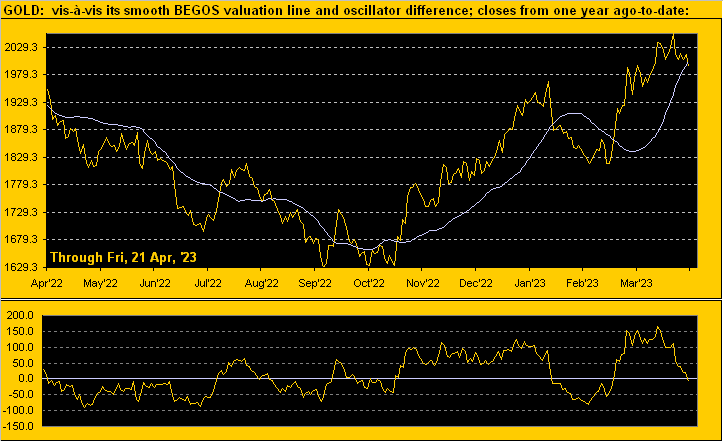

Such “El Plungo” by the Baro obviously elicits the “R” word. Recall the back-to-back StateSide negative Gross Domestic Product readings for Q1 and Q2 of 2022 as having “defined” a recession … which was met with a rising Q3 and Q4, (i.e. per the lowly convention wisdom level, “the recession ended as soon as it started”). And now come this Thursday (27 April) we’ve the first peek at Q1 GDP, consensus calling for +2.0% annualized growth, albeit weaker than the prior two quarterly readings respectively of +3.2% (Q3) and then +2.6% (Q4). ![]() “Slip Slidin’ Away” –[Paul Simon, ’77]

“Slip Slidin’ Away” –[Paul Simon, ’77] ![]()