‘Course, all the post-Fed excitement is over the stock market’s ![]() “Going to a Go-Go”

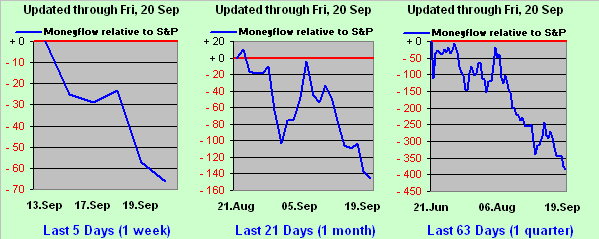

“Going to a Go-Go”![]() –[The Miracles, ’65]. But as we “X’d” (@deMeadvillePro) last evening, the MoneyFlow of the S&P 500 — as regressed into S&P points — is vastly underperforming the Index itself. Be it by the latest weekly, monthly, or quarterly measure, the euphoric buying to a record high (5734) is at best thin as we below see per one of our favourite market-leading indicators. We thus anticipate lower S&P levels near-term; after all, ’tis the first day of “fall”; (write it down):

–[The Miracles, ’65]. But as we “X’d” (@deMeadvillePro) last evening, the MoneyFlow of the S&P 500 — as regressed into S&P points — is vastly underperforming the Index itself. Be it by the latest weekly, monthly, or quarterly measure, the euphoric buying to a record high (5734) is at best thin as we below see per one of our favourite market-leading indicators. We thus anticipate lower S&P levels near-term; after all, ’tis the first day of “fall”; (write it down):

Having opened with the Fed, let’s close with same. Over here, financial friends with whom we spoke almost all agreed that the Fed’s rate cut would be -0.25% (as, in fact, voted FOMC member Michelle Bowman), although a case was made for -0.50%, if for no other reason than a shift from the prior 5.25%-5.50% target range to now 4.75%-5.00% wasn’t that material of a change, (whereas from say 1.50% to 1.00% would be quite significant). But again as earlier cited, should the economy be garnering some renewed strength with money now a bit easier by which to come, then shall inflation add to a higher sum? Better to not be a dumbo without Gold, but fly as Dumbo with that which you hold.

Which brings us to this cool view of Disney’s Dumbo 1/4oz. Gold coin:

Now that really is the only way to fly: Gold High!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro