Within Gold’s ongoing negative trend, be it by near-to-medium-term linear regression or by our weekly parabolics et alia, price this past Wednesday at 23:14 GMT posted a year-to-date low of 4046. At that instant, ’twas a net change in 2026 of -6.6%, even though “AI” (“Assembled Inaccuracy”) a week ago had stated that “Gold is having another incredible year.”

We love Gold for its inevitably higher — indeed far higher — levels; however price’s reality of trend, means reversion, and adherence to Fair Value regularly reminds us of present pricing reality. Pure and simple. (The S&P 500 faces that rude awakening, but we digress…)

Given such reality for Gold, we comprised this week’s title by hearkening back to the year 1894, (Gold then ’round $21/ounce). For then from these Mediterranean climes was registered one of the most time-honoured “immortal pillar” standards in musical history as penned and scored by the Neapolitan brothers Ernesto and Giambattista de Curtis: ![]() “Torna a Surriento”

“Torna a Surriento”![]() , which for you WestPalmBeachers down there is

, which for you WestPalmBeachers down there is ![]() “Return (or as on occasion is ascribed “Come Back”) to Sorrento”

“Return (or as on occasion is ascribed “Come Back”) to Sorrento” ![]() . ‘Tis since been modern-day crooned by many-a-star including Frankie (’51), Dino (’52) and Elvis (’61) … just in case you’re scoring at home. And in this case for The Gold Update, we’ve reverently revised it to

. ‘Tis since been modern-day crooned by many-a-star including Frankie (’51), Dino (’52) and Elvis (’61) … just in case you’re scoring at home. And in this case for The Gold Update, we’ve reverently revised it to ![]() “Return to Fair Value”

“Return to Fair Value”![]() .

.

“Because, mmb?”

Because, Squire, upon Gold reaching down to the aforementioned 4046, ’twas within one day’s expected daily trading range of tapping Fair Value at what is now 3949. True, price did not fully [yet] get there; however ’tis ultimately the “raison d’être” (a little French lingo there) of the “Means Reversion Dept.”

To be sure, Gold from 4046 instead bounced to as high as 4267 before settling the week yesterday (Friday) at 4240. But as the noted trends remain negative, price soon reaching down to Fair Value appears reasonable, Gold having just posted its lowest weekly close year-to-date and sixth down week of the last eight.

Not helping Gold is the Federal Reserve Open Market Committee’s having its knickers in a bit of a bunch. “To raise, or not to raise”, that is the question. Indubitably “yes”, albeit as previously written, we still sense the FOMC shan’t vote to raise the Bank’s Funds rate until their Policy Statement of 29 July, rather than so doing this next Wednesday (17 June), the intrigue of course as overseen by new FedHead Kevin “The Warrior” Warsh.

Were the war to wane between those two FOMC dates, (not to mention a “peace deal” possibly being signed at any moment), that could give the Fed some breathing room. But May’s inflation data already is rolling in, the headline Producer Price Index of +1.1% if annualized now +13.2%: Ouch! And ’twill tend to lead June’s Consumer Price Index. As for the “Fed-favoured” Personal Consumption Expenditures Index, its May reading shan’t be released until a week after this next FOMC gathering. But both the PPI and CPI are running sufficiently hot as to be well beyond (understatement) the Fed’s annualized target of +2.0%.

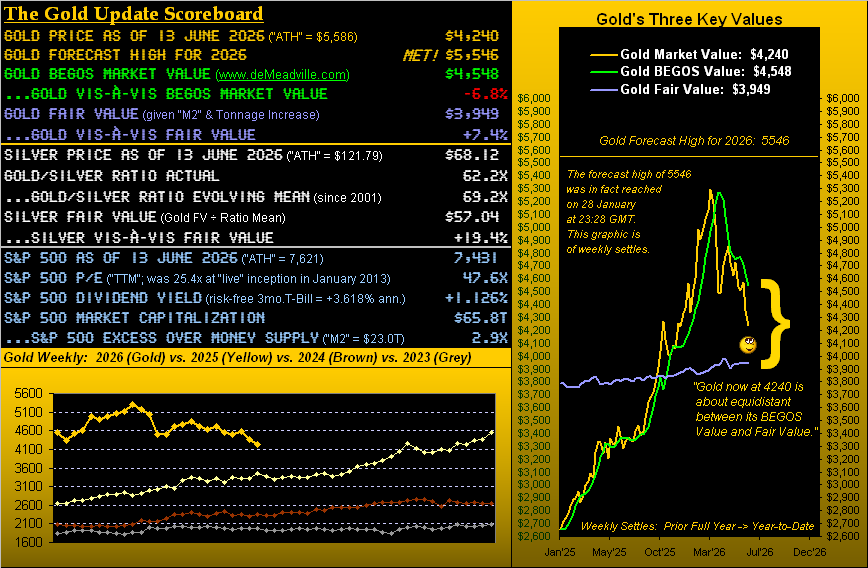

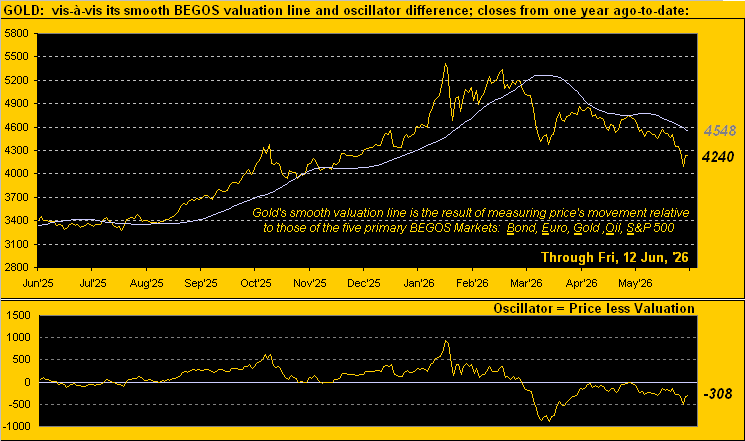

‘Tis thus a convenient period for Gold to return to Fair Value, above which (per the opening Scoreboard) price is presently +7.4% (+291 points) whilst nonetheless being -6.8% (-308 points) below its BEGOS Market Value, the latter as we see here year-over-year:

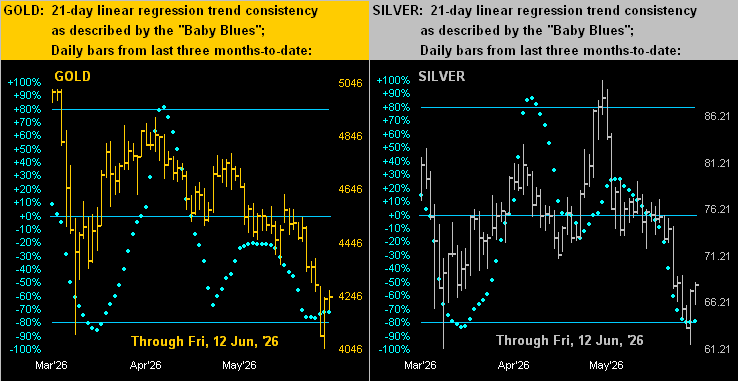

Note in the Baro’s lower-right corner the S&P 500’s price/earnings ratio having settled the week at 47.6x. Following Wednesday’s -1.6% demise, the mighty (albeit inanely overvalued) Index rebounded +2.3% through Friday. Despite that however, into week’s end the S&P futures’ 21-day linear regression trend rotated to negative for the first time since 10 April, thus reinforcing our sense that the Index remains in “correction” mode down into the 6800s (as herein laid out a week ago) … or further still should the Fed instead unexpectedly be proactive with a Funds rate raise on Wednesday. “Got stops?”

Toward wrapping with that, here first is the stack:

The Gold Stack (continuous contract pricing):

Gold’s All-Time Intra-Day High: 5586 (29 January 2026)

2026’s High: 5586 (29 January)

Gold’s All-Time Closing High: 5411 (28 January 2026)

The Weekly Parabolic Price to flip Long: 4988

Gold’s BEGOS Market Value (from our opening “Scoreboard”): 4548

10-Session “volume-weighted” average price magnet: 4337

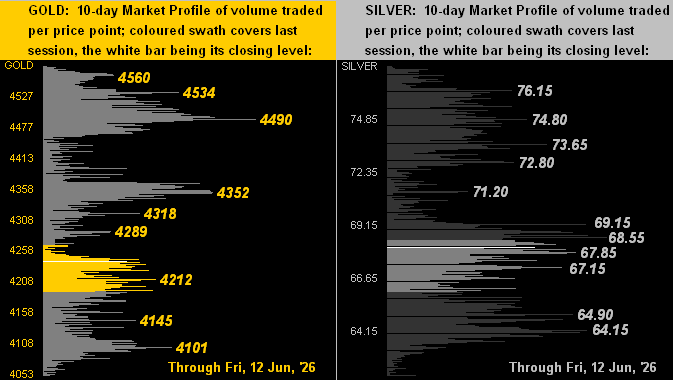

Trading Resistance: Market Profile notables: 4289 / 4318 / 4352 / 4490 / 4534 / 4560

Gold Currently: 4240, (expected daily trading range [“EDTR”]: 118 points)

Trading Support: per the Market Profile: 4212 / 4145 / 4101

The 300-Day Moving Average: 4070 and rising

10-Session directional range: down to 4046 (from 4577) = -531 points or -11.6%

2026’s Low: 4046 (11 May)

Gold’s Fair Value per Dollar Debasement, (from our opening “Scoreboard”): 3949

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

And so ’tis toward “Fed Day”, featuring for the first time “The Warrior” as aforementioned. And whilst the Chairman’s vote is but one of 12 comprising the FOMC, his follow-up presser most certainly shall find him in the “hot seat”, so to speak:

‘Course, we wish Warsh well.

But stay with your Gold for the long spell, as a return to Fair Value would not be farewell!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro