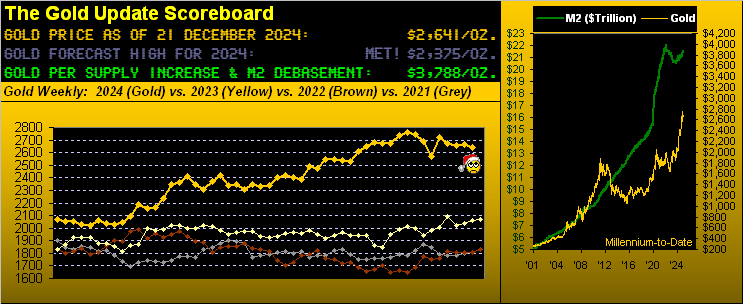

In turn challenged by it all, Gold is doing its darnedest to seek some charisma. Despite price’s rampant volatility, Gold settled the week at 2641, “net net” again being little changed as we’d seen the week prior. Two weeks ago, Gold traced 112 points for a net change of only +11; now this past week, Gold traced 87 points for a net change of only -25. Thus Gold’s net two-week change is but -14 points. Reprise Chris Isaak’s tune from back in ’95: ![]() “Goin’ Nowhere“

“Goin’ Nowhere“![]()

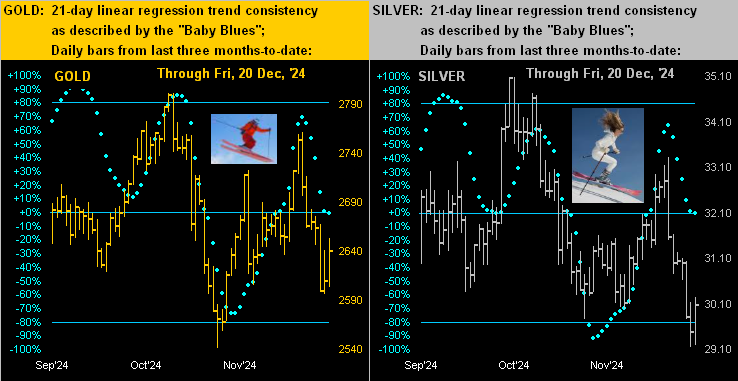

That warbled, Gold has wobbled on balance a bit lower within the context of its ongoing parabolic Short trend per the weekly bars as next shown from a year ago-to-date. Indeed, this past week’s low — 2597 — was the lowest level traded since 2569 back on 18 November. Further upon this Short parabolic trend’s commencement, you may recall our penned suggestion of “…Gold revisiting the upper 2400s on this run…” given the weekly MACD (moving average convergence divergence) also then having crossed to negative, which since has continued to deteriorate. Rather anti-charismatic, that. To the bars and rightmost red-dotted Short trend, now six weeks in duration:

Thus as we glide into winter and the first of two back-to-back abbreviated trading weeks, let’s assess the state of The Stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3788

Gold’s All-Time Intra-Day High: 2802 (30 October 2024)

2024’s High: 2802 (30 October 2024)

Gold’s All-Time Closing High: 2799 (30 October 2024)

The Weekly Parabolic Price to flip Long: 2777

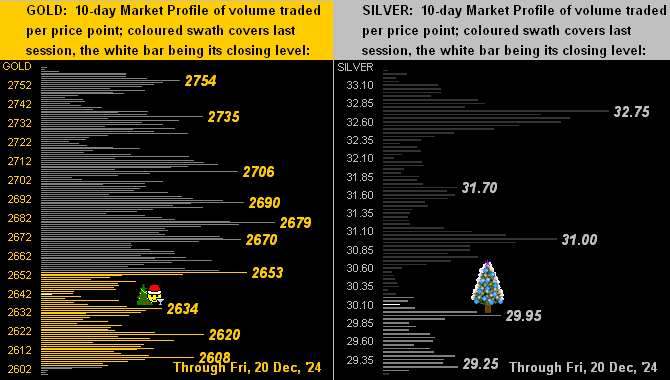

10-Session “volume-weighted” average price magnet: 2681

Trading Resistance: notable nearby Profile nodes 2653 / 2670 / 2679 / 2690

Gold Currently: 2641, (expected daily trading range [“EDTR”]: 44 points)

Trading Support: 2634 / 2620 / 2608

10-Session directional range: down to 2599 (from 2761) = -162 points or -5.9%

The 300-Day Moving Average: 2329 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

In sum, Gold whilst seeking some charisma at least technically still looks to falter a bit; but fundamentally as the late great Richard Russell would remind us, there’s never a bad time to buy it. This gem to wit, courtesy of The Royal Mint:

Indeed, Merry Everything to Everybody Everywhere and don’t forget the Gift of Gold!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro