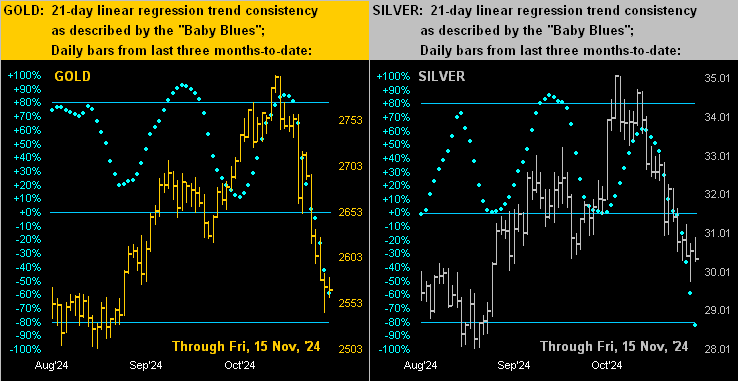

Further as noted, when the Buck gets the bids, “everything else” goes on the skids, including ‘natch the precious metals. ‘Tis not the happiest of two-panel displays, but here next are the last three months-to-date of daily bars for Gold on the left and for Silver on the right, along with their respective baby blue dots of trend consistency. Cue our lead (pun intended) conductor with ![]() “Follow the Blues instead of the news, else lose yer shoes…“

“Follow the Blues instead of the news, else lose yer shoes…“![]() :

:

And so to wrap, let’s go with The Stack:

The Gold Stack

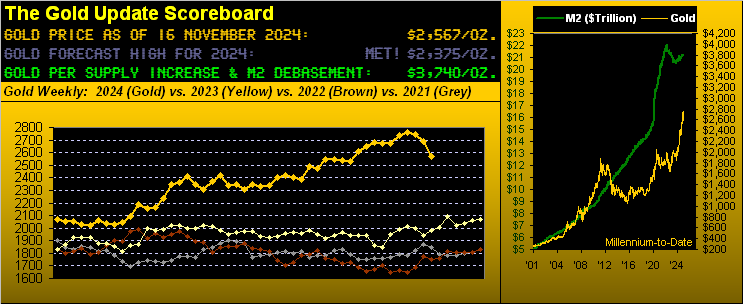

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3740

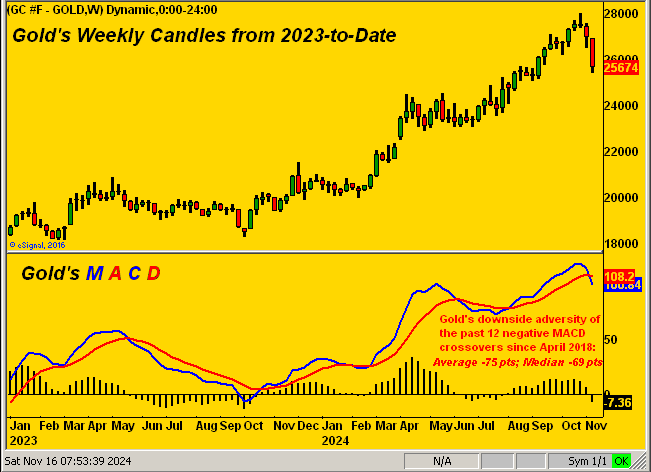

Gold’s All-Time Intra-Day High: 2802 (30 October 2024)

2024’s High: 2802 (30 October 2024)

The Weekly Parabolic Price to flip Long: 2802

Gold’s All-Time Closing High: 2799 (30 October 2024)

10-Session “volume-weighted” average price magnet: 2656

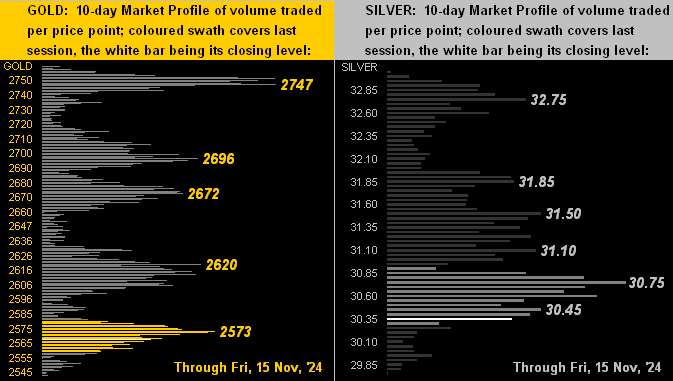

Trading Resistance: notable Profile nodes 2573 / 2620 / 2672 / 2696 / 2474

Gold Currently: 2567, (expected daily trading range [“EDTR”]: 43 points)

10-Session directional range: down to 2542 (from 2759) = -253 points or -7.9%

Trading Support: none notable per the Profile

The 300-Day Moving Average: 2268 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

‘Tis a fairly light, ensuing week for incoming Econ Baro metrics, the most attention-getting one to be the Conference Board’s compiled negative reading of October’s Leading Indicators, (which as led by the Baro we instead refer to as “Lagging”). Too, ’tis the final week of Q3 Earnings Season, which as you know (should you follow its page and/or read the Prescient Commentary) is sub-par compared to average quarterly year-over-year improvement. But as we’ve quite a bit quipped, earnings today are irrelevant to equities’ investing: else the S&P 500 would be at but half its current level.

Otherwise, notwithstanding some further near-term demise, Gold remains ever so cheap for the wise … the bottom line thus being:

Got Gold? Don’t be a chicken! Get yourself some real nuggets and win!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro