In fact, ’tis to laugh: with respect to the S&P’s taking a bit of a bath, recall this from last week’s missive? “…the Associated Press referred to the intra-week selling as a ‘wipeout’. Honestly … they … don’t know what a ‘wipeout’ is…” Well folks, the “somehow still surviving” CNN jumped on the same band wagon just this past week with (get ready): “Why the stock market is suddenly freaking out”. How’s that for journalistic professionalism? So the S&P’s weekly loss was -2.1%; (remember the first intra-day circuit breaker isn’t even instituted until -7%). Across the last 52 trading weeks (which for you WestPalmBeachers down there is since this time a year ago), the S&P 500 has actually recorded six worse weeks than that just past. “Who knew?” The FinMedia may be frantic over natural market pullback (remember that when stocks go down, so do viewership ratings); but we nonetheless offer this ad nauseam reprise: ![]() ““You ain’t seen nothing yet…” ”

““You ain’t seen nothing yet…” ”![]() –[BTO, ’74]).

–[BTO, ’74]).

Thus in seguing to that which very few are seeing, here is the Economic Barometer from one year ago-to-date along with the comparatively wee drop in the S&P. But as to the Econ Baro, of last week’s 15 incoming metrics, 11 were worse period-over-period, notably in the Payrolls arena:

To close, let’s briefly revisit the S&P 500. Hysteria aside, the mighty Index (whilst fundamentally hyper-overvalued) is now seven consecutive trading days “textbook oversold”. More importantly, should you make a brief trip to the MoneyFlow page, last week’s selling stint was actually not as negative by monetary outflow as was the change in the Index itself. (We tend to notice little things like that, especially as they generally lead price).

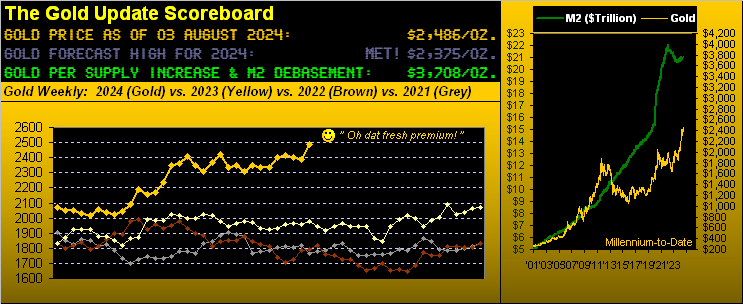

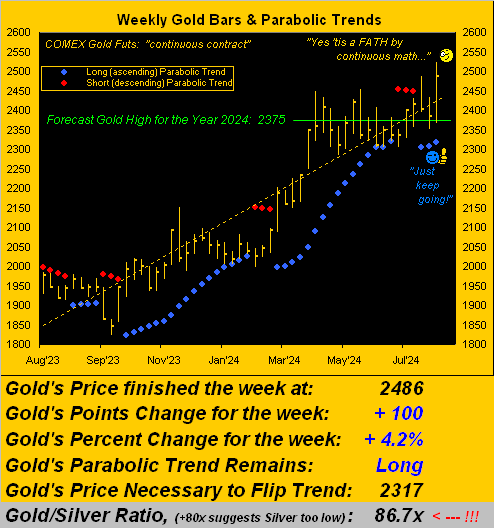

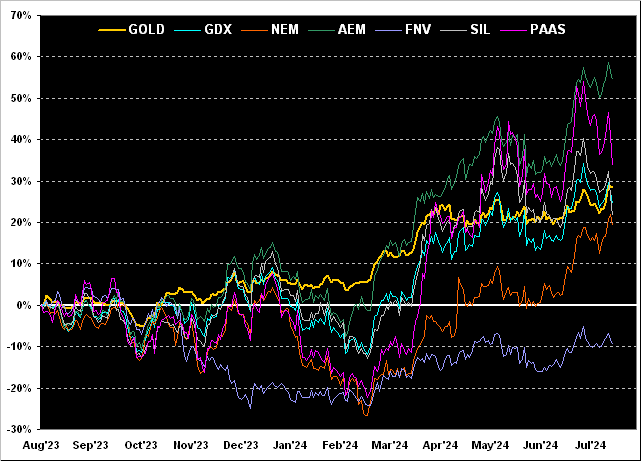

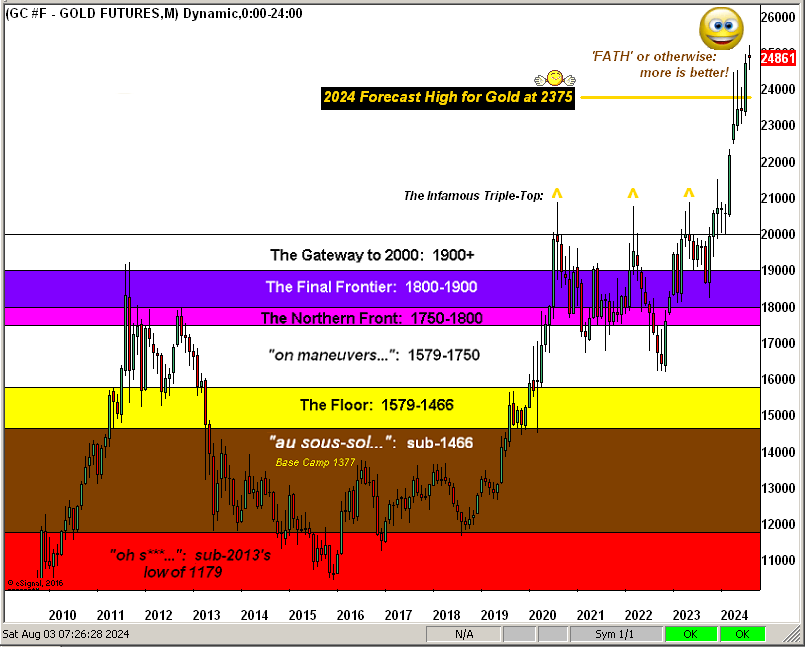

That noted, keep thy eyes upon the precious metals: for “FATH” or otherwise … (as crooned Alpheus back in ’07) … ![]() Keep the Gold Faith!

Keep the Gold Faith!![]()

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro