Now prior to our wrap ’round CRWD’s MSFT update trap, here next we’ve the stack:

The Gold Stack

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3715

Gold’s All-Time Intra-Day High: 2488 (17 July 2024)

2024’s High: 2488 (17 July 2024)

10-Session directional range: up to 2488 (from 2357) = +131 points or +5.6%

Gold’s All-Time Closing High: 2474 (16 July 2024)

10-Session “volume-weighted” average price magnet: 2420

Trading Resistance: notables per the Profile 2414 / 2420 / 2470 2341

Gold Currently: 2403, (expected daily trading range [“EDTR”]: 36 points)

Trading Support: notables per the Profile 2401 / 2387 / 2367

The Weekly Parabolic Price to flip Short: 2305

The 300-Day Moving Average: 2090 and rising

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Wrap warning: do not read the following whilst drinking, lest — in a fit of laughter — the liquid spout from your nose.

“Everybody everywhere” is aware of yesterday’s CrowdStrike security update that rendered useless many a Microsoft (et alia) platform. (Indeed we were directly affected, a trading algorithm firing off a S&P futures Short signal, but the code was unable to connect to the broker … ![]() ““Mama said there’ll be days like this” ”

““Mama said there’ll be days like this” ”![]() –[The Shirelles, ’61]).

–[The Shirelles, ’61]).

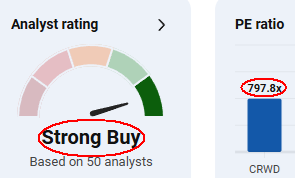

But to our point: shares of CRWD took an -11% Friday tumble. Yet when briefly visiting MSFT’s “Bing” search engine, it therein displayed for CRWD the following snippet, appropriately annotated with our red ink (put your glass down):

Honestly: who on earth pays $797 for something that earns $1? And yet ’tis a “Strong Buy”?? Is it any wonder we regularly refer to this as the Investing Age of Stoopid???

‘Tis immeasurably better to pay 2403 for something worth (by our opening Scoreboard) 3715: GOLD!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro