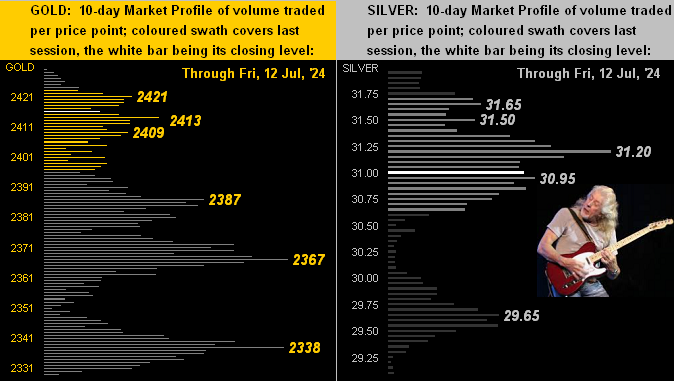

Too, we have the dual-panel display for Gold’s 10-day Market Profile (below left) and that for Silver (below right). The yellow metal’s two nearby volume support prices are 2387 and 2367 as labeled, whilst for the white metal, although 29.65 would seem safe, getting back above 31.20 — her most commonly traded price of the past fortnight — would allow for more upside ![]() ““Room to Move” ”

““Room to Move” ”![]() –[John Mayall, ’69]:

–[John Mayall, ’69]:

Now to wrap ahead of 14 incoming metrics due next week for the Econ Baro, we (being from a media family) are reminded that one’s choice of news source doesn’t necessarily convey truth. Recall above we alluded to inflation as “having been tamed in June”. Oh to be sure, at the retail level, June’s headline Consumer Price Index was a deflationary -0.1% pace, its first negative reading since that from the COVID Spring (double entendre) in 2020. However: ’twas a different story for wholesale inflation, the headline Producer Price Index rising from a pre-revised -0.2% pace in May to June’s +0.2%. “Whoopsie…” True, the PPI is more erratic than the CPI; but the former does have a leading tendency over the latter. Anyhooo, to our media point with these two quotes:

- Hat-tip Dow Jones Newswires: “Wholesale prices tame in June, PPI finds, and also point to lower inflation”;

- Hat-tip Breitbart Business Digest: “Producer inflation surges much higher than expected; Core inflation hits worst level in a year”.

To the second quote, before you say “No way!”, let’s once again do the math: the 12-month summation of Core PPI through June is at its highest level (+2.6%) in 14 months.

“Well that wasn’t on the TV, mmb…“

Squire, we wouldn’t know, having abandoned FinTV long ago. Either way, let’s cue for our parroting FinMedia colleagues some wisdom from the eternally-iconic Charles M. Schultz:

Whilst at the end of the day the media’s life-blood is advertising revenue, when it comes to your wealth management: do the math determinative and keep Gold in the affirmative!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro