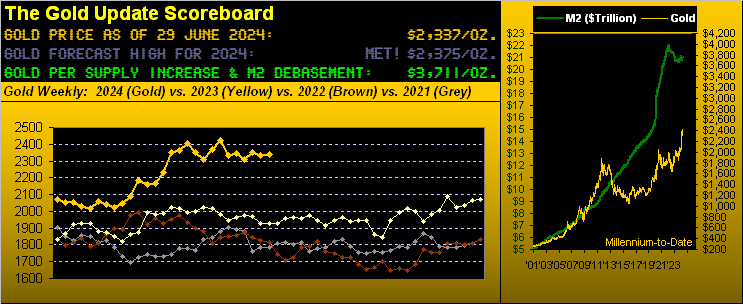

“And so we are halfway.” In this case ’tis not Fräulein Irma Bunt to James Bond (in the guise of Sir Hilary Bray) whilst walking upon the snowy flanks of Switzerland’s Schilthorn –[O.H.M.S.S, UA, ’69], but rather for our purposes the mid-point of 2024’s trading year. (Yes, we are aware that the precise mid-point is not until this Tuesday’s settle when with 126 trading days in the books there’ll remain 126 in the balance). Nonetheless, ’tis the end of June and thus time for our monthly view of it all.

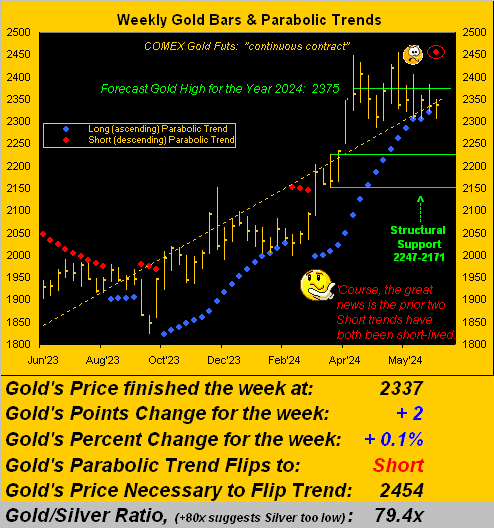

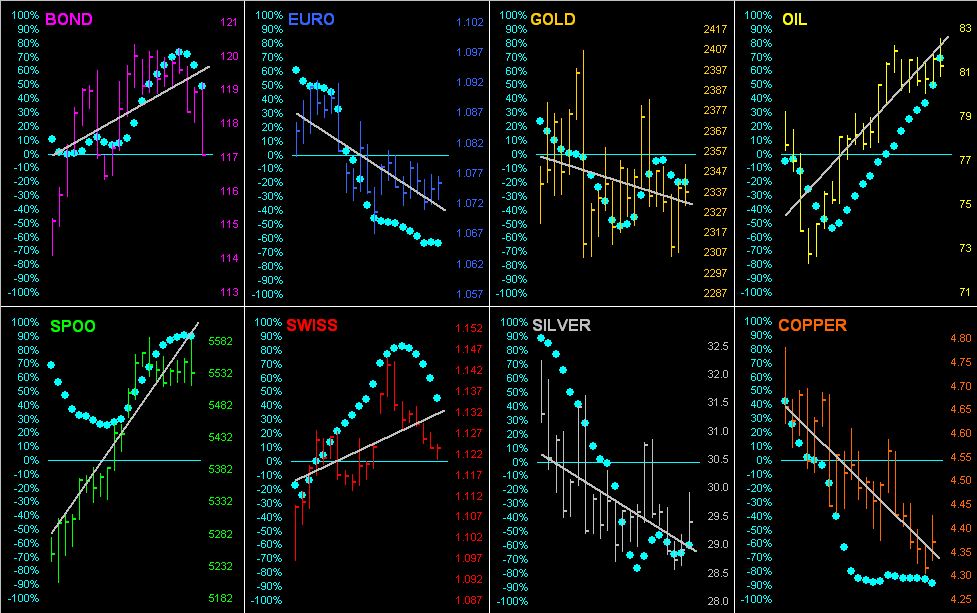

And bang on time in stride with our negative near-term bent for Gold — whilst settling yesterday (Friday) at 2337 for a whopping weekly gain of +2 points — on Wednesday, Gold’s anticipated damage was done as price broke below 2320 such as to flip our key 16-week parabolic Long trend now to Short. (Expected as ’twas, ’twasn’t a beautiful thAng, even as we then “X’d” [@deMeadvillePro] notice of said flip). Regardless, as scored by Chicago back in ’69: ![]() ““Where do we go from here?” ”

““Where do we go from here?” ”![]()

‘Course, you regular readers already know the answer to our musical query. For waiting in the wings as herein depicted via recent missives is Gold’s 2247-2171 structural support zone. Below ’tis with the weekly bars from a year ago-to-date. And encircled therein is the rightmost red dot heralding the start of the new parabolic Short trend:

Specific to the Econ Baro, ’twasn’t all bleak last week. The Chicago Purchasing Managers’ Index for June — whilst still in net contraction for 21 of the past 22 months — nonetheless improved to 47.4, its best reading since that for November of last year; (yet a reading below 50 still signifies manufacturing contraction). Too, Personal Income for May increased +0.5%, tying it for the second-best increase across the past 12 months. But is that inflationary, (nudge-nudge, hint-hint, wink-wink, elbow-elbow…)

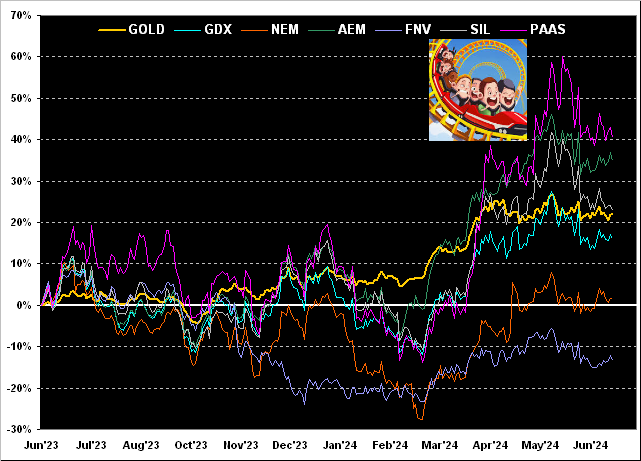

Hardly inflationary has been Silver’s rise to the top of our BEGOS Market Standings year-to-date. Best of the bunch as she is, Sister Silver remains cheap! The Gold/Silver ratio is now 79.4x: but the century-to-date average is 68.3x; were Silver thus priced by that yardstick today (just in case you’re scoring at home), rather than being now at 29.44, she’d be +16% higher at 34.22.

Then in second spot lies (appropriate verb there) the S&P 500, its being purely herd driven on Investing Age of Stoopid delusion. Cue that recorded in 1929 by Memphis Minnie and Kansas Joe McCoy: ![]() ““When the Levee Breaks” ”

““When the Levee Breaks” ”![]() Remember what also happened that year? When the “Look Ma! No Money!” crash hits, ’twill be pure herd fear, whilst Silver and Gold are held dear:

Remember what also happened that year? When the “Look Ma! No Money!” crash hits, ’twill be pure herd fear, whilst Silver and Gold are held dear:

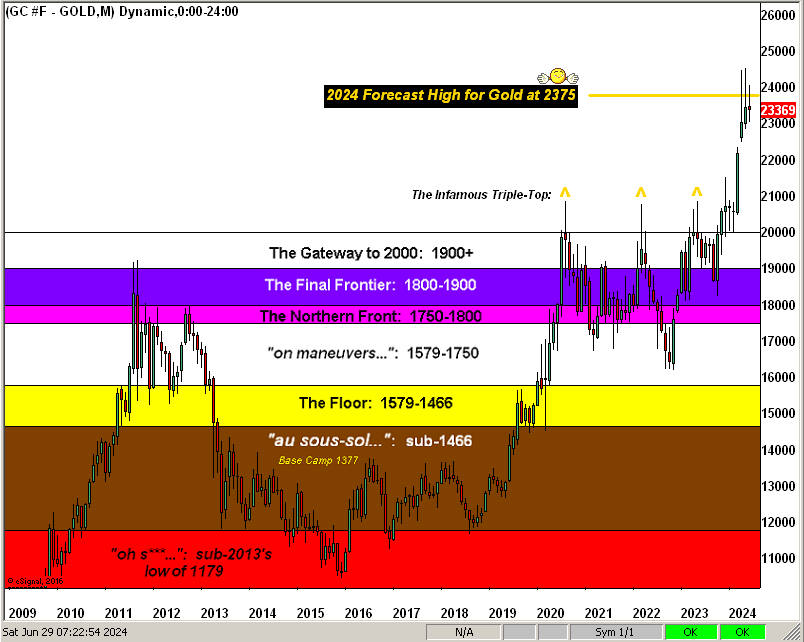

Thus with half the year gone, in the proverbial nutshell: Gold broadly looks great to go, but near-term technicals initially say no. Either way, we’ll see what shows. Indeed, how much Gold have you got stowed?

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro