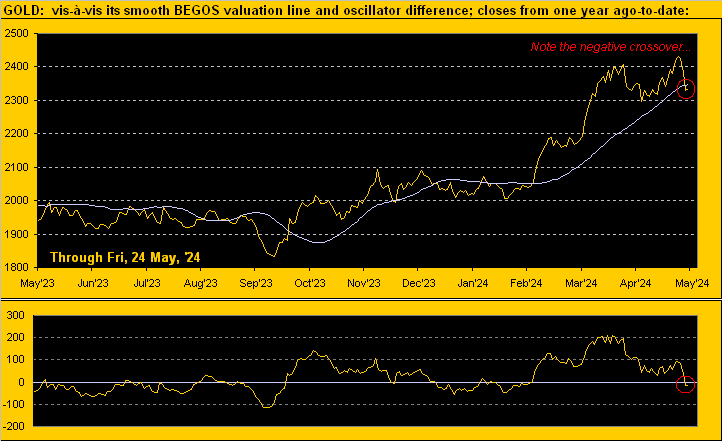

Our takeaway is: ‘twould be folly not to anticipate lower Gold prices near-term. In addition to price having just crossed beneath the aforeshown smooth valuation line, we’ve the following technical negatives: Gold’s daily Parabolics flipped from Long to Short effective yesterday’s open as did the MACD (moving average convergence divergence); the daily Price Oscillator is dwindling and the Moneyflow is nearing a cross from inflow to outflow.

Still, with prudent cash management always paramount — and acknowledging that “shorting Gold is a bad idea” — let’s wrap with the stack:

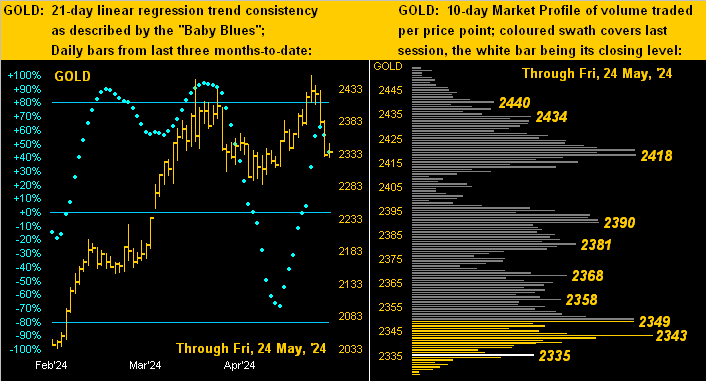

The Gold Stack

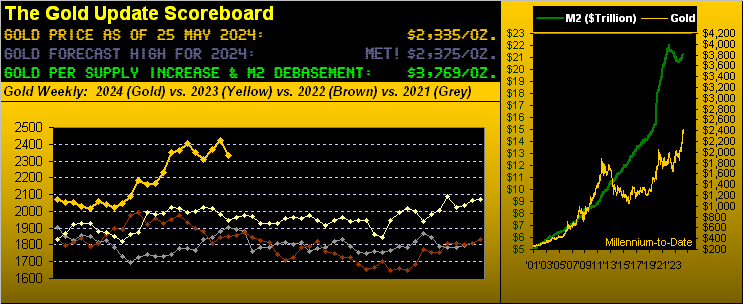

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3769

Gold’s All-Time Intra-Day High: 2454 (20 May 2024)

2024’s High: 2454 (20 May 2024)

Gold’s All-Time Closing High: 2430 (20 May 2024)

10-Session “volume-weighted” average price magnet: 2385

Trading Resistance: various per the Profile from here at 2335 up to 2440

Gold Currently: 2335, (expected daily trading range [“EDTR”]: 38 points)

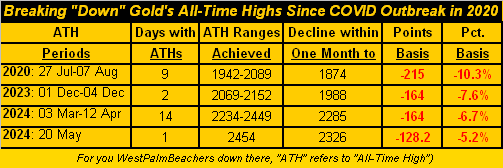

10-Session directional range: down to 2326 (from 2454) = -128 points or -5.2%

Trading Support: none per the Profile

The Weekly Parabolic Price to flip Short: 2263

Structural Support: 2247-2171

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar’22); 2085 (04 May ’23)

The 300-Day Moving Average: 2046 and rising

2024’s Low: 1996 (14 February)

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

‘Course the bottom line is, regardless of its marginal high but then habitual cry, don’t miss out when Gold goes to the sky!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro