We’ve penned it before, so let’s pen it again:

“Gold when technically overbought [as clearly now ’tis] might actually be considered a good thing … [as] great bull markets (or the resumption thereof) do breakout as such.”

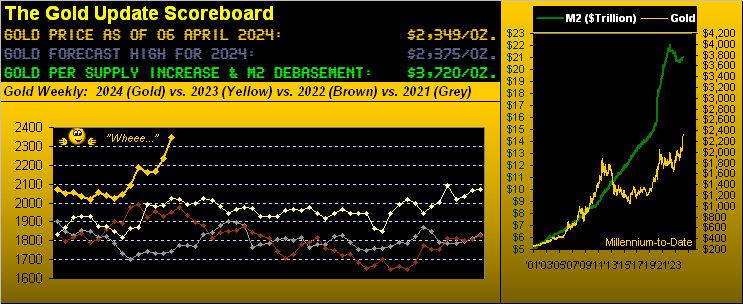

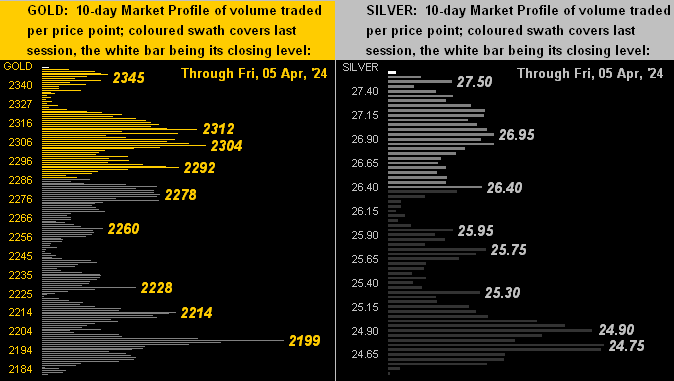

That quintessentially describes the nature of Gold’s price over the past five weeks. And the Gold bid is substantive: the combined COMEX trading volume of Gold from 04 March-to-date is the largest for any five-week stint since the world balked at COVID in 2020. Back then, the price of the yellow metal after having settled the prior year of 2019 at 1550, powered up to 2089 come 07 August 2020, a nearly +35% increase in 152 trading days: that All-Time High then remained in place until ’twas eclipsed more than three years later this past 27 December.

Moreover, Gold’s June contract settled yesterday (Friday) at 2349 inclusive of an intraday 2350 All-Time High, just 25 points shy of our predicted 2375 high for the entirety of this year. Further, Gold’s “expected daily trading range” (EDTR) is now 35 points: so priced today at 2349, Gold is within a day’s range of reaching our 2375 target. (Yes there are some +20 points of eroding premium in Gold’s futures price, but again given the EDTR is 35 points, such excess is at best noise).

“And it’s not too late to buy, right mmb?“

Actually, Squire, in the broader picture — especially as “under-owned” as remains Gold — hardly is it late: rather, ‘tis still early! We only mention this to dispel any investor concerns of having “missed the move” as Gold has still so far up to go. Oh to be sure, ‘twould be untoward technically for Gold not to pullback near-term; but fundamentally Gold remains extraordinarily inexpensive relative to U.S. Dollar debasement, such valuation by our opening Scoreboard now 3720.

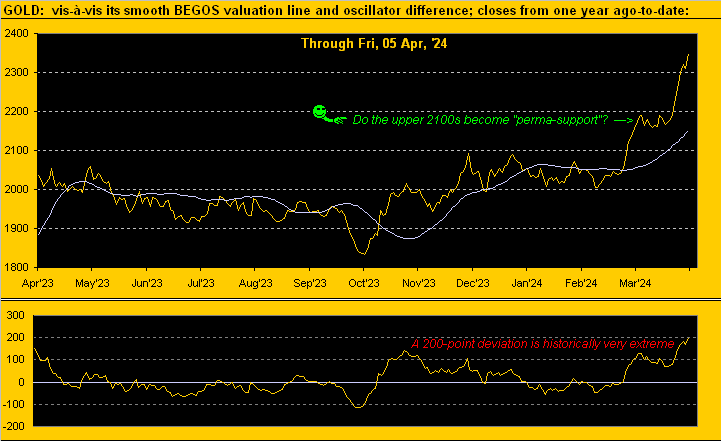

The key point here is: Gold finally and rightly is getting repriced to a somewhat more reasonable level, albeit still well below said Scoreboard valuation. Again, that is broad-term. As for near-term, our 2375 looks ripe for the taking; indeed you may remember our couching that level as “conservative” when we first made the call; (see via the website The Gold Update from last 30 December, entitled “Gold – We Conservatively Forecast 2375 for 2024’s High”). And now year-to-date, Gold is +13.4%. As for year-over-year, ’tis +15.3% in turning to price’s weekly bars from 05 April a year ago, the rightmost blue-dotted parabolic Long trend now increasing its upside acceleration: