Towards the wrap, here’s The Gold Stack:

The Gold Stack

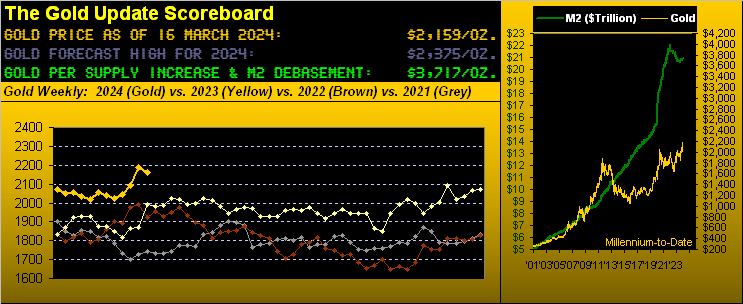

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3717

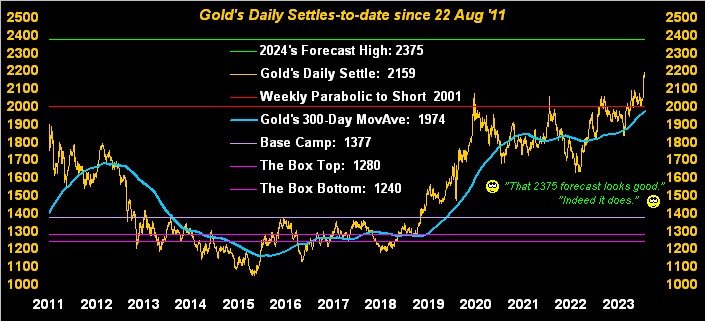

Gold’s All-Time Intra-Day High: 2203 (08 March 2024)

2024’s High: 2203 (08 March)

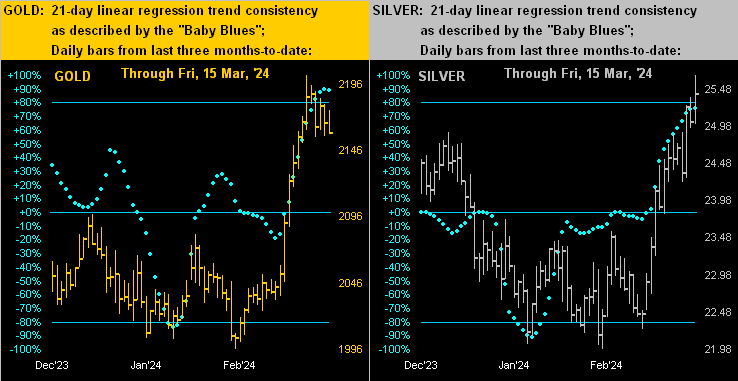

10-Session directional range: up to 2203 (from 2088) = +115 points or +5.5%

Gold’s All-Time Closing High: 2189 (11 March 2024)

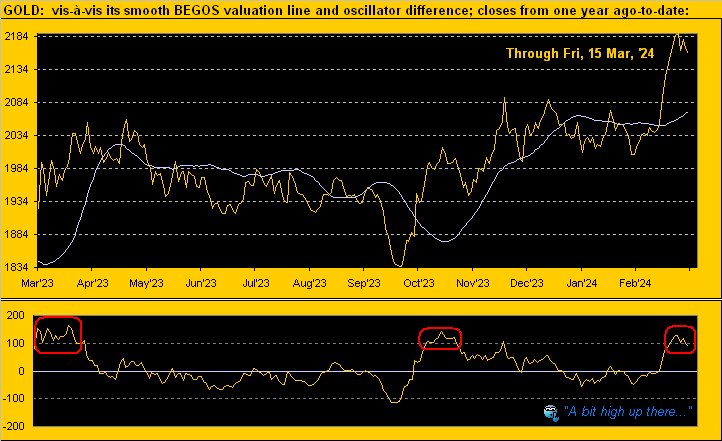

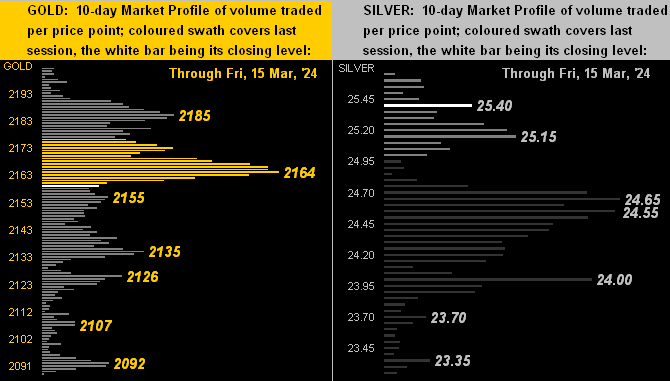

Trading Resistance: 2185 / 2164

Gold Currently: 2159, (expected daily trading range [“EDTR”]: 26 points)

10-Session “volume-weighted” average price magnet: 2157

Trading Support: 2155 / 2135 / 2126 / 2107 / 2092

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar ’22); 2085 (04 May ’23)

The Weekly Parabolic Price to flip Short: 2001

2024’s Low: 1996 (14 February)

The 300-Day Moving Average: 1974 and rising

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

‘Tis a fairly quiet week ahead for incoming Econ Baro metrics: just seven are scheduled, four of which relate to Housing. Still as cited, The Main Event is Wednesday’s FOMC “maintain the target range” decision. But in and amongst the Statement, Powell Presser and FedSpeak, might the phrase “rate increase” slip out … just as a little future possibility? Quel drame, mes amis…

Either way, with Gold paused per its detinue, consider adding more to your metals’ milieu!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro