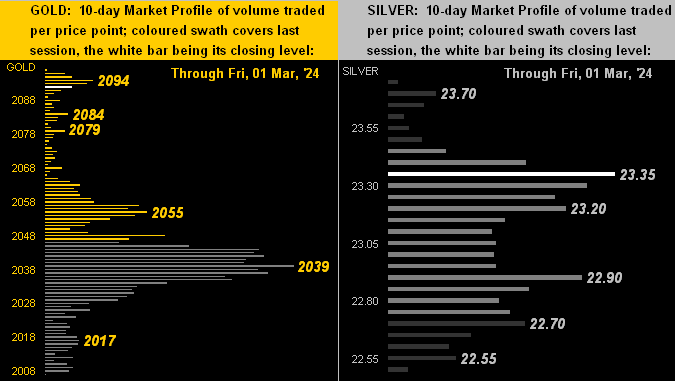

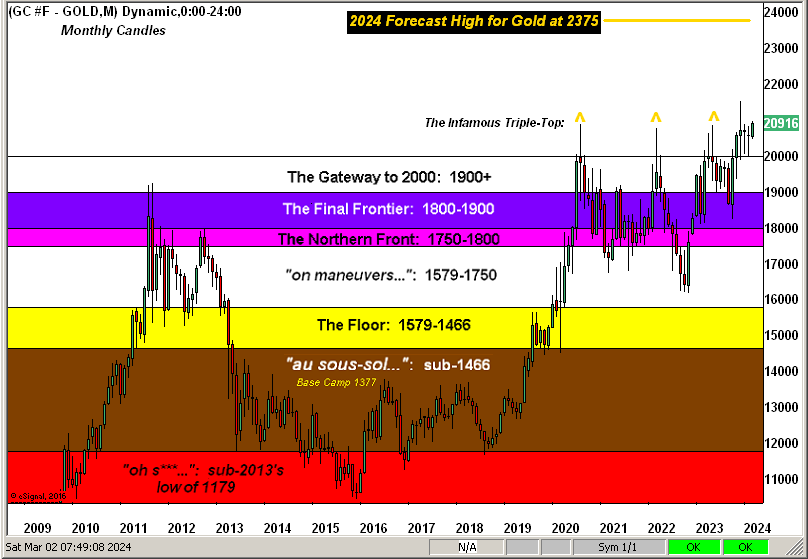

A bold title to head this recital, Gold on Friday posting its best low-to-high intraday gain (+2.4% or +50 points) since 13 December toward settling the week at 2092, essentially tying its highest-ever weekly closing price (with that recorded this past 01 December). To maintain perspective, Gold’s All-Time High remains 2152 (per last 04 December).

Credit Gold’s Friday flight with our Economic Barometer consumed by blight. Straightaway as the incoming metrics low-lighted economic decay, no sooner had we posted the Econ Baro just after the 16:00 (CET) barrage of negative data that Gold got the bid, the FinMedia in full throat for the Federal Reserve to cut rates. But as to inflation: ’tis going the wrong way!

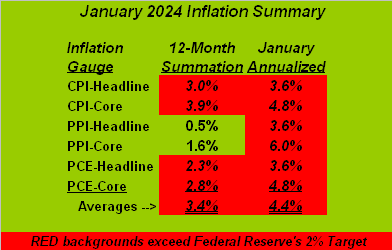

So as succinctly set out in his 2008 tome “When Markets Collide”, one Mohamed El-Erian writes of stagflation as “a situation characterized by disappointingly low economic growth and high inflation.” Is such situation suddenly starting? From our bold title, let’s get straight to two bold graphics: first the economy and second inflation.

1) The Economic Barometer: just as ’twas all going great for the StateSide economy, the FinMedia consistently reminding us of the successes in having embraced Bidenomics, what just happened? In turning below to the Econ Baro from one year-ago-to-date, that rightmost vertical drop is its second-worst six trading-day plunge since this time a year ago. Should such reversal of fortune continue to work its way into the data for computing Gross Domestic Product, that’ll be El-Erian’s “disappointingly low economic growth” … ![]() “Whoomp! There it is!””

“Whoomp! There it is!””![]()

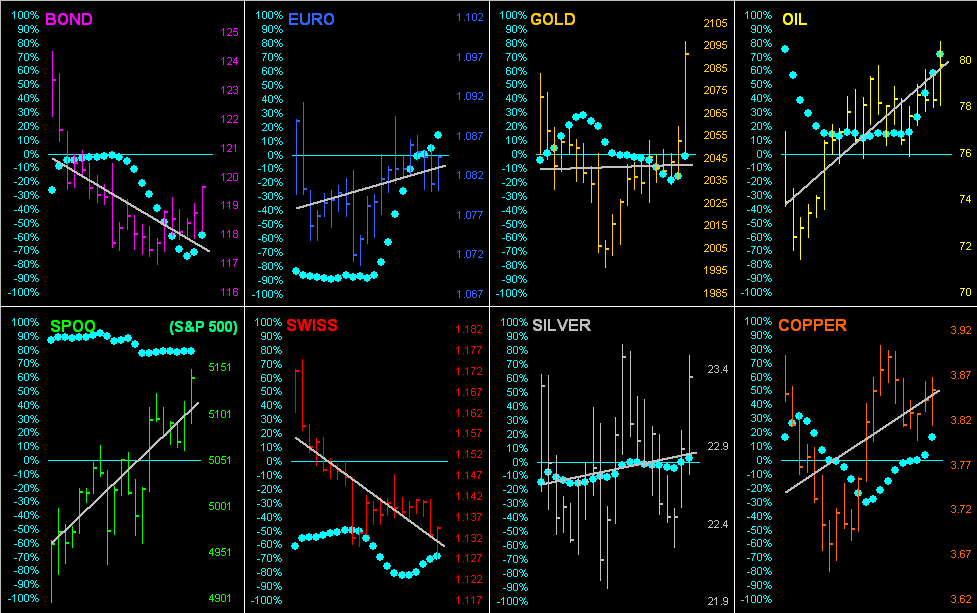

As for 2024’s brief stint year-to-date, despite Gold’s Friday upstate, price so far hasn’t done that great. For in turning to the BEGOS Markets Standings to this point of the year, Gold is up but a wee +1.0%, (even as the Dollar Index is +2.8%, but as you know, Gold plays no currency favourites). Topping the podium at present is Oil, +11.9% followed by the “Casino 500” +7.7%. Indeed specific to the S&P, through the first 42 trading days of this year, that +7.7% gain ranks second only to 2019’s stint (+11.4%) across the same number of days. But there’s a glaring difference between ![]() “Now and Then””

“Now and Then””![]() –[The BeaTles, ’23]. Then the “live” price earnings ratio of the S&P 500 was 30.6x (yield 2.054%). Now ’tis 46.5x (yield 1.400%.). Three-month risk-free dough then? 2.375%. And now? 5.215%. Yet you’re still in the stock market? Sheer guts. Regardless, as the fuse burns off, let’s get to the Standings before the whole thing blows up:

–[The BeaTles, ’23]. Then the “live” price earnings ratio of the S&P 500 was 30.6x (yield 2.054%). Now ’tis 46.5x (yield 1.400%.). Three-month risk-free dough then? 2.375%. And now? 5.215%. Yet you’re still in the stock market? Sheer guts. Regardless, as the fuse burns off, let’s get to the Standings before the whole thing blows up:

To sum it all up for this week, we’ve emphasized the Fed having to face what appears as the early machinations of a stagflating economy, a “damned if they do, damned if they don’t” scenario. Despite all the FinMedia blather about inflation being tamed — given we instead do the math — ’tisn’t. Our puke-green table with the red 2.0% overages ought be on every news desk in the nation and ’round the world. (But as is sadly typical, the truth wrecks the narrative). And as for the suddenly slipping economy, 13 metrics hit the Econ Baro next week, of which just five “by consensus” are supposed to show period-over-period improvement.

Thus as the cost to survive goes on the rise whilst that upon which you rely slips by, ’tis probably a good idea to have a little Gold! Or a lot of Gold!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro