The Gold Update by Mark Mead Baillie — 745th Edition — Monte-Carlo — 24 February 2024 (published each Saturday) — www.deMeadville.com

“Gold – Short n’ Sweet“

Valued readers ’round the world: today is our fifth day as beset with a nasty flu. So this edition (no. 745) is one of our most minimal missives extending as far back as 21 November 2009 (no. 1). But having never missed a single solitary Saturday, we’ll be damned if some viral bug is going to pull our streak’s plug. (Or as someone quipped years ago: “Ya don’t mess with the mmb.”)

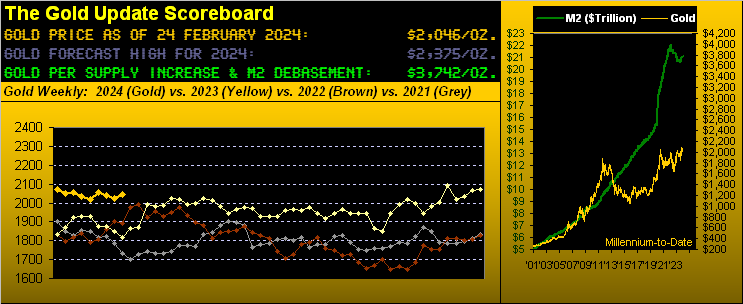

So here we go with “Gold – Short n’ Sweet“. We’ve just a few of our core foundational graphics, albeit without the usual annotating. “Short” in this case is a double entendre for the missive’s brevity, but moreover a reminder that Gold’s weekly parabolic trend a week ago flipped from Long to Short. “Sweet” in this case is that Gold hasn’t succumbed a wit to such new Short trend, price having settled yesterday (Friday) at 2046, the +1.0% net weekly gain being second-best through the young year’s eight weeks-to-date. Still, we continue to look for Gold to work lower, protected more broadly by the 2020-1936 structural support zone. You can refer back to last week’s piece (no. 744) as to how low may be low. Meanwhile, here are the weekly bars from one year ago-to-date:

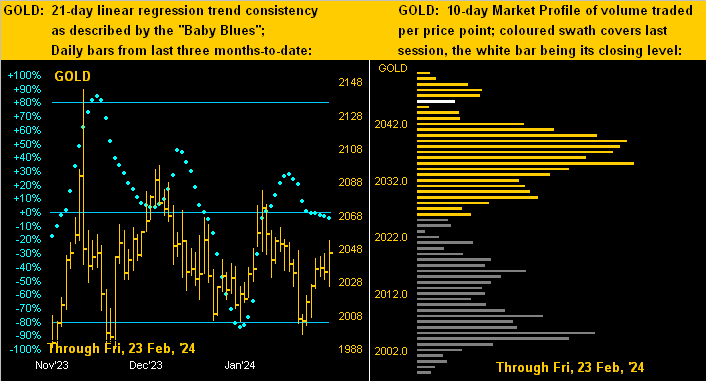

Next we’ve Gold’s two-panel graphic featuring the daily bars from three months ago-to-date on the left, and 10-day Market Profile on the right. Clearly Gold’s baby blue dots of trend consistency are directionally neutral, whereas the Profile suggests trading support in the 2030s, (but we’re not holding our breath):

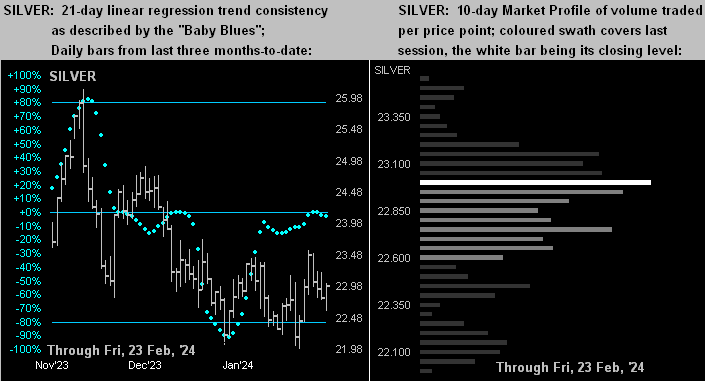

And of course for Silver we’ve same, her “Baby Blues” (below left) having gone completely stagnant. Sister Silver settled the week at 22.98, the Profile’s (below right) white bar being 23.00 and representing the most commonly-traded price of the past two weeks.

As for the Economic Barometer, ’twas a very quiet week: just three incoming metrics were recorded. Not to worry: next week has 14 metrics scheduled including the “Fed-favoured” inflation gauge of Core Personal Consumption Expenditures Prices. And the consensus estimate for January’s pace (+0.4%) is double that recorded for December (+0.2%). Here’s the Baro:

To close, these three notes.

■ You regular readers will recall that in this year’s first Gold Update (some seven weeks ago) we “contrarily” put forth the notion (not a prediction) that the Fed perhaps shall have to continue raising rates. No, we were not maligned, made fun of, nor impugned; but at that time, all the talk was as to when the Fed would begin cutting rates because ’twas so obvious they’d have to so do. Really?Do the math, just as we graphically herein detailed a week ago. Well guess what suddenly came to the fore this past Tuesday. Ready?Bloomy: “Markets Start to Speculate if the Next Fed Move is Up, not Down.”Dow Jones Newswires: “Traders are flirting with the idea of a Fed Rate Hike as January Meeting Minutes Loom.” You see, if we just sweep around them, they eventually catch up.

■Next week is the grande finale to Q4 Earnings Season. And given the relentless rise in the S&P 500, it must be one of the best Earnings Seasons ever, right? Wrong. For the S&P 500, the average number of constituents improving year-over-year is typically 66%. This Earnings Season? Just 60%. ‘Tis why the “live” P/E of the S&P is stuck up in the stoopidsphere at 46.3x

■Brief as we are today, don’t overlook the website’s other market-leading pages, notably for both Gold and Silver!