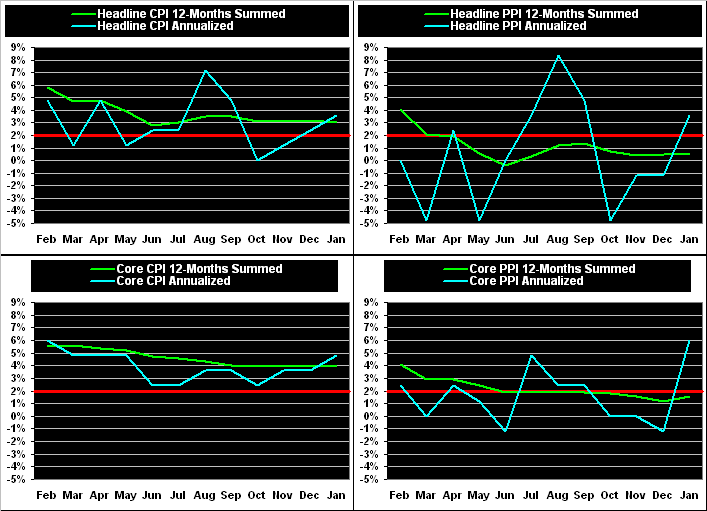

We’ll close with this absurd deception from the rather desperate “It’s All Good!” FinMedia. (Ensure you’re not sipping your favourite beverage, lest it spew from your nose given uncontrollable laughter). Following Tuesday’s release of renewed retail inflation per the CPI, floundering CNN Business ran with this headline, (put your glass down…): “Good News for Americans: Inflation cooled back down in January”. Again, the CPI’s pace increased from +0.2% in December to +0.3%, and its core reading from +0.3% to 0.4%. Cool, baby.

Cheers! (And don’t forget the Gold!)

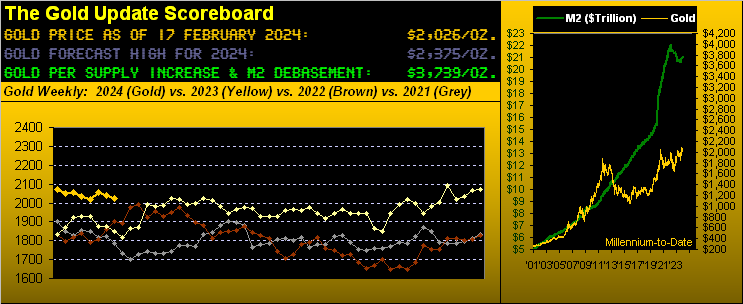

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro