“You say ‘lousy’, mmb? 75% of S&P companies have beaten estimates…“

Squire revels in playing this earnings game. Truth be told, only 56% of bottom lines have improved over a year ago, thus far making Q4 the sixth-worst S&P 500 Earnings Season of the past 27. Rising yields, a rising Dollar, scant earnings growth, and this Casino 500 sits at an all-time closing high (4959)? Ought we re-classify The Investing Age of Stoopid to that of Braindead?

But wait, there’s more: within several missives dating as far back as last mid-November, we’ve likened what we’ve been seeing in the Casino 500 to that which ultimately fed into the DotComBomb some two decades ago. And — late as they may be in figuring this out — major investment banks are (finally) seeing same. Hat-tip Bloomy for reporting last Tuesday that “JP Morgan Quants Warn of Dot-Com Style Concentration in US Stocks”, and then followed that yesterday with “BofA’s Hartnett Says Stock Markets Are Behaving Like Dot-Com Era”. Are the Big Banks at last actually doing the math?

The “live” price/earnings ratio of the Casino 500 is now 50.5x … and as we’ve previously noted, that is higher than ’twas at the outset of the DotComBomb, which high-to-low from 2000 into 2002 found the S&P “correct” more than -50% … just in case you’re scoring — or better yet preparing — at home. Because in reprising Bachman–Turner Overdrive from back in ’74: ![]() “You Ain’t Seen Nothing Yet”

“You Ain’t Seen Nothing Yet”![]()

‘Course, the “talk of the town” remains the so-called “Magnificent Seven”. Per yesterday’s settle, the combined market capitalization of: both Alphabet tranches, Apple, Amazon, Meta, Microsoft, Nvidia and Tesla represents 29.2% of the entire S&P 500. Their average P/E is now 46.5x (44.8x cap-weighted, were they in their own index of just seven companies). This is beyond lunacy by any historical measure.

Moreover as we’ve all along been wary, the annualized risk-free yield per yesterday’s settle on the three-month U.S. T-bill is 5.210%; that on the risk-all Casino 500 is 1.431%. (Further, as you regular readers well know, the market cap of the S&P is more than twice the readily available money supply to cover it … oops).

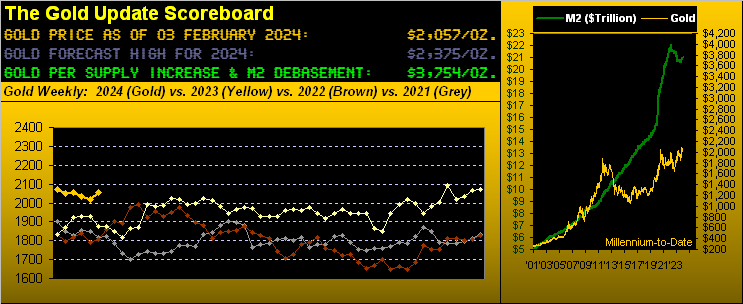

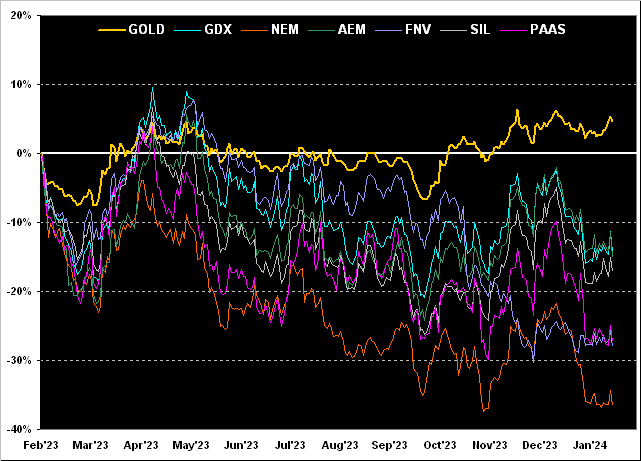

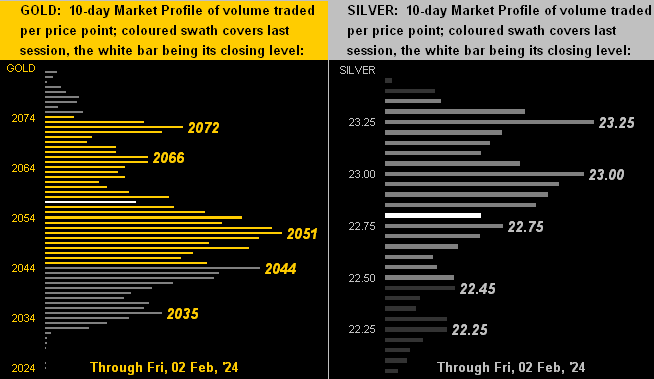

But back to Gold — the true hard asset currency dating at least as far back as Lydia’s King Croesus, circa 550 BC — ’tis time to bring up our year-over-year comparison of the yellow metal vis-à-vis its key equity brethren. So from worst to first we’ve: Newmont (NEM) -37%, Franco-Nevada (FNV) -28%, Pan American Silver (PAAS) -27%, the Global X Silver Miners exchange-traded fund (SIL) -17%, Agnico Eagle Mines (AEM) -15%, the VanEck Vectors Gold Miners exchange-traded fund (GDX) -14%, but Gold itself +5%. Does this mean the price of Gold (2057) is too high? Hardly, given our opening Gold Scoreboard’s valuation (3754). But in this goofball era of “The Magnificent Seven, or Nothing!”, the precious metals remain the wallflowers. It shan’t last; (it never has). Here’s the graphic:

The ensuing week appears underwhelming for the Econ Baro: just five metrics are due. But for Q4 Earnings Season, another 98 reports are scheduled for the S&P 500 as the Index’s insanity continues … or starts to come to its senses. On verra…

‘Course, nothing is more sensible than having a little Gold!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro