“Worst start to Earnings Season in memory, mmb?“

Across our 14 years of recording earnings, Squire, we’ve never seen a start worse than this. Rightly however, as we “tweeted” (@deMeadvillePro) this past Thursday: “This may be statistically insignificant as ’tis very, very early in Q4 Earnings Season.” And yet through the balance of the week, the poor trend continued. Specific to the S&P 500: 31 companies have thus far reported, of which just a scant nine (29%) bettered their bottom lines over Q4 of a year ago. In our records, that is worse than the S&P’s worst prior all-in quarter which registered only 36% having bettered for Q2 of COVID-plagued 2020.

And yet, the Casino 500 yesterday recorded its first all-time high (4842) since that on 04 January 2022 (4819). To again reprise the late, great Vince Lombardi: “What da hell’s goin’ on out dere?!?!?”

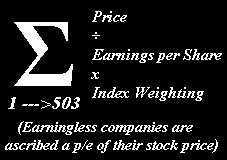

This really is becoming scary. One can be securely safe in U.S. Treasuries at triple the yield of S&P 500. But maybe that’s not considered fun. Surely it shan’t be fun should the stock market shut because the money doesn’t exist to fund folks’ stock sales. Today, obviously teaching Personal Finance at the undergraduate level is a waste of time. Remember our herein quoting Jerome B. Cohen: “In a bear market many stocks will sell at 5 to 7 times earnings, while in bull markets the average level would be about 15 to 18 times earnings.” As penned on the above Econ Baro, the “live” price/earnings ratio right now for the Casino 500 is 49.7x. If you don’t believe it, do something your broker can’t do … the math:

As for having to pass Portfolio Theory at the graduate level, forget about it: ’tis no longer needed given earnings no longer have meaning.

But wait, there’s more. Shame on you if not following the website’s S&P MoneyFlow page. And WOW did it whirl ’round this past week to upside. Here’s the problem: decade-to-date (the S&P’s closing span being from 3701 to now 4840) the average amount of money requisite to move the S&P up or down one point is $1,100,278 … as of yesterday the actual amount is a thin $540,068. That essentially means this “record-setting rally” is frothy and built on a lot of small trading block BS (can we print that, Mr. Editor?)

The point is: if you’re wedded to stocks, be wary to withstand having a hellova haircut. ‘Tis coming and ’twill be comprehensively butt-ugly. Or as we’ve on occasion quipped: “Market-to-market, everybody’s a millionaire; market-to-reality, they ain’t worth squat.” Write it down.

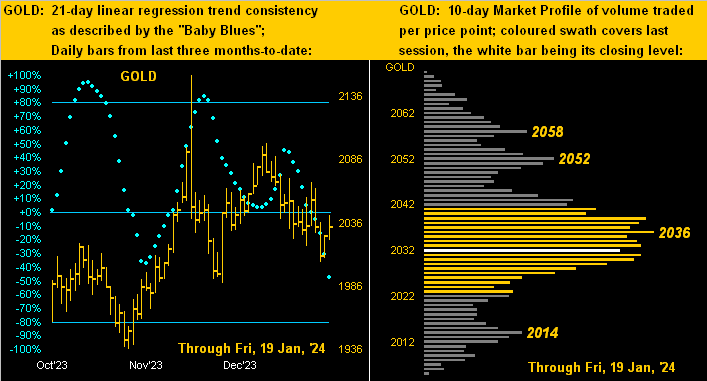

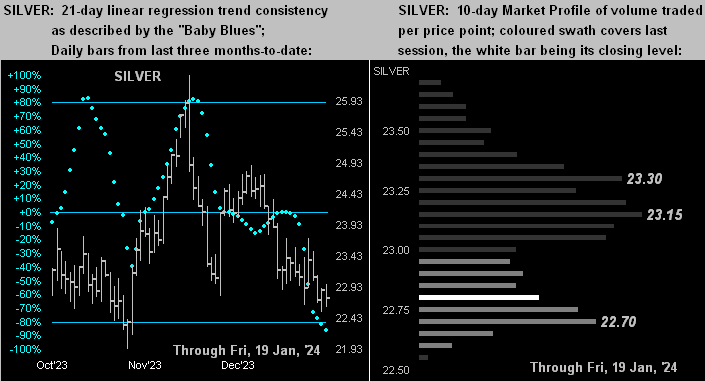

Meanwhile as cited, Gold’s price continues to be written down of late. In our two-panel graphic at left the old adage of “Follow the blues instead of the news, else lose your shoes” is in full cavort (but best not to go Short). Then at right, Gold’s 10-day Market Profile finds price rather clinging to the final bulge of support:

Before our final quip to close, let’s see what the Gold stack shows:

The Gold Stack

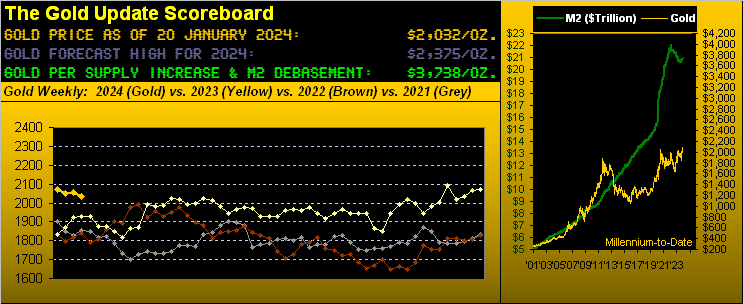

Gold’s Value per Dollar Debasement, (from our opening “Scoreboard”): 3738

Gold’s All-Time Intra-Day High: 2152 (04 December 2023)

Gold’s All-Time Closing High: 2092 (01 December 2023)

The 2000’s Triple-Top: 2089 (07 Aug ’20); 2079 (08 Mar ’22); 2085 (04 May ’23)

2024’s High: 2088 (02 January)

10-Session “volume-weighted” average price magnet: 2037

Trading Resistance: 2036 / 2052 / 2058

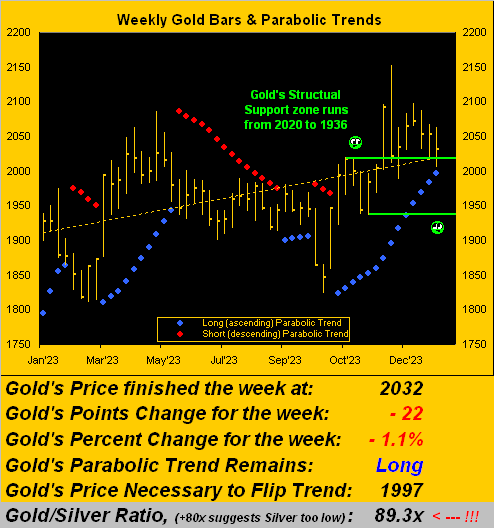

Gold Currently: 2032, (expected daily trading range [“EDTR”]: 26 points)

Trading Support: 2014

10-Session directional range: down to 2005 (from 2071) = -66 points or -3.2%

2024’s Low: 2005 (17 January)

The Weekly Parabolic Price to flip Short: 1997

The 300-Day Moving Average: 1937 and rising

The Gateway to 2000: 1900+

The Final Frontier: 1800-1900

The Northern Front: 1800-1750

On Maneuvers: 1750-1579

The Floor: 1579-1466

Le Sous-sol: Sub-1466

The Support Shelf: 1454-1434

Base Camp: 1377

The 1360s Double-Top: 1369 in Apr ’18 preceded by 1362 in Sep ’17

Neverland: The Whiny 1290s

The Box: 1280-1240

Indeed to close, let’s go to the Swiss snows at the WEF (World Elites’ Forum) wherein the “It Doesn’t Apply to Us Dept.” was in full folly, (as you may well have already heard). The “emphasis” of this year’s Davos boondoggle being “Climate Change” and “AI”, one John Forbes Kerry — THE U.S. Special Presidential Envoy for Climate (his having previously been both U.S. Secretary of State and U.S. Senator from The Commonwealth of Massachusetts, as well as having served in Viet Nam) — was media-queried in reference to the 1,000+ private jets having carbonized their way to either Zurich or St. Gallen-Altenrhein. The response: “That’s a stupid question”.

Which leads one to wonder what a Davos plat du jour was this year …

Avoid stoopid. Acquire Gold!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro