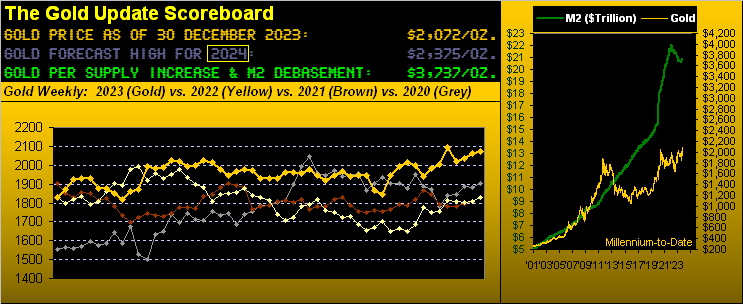

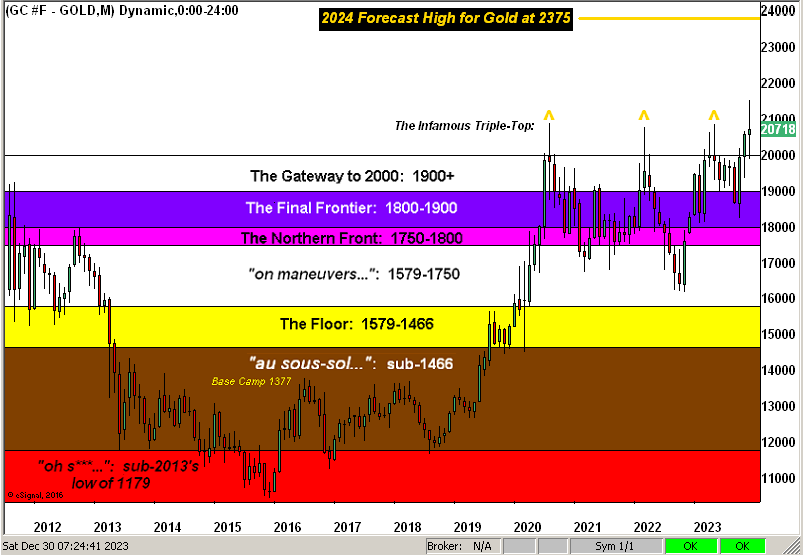

In transiting through New Year, one wonders how much longer the S&P 500 can withstand trading at nearly double its earnings valuation and Gold at nearly half of its currency debasement valuation. Ours indeed is to reason why — to seek reversion — for at some point it shall be nigh. And historically, ’tis always arrived.

But now for the present, ’tis time to imbibe! Thus from the entire deMeadville crew, a most Golden New Year to All of You!

Santé !

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro