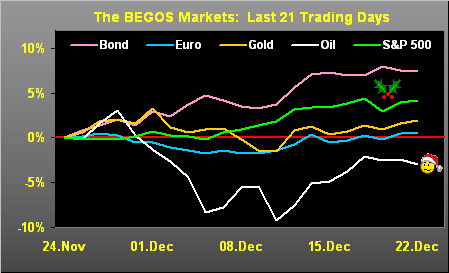

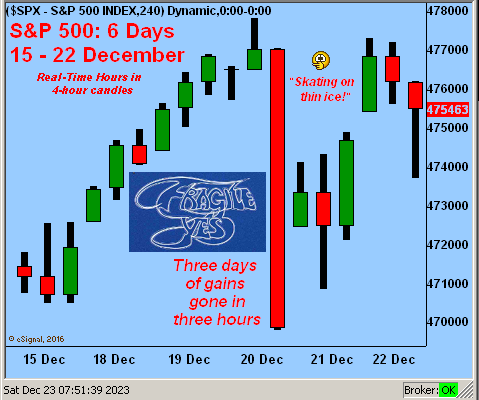

And therein note ole St. Nick pointing down at the top of the S&P. We’ve documented beyond ad nauseam the bazillion reasons for a major S&P correction, (e.g. “Stocks Suicide Mission” from just a week ago). Further, we witnessed on Wednesday (as tweeted @deMeadvillePro) a microcosm of how swiftly it can go. From Friday (15 December) into Wednesday (20 December) the S&P 500 garnered three successive days of “higher highs” … then late-session Wednesday, those three days of gains were gone in just three hours. Deeper into the numbers: the pace at which stocks hit downside bids was nine times the pace they’d previously been hitting upside offers. That is a fear-filled, comparatively monstrous downside pace. True, it didn’t last long, and the S&P then rather messily tried to recover to close its week. But it shows us just how thin is the ice on which the S&P is now skating. Or to cue the popular Yes album from back in ’71: ![]() “Fragile”

“Fragile”![]() Oh yes, indeed:

Oh yes, indeed:

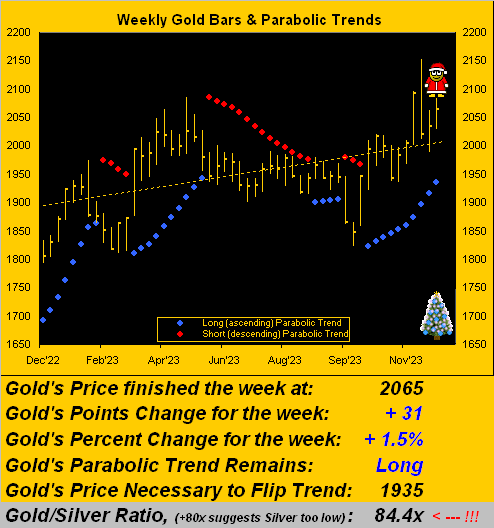

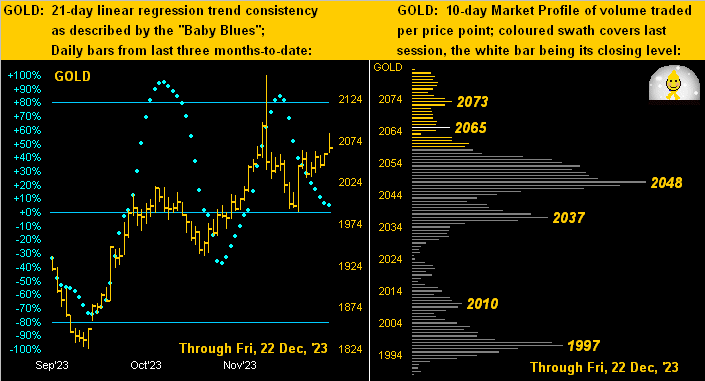

Thus there we are with but four trading days remaining in 2023. And as entitled, Gold’s pre-Chirstmas five-day gain at least by historical comparison is a great gift for the yellow metal going into next year. ‘Course, next week we’ll be here with our wrap for the year and as to how 2024 may well appear.

So with a tip of the cap to our IT crew for voluntarily creating this lovely card from us…

…as they say ’round these parts: “Joyeux Noël !” And give the gift of Gold!

Cheers!

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro