To close, per our aforementioned tease, here we go courtesy of the “Where Have You Been These Last Four Years? Dept.”

Regular readers know — and notably so since 2019 — we’ve been constantly concerned as to the overvalued state of equites, especially the S&P 500 Index as a whole. Oft we’ve quipped that we’re in “The Investing Age of Stoopid” purely by doing the honest math to compute the S&P’s price/earnings ratio, presently 37.7x as opposed to the parroted, dumbed-down 24.5x believed by your broker, (who frankly today appears incapable of doing the math). But that’s where we are now. And as we herein have written ad nauseum through these recent years: “…earnings are not supportive of price…”

Well here it comes… READY?

This past Wednesday the lightbulb finally illuminated in the children’s writing pool over at Barron’s, headlining their webpage “above the fold in bold” with:

“The Stock Market Has a Big Problem. It’s Called Earnings.”

They’re just figuring this out now???

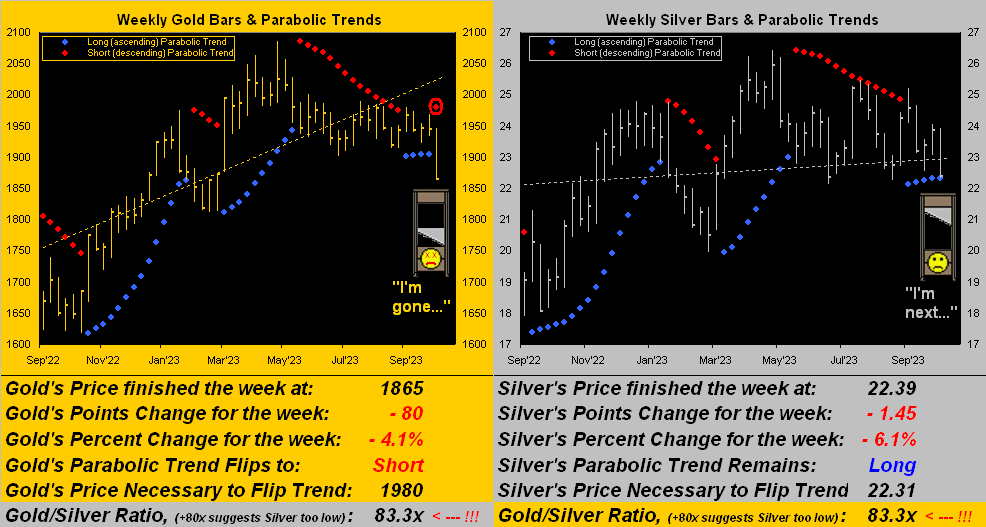

And yet when we view our MoneyFlow page for the S&P 500 — even during its current decline — true “fear” has yet to appear.

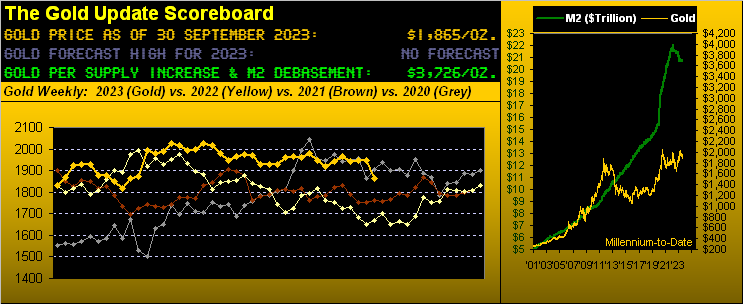

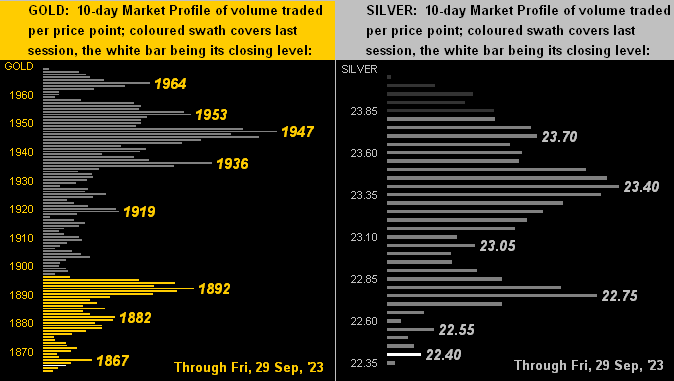

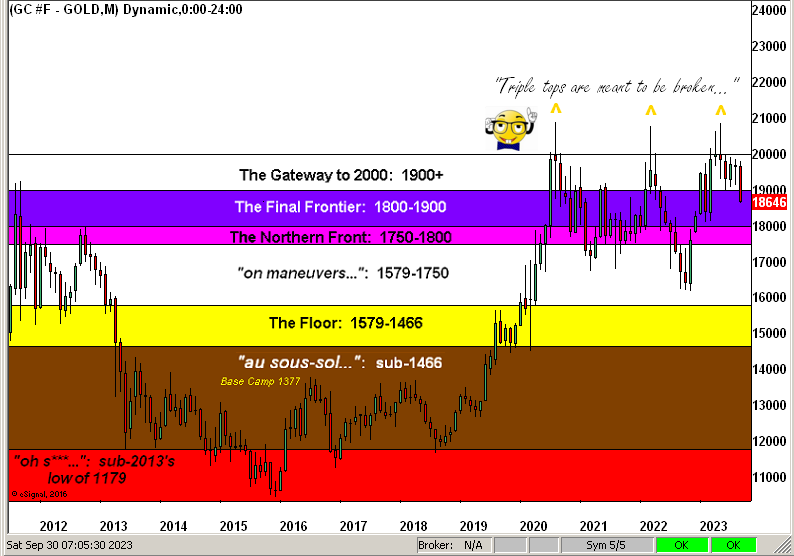

But what appears most appealing to us is Gold being priced today (1865) at just half its Dollar debasement value (3726) per our opening Gold Scoreboard.

Thus — precious metal guillotines and Dollar Revolution aside — in strolling along life’s path, what ought you have glowing in your vault? Gold!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro