‘Course, cash management has become a crap-shoot if investing via the StateSide trendless economy. “It’s up … no wait … it’s down … no wait … it’s ad nauseum…” Or as crooned by The Moody Blues: ![]() “School taught one and one is two. But by now, that answer just ain’t true…“

“School taught one and one is two. But by now, that answer just ain’t true…“ ![]() –[‘Ride My See-Saw’, ’68].

–[‘Ride My See-Saw’, ’68].

Too, there’s the standard verbage in the Policy Statements from the Federal Open Market Committee that it “will continue to monitor the implications of incoming information for the economic outlook”. Is it any wonder ongoing FedSpeak is so vague? Can you make heads or tails of it all? “In Search of the Lost Chord” indeed as we turn to the Economic Barometer:

Notwithstanding the precious metals needing a boost into the new week, we wrap this missive with “Breaking News”:

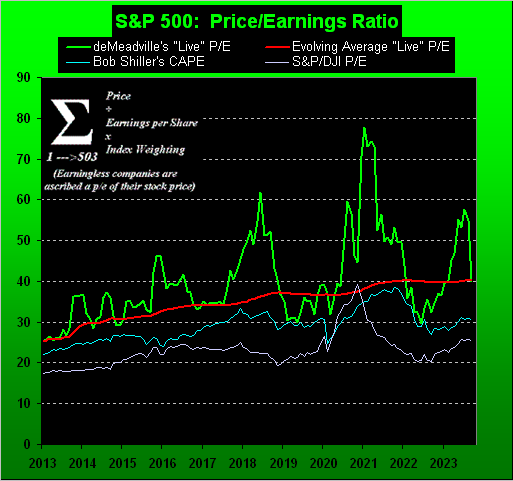

The long-sought reversion of our “live” price-earnings ratio to its mean has finally occurred. And both elements of the fraction thereto contributed. The “P” of the S&P 500 at 4457 is -7% below its all-time high (4819 on 04 January 2022). And the Index’s “E” — which for Q2 grew year-over-year by +6% — was recently enhanced by post-earnings season power profits, notably from the large market capitalization likes of Nvidia (NVDA) and Berkshire Hathaway (BRK.B). Indeed, those two companies by cap-weighting comprise 4.1% of the S&P 500’s total of 503 constituents. Here’s our enhanced graphic, the green line having once again reverted to the red line:

So is that as low as the S&P shall go? Per what we know: no. With our “live” P/E today at 39.9x, ’tis still a very strained distance above Bob Shiller’s CAPE, which in turn has yet to re-meet with the oft-parroted S&P/DJI version of “twenty-something”. And should the economy recess and earnings not grow, a return to the “live” P/E’s low (25.4x in January 2013) means an S&P “correction” from here of -36%; (that’d be to 2852, just in case you’re scoring at home … and recall our musing earlier this year of an S&P sub-3000). As well, the imputed S&P yield per the P/E ( 1 ÷ 39.9 ) is 2.507%; but the actual cap-weighted yield is only 1.537% … and yet the three-month annualized T-Bill yield is more than triple that at 5.293%, and ’tis risk-free! Thus you can see where your money ought be.

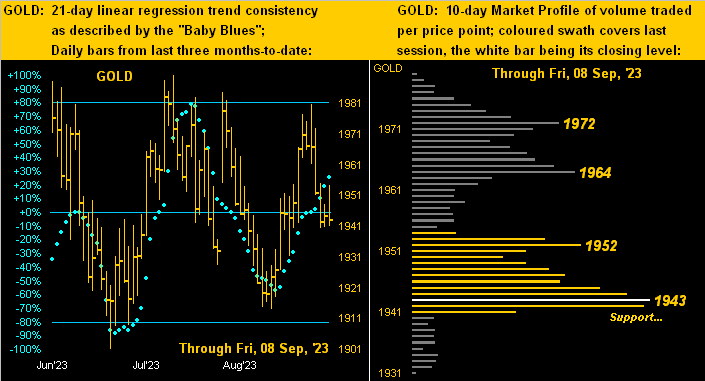

But for security above and beyond risk-free we’ve the world’s best currency: Gold! Today’s 1943 level prices it at just 52% of its Dollar debasement valuation, which per the opening Gold Scoreboard’s calculation of 3709 even accounts for the increase in the supply of Gold itself. And save for smart sovereigns, just because “nobody” owns Gold yet, do not be without! Got Yours?

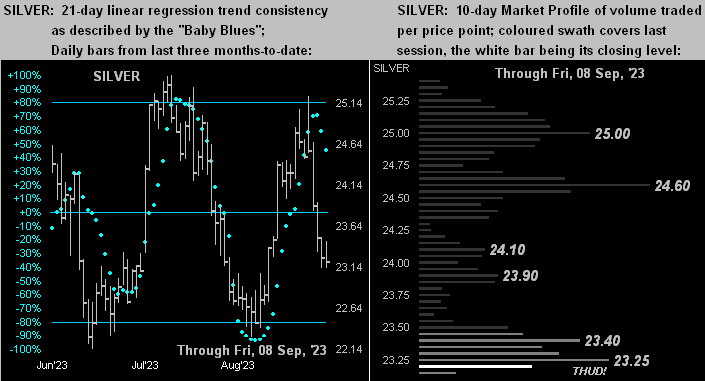

Never in a million years, Sweet Sister Silver!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on Twitter(“X”): @deMeadvillePro